Market Overview:

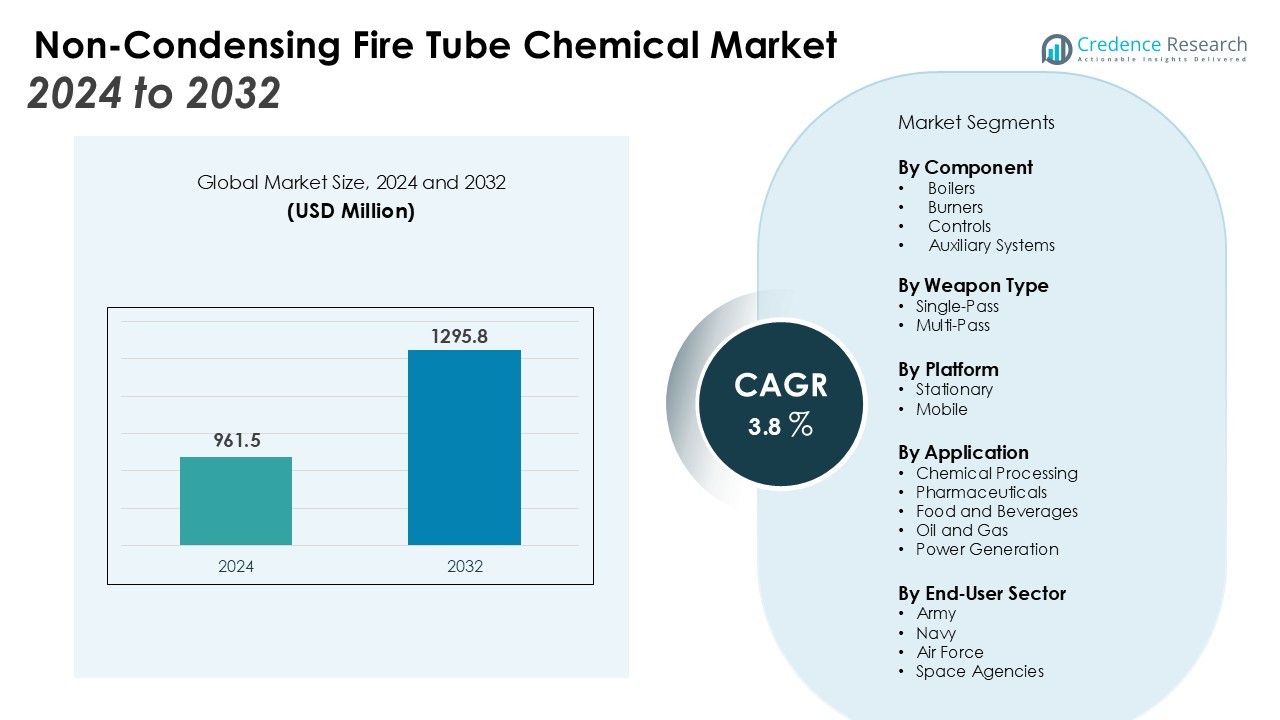

The Non-Condensing Fire Tube Chemical Market size was valued at USD 961.5 million in 2024 and is anticipated to reach USD 1295.8 million by 2032, at a CAGR of 3.8% during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Non-Condensing Fire Tube Chemical Market Size 2024 |

USD 961.5 Million |

| Non-Condensing Fire Tube Chemical Market, CAGR |

3.8% |

| Non-Condensing Fire Tube Chemical Market Size 2032 |

USD 1295.8 Million |

Market growth is primarily fueled by rising demand for energy-efficient thermal systems in chemical processing and manufacturing industries. Non-condensing fire tube boilers provide durability, simpler operation, and lower upfront investment compared to condensing alternatives, making them favorable for industrial buyers. In addition, stricter safety standards and modernization of older boiler systems are encouraging industries to invest in advanced fire tube solutions with improved efficiency and operational safety.

Regionally, North America holds a significant share of the Non-Condensing Fire Tube Chemical Market, supported by established chemical manufacturing infrastructure and ongoing modernization projects. Europe follows closely due to stricter emission norms and strong focus on equipment reliability across industries. The Asia Pacific region is expected to record the fastest growth, led by rapid industrial expansion in China, India, and Southeast Asia, where chemical and processing plants are increasing their adoption of cost-effective and reliable heating systems. Rising government investments in industrial energy infrastructure are further boosting market expansion across emerging economies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Non-Condensing Fire Tube Chemical Market is valued at USD 961.5 million and projected to reach USD 1295.8 million by 2032, registering a CAGR of 3.8%.

