Market Overview

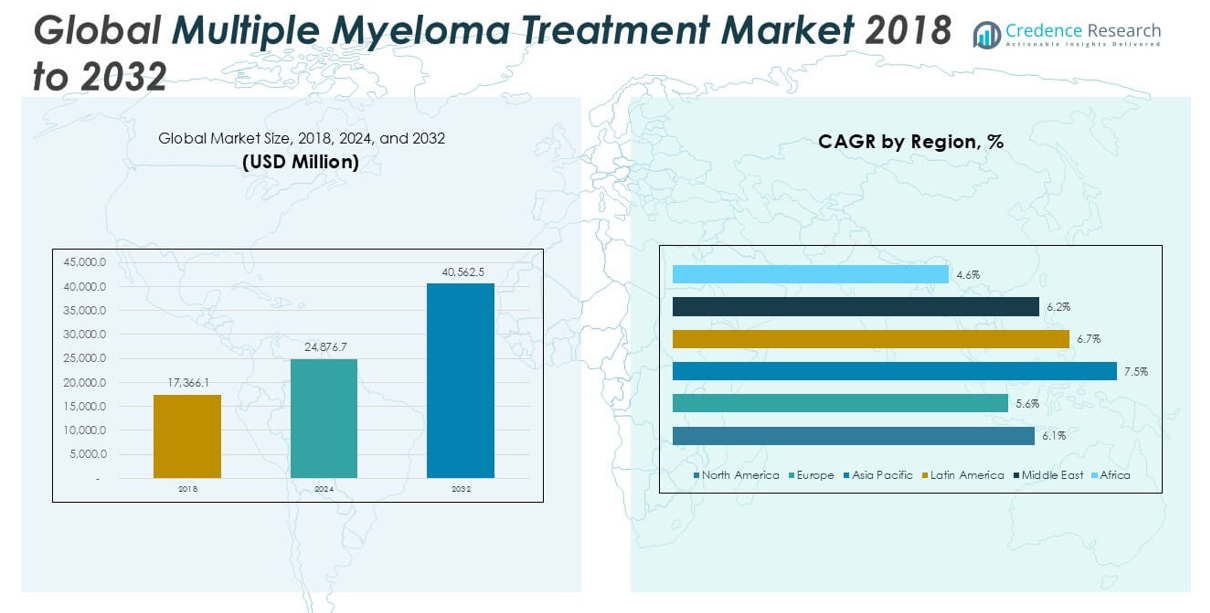

The Multiple Myeloma Treatment market size was valued at USD 17,366.1 million in 2018, increased to USD 24,876.7 million in 2024, and is anticipated to reach USD 40,562.5 million by 2032, growing at a CAGR of 6.33% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Multiple Myeloma Treatment Market Size 2024 |

USD 24,876.7 million |

| Multiple Myeloma Treatment Market, CAGR |

6.33% |

| Multiple Myeloma Treatment Market Size 2032 |

USD 40,562.5 million |

The Multiple Myeloma Treatment market is driven by key players such as Johnson & Johnson Services, Inc., Bristol-Myers Squibb Company, Novartis AG, Celgene Corporation, Amgen Inc., Merck KGaA, AbbVie, Inc., Sanofi S.A., Takeda Pharmaceutical Industries Ltd., and Kesios Therapeutics Limited. These companies maintain a competitive edge through extensive product portfolios, robust R&D investments, and strategic collaborations. North America leads the global market, capturing approximately 34.6% of the total share in 2024, supported by advanced healthcare infrastructure, high treatment adoption rates, and strong pharmaceutical presence. Europe follows as a significant contributor with a 24.0% market share, driven by growing patient awareness and supportive reimbursement policies. Asia Pacific, holding 21.6% of the market, is emerging as a fast-growing region due to improving healthcare access and increasing disease prevalence. The competitive landscape remains dynamic, with companies focusing on innovative therapies and expanding global reach.

Market Insights

- The Multiple Myeloma Treatment market was valued at USD 24,876.7 million in 2024 and is expected to reach USD 40,562.5 million by 2032, growing at a CAGR of 6.33% during the forecast period.

- Rising prevalence of multiple myeloma, growing elderly population, and increasing demand for advanced therapies are driving the market growth globally.

- The market is witnessing strong trends in the adoption of monoclonal antibodies and combination therapies, with drug therapy holding the largest segment share due to its high efficacy and patient preference.

- North America holds the largest regional market share at approximately 34.6%, followed by Europe at 24.0% and Asia Pacific at 21.6%, with Asia Pacific projected to grow rapidly due to improving healthcare infrastructure.

