Market Overview

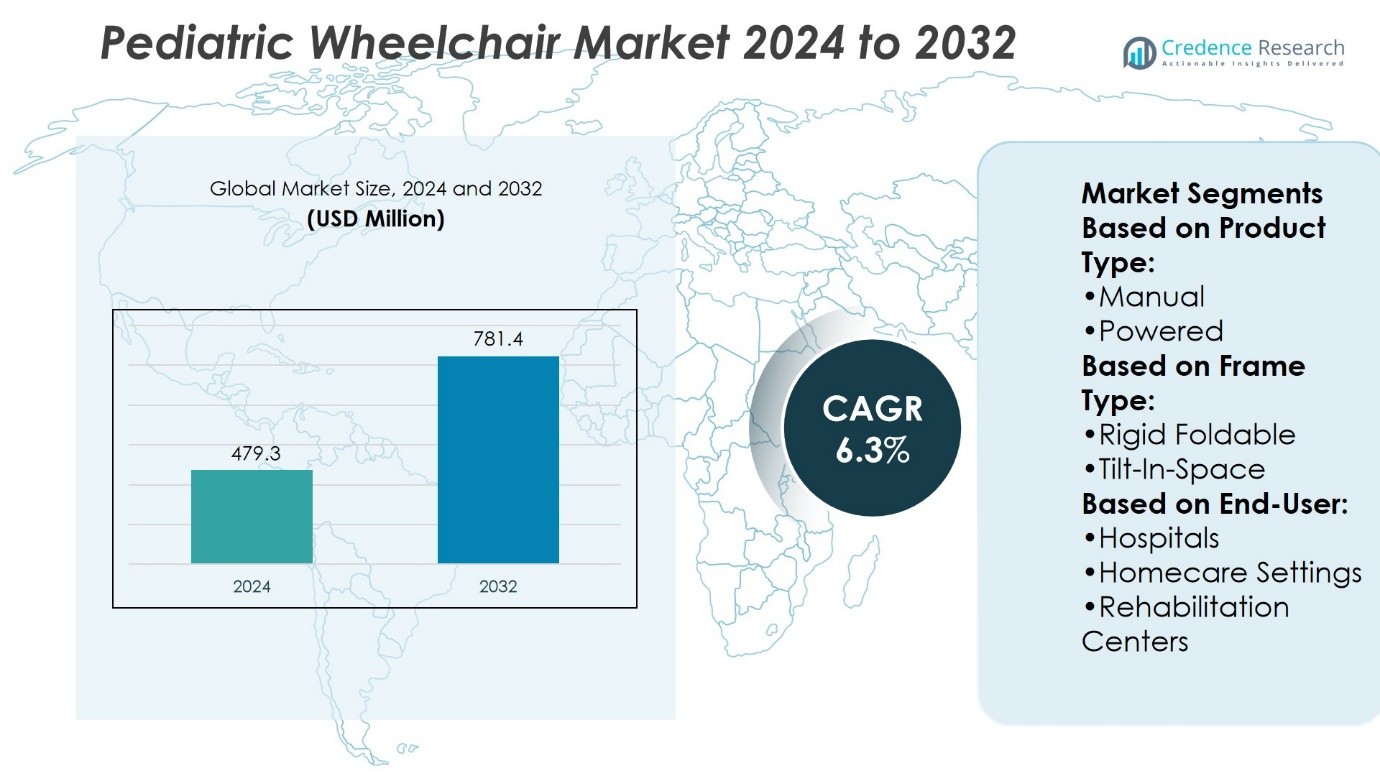

Pediatric Wheelchair Market size was valued at USD 479.3 million in 2024 and is anticipated to reach USD 781.4 million by 2032, at a CAGR of 6.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Pediatric Wheelchair Market Size 2024 |

USD 479.3 Million |

| Pediatric Wheelchair Market , CAGR |

6.3% |

| Pediatric Wheelchair Market Size 2032 |

USD 781.4 Million |

The pediatric wheelchair market grows steadily due to rising prevalence of childhood disabilities, increasing awareness of mobility aids, and expanding access to rehabilitation services. Strong government support programs and insurance coverage improve affordability, encouraging higher adoption rates. Manufacturers focus on lightweight, customizable, and ergonomic designs that enhance comfort and independence for children. Technological advancements, including powered wheelchairs with digital controls and smart features, further strengthen demand. Trends also highlight increasing investment in sustainable materials and eco-friendly production. Growing emphasis on inclusive education and expanding healthcare infrastructure in emerging economies continue to create new opportunities for market expansion worldwide.