- Demand is strongly driven by energy-efficient and reliable thermal systems required in chemical and manufacturing sectors.

- Cost-effectiveness and lower upfront investment make non-condensing fire tube boilers attractive in price-sensitive markets.

- Compliance with stricter safety regulations and modernization of older systems is fueling market adoption.

- North America holds 32% share, followed by Europe at 27%, supported by industrial modernization and regulatory frameworks.

- Asia Pacific accounts for 29% share and is the fastest-growing region, driven by rapid industrial expansion in China, India, and Southeast Asia.

- The Middle East holds 7% share, while Latin America records 5%, both benefiting from petrochemical growth and infrastructure development.

Market Drivers:

Rising Demand for Energy-Efficient and Reliable Thermal Systems

The Non-Condensing Fire Tube Chemical Market is expanding due to rising demand for energy-efficient and reliable thermal solutions. Chemical processing industries require stable and consistent heat supply, making these systems an attractive choice. Non-condensing fire tube boilers offer strong durability and lower operating complexities compared to condensing alternatives. Their ability to deliver high performance at competitive costs strengthens their position in industrial adoption.

Cost-Effectiveness and Lower Initial Investment

Non-condensing fire tube boilers hold an advantage in cost-effectiveness, which is a critical factor for buyers in chemical and manufacturing sectors. They require lower initial investment compared to advanced condensing systems, making them appealing for facilities aiming to modernize without high capital costs. It also reduces maintenance expenses, supporting long-term savings. This financial practicality continues to drive strong uptake in price-sensitive markets.

- For instance, the Fulton Thermal Corporation ICS 50 non-condensing fire tube boiler delivers 1,992,000 BTU input capacity with a compact design, providing a cost-effective steam solution with a lower initial investment compared to more complex condensing boilers.

Compliance with Safety Regulations and Industry Standards

Stringent safety regulations are shaping the market by encouraging industries to adopt advanced and compliant systems. Non-condensing fire tube boilers are being modernized to align with updated safety and operational standards, enhancing their reliability. It ensures safe handling of high-pressure processes commonly found in chemical industries. Regulatory compliance strengthens buyer confidence and supports wider adoption across key regions.

Industrial Expansion and Modernization Programs

Growing industrial expansion across global markets is driving steady demand for thermal systems. The Non-Condensing Fire Tube Chemical Market benefits from modernization programs that replace outdated boilers with efficient fire tube designs. It addresses both operational performance and sustainability goals of industrial operators. Expanding infrastructure in Asia Pacific and the Middle East continues to create growth opportunities for manufacturers in this sector.

- For instance, John Zink’s Coen Burner Division has modernized boilers to achieve low NOx emissions as low as 0.12 lbs per million BTU, significantly enhancing combustion efficiency and reducing maintenance costs in industrial applications.

Market Trends:

Growing Integration of Automation and Digital Monitoring Technologies

Automation and digital monitoring are becoming central trends in the Non-Condensing Fire Tube Chemical Market. Industries are adopting advanced control systems that enable real-time monitoring of boiler performance, fuel usage, and safety compliance. It helps operators optimize efficiency, reduce downtime, and extend equipment life through predictive maintenance features. Smart sensors and IoT-enabled solutions are also enhancing operational transparency, ensuring industries maintain consistent output quality. Digitalization supports regulatory compliance by providing accurate reporting and data-driven decision-making. These advancements are aligning with broader industrial automation strategies and creating long-term value for chemical manufacturers.

- For instance, Cleaver-Brooks’ Prometha IoT solution collects at least 250 data points on each monitored boiler asset 10 times per minute, providing actionable insights that help reduce unplanned downtime and improve efficiency.

Increasing Focus on Sustainability and Replacement of Aging Infrastructure

The market is also witnessing a clear trend toward sustainability and replacement of outdated systems. Industries are focusing on upgrading older fire tube boilers with newer models that reduce fuel consumption and emissions while maintaining operational reliability. It reflects the growing emphasis on reducing environmental impact without compromising cost-effectiveness. Governments and industries in regions such as Asia Pacific are investing heavily in modernization projects, driving wider adoption of non-condensing fire tube boilers. Energy-intensive sectors are prioritizing solutions that balance performance with sustainability commitments. This shift is expanding opportunities for manufacturers to deliver robust and compliant systems that meet both operational and environmental expectations.

