Market Overview

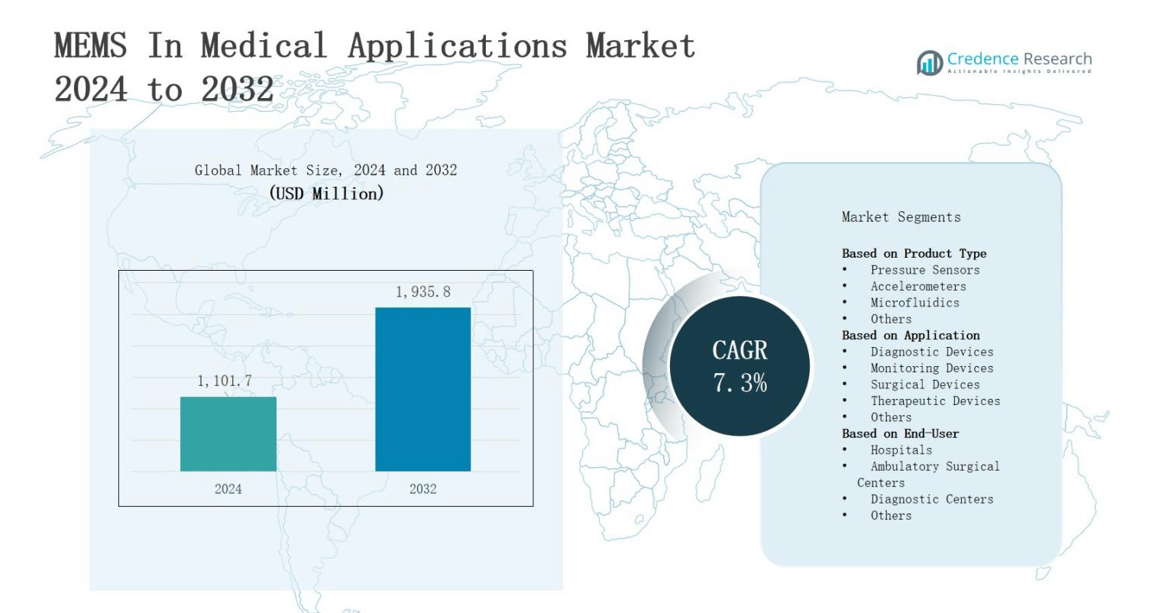

The MEMS in medical applications market is projected to grow from USD 1,101.7 million in 2024 to USD 1,935.8 million by 2032, registering a CAGR of 7.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Marine Autopilot Control Unit Market Size 2024 |

USD 1,101.7 million |

| Marine Autopilot Control Unit Market, CAGR |

7.3% |

| Marine Autopilot Control Unit Market Size 2032 |

USD 1,935.8 million |

The MEMS in medical applications market is driven by the increasing demand for miniaturized, high-precision medical devices, advancements in diagnostic and therapeutic technologies, and the growing adoption of remote patient monitoring solutions. Rising prevalence of chronic diseases and the need for minimally invasive procedures are accelerating integration of MEMS-based sensors and actuators in medical equipment. Trends include the development of wearable and implantable devices with enhanced functionality, adoption of wireless connectivity for real-time data transmission, and continuous innovations in bio-MEMS for lab-on-chip and point-of-care diagnostics, enabling faster, more accurate, and patient-centric healthcare solutions.

The MEMS in medical applications market is characterized by strong competition among global technology providers and medical device manufacturers focusing on innovation, quality, and regulatory compliance. It features established companies such as Abbott Laboratories, Boston Scientific Corporation, Medtronic plc, STMicroelectronics, Texas Instruments Incorporated, Analog Devices, Inc., Honeywell International Inc., General Electric Company, Philips Healthcare, Siemens Healthineers, Omron Corporation, and Teledyne Technologies Incorporated. These players invest heavily in R&D to enhance product performance, miniaturization, and integration with digital health platforms. Strategic collaborations with healthcare providers and research institutions accelerate product validation and market penetration. It leverages advancements in microfabrication, bio-MEMS, and wireless connectivity to deliver solutions for diagnostics, monitoring, surgical, and therapeutic applications. Companies compete on technological differentiation, cost efficiency, and the ability to meet stringent medical device regulations while expanding their geographic presence through partnerships, acquisitions, and localized manufacturing.

Market Insights

- The MEMS in medical applications market is projected to grow from USD 1,101.7 million in 2024 to USD 1,935.8 million by 2032, registering a CAGR of 7.3% during the forecast period.

- Rising demand for miniaturized, high-precision medical devices is driving adoption across portable monitoring systems, imaging equipment, and implantable devices.

- Increasing preference for minimally invasive surgical procedures boosts the use of MEMS-enabled instruments, improving procedural safety and patient recovery.

- Expanding use of wearable health monitors and remote patient management systems enhances preventive care and chronic disease management.

- Innovations in bio-MEMS, including lab-on-chip and microfluidics, enable faster diagnostics and targeted therapeutic delivery.

- High manufacturing costs, complex fabrication processes, and strict regulatory compliance requirements present challenges to market growth.

- North America holds 38% market share, followed by Europe at 28%, Asia-Pacific at 24%, and Rest of the World at 10%, reflecting diverse adoption drivers and healthcare infrastructure levels.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Miniaturized and High-Precision Medical Devices

The MEMS in medical applications market benefits from the growing requirement for compact, precise, and reliable components in modern healthcare devices. It supports enhanced diagnostic accuracy and therapeutic outcomes by enabling the integration of high-performance sensors and actuators. This demand is expanding across portable monitoring systems, imaging equipment, and implantable devices. Manufacturers invest heavily in microfabrication technologies to deliver advanced solutions. It meets the healthcare sector’s focus on accuracy, patient comfort, and operational efficiency.

- For instance, MEMS accelerometers are integrated into devices like pacemakers and insulin pumps, where their high precision and low power consumption provide reliable real-time monitoring and control.

Growing Adoption of Minimally Invasive Procedures

The MEMS in medical applications market gains momentum from the global shift toward minimally invasive surgical techniques. It facilitates smaller incisions, faster recovery, and reduced patient trauma by enabling high-precision surgical instruments and catheters. MEMS sensors improve navigation, control, and procedural safety. Surgeons increasingly rely on these devices for real-time data and feedback during complex interventions. It aligns with rising patient preference for procedures that reduce hospitalization and healthcare costs.

- For instance, Medtronic’s Hugo™ Robotic Assisted Surgery system employs pressure and movement sensors that enable surgeons to perform complex minimally invasive surgeries with greater precision and less trauma, resulting in faster patient recovery times.

Expansion of Remote Patient Monitoring and Wearable Devices

The MEMS in medical applications market experiences growth from expanding use of wearable health monitors and remote patient management systems. It enables continuous, accurate measurement of vital signs such as blood pressure, glucose levels, and respiratory rate. Integration with wireless communication enhances usability and data accessibility. Healthcare providers utilize these solutions to improve disease management and patient engagement. It supports preventive care strategies and reduces hospital readmission rates in chronic disease management.

Advancements in Bio-MEMS for Diagnostics and Therapeutics

The MEMS in medical applications market advances through innovations in bio-MEMS technologies for diagnostics, drug delivery, and lab-on-chip systems. It supports faster, more accurate point-of-care testing by integrating microfluidics and biosensors. These solutions enhance early disease detection and treatment planning. Researchers develop MEMS platforms capable of personalized therapeutic delivery. It strengthens the healthcare industry’s capability to provide targeted, efficient, and patient-centric care across diverse clinical applications.

Market Trends

Integration of Wireless Connectivity and IoT Capabilities

The MEMS in medical applications market is witnessing a strong trend toward embedding wireless communication and IoT integration into healthcare devices. It enables seamless real-time data transfer between patients and healthcare providers, improving monitoring efficiency and clinical decision-making. These advancements allow remote access to vital patient information, reducing the need for hospital visits. IoT-enabled MEMS devices support predictive analytics for early intervention. It strengthens connected healthcare ecosystems and enhances long-term patient care outcomes.

- For instance, MEMS biosensors integrated into wireless systems monitor ECG, blood pressure, and temperature, transmitting data via Bluetooth to smartphone apps and cloud databases for enhanced remote health management.

Development of Wearable and Implantable Health Monitoring Devices

The MEMS in medical applications market is progressing with the rapid evolution of wearable and implantable solutions for continuous health tracking. It drives the creation of compact, comfortable devices capable of monitoring key health parameters without disrupting daily activities. Manufacturers focus on extended battery life, precision sensing, and improved user experience. Such devices cater to patients managing chronic conditions. It aligns with growing demand for personalized healthcare and preventive treatment approaches worldwide.

- For instance, the Huawei Band 10, launched in February 2025, features advanced health monitoring such as sleep tracking, heart rate variability, and arrhythmia analysis, with a battery life of up to 14 days, combining precision sensing with user convenience.

Advancements in Microfluidics and Lab-on-Chip Technologies

The MEMS in medical applications market benefits from breakthroughs in microfluidics and lab-on-chip platforms for rapid diagnostics. It enables healthcare professionals to conduct multiple tests using minimal samples, improving speed and accuracy in disease detection. Lab-on-chip systems are becoming more cost-effective and scalable. These innovations support point-of-care testing in both clinical and remote settings. It improves diagnostic accessibility, particularly in regions with limited healthcare infrastructure and resources.

Focus on Energy-Efficient and Low-Power MEMS Designs

The MEMS in medical applications market is moving toward low-power, energy-efficient device architectures to support portable and implantable applications. It allows extended operational life without frequent battery replacements, which is vital for patient comfort and safety. Designers adopt innovative fabrication methods and advanced materials to reduce power consumption. These developments enhance device reliability and sustainability. It ensures continuous operation in critical care environments and strengthens trust in advanced medical technologies.

Market Challenges Analysis

High Manufacturing Costs and Complex Fabrication Processes

The MEMS in medical applications market faces challenges from the high costs and technical complexities involved in manufacturing. It requires precision microfabrication techniques, cleanroom environments, and advanced equipment, which increase production expenses. The integration of MEMS components with medical devices demands strict quality control and compliance with healthcare regulations. Smaller companies often struggle to meet these standards due to limited resources. It also faces scalability issues when transitioning from prototypes to mass production while maintaining reliability and performance.

Regulatory Compliance and Product Validation Barriers

The MEMS in medical applications market is constrained by stringent regulatory requirements and time-intensive validation processes. It must adhere to rigorous safety, efficacy, and biocompatibility standards before approval for clinical use. Navigating diverse regulatory frameworks across regions can delay product launches and increase operational costs. Frequent updates to medical device regulations require constant adaptation. It also encounters challenges in conducting long-term clinical testing, which is essential to ensure patient safety and secure market acceptance.

Market Opportunities

Expansion in Personalized and Preventive Healthcare Solutions

The MEMS in medical applications market holds strong opportunities in the growing adoption of personalized and preventive healthcare models. It enables continuous monitoring and early detection of medical conditions through wearable, implantable, and remote sensing devices. These technologies support tailored treatment plans based on individual health data. The demand for precision medicine is creating new application areas for bio-MEMS and lab-on-chip platforms. It aligns with healthcare systems prioritizing cost reduction, improved patient outcomes, and proactive disease management.

Emerging Demand in Telemedicine and Home Healthcare

The MEMS in medical applications market can capitalize on the rising need for advanced devices in telemedicine and home-based care. It offers solutions that facilitate real-time vital sign monitoring, remote diagnostics, and efficient chronic disease management. Growing investments in digital health infrastructure enhance the adoption potential of MEMS-based devices. These systems improve healthcare accessibility for aging populations and rural communities. It creates pathways for scalable, connected solutions that strengthen long-term patient engagement and care delivery.

Market Segmentation Analysis:

By Product Type

The MEMS in medical applications market is segmented into pressure sensors, accelerometers, microfluidics, and others. Pressure sensors hold a significant share due to their critical role in monitoring blood pressure, respiratory function, and intraocular pressure. Accelerometers are widely used in fall detection, motion analysis, and rehabilitation devices. Microfluidics supports advanced diagnostics through lab-on-chip solutions. It continues to gain traction in applications requiring precision fluid control, driving innovation in portable and point-of-care testing devices.

- For instance, CardioMEMS’ HeartSensor, a wireless device that non-surgically measures intracardiac pressure in congestive heart failure patients, allowing remote daily monitoring and early disease detection.

By Application

The MEMS in medical applications market covers diagnostic devices, monitoring devices, surgical devices, therapeutic devices, and others. Diagnostic devices dominate due to the rising need for early and accurate disease detection. Monitoring devices, such as wearable health trackers, are expanding with demand for remote patient management. Surgical devices leverage MEMS technology for enhanced precision and safety during procedures. It strengthens therapeutic devices by enabling targeted drug delivery systems and improving treatment efficiency across multiple medical disciplines.

- For instance, MEMS sensors integrated into surgical tools help improve the accuracy of minimally invasive surgeries.

By End-User

The MEMS in medical applications market is categorized into hospitals, ambulatory surgical centers, diagnostic centers, and others. Hospitals represent the largest segment, supported by high patient volumes and advanced equipment adoption. Ambulatory surgical centers benefit from the shift toward minimally invasive procedures requiring compact, high-performance devices. Diagnostic centers utilize MEMS technology for fast, accurate test results. It also serves emerging end-users such as home healthcare providers, expanding the reach of MEMS-enabled solutions in decentralized care models.

Segments:

Based on Product Type

- Pressure Sensors

- Accelerometers

- Microfluidics

- Others

Based on Application

- Diagnostic Devices

- Monitoring Devices

- Surgical Devices

- Therapeutic Devices

- Others

Based on End-User

- Hospitals

- Ambulatory Surgical Centers

- Diagnostic Centers

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

The MEMS in medical applications market in North America holds a 38% share, driven by advanced healthcare infrastructure, strong R&D investment, and early adoption of innovative medical technologies. It benefits from a high prevalence of chronic diseases that require continuous monitoring and precision diagnostics. Regulatory frameworks support the integration of MEMS-based solutions into clinical practice. The presence of leading medical device manufacturers and technology firms accelerates product innovation. It also gains momentum from increasing demand for telemedicine and home healthcare services. Strategic collaborations between healthcare providers and tech companies further enhance market penetration.

Europe

Europe accounts for 28% of the MEMS in medical applications market, supported by a well-established healthcare system and strong focus on quality care. It benefits from government-led initiatives to promote minimally invasive treatments and early disease detection. The region has a strong base of medical device manufacturers leveraging MEMS technologies for diagnostics, surgical tools, and therapeutic systems. Rising investments in wearable healthcare devices drive demand. It also responds to stringent regulatory standards that ensure safety and performance. Adoption is particularly strong in countries with high healthcare expenditure and robust innovation ecosystems.

Asia-Pacific

The MEMS in medical applications market in Asia-Pacific captures a 24% share, fueled by rapid urbanization, increasing healthcare spending, and expanding medical infrastructure. It benefits from a growing middle-class population seeking advanced healthcare solutions. Demand is rising for portable and affordable diagnostic devices, particularly in rural and underserved areas. Government investments in healthcare modernization support adoption. It also gains from a thriving electronics manufacturing sector that enables cost-effective MEMS production. Local startups and global companies actively collaborate to expand regional product availability.

Rest of the World

The Rest of the World holds a 10% share of the MEMS in medical applications market, with growth driven by improving healthcare access and technology adoption in Latin America, the Middle East, and Africa. It benefits from rising investments in hospital infrastructure and diagnostic facilities. Demand is increasing for mobile and point-of-care testing devices in remote areas. Partnerships with international device manufacturers facilitate technology transfer. It also responds to growing interest in wearable and connected healthcare solutions. Market penetration is expanding through public health initiatives and targeted medical programs.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Philips Healthcare

- Analog Devices, Inc.

