Market Overview

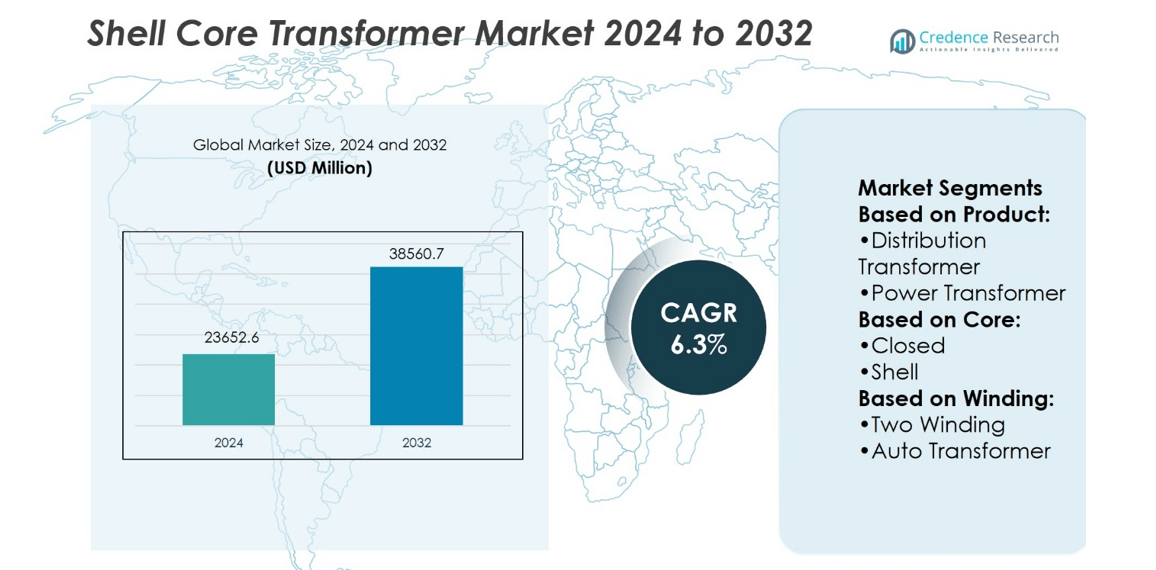

Shell Core Transformer Market size was valued at USD 23652.6 million in 2024 and is anticipated to reach USD 38560.7 million by 2032, at a CAGR of 6.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Shell Core Transformer Market Size 2024 |

USD 23652.6 million |

| Shell Core Transformer Market, CAGR |

6.3% |

| Shell Core Transformer Market Size 2032 |

USD 38560.7 million |

The Shell Core Transformer Market grows through rising electricity demand, grid modernization, and renewable energy integration. Governments enforce stricter efficiency standards, driving adoption of eco-friendly insulation and low-loss designs. It gains momentum from digital monitoring solutions that support predictive maintenance and operational reliability. Urbanization fuels demand for compact models, while industrial expansion increases need for high-capacity units. Renewable projects across emerging economies strengthen adoption of durable, efficient shell core designs. The market also benefits from continuous innovation in materials and smart grid compatibility. It ensures transformers remain central to reliable and sustainable global power distribution networks.

The Shell Core Transformer Market shows strong presence across Asia-Pacific, North America, Europe, Latin America, and the Middle East & Africa. Asia-Pacific leads growth with rapid electrification and industrial expansion, while North America and Europe emphasize grid modernization and efficiency standards. Latin America and Middle East & Africa expand through infrastructure development and renewable projects. Key players shaping the market include Siemens, ABB, GE Co, Schneider Electric, Mitsubishi Electric Corporation, Hyundai Heavy Industries, Crompton Greaves, BHEL, Alstom SA, and Kirloskar Electric.

Market Insights

- Shell Core Transformer Market size was valued at USD 23652.6 million in 2024 and is anticipated to reach USD 38560.7 million by 2032, at a CAGR of 6.3%.

- Rising electricity demand, grid modernization, and renewable energy integration drive market growth.

- Stricter efficiency standards and eco-friendly insulation materials shape major market trends.

- Competition remains strong with global players focusing on smart grid and digital solutions.

- High manufacturing costs and supply chain issues act as restraints for the market.

- Asia-Pacific leads growth, while North America and Europe focus on modernization and efficiency.

- Latin America and Middle East & Africa expand with infrastructure projects and renewable integration.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Reliable Power Distribution

The Shell Core Transformer Market expands with increasing electricity demand from industrial, commercial, and residential sectors. It supports grid stability by handling high load fluctuations effectively. Rapid urbanization creates a consistent requirement for advanced transformers that ensure uninterrupted power. Governments push for improved power infrastructure to reduce energy losses. This drives investments in modern, high-capacity shell core designs. It ensures transformers remain essential for both new installations and replacement of outdated units.

- For instance, Kirloskar Electric supplied multiple transformers—40 MVA at 33/11.5 kV and 16 MVA at 11/3.45 kV—to various power projects, validated through short-circuit testing at CPRI, enhancing load-handling capacity.

Integration of Renewable Energy into Power Grids

The Shell Core Transformer Market gains traction through renewable energy integration. Wind and solar plants require efficient transformers to manage variable outputs. It ensures smooth transmission from generation sources to distribution networks. Growing renewable projects worldwide fuel the demand for high-performance designs. These transformers enhance energy transfer efficiency and reduce operational losses. Utilities adopt shell core technology to handle renewable-based grid fluctuations. It secures the market’s position in global energy transition strategies.

- For instance, GE Vernova is set to supply over 70 units of 765 kV-class extra high-voltage transformers and shunt reactors to POWERGRID, to support India’s renewable power corridors.

Regulatory Push for Efficiency and Sustainability

The Shell Core Transformer Market benefits from stricter government regulations on efficiency and sustainability. Policies encourage the adoption of eco-friendly insulation and cooling systems. It aligns with global efforts to reduce carbon footprints in energy infrastructure. Efficiency-focused standards push utilities toward advanced transformer designs. Manufacturers respond with innovations that improve performance while lowering energy consumption. These regulatory measures strengthen demand for shell core units across regions. It ensures the market continues evolving with sustainable practices.

Advancements in Digital Monitoring and Smart Grid Integration

The Shell Core Transformer Market strengthens with rising adoption of smart grid technologies. Digital monitoring solutions improve predictive maintenance and operational reliability. It allows utilities to detect faults early and optimize transformer performance. Integration with IoT and automation systems boosts demand for intelligent units. These capabilities extend equipment life and reduce downtime risks. The adoption of smart-enabled transformers creates new growth opportunities. It drives continuous innovation and technological advancements in the sector.

Market Trends

Growing Shift Toward Smart and Digital Transformers

The Shell Core Transformer Market evolves with stronger adoption of smart technologies. Utilities deploy digital monitoring systems to track performance and predict failures. It reduces downtime and enhances operational reliability across power networks. Smart features such as IoT integration and remote diagnostics expand transformer functionality. The demand for intelligent solutions grows with modernization of aging grids. This trend reinforces investment in advanced shell core designs that support automation. It secures the role of smart transformers in global energy infrastructure.

- For instance, Crompton Greaves also produces compact SLIM® transformers using DuPont Nomex® insulation, offