Market Overview

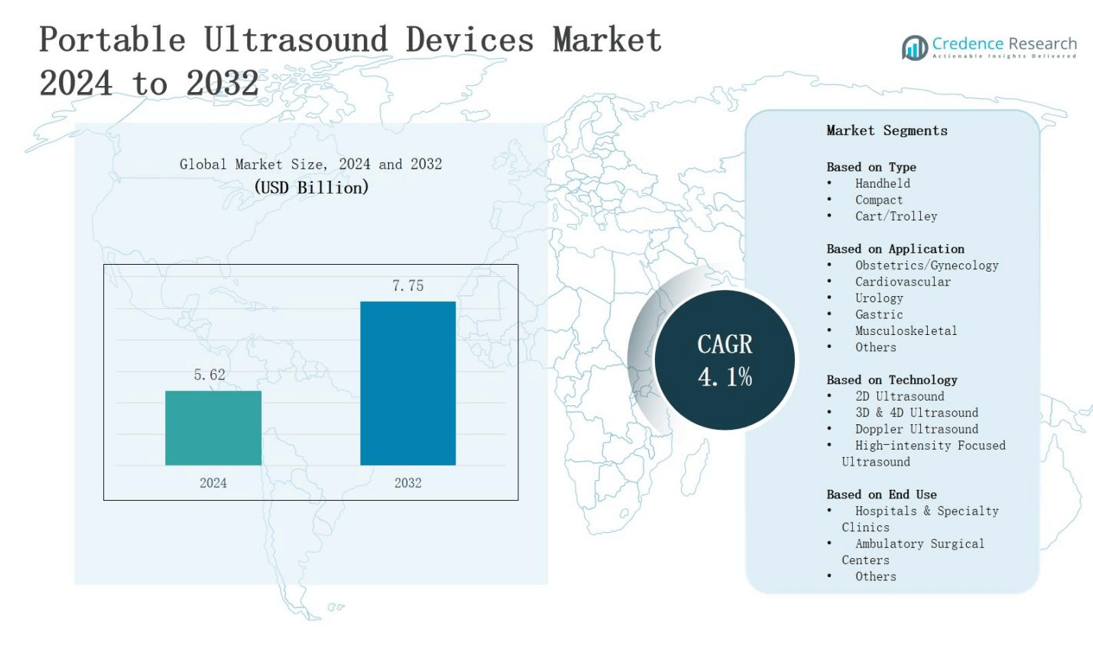

The global portable ultrasound devices market is projected to grow from USD 5.62 billion in 2024 to USD 7.75 billion by 2032, registering a CAGR of 4.1%.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Portable Ultrasound Devices Market Size 2024 |

USD 5.62 billion |

| Portable Ultrasound Devices Market, CAGR |

4.1% |

| Portable Ultrasound Devices Market Size 2032 |

USD 7.75 billion |

The portable ultrasound devices market is driven by rising demand for point-of-care diagnostics, increasing prevalence of chronic diseases, and growing adoption of minimally invasive procedures. Advancements in imaging technology, including AI integration and wireless connectivity, are enhancing accuracy and usability, fostering wider clinical adoption. The surge in telemedicine and home healthcare further accelerates demand for compact and cost-effective diagnostic tools. Moreover, rising healthcare investments in emerging economies and the need for efficient emergency and remote patient care support market expansion. These trends collectively strengthen the role of portable ultrasound devices in modern healthcare delivery systems.

The portable ultrasound devices market shows strong geographical presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, each contributing to its global expansion. North America leads with advanced infrastructure, while Europe emphasizes preventive care. Asia-Pacific grows rapidly through expanding healthcare access, Latin America advances with modernization efforts, and the Middle East & Africa adopt affordable solutions for underserved areas. Key players include General Electric Company, Siemens, Koninklijke Philips N.V., FUJIFILM Holdings Corporation, Samsung, Canon Inc., Hitachi, Butterfly Network, and Shenzhen Mindray Bio-medical Electronics Co., Ltd.

Market Insights

- The portable ultrasound devices market is projected to grow from USD 5.62 billion in 2024 to USD 7.75 billion by 2032, recording a steady CAGR of 4.1%.

- Handheld devices dominate with 45% share, followed by compact systems at 35% and cart/trolley-based units at 20%, driven by affordability, ease of use, and strong adoption in emergency care.

- Obstetrics/gynecology leads applications with 30% share, followed by cardiovascular at 25%, supported by rising maternal health needs, prenatal monitoring, and growing cases of lifestyle-related chronic conditions globally.

- By technology, 2D ultrasound holds 50% share due to affordability and wide clinical use, while 3D & 4D systems, Doppler, and high-intensity focused ultrasound gain traction in advanced diagnostics.

- Regionally, North America leads with 35% share, followed by Europe at 27%, Asia-Pacific at 25%, Latin America at 7%, and Middle East & Africa at 6%, reflecting diverse adoption trends.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Point-of-Care Diagnostics

The portable ultrasound devices market benefits from the growing emphasis on point-of-care diagnostics, particularly in emergency and rural healthcare settings. It allows physicians to make faster and more accurate clinical decisions without relying on large imaging infrastructure. The need for immediate diagnosis in critical care, maternity, and cardiac applications supports adoption. Healthcare systems prioritize cost-efficient solutions, and portable ultrasound proves reliable. Growing patient volumes encourage hospitals to deploy it more broadly.

- For instance, Philips Lumify connects directly to a smartphone or tablet and is routinely used by clinicians for cardiac, abdominal, and vascular assessments in emergency departments—enabling real-time, on-the-spot decision-making.

Increasing Prevalence of Chronic and Lifestyle Diseases

Chronic illnesses, including cardiovascular disorders, diabetes, and cancer, drive higher usage of portable imaging tools. The portable ultrasound devices market responds to the demand for early diagnosis and routine monitoring in outpatient care. It supports screening of high-risk populations, reducing the burden on tertiary hospitals. Growing urbanization and lifestyle shifts raise incidence rates, fueling diagnostic requirements. It provides safe, non-invasive evaluation, building confidence among both physicians and patients. Demand intensifies globally.

- For instance, GE HealthCare’s Vscan Air™, a wireless handheld ultrasound, has been adopted by clinicians for bedside cardiac and abdominal evaluations, assisting in faster decision-making without requiring patients to visit large imaging centers

Technological Advancements Enhancing Usability

The portable ultrasound devices market expands with technological upgrades that strengthen image clarity, portability, and integration with smart platforms. It benefits from AI-driven imaging, cloud-based reporting, and wireless connectivity, improving diagnostic precision. Compact designs enable easy use across multiple clinical departments. Hospitals adopt solutions that shorten diagnostic timelines and reduce error rates. It creates efficiencies in workflows and enhances physician confidence. Advancements reinforce adoption and differentiate competitive offerings in healthcare.

Growing Adoption in Remote and Home Healthcare

The portable ultrasound devices market witnesses rising utilization in remote healthcare, home care, and telemedicine. It empowers healthcare professionals to extend advanced diagnostics to underserved areas. Portable systems meet the need for reliable and affordable solutions in low-resource settings. Governments and NGOs promote deployment in community health programs. It offers flexibility for patient-centered care models, ensuring timely assessments. The shift toward decentralized healthcare strengthens its position across global medical practices.

Market Trends

Integration of Artificial Intelligence and Smart Features

The portable ultrasound devices market experiences strong momentum through integration of artificial intelligence and advanced software features. It supports physicians by automating image interpretation and improving diagnostic confidence in complex cases. AI tools help reduce operator dependency, ensuring consistent results across different care environments. Smart connectivity allows seamless sharing of scans for second opinions and remote consultations. Hospitals value these enhancements, which improve efficiency and accuracy. It elevates the clinical relevance of portable solutions.

Expansion of Telemedicine and Remote Care Applications

The portable ultrasound devices market gains traction from its growing role in telemedicine and remote patient care. It enables specialists to perform virtual diagnostics and guide less experienced practitioners in rural areas. Compact devices with wireless transmission features integrate smoothly into digital health ecosystems. Demand increases for equipment that can link patients with urban hospitals. It makes healthcare delivery more inclusive and responsive. Widespread adoption highlights its transformative impact on healthcare access.

- For instance, Butterfly Network introduced the Butterfly iQ, the world’s first whole-body ultrasound imager on a silicon chip, which connects via a smartphone and uses cloud-based image sharing, enabling specialists to remotely guide procedures in real time.

Rising Popularity of Home Healthcare Solutions

The portable ultrasound devices market benefits from rising preference for home-based healthcare services. It empowers patients and caregivers to access reliable diagnostics without visiting hospitals. Elderly populations and individuals with chronic illnesses prefer convenient solutions that support frequent monitoring. Healthcare providers adopt portable systems to reduce inpatient loads and improve continuity of care. It encourages patient engagement in disease management. Home healthcare trends strengthen adoption rates and broaden application scope for portable devices.

- For instance, ASUS developed a 64-channel portable ultrasound device that is pocket-sized, wireless, and offers up to four hours of battery life, making it suitable for home visits and telecare scenarios.

Focus on Miniaturization and Cost Efficiency

The portable ultrasound devices market advances with innovations in miniaturization and affordability. It drives demand among small clinics, ambulatory centers, and resource-limited facilities. Manufacturers prioritize compact designs that maintain imaging quality while reducing costs. Greater affordability allows wider adoption across developing nations. It supports healthcare systems seeking scalable diagnostic options. Miniaturization also promotes portability, enabling professionals to deliver on-site care. This trend positions portable ultrasound as a critical tool in expanding medical outreach.

Market Challenges Analysis

High Cost of Advanced Technologies and Limited Affordability

The portable ultrasound devices market faces challenges due to the high cost of advanced technologies and limited affordability in low-resource settings. It requires significant investment in research and development, which raises device prices and restricts accessibility for smaller healthcare facilities. Budget constraints in developing nations limit adoption, especially in primary care centers. Hospitals often prioritize other critical equipment, delaying procurement of portable ultrasound systems. It creates disparities in healthcare delivery and slows market penetration.

Shortage of Skilled Professionals and Training Barriers

The portable ultrasound devices market encounters hurdles linked to a shortage of skilled professionals and training limitations. It demands operators with specialized knowledge to ensure accurate diagnosis and avoid misinterpretation. Many rural and semi-urban regions lack trained sonographers, reducing the effectiveness of portable solutions. Healthcare organizations struggle to maintain continuous training programs due to costs and staffing pressures. It hinders adoption and affects the consistency of outcomes, challenging widespread market integration.

Market Opportunities

Expansion Across Emerging Economies and Rural Healthcare

The portable ultrasound devices market holds significant opportunities through expansion across emerging economies and rural healthcare systems. It offers affordable and mobile diagnostic solutions that align with government initiatives to strengthen primary healthcare infrastructure. Rising investments in healthcare access create demand for compact and efficient imaging tools. Clinics and outreach programs benefit from its portability, reducing patient dependence on urban hospitals. It supports wider screening programs and accelerates early disease detection in underserved regions.

Growth Potential in Home Healthcare and Preventive Medicine

The portable ultrasound devices market presents strong opportunities within home healthcare and preventive medicine. It aligns with growing patient preference for convenient, accessible diagnostic solutions. Rising prevalence of chronic illnesses drives need for frequent monitoring outside hospitals. Portable systems empower caregivers and reduce pressure on inpatient facilities. It also supports preventive care models by enabling early intervention and lowering treatment costs. Growing awareness of wellness and proactive healthcare strengthens long-term market prospects.

Market Segmentation Analysis:

By Type

In the portable ultrasound devices market, the handheld segment dominates with around 45% share, driven by rising adoption in emergency care, home healthcare, and remote medical services. Compact systems account for nearly 35%, supported by their use in hospitals and diagnostic centers requiring balance between portability and performance. Cart/trolley-based devices hold close to 20%, catering to specialized departments. The preference for handheld models grows due to ease of use, affordability, and integration with wireless platforms.

- For instance, the GE Vscan Air SL handheld ultrasound system is widely favored in cardiology and emergency departments due to its dual-probe design and wireless connectivity, enhancing bedside cardiac assessments.

By Application

The obstetrics/gynecology segment leads with nearly 30% share in the portable ultrasound devices market, supported by rising maternal healthcare needs and prenatal monitoring. Cardiovascular applications represent about 25%, reflecting growing incidence of heart-related conditions. Urology captures around 15%, while musculoskeletal accounts for close to 12%. Gastric applications hold nearly 10%, with others making up the remainder. High demand for non-invasive diagnostics in maternal care and chronic disease management drives market growth across applications.

- For instance, Philips’ Lumify portable ultrasound is widely used in cardiology clinics, and a 2022 clinical review highlighted that handheld devices helped detect left ventricular dysfunction with over 80% accuracy compared to traditional echocardiography.

By Technology

In the portable ultrasound devices market, the 2D ultrasound segment dominates with around 50% share, owing to its affordability, reliability, and wide clinical utility. The 3D & 4D ultrasound segment captures nearly 25%, driven by demand for detailed imaging in obstetrics and advanced diagnostics. Doppler ultrasound holds close to 20%, particularly valuable in cardiovascular evaluations. High-intensity focused ultrasound remains niche with about 5%, but it gains attention in therapeutic applications. Cost efficiency sustains 2D technology leadership.

Segments:

Based on Type

- Handheld

- Compact

- Cart/Trolley

Based on Application

- Obstetrics/Gynecology

- Cardiovascular

- Urology

- Gastric

- Musculoskeletal

- Others

Based on Technology

- 2D Ultrasound

- 3D & 4D Ultrasound

- Doppler Ultrasound

- High-intensity Focused Ultrasound

Based on End Use

- Hospitals & Specialty Clinics

- Ambulatory Surgical Centers

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds the largest share of the portable ultrasound devices market at 35%, supported by strong healthcare infrastructure and advanced adoption of innovative diagnostic technologies. It benefits from high demand for point-of-care diagnostics and growing applications in emergency medicine. Favorable reimbursement policies encourage hospitals and clinics to invest in portable systems. The region experiences rising usage in home healthcare, particularly for elderly populations. It also gains momentum from the presence of leading manufacturers. Continuous R&D investments further reinforce market leadership.

Europe

Europe accounts for 27% of the portable ultrasound devices market, driven by increasing emphasis on preventive care and rising prevalence of chronic diseases. The region demonstrates strong adoption in cardiology, obstetrics, and musculoskeletal applications. Governments actively support initiatives to strengthen healthcare access, boosting demand for portable solutions in rural and urban settings. It gains from robust regulatory standards that enhance quality assurance. Growing healthcare expenditure across major economies sustains growth. The market benefits from expanding telemedicine practices in the region.

Asia-Pacific

Asia-Pacific represents 25% of the portable ultrasound devices market, supported by rapid improvements in healthcare infrastructure and expanding access in emerging economies. Rising birth rates and maternal health awareness strengthen demand in obstetrics. The increasing burden of cardiovascular and lifestyle-related conditions fuels adoption across hospitals and clinics. It shows strong momentum from government-backed health programs in countries such as India and China. Rising affordability of handheld devices accelerates usage in rural areas. Local manufacturing initiatives also drive competitive growth.

Latin America

Latin America holds 7% of the portable ultrasound devices market, shaped by growing investments in healthcare modernization and expanding private healthcare facilities. Rising demand for non-invasive diagnostic solutions in maternal and emergency care supports adoption. It faces challenges with limited affordability in low-income regions, yet government partnerships help expand outreach programs. The market grows steadily in countries such as Brazil and Mexico. Portable devices support rural healthcare initiatives and mobile medical services. Increasing awareness of early diagnosis boosts utilization.

Middle East & Africa

The Middle East & Africa region accounts for 6% of the portable ultrasound devices market, driven by gradual improvements in healthcare systems and rising demand for affordable diagnostic tools. It benefits from international collaborations aimed at strengthening healthcare infrastructure. Portable systems are increasingly used in remote and underserved areas where access to hospitals is limited. Rising prevalence of chronic diseases pushes demand for cost-effective solutions. The market also gains traction in maternity and emergency care. It expands steadily with targeted government programs.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Clarius Mobile Health

- ESAOTE SPA

- SAMSUNG

- BenQ Corporation

- Shenzhen Mindray Bio-medical Electronics Co., Ltd.

- Siemens

- Hitachi

- General Electric Company

- Canon Inc.

- FUJIFILM Holdings Corporation

- Koninklijke Philips N.V.

- Butterfly Network

Competitive Analysis

The portable ultrasound devices market is highly competitive, characterized by the presence of established multinational corporations and innovative startups focusing on advanced imaging solutions. Leading players such as General Electric Company, Siemens, Koninklijke Philips N.V., and FUJIFILM Holdings Corporation leverage strong R&D capabilities and global distribution networks to strengthen their positions. It emphasizes innovation with AI-driven features, wireless connectivity, and compact designs to meet rising demand for point-of-care diagnostics. Companies like Samsung, Canon Inc., and Hitachi expand portfolios with user-friendly and affordable systems, targeting diverse clinical applications. Emerging firms including Butterfly Network, Clarius Mobile Health, and BenQ Corporation enhance competition by introducing cost-effective handheld devices that appeal to home healthcare and rural markets. Shenzhen Mindray Bio-medical Electronics Co., Ltd. and ESAOTE SPA focus on expanding market presence through strategic product launches and partnerships in developing regions. It remains a dynamic landscape where players compete on technology, pricing, and accessibility, pushing continuous innovation to capture broader healthcare segments.

Recent Developments

- In June 2025, Philips launched the Flash 5100 POC point-of-care ultrasound system, designed with AI-driven automation, intuitive touchscreen features, and built-in tele-ultrasound support for real-time collaboration.

- In February 2025, Esaote unveiled its new C-Series portable ultrasound systems, expanding their offerings for mobile diagnostic use.

- In March 2025, at the ACC Annual Scientific Session, Philips introduced the Compact Ultrasound 5500CV, equipped with AI-based measurement tools and live 3D transesophageal echocardiography imaging to improve diagnostic efficiency in cardiac care.

- In 2024, GE HealthCare revealed an agreement to acquire Intelligent Ultrasound Group PLC, integrating real-time image recognition AI into its women’s health and portable ultrasound platforms for faster and more accurate diagnoses.

Market Concentration & Characteristics

The portable ultrasound devices market displays a moderately concentrated structure, with a mix of established multinational corporations and emerging innovators competing across regions. Leading players such as General Electric Company, Siemens, Koninklijke Philips N.V., Samsung, and FUJIFILM Holdings Corporation hold strong market positions through extensive product portfolios and global distribution networks. It reflects competitive characteristics shaped by technological advancement, pricing strategies, and continuous R&D investments aimed at improving portability, connectivity, and imaging accuracy. New entrants like Butterfly Network and Clarius Mobile Health create disruption by introducing affordable handheld devices that expand accessibility in home healthcare and rural settings. It demonstrates steady innovation cycles, with increasing focus on AI integration, wireless solutions, and compact designs to enhance usability. Market dynamics emphasize affordability, patient-centric care, and technological superiority, which define competitive differentiation. It remains influenced by healthcare infrastructure, regulatory standards, and rising demand for efficient diagnostic tools across both developed and emerging economies.

Report Coverage

The research report offers an in-depth analysis based on Type, Application, Technology, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand will rise for handheld devices due to their ease of use in emergency care and home healthcare.

- AI-powered imaging features will enhance diagnostic accuracy and reduce operator dependency.

- Telemedicine integration will strengthen adoption in remote and underserved regions.

- Hospitals will prioritize compact systems that balance performance with portability.

- Preventive healthcare initiatives will drive higher use in maternal and chronic disease monitoring.

- Affordability improvements will expand penetration across developing economies.

- Wireless connectivity and cloud-based reporting will support faster decision-making.

- Miniaturization will continue to enhance mobility and cross-department usage.

- Regulatory approvals will shape faster entry of innovative devices into clinical practice.

- Strategic collaborations and partnerships will accelerate market expansion across global healthcare ecosystems.