North America leads the pediatric wheelchair market with strong healthcare systems and high adoption, followed by Europe with supportive reimbursement policies and advanced manufacturing. Asia-Pacific shows the fastest growth, driven by rising pediatric populations and improving access to care. Latin America and the Middle East & Africa hold smaller shares but display steady potential through awareness programs and infrastructure development. Key players shaping the market include Sunrise Medical, Ottobock, Drive Medical, Medline, Roma Medical Aids, Graham-Field, and MJM International.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- Pediatric Wheelchair Market size was valued at USD 479.3 million in 2024 and is projected to reach USD 781.4 million by 2032, at a CAGR of 6.3%.

- Rising prevalence of childhood disabilities and growing awareness of mobility aids drive consistent demand.

- Expanding access to rehabilitation services and strong government support programs boost adoption.

- Technological advancements in powered wheelchairs with smart features highlight a major market trend.

- Competition intensifies as players focus on lightweight, ergonomic, and customizable pediatric wheelchair designs.

- High product costs and limited insurance coverage in developing regions act as restraints.

- North America dominates, Europe follows, Asia-Pacific grows fastest, while Latin America and MEA show steady potential.

Market Drivers

Growing Incidence of Pediatric Mobility Disorders

The rising prevalence of mobility-related disorders among children strongly drives the Pediatric Wheelchair Market. Conditions such as cerebral palsy, muscular dystrophy, and spinal cord injuries create consistent demand. Pediatric wheelchairs address the unique ergonomic and functional needs of young patients. It supports improved independence and quality of life for children with limited mobility. Healthcare providers recommend specialized designs tailored for growth and development. Governments and NGOs further promote adoption through subsidies and patient assistance programs.

- For instance, according to UNICEF, an estimated 240 million children worldwide live with some form of disability, which includes a wide range of physical, intellectual, and sensory impairments. While not all of these children have mobility issues requiring a wheelchair, the figure highlights the significant, and often underserved, population of children with specific clinical needs. For children with physical disabilities such as cerebral palsy, muscular dystrophy, and spinal cord injuries, there is a clear demand for specialized pediatric wheelchairs.

Advancements in Wheelchair Technology

Continuous innovation in wheelchair design fuels market expansion worldwide. Lightweight frames, foldable structures, and customizable seating systems enhance usability. Electric-powered models with smart control features improve maneuverability for children and caregivers. It integrates IoT-enabled tracking and safety mechanisms for better monitoring. Companies focus on adjustable designs to accommodate children’s growth phases. These improvements raise caregiver confidence and boost adoption in homecare and hospital settings.

- For instance, many companies in the wheelchair manufacturing industry produce a wide range of models, often exceeding twenty different types to meet diverse user needs. Common offerings in the market include models with lightweight aluminum frames and foldable designs, which are standard features across the industry to improve portability.

Increasing Awareness and Healthcare Support

Rising awareness about pediatric mobility solutions contributes significantly to demand growth. Educational campaigns highlight the benefits of early wheelchair use in rehabilitation. Hospitals and clinics are expanding specialized pediatric rehabilitation programs. It strengthens the availability of custom solutions for long-term patient needs. Non-profit organizations and advocacy groups promote accessibility in schools and public spaces. Growing healthcare budgets in developing economies also support procurement of pediatric wheelchairs.