- High treatment costs, complex therapy regimens, and limited access to advanced care in developing regions are key restraints impacting market expansion.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

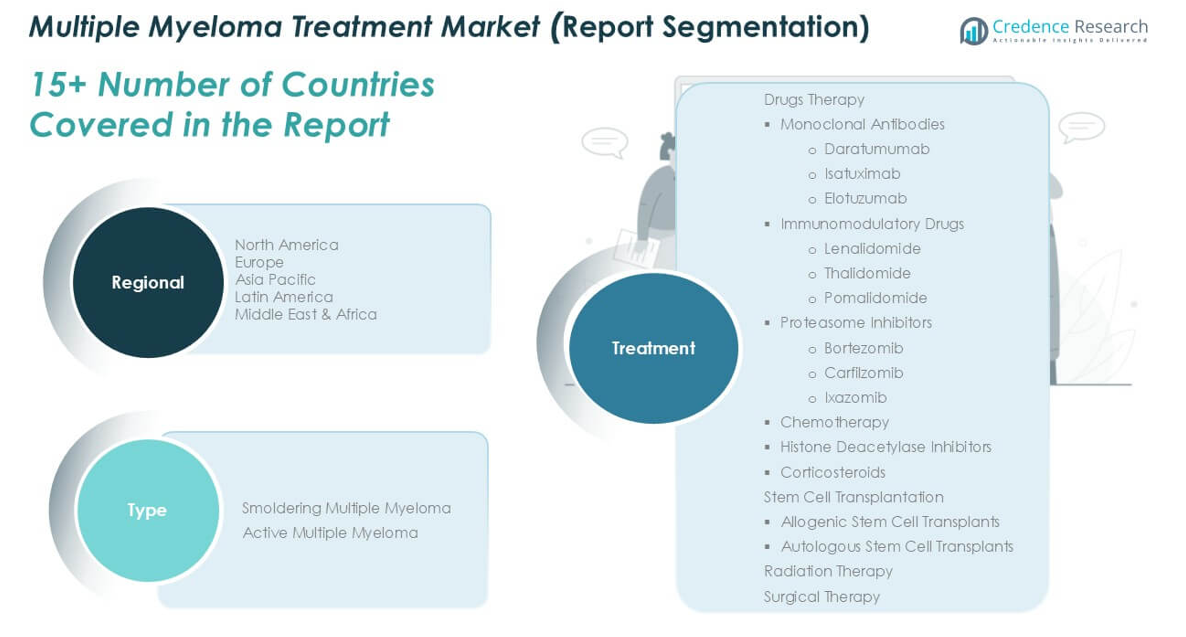

Market Segmentation Analysis:

By Myeloma Type:

The Multiple Myeloma Treatment market is segmented into Smoldering Multiple Myeloma and Active Multiple Myeloma. Among these, the Active Multiple Myeloma segment holds the dominant market share due to its higher diagnosis rates and immediate treatment requirements. The aggressive progression of active myeloma drives the demand for timely therapeutic interventions, including advanced drug therapies and stem cell transplants. In contrast, smoldering myeloma is typically asymptomatic and managed with observation, contributing to a smaller market share. Increasing awareness and improved diagnostic capabilities continue to support the expansion of the Active Multiple Myeloma segment.

- For instance, in a phase III trial, Bristol-Myers Squibb’s Pomalyst (pomalidomide) demonstrated a median progression-free survival of 11.2 months in relapsed and refractory multiple myeloma patients after at least two prior therapies.

By Treatment

Drug Therapy dominates the Multiple Myeloma Treatment market, accounting for the largest revenue share due to its effectiveness and the availability of a wide range of therapeutic agents. Within this segment, monoclonal antibodies, particularly Daratumumab, lead the market owing to their proven efficacy in improving survival rates and delaying disease progression. The rising adoption of immunomodulatory drugs like Lenalidomide and proteasome inhibitors such as Bortezomib further fuels growth. Beyond drug therapies, Stem Cell Transplantation is a significant segment, with Autologous Stem Cell Transplants holding the largest share due to their higher success rates and lower risk of rejection compared to allogenic transplants. Radiation Therapy and Surgical Therapy capture smaller portions of the market, primarily used in supportive or palliative care settings. Advances in transplantation techniques and broader eligibility criteria have expanded patient access to these treatments.

- For instance, the European Society for Blood and Marrow Transplantation (EBMT) reported that 16,145 autologous stem cell transplants were performed for multiple myeloma in Europe in 2021.

Market Overview

Increasing Prevalence of Multiple Myeloma

The rising global incidence of multiple myeloma significantly drives the market growth. Factors such as aging populations and improved diagnostic capabilities contribute to the increasing number of diagnosed cases. Early detection rates have improved due to the availability of advanced imaging and biomarker testing, leading to higher demand for treatment. As awareness about multiple myeloma grows among both healthcare providers and patients, the need for effective and accessible therapies continues to expand, fostering sustained growth in the treatment market.

- For instance, Siemens Healthineers’ Biograph Vision PET/CT system offers a time-of-flight resolution of 214 picoseconds and a spatial resolution of 3.5 millimeters, enabling clinicians to detect myeloma lesions smaller than 5 millimeters, significantly improving early-stage diagnosis accuracy.

Advancements in Drug Therapies

Continuous innovation in drug development is propelling the multiple myeloma treatment market forward. The emergence of monoclonal antibodies, immunomodulatory drugs, and proteasome inhibitors has revolutionized treatment protocols, improving patient outcomes and survival rates. Pharmaceutical companies are focusing on developing combination therapies and next-generation biologics, offering more targeted and less toxic options. Regulatory bodies are also fast-tracking approvals for promising therapies, accelerating market penetration. These advancements collectively enhance treatment efficacy and broaden therapeutic options, supporting steady market expansion.

- For instance, in the CANDOR phase III trial, Amgen’s Kyprolis (carfilzomib) combined with dexamethasone and Darzalex achieved a median progression-free survival of 28.6 months in patients with relapsed multiple myeloma, compared to 15.2 months in patients receiving Kyprolis and dexamethasone alone.

Expansion of Stem Cell Transplant Procedures

The increasing acceptance and availability of stem cell transplantation, especially autologous transplants, serve as a major growth driver for the market. Advances in transplantation techniques, supportive care, and conditioning regimens have improved patient eligibility and post-transplant outcomes. Growing investment in healthcare infrastructure, particularly in developing regions, is facilitating wider access to transplant facilities. The combination of stem cell transplants with novel drug therapies is becoming a standard approach, further driving the demand for comprehensive multiple myeloma treatment solutions.

Key Trends & Opportunities

Growing Focus on Personalized Medicine

The shift towards personalized medicine presents a significant opportunity in the multiple myeloma treatment market. Tailoring therapies based on genetic profiling and patient-specific disease characteristics is gaining traction. This approach enhances treatment efficacy while minimizing adverse effects, offering a more targeted and efficient therapeutic pathway. Pharmaceutical companies are increasingly investing in precision medicine research, aiming to develop biomarker-driven treatment regimens. The integration of genetic diagnostics and individualized care strategies is expected to reshape the treatment landscape and create substantial growth opportunities.

- For instance, the Multiple Myeloma Research Foundation’s (MMRF) CoMMpass Study has genomically profiled 1,144 patients to date, with longitudinal follow-up, providing a robust dataset that identified over 27 unique genetic alterations, enabling targeted therapeutic selection based on precise molecular characteristics.

Increasing Adoption of Combination Therapies

The trend towards combination therapies is reshaping multiple myeloma treatment strategies. Combining proteasome inhibitors, immunomodulatory drugs, and monoclonal antibodies has demonstrated superior efficacy compared to single-agent regimens. These multi-drug protocols are extending progression-free survival and improving overall patient outcomes. The growing body of clinical evidence supporting combination treatments is encouraging regulatory approvals and influencing treatment guidelines worldwide. As research continues to explore new synergistic combinations, this trend is set to drive market growth and expand therapeutic options.

- For instance, in the GRIFFIN Phase II trial, the combination of Johnson & Johnson’s Darzalex (daratumumab), Celgene’s Revlimid (lenalidomide), Velcade (bortezomib), and dexamethasone achieved stringent complete response in 42 out of 99 patients after consolidation therapy, compared to 22 out of 102 patients in the non-daratumumab group.

Key Challenges

High Cost of Treatment

One of the primary challenges in the multiple myeloma treatment market is the high cost associated with advanced therapies and stem cell transplantation. Monoclonal antibodies, immunomodulators, and novel biologics are expensive, placing a considerable financial burden on healthcare systems and patients. Limited affordability and insufficient reimbursement in some regions restrict access to optimal treatments, particularly in developing countries. These cost-related barriers can lead to delayed or substandard care, impeding the broader adoption of innovative therapies despite their clinical benefits.

Complex Treatment Regimens and Side Effects

Multiple myeloma treatment often involves complex, long-term therapy regimens that can be physically and emotionally taxing for patients. Side effects such as neuropathy, infections, and bone complications are common, which may reduce treatment adherence and quality of life. Managing these adverse effects requires multidisciplinary care and careful monitoring, adding complexity to treatment delivery. The need for continuous adjustments in drug combinations and doses further complicates patient management, presenting a significant challenge for healthcare providers and affecting treatment outcomes.

Limited Curative Options

Despite therapeutic advancements, multiple myeloma remains largely incurable, with most patients eventually experiencing relapse or disease progression. While new drug classes and combination therapies have extended survival rates, achieving long-term remission remains challenging. The development of resistance to current treatments and limited availability of curative options hinder the goal of sustained disease control. This persistent gap highlights the ongoing need for breakthrough therapies and curative strategies, which remain a significant challenge in the multiple myeloma treatment landscape.

Regional Analysis

North America

North America dominated the Multiple Myeloma Treatment market in 2024, holding the largest market share of approximately 34.6%, up from USD 6,097.24 million in 2018 to USD 8,615.86 million in 2024, and is projected to reach USD 13,791.24 million by 2032 at a CAGR of 6.1%. The region’s growth is driven by advanced healthcare infrastructure, rapid adoption of novel therapies, and increasing awareness. The high prevalence of multiple myeloma and the presence of major pharmaceutical companies contribute significantly to North America’s leading position in the global market.

Europe

Europe accounted for around 24.0% of the global Multiple Myeloma Treatment market share in 2024, growing from USD 4,322.42 million in 2018 to USD 5,966.85 million in 2024, and is expected to reach USD 9,240.13 million by 2032, registering a CAGR of 5.6%. The market growth in Europe is supported by strong government healthcare systems, rising elderly population, and increasing adoption of innovative treatment protocols. Additionally, ongoing clinical trials and favorable reimbursement policies are enhancing access to advanced therapies, solidifying Europe’s position as a key contributor to global market expansion.

Asia Pacific

Asia Pacific emerged as one of the fastest-growing regions in the Multiple Myeloma Treatment market, holding a 21.6% market share in 2024. The market size rose from USD 3,501.01 million in 2018 to USD 5,375.49 million in 2024, and is projected to reach USD 9,548.41 million by 2032, expanding at a robust CAGR of 7.5%. Rapid healthcare infrastructure development, increasing patient awareness, and rising prevalence of multiple myeloma are key growth drivers in the region. Additionally, growing investments by pharmaceutical companies and improving access to modern therapies further accelerate market growth in Asia Pacific.

Latin America

In 2024, Latin America held approximately 10.7% of the global Multiple Myeloma Treatment market share. The market expanded from USD 1,826.91 million in 2018 to USD 2,668.20 million in 2024, and is anticipated to reach USD 4,461.87 million by 2032, growing at a CAGR of 6.7%. Increasing healthcare expenditure, improved access to diagnostic services, and the gradual availability of novel therapies are driving growth in the region. Countries like Brazil and Mexico are key contributors, with improving cancer care facilities and supportive government initiatives enhancing the treatment landscape across Latin America.

Middle East

The Middle East accounted for around 6.6% of the Multiple Myeloma Treatment market share in 2024. The regional market grew from USD 1,163.53 million in 2018 to USD 1,651.81 million in 2024, and is projected to reach USD 2,660.90 million by 2032, expanding at a CAGR of 6.2%. Growth in the Middle East is supported by increasing investments in healthcare infrastructure, rising awareness, and the gradual introduction of advanced treatment options. Expanding healthcare accessibility in Gulf countries and the growing focus on specialized cancer care centers contribute to the steady growth of this market.

Africa

Africa represented a smaller but steadily growing segment in the Multiple Myeloma Treatment market, holding a 2.4% market share in 2024. The market value increased from USD 454.99 million in 2018 to USD 598.46 million in 2024, and is expected to reach USD 859.92 million by 2032, registering a CAGR of 4.6%. Market growth is driven by improving healthcare access, increasing cancer awareness, and growing international support for healthcare advancements. However, limited treatment accessibility, high costs, and underdeveloped healthcare infrastructure continue to challenge market expansion in many parts of the African continent.

Market Segmentations:

By Myeloma Type:

- Smoldering Multiple Myeloma

- Active Multiple Myeloma

By Treatment:

- Drugs Therapy

- Monoclonal Antibodies

- Daratumumab

- Isatuximab

- Elotuzumab

- Immunomodulatory Drugs

- Lenalidomide

- Thalidomide

- Pomalidomide

- Proteasome Inhibitors

- Bortezomib

- Carfilzomib

- Ixazomib

- Chemotherapy

- Histone Deacetylase Inhibitors

- Corticosteroids

- Stem Cell Transplantation

- Allogenic Stem Cell Transplants

- Autologous Stem Cell Transplants

- Radiation Therapy

- Surgical Therapy

By Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Multiple Myeloma Treatment market is highly competitive and characterized by the presence of several global pharmaceutical giants and emerging biotechnology firms. Key players such as Johnson & Johnson Services, Inc., Bristol-Myers Squibb Company, Novartis AG, Amgen Inc., and Takeda Pharmaceutical Industries Ltd. dominate the market through extensive product portfolios and strong research and development pipelines. These companies focus on continuous innovation, strategic partnerships, and acquisitions to strengthen their market positions and expand their treatment offerings. The market also witnesses significant contributions from emerging players like Kesios Therapeutics Limited and Xencor, Inc., which are actively involved in clinical trials and novel drug development. Competition is further intensified by the increasing adoption of combination therapies, the introduction of biosimilars, and the growing emphasis on personalized medicine. Additionally, regulatory approvals for advanced monoclonal antibodies and immunotherapies continue to shape the competitive dynamics, with companies striving to differentiate themselves through improved efficacy and patient outcomes.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Johnson & Johnson Services, Inc.

- Bristol-Myers Squibb Company

- Novartis AG

- Celgene Corporation

- Amgen Inc.

- Merck KGaA

- AbbVie, Inc.

- Sanofi S.A.

- Takeda Pharmaceutical Industries Ltd.

- Kesios Therapeutics Limited

Recent Developments

- In October 2024, Novartis discontinued its autologous BCMA-targeting CAR-T project (durcabtagene autoleucel, PHE885) for multiple myeloma, citing the rapidly evolving treatment landscape.

- In June 2024, Merck KGaA announced plans to advance its oncology pipeline by initiating Phase Ib and II clinical studies for several novel drug candidates. These include the DNA damage response (DDR) inhibitors tuvusertib and M9466, as well as advanced antibody-drug conjugates (ADCs) M9140 and M3554.

- In April 2024, Johnson & Johnson’s CARVYKTI® (ciltacabtagene autoleucel) received approval from the European Medicines Agency (EMA) for adults with relapsed or refractory multiple myeloma who have received at least one prior therapy. The approval was based on data from the CARTITUDE-4 trial, showing deep and sustained minimal residual disease (MRD)negativity rates, with 86% of evaluable patients achieving MRD negativity at six months.

- In December 2023, Amgen highlighted continued development of KYPROLIS® (carfilzomib) as a key treatment for relapsed/refractory multiple myeloma, with new data presented at ASH 2023.

Market Concentration & Characteristics

The Multiple Myeloma Treatment Market demonstrates moderate to high concentration, dominated by a few major pharmaceutical companies with strong global reach and extensive product portfolios. Key players focus on continuous product innovation, strategic acquisitions, and clinical advancements to maintain their competitive positions. It features a strong emphasis on drug therapies, particularly monoclonal antibodies, immunomodulatory drugs, and proteasome inhibitors, which collectively account for the largest revenue share. The market is characterized by high research intensity, frequent product launches, and robust regulatory activity. Companies invest heavily in combination therapies to improve treatment outcomes and extend patient survival rates. It shows a growing shift toward personalized medicine, where genetic profiling increasingly guides treatment selection. Access to advanced therapies remains concentrated in developed regions, while emerging markets experience slower adoption due to limited healthcare infrastructure and high treatment costs. Pricing pressure and patent expirations present ongoing challenges, driving companies to pursue new drug development and strategic collaborations. The market remains highly responsive to regulatory approvals and new clinical guidelines that shape treatment practices and patient access globally.

Report Coverage

The research report offers an in-depth analysis based on Myeloma Type, Treatment and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The demand for targeted therapies is expected to grow due to their improved efficacy and reduced side effects.

- Monoclonal antibodies will continue to gain significant traction in treatment protocols.

- The adoption of combination therapies is projected to increase across major healthcare systems.

- Stem cell transplantation procedures will see steady growth with expanding patient eligibility.

- Asia Pacific markets will experience faster growth supported by improving healthcare infrastructure.

- Key players are likely to focus on expanding their drug pipelines through clinical research and innovation.

- Personalized medicine approaches will become more prominent in treatment strategies.

- The introduction of biosimilars is expected to create competitive pricing pressures in the market.

- Advances in diagnostic technologies will support earlier detection and timely intervention.

- Strategic collaborations and mergers among pharmaceutical companies will strengthen market presence and global reach.