- For instance, BASF’s Durham facility eliminated energy losses from fire tube boiler back walls, saving over $25,000 annually by replacing aging boilers with more efficient watertube designs.

Market Challenges Analysis:

High Operating Costs and Efficiency Limitations

The Non-Condensing Fire Tube Chemical Market faces challenges due to higher fuel consumption compared to condensing systems. Non-condensing boilers release a portion of heat through exhaust, reducing overall efficiency and increasing operating costs. It places pressure on industries that are under growing demand to control expenses and improve energy performance. Rising fuel prices intensify this concern, limiting wider adoption among cost-sensitive buyers. The efficiency gap also makes it harder for these systems to compete against advanced condensing technologies that provide stronger returns over the long term.

Compliance Pressures and Intense Competitive Landscape

Tightening environmental regulations present another barrier for the Non-Condensing Fire Tube Chemical Market. Non-condensing boilers are often less favored in regions with strict emission standards, pushing industries toward alternatives. It restricts market penetration in advanced economies where compliance costs are rising. Competition from condensing fire tube systems and other energy-efficient technologies also challenges growth opportunities. Manufacturers face pressure to innovate while maintaining cost competitiveness, which creates significant strain on profit margins. This competitive and regulatory environment remains a critical challenge for industry players.

Market Opportunities:

Expansion in Emerging Industrial Markets

The Non-Condensing Fire Tube Chemical Market holds strong opportunities in emerging industrial regions. Rapid industrialization in Asia Pacific, Latin America, and the Middle East is creating higher demand for reliable and affordable thermal systems. It offers significant potential for manufacturers to serve industries that require cost-effective solutions without complex infrastructure. Chemical, pharmaceutical, and processing sectors in these regions are prioritizing systems with proven durability and lower upfront costs. Local government investments in industrial infrastructure also enhance adoption rates. Expanding production facilities and modernization programs across these economies provide a strong platform for long-term market growth.

Technological Advancements and Product Innovation

Opportunities are also emerging through advancements in product design and technology integration. The Non-Condensing Fire Tube Chemical Market is seeing innovations that enhance efficiency, reduce emissions, and extend service life. It allows manufacturers to deliver systems that meet both regulatory standards and operational needs. Integration of smart monitoring, automation, and IoT-based controls further increases the appeal of these boilers for modern plants. Companies focusing on hybrid solutions or retrofitting options are well-positioned to capture evolving customer demand. Continuous innovation in this segment is expected to create a competitive edge and expand market penetration across multiple industries.

Market Segmentation Analysis:

By Component

The Non-Condensing Fire Tube Chemical Market is segmented by component into boilers, burners, controls, and auxiliary systems. Boilers account for the largest share, driven by their critical role in generating stable heat supply for chemical processing. It continues to see demand due to strong durability and simpler operation compared to condensing alternatives. Burners and control systems are also gaining traction as industries focus on efficiency and safety compliance. Auxiliary systems support operational reliability and are increasingly integrated with automated monitoring features.

- For instance, Cleaver-Brooks’ CBLE firetube boiler offers steam capacity up to 300 psig, providing robust and reliable operation suited for chemical processing environments.

By Weapon Type

In the Non-Condensing Fire Tube Chemical Market, segmentation by weapon type includes single-pass and multi-pass designs. Multi-pass fire tube boilers dominate the segment, offering higher efficiency and better thermal performance for industrial users. It supports industries aiming to balance energy savings with operational cost control. Single-pass systems remain relevant for facilities with smaller-scale operations or limited capital budgets. The trend toward multi-pass adoption reflects industrial preference for higher output and improved reliability.

- For instance, the Cleaver-Brooks CBEX model offers 2,500 boiler horsepower and operates with a turndown ratio of 10:1, allowing precise modulation from high to low output, which supports energy-efficient industrial steam generation.

By Platform

Segmentation by platform covers stationary and mobile applications. Stationary platforms hold the majority share, supported by large-scale deployment in chemical plants and industrial facilities. It is particularly suited for continuous operations that require stable and efficient heating. Mobile platforms, though smaller in share, are finding applications in temporary or remote industrial setups. Their flexibility in deployment and ease of installation make them suitable for niche requirements. Both platforms highlight the adaptability of non-condensing fire tube boilers across diverse industrial environments.

Segmentations:

By Component

- Boilers

- Burners

- Controls

- Auxiliary Systems

By Weapon Type

By Platform

By Application

- Chemical Processing

- Pharmaceuticals

- Food and Beverages

- Oil and Gas

- Power Generation

By Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

Strong Market Position in North America and Europe

North America accounts for 32% share of the Non-Condensing Fire Tube Chemical Market, supported by established industrial infrastructure. Europe holds 27% share, reflecting strong adoption driven by emission compliance and modernization programs. It benefits from rising demand in sectors that value reliability and efficient thermal performance. Regulatory initiatives in both regions are pushing industries to replace aging systems with advanced designs. Germany, the U.K., and France remain key contributors to Europe’s growth. Suppliers focusing on durability and compliance continue to strengthen their market presence.

Rapid Industrial Growth Across Asia Pacific

Asia Pacific captures 29% share of the Non-Condensing Fire Tube Chemical Market, making it a leading growth region. China and India are at the forefront, supported by industrial expansion and government-backed infrastructure programs. It aligns with the region’s energy demand and preference for cost-effective solutions. Southeast Asian countries are also emerging as key adopters, benefiting from growing manufacturing bases. Domestic and international suppliers are responding with efficient and competitively priced systems. The region’s large-scale industrialization is expected to drive its share higher in the coming years.

Emerging Potential in the Middle East and Latin America

The Middle East holds 7% share of the Non-Condensing Fire Tube Chemical Market, driven by petrochemical and energy sector demand. Latin America records 5% share, supported by expansion in Brazil and Mexico’s processing industries. It is gaining traction in both regions as industries focus on durable and affordable heating systems. Infrastructure projects in Saudi Arabia and the UAE are fueling opportunities for suppliers. Mexico and Brazil continue to strengthen demand with modernization of chemical facilities. These regions hold strong long-term growth potential for global and regional players.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Babcock Wanson

- Forbes Marshall

- Fulton Boiler Works

- Miura Boiler

- Johnston Boiler Company

- Hurst Boiler & Welding Co.

- Cleaver-Brooks

- Superior Boiler Works

- Thermodyne Engineering Systems

- Bosch Industriekessel GmbH

- Cochran Ltd.

Competitive Analysis:

The Non-Condensing Fire Tube Chemical Market is highly competitive with the presence of global and regional manufacturers. Leading players such as Cleaver-Brooks, Hurst Boiler & Welding Co., Fulton Boiler Works, and Bosch Industriekessel GmbH focus on product reliability, energy efficiency, and cost optimization to strengthen their positions. It is witnessing continuous innovation in boiler design, control systems, and integration of automation technologies to meet evolving industrial requirements. Regional players like Forbes Marshall, Thermodyne Engineering Systems, and Cochran Ltd. are expanding their reach by offering tailored solutions at competitive pricing. Partnerships, capacity expansions, and modernization projects remain central strategies for sustaining market growth. The competitive landscape reflects a balance between established global companies and agile regional suppliers, both aiming to capture opportunities created by industrial expansion, regulatory compliance, and rising demand for durable and efficient non-condensing fire tube systems.

Recent Developments:

- In August 2025, Babcock Wanson launched its PowerPack range, a new line of energy-efficient firetube boilers.

- In March 2024, Hurst Boiler & Welding Co. entered into a formal sales representative agreement with Nationwide Boiler Inc., making Nationwide its exclusive representative in California and the Houston, Texas area.

- In October 2024, Miura introduced the LXN-300SG-A, a new ultra-low NOx steam boiler that reduces emissions to below 5 ppm.

Report Coverage:

The research report offers an in-depth analysis based on Component, Weapon Type, Platform, Application and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The Non-Condensing Fire Tube Chemical Market will continue to gain traction in chemical and manufacturing industries due to stable heat supply requirements.

- Energy efficiency will remain a key priority, with manufacturers investing in improved designs and operational reliability.

- Adoption of automation and IoT-enabled monitoring solutions will expand, supporting predictive maintenance and reducing downtime.

- Replacement of aging boiler infrastructure will create strong opportunities for suppliers offering advanced and compliant systems.

- Cost-effectiveness will sustain demand in price-sensitive regions where lower upfront investment is a critical factor.

- Stricter safety and environmental regulations will encourage modernization, driving industries to adopt updated fire tube technologies.

- Asia Pacific will strengthen its position as the fastest-growing regional market, fueled by industrialization in China, India, and Southeast Asia.

- North America and Europe will maintain steady demand, supported by modernization programs and regulatory compliance requirements.

- Emerging markets in Latin America and the Middle East will provide long-term growth potential through infrastructure and petrochemical projects.

- Competitive dynamics will push manufacturers to innovate while balancing cost, efficiency, and durability to sustain market leadership.