- Medtronic plc

- Siemens Healthineers

- STMicroelectronics

- Omron Corporation

- Honeywell International Inc.

- Abbott Laboratories

- Teledyne Technologies Incorporated

- General Electric Company

- Texas Instruments Incorporated

- Boston Scientific Corporation

Competitive Analysis

The MEMS in medical applications market is characterized by strong competition among global technology providers and medical device manufacturers focusing on innovation, quality, and regulatory compliance. It features established companies such as Abbott Laboratories, Boston Scientific Corporation, Medtronic plc, STMicroelectronics, Texas Instruments Incorporated, Analog Devices, Inc., Honeywell International Inc., General Electric Company, Philips Healthcare, Siemens Healthineers, Omron Corporation, and Teledyne Technologies Incorporated. These players invest heavily in R&D to enhance product performance, miniaturization, and integration with digital health platforms. Strategic collaborations with healthcare providers and research institutions accelerate product validation and market penetration. It leverages advancements in microfabrication, bio-MEMS, and wireless connectivity to deliver solutions for diagnostics, monitoring, surgical, and therapeutic applications. Companies compete on technological differentiation, cost efficiency, and the ability to meet stringent medical device regulations while expanding their geographic presence through partnerships, acquisitions, and localized manufacturing.

Recent Developments

- On February 19, 2025, Millar announced the acquisition of Sentron, strengthening its MEMS sensor portfolio. This acquisition enables Millar to deliver end-to-end solutions in the design, fabrication, and manufacturing of precision sensors, including pressure, pH, electrical conductivity, and oxidation-reduction potential sensors, for medical, industrial, and environmental applications.

- On July 24, 2025, STMicroelectronics entered into an agreement to acquire NXP Semiconductors’ MEMS sensors business for up to USD 950 million, aiming to broaden its global sensor offerings across automotive, industrial, and medical markets.

- On January 15, 2025, Infineon Technologies launched an advanced MEMS-based ultrasound transducer, designed to expand applications in medical imaging, diagnostics, and industrial ultrasound sensing.

- At CES 2025 on January 28, 2025, USound introduced new in-ear MEMS speaker integrations featuring Audioplethysmography (APG) technology, enabling heart rate and vital sign monitoring through true wireless stereo earbuds.

Market Concentration & Characteristics

The MEMS in medical applications market exhibits a moderately concentrated structure, with a mix of global leaders and specialized niche players competing on technology, quality, and regulatory compliance. It is dominated by established companies with strong R&D capabilities, extensive product portfolios, and wide distribution networks, enabling them to maintain competitive advantage. Mid-sized and emerging firms focus on innovation in bio-MEMS, microfluidics, and low-power designs to capture specific application segments. It features high entry barriers due to complex manufacturing processes, stringent safety standards, and significant capital requirements. Competition centers on technological differentiation, integration with digital healthcare platforms, and ability to meet diverse regional regulations. Strategic alliances, mergers, and acquisitions are common to expand geographic reach and strengthen market positioning. It continues to evolve with advancements in wearable and implantable devices, increasing the pace of product development and commercialization in diagnostic, monitoring, surgical, and therapeutic applications.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for wearable and implantable MEMS-based devices will increase with the growth of personalized healthcare.

- Advancements in bio-MEMS will enhance capabilities in rapid diagnostics and targeted drug delivery.

- Integration of wireless connectivity will improve real-time patient monitoring and data sharing.

- Development of energy-efficient MEMS designs will support longer operational life in portable devices.

- Adoption of MEMS in minimally invasive surgical tools will expand across advanced healthcare facilities.

- Growth in telemedicine will drive demand for MEMS-enabled remote diagnostic solutions.

- Expansion of point-of-care testing will boost microfluidics-based MEMS adoption in underserved regions.

- Strategic collaborations between technology firms and healthcare providers will accelerate product innovation.

- Increasing automation in manufacturing will reduce production costs and improve scalability.

- Regulatory harmonization across key markets will facilitate faster product approvals and global deployment.