Rising Demand from Homecare and Rehabilitation Centers

Homecare services and rehabilitation centers represent a growing share of demand. Families seek convenient, durable, and safe wheelchairs for children’s everyday activities. Hospitals increasingly partner with rehabilitation units to provide tailored equipment. It enhances recovery outcomes and helps integrate children into social settings. Specialized centers focus on mobility training, increasing the importance of adaptive devices. Insurance coverage expansion further supports the affordability of pediatric wheelchairs in multiple regions.

Market Trends

Growing Shift Toward Lightweight and Portable Designs

The Pediatric Wheelchair Market is witnessing a strong trend toward lightweight and foldable designs. Families and caregivers demand products that provide easy transportation and storage. Aluminum and carbon fiber frames are increasingly adopted for durability and reduced weight. It enhances mobility for children during school, travel, and recreational activities. Compact designs support greater independence for users and convenience for caregivers. Manufacturers continue to refine materials and structure to meet these evolving preferences.

- For instance, the Quickie 2 model features a stronger 7000-series aerospace-grade aluminum cross-brace, increasing weight capacity while keeping the chair lightweight.

Rising Adoption of Electric and Smart Wheelchairs

Electric-powered pediatric wheelchairs are gaining wider acceptance in healthcare and homecare settings. These models provide improved control, reduced physical strain, and better maneuverability for children. Smart features such as joystick navigation, battery monitoring, and obstacle detection enhance safety. It reflects a growing alignment with technological progress in medical devices. Caregivers and healthcare providers prefer such models for children with higher mobility limitations. Integration of digital features ensures comfort and long-term usability.

- For instance, Roma Medical Aids distributes its pediatric and mobility products through a network of dealers across more than 25 countries, ensuring global reach and accessibility for diverse user groups.

Customization and Growth-Oriented Features

Personalized wheelchairs tailored to children’s needs are becoming central to market growth. Adjustable seating, modular components, and ergonomic supports help accommodate physical development. It allows long-term usage while ensuring safety and comfort. Hospitals and rehabilitation centers emphasize wheelchairs that adapt to therapy requirements. Custom designs encourage better compliance among young patients and their families. Market players expand product lines with options addressing growth stages and medical conditions.

Expansion of Accessibility and Healthcare Support

Governments and organizations are strengthening policies to enhance wheelchair accessibility. Subsidies, reimbursement schemes, and NGO initiatives expand affordability for families worldwide. Schools and public spaces integrate accessible infrastructure to support inclusion. It reflects a broader commitment to children’s mobility rights and independence. Healthcare systems invest in pediatric rehabilitation centers to provide tailored wheelchair solutions. These combined efforts strengthen awareness and accelerate adoption across multiple regions.

Market Challenges Analysis

High Cost and Limited Affordability

The Pediatric Wheelchair Market faces significant challenges due to high product costs. Advanced models with electric features and smart technologies remain out of reach for many families. It creates a gap between the availability of innovative solutions and their actual adoption. Insurance coverage often fails to fully support pediatric mobility equipment, leading to financial strain. In developing regions, limited access to funding and subsidies further restricts demand. Manufacturers face pressure to balance affordability with innovation, creating a complex challenge for sustained growth.

Infrastructure and Awareness Barriers

Limited infrastructure and awareness hinder market expansion, particularly in low and middle-income countries. Schools, playgrounds, and public spaces often lack adequate accessibility for wheelchair users. It reduces the effectiveness of mobility solutions and restricts participation in daily activities. Families in rural areas face difficulty accessing specialized wheelchair providers and service centers. Awareness about early intervention and the benefits of pediatric mobility devices also remains low. Addressing these barriers requires collaboration between governments, healthcare providers, and advocacy groups to create inclusive environments.

Market Opportunities

Technological Advancements and Product Innovation

The Pediatric Wheelchair Market presents strong opportunities through advancements in design and technology. Integration of smart features such as obstacle detection, joystick control, and connected monitoring improves usability. It creates higher acceptance among caregivers and healthcare providers seeking safer and more efficient solutions. Lightweight materials and modular designs further enhance comfort and adaptability for growing children. Manufacturers investing in customization and ergonomic innovations can capture rising demand. These opportunities strengthen the market’s long-term potential across developed and emerging economies.

Expanding Healthcare Support and Accessibility Initiatives

Governments and organizations are increasing investments in mobility support programs, creating new growth avenues. Subsidies, insurance reforms, and NGO-led initiatives make pediatric wheelchairs more accessible to families. It allows broader adoption of both manual and electric models in diverse settings. Expansion of pediatric rehabilitation centers drives demand for tailored mobility solutions. Schools and public facilities adopting inclusive infrastructure further accelerate market opportunities. Growing emphasis on mobility rights ensures long-term prospects for the global pediatric wheelchair industry.

Market Segmentation Analysis:

By Product Type

The Pediatric Wheelchair Market is segmented into manual and powered wheelchairs. Manual wheelchairs dominate due to affordability, ease of use, and suitability for mild mobility needs. They remain widely adopted in hospitals and homecare where basic mobility support is sufficient. Powered wheelchairs, however, are gaining momentum with rising demand for advanced mobility solutions. It provides enhanced independence, especially for children with severe mobility limitations. The inclusion of smart navigation, joystick controls, and adjustable seating positions strengthens their adoption. Rising disposable incomes and healthcare funding are expected to accelerate the powered segment’s growth in the coming years.

- For instance, the Vive Mobility Electric Wheelchair Model V has a weight capacity of 300 lbs, enabling it to support users with higher mobility needs safely and reliably.

By Frame Type

Frame type segmentation includes rigid, foldable, and tilt-in-space models. Rigid frames provide stability, durability, and support for long-term use in intensive care environments. Foldable designs attract families and caregivers seeking lightweight, portable, and travel-friendly options. It enhances convenience during school, recreational activities, and transportation. Tilt-in-space wheelchairs are preferred in advanced rehabilitation and hospital settings, offering posture support and pressure relief. They help reduce the risk of complications associated with prolonged sitting in children with chronic conditions. The growing focus on ergonomic and adaptive frames highlights the shift toward comfort-driven solutions.

- For instance, Medline distributes over 335,000 different medical products, more than 190,000 of which are under its own brand, across more than 50 distribution centers in North America.

By End User

End-user segmentation covers hospitals, homecare settings, and rehabilitation centers. Hospitals remain key users due to their focus on post-surgical recovery and treatment of mobility-related disorders. Rehabilitation centers play a vital role in driving demand for specialized and adjustable wheelchair models tailored to therapy needs. It supports patient engagement in structured mobility training programs. Homecare settings are expanding as families increasingly invest in personalized mobility solutions for daily use. Growth in home-based care highlights the demand for convenient, durable, and cost-effective products. Together, these end-user segments create diverse opportunities across global healthcare ecosystems, strengthening the market outlook.

Segments:

Based on Product Type:

Based on Frame Type:

- Rigid Foldable

- Tilt-In-Space

Based on End-User:

- Hospitals

- Homecare Settings

- Rehabilitation Centers

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds the largest share of the pediatric wheelchair market, accounting for about 35–39% in 2023–2024. The U.S. leads due to strong healthcare infrastructure, insurance coverage, and higher awareness of mobility aids. Pediatric wheelchair demand grows as advanced customization technologies and supportive government programs expand. Canada contributes significantly, with rising adoption of powered wheelchairs and increased focus on inclusive mobility solutions. The region’s dominance remains steady, supported by well-established distribution channels and high spending capacity among families.

Europe

Europe represents the second-largest market with an estimated 27–30% share. Countries like Germany, France, and the U.K. drive growth through strong public healthcare systems and supportive reimbursement policies. The region shows high adoption of manual and powered pediatric wheelchairs, supported by local manufacturers and international brands. Increasing emphasis on accessibility, coupled with regulatory support for children with disabilities, sustains demand. Advancements in ergonomic designs and sustainability standards further shape market expansion across the European Union.

Asia-Pacific

Asia-Pacific accounts for nearly 20% share but records the fastest growth, with a projected double-digit CAGR. China, Japan, and India lead the region due to rising pediatric populations and improving healthcare access. Government initiatives to strengthen rehabilitation services boost adoption of pediatric wheelchairs. Demand for cost-effective manual wheelchairs is higher, but powered wheelchair adoption is increasing in urban markets. Growing investments by global players, combined with local manufacturing support, strengthen the regional outlook and gradually increase its share.

Latin America

Latin America contributes around 8–10% share of the global pediatric wheelchair market. Brazil and Mexico dominate regional demand, driven by expanding healthcare access and supportive non-governmental initiatives. However, limited insurance coverage and high product costs restrict wider adoption across low-income populations. Local distribution partnerships help improve accessibility, while international brands target urban markets. Despite challenges, awareness campaigns and rehabilitation center expansion sustain moderate growth across the region.

Middle East & Africa

The Middle East & Africa region holds the smallest share, estimated at 5–6%. Countries like Saudi Arabia, South Africa, and the UAE lead adoption, supported by gradual improvements in healthcare funding. Manual pediatric wheelchairs dominate due to affordability, while powered models remain limited to high-income families. Market expansion faces challenges from lower awareness and uneven healthcare distribution. However, increased government focus on inclusive education and mobility support programs is expected to drive steady demand growth in the coming years.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The competitive landscape of the pediatric wheelchair market includes players such as Drive Medical, Guangdong Shunde Jaeyong Hardware, Sunrise Medical, Sammons Preston, Roma Medical Aids, MJM International, Ottobock, Vive, Medline, TumbleForms, and Graham-Field. The pediatric wheelchair market shows intense competition driven by innovation, affordability, and accessibility. Manufacturers focus on expanding product portfolios that include both manual and powered models, with growing emphasis on lightweight and customizable designs. Companies compete by enhancing ergonomics, improving safety features, and offering flexible options for hospitals, rehabilitation centers, and homecare settings. Pricing strategies and strong distribution networks remain vital to securing market presence, especially in emerging regions. Many players also invest in research to introduce advanced mobility solutions, including smart wheelchairs with digital integration. Strategic partnerships with healthcare providers and non-governmental organizations further strengthen outreach, ensuring access for children with diverse needs. The competitive landscape continues to evolve as firms balance affordability with technological advancement to capture a wider global audience.

Recent Developments

- In April 2025, Aveanna Healthcare Holdings announced an agreement to acquire Thrive Skilled Pediatric Care, a major provider of pediatric home care services including skilled nursing and therapy for medically complex children. This acquisition enhances Aveanna’s service footprint and integrates specialized care models that support pediatric wheelchair users in home-based settings.

- In November 2024, MIGA Holdings LLC completed the acquisition of Invacare’s North American business, creating opportunities for operational optimization and market expansion in the pediatric wheelchair segment.

- In October 2024, Permobil launched the TiLite X and TiLite Z ultra-lightweight manual wheelchairs featuring over 1 billion configurations, with weights of 12.1 pounds and 11.3 pounds respectively, demonstrating advances in customization and weight reduction for pediatric applications.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Frame Type, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see rising demand for powered pediatric wheelchairs with smart mobility features.

- Customization and ergonomic designs will become standard to meet specific child mobility needs.

- Technological integration such as sensors and digital controls will enhance wheelchair safety.

- Growth in homecare and rehabilitation settings will drive consistent adoption worldwide.

- Manufacturers will expand presence in Asia-Pacific as demand grows with healthcare access.

- Partnerships with NGOs and healthcare providers will improve wheelchair availability in low-income regions.

- Sustainability and eco-friendly materials will play a larger role in product development.

- Insurance coverage and government support programs will increase affordability for families.

- Online sales channels and direct-to-consumer distribution will grow stronger across regions.

- Market rivalry will intensify with new entrants focusing on low-cost and innovative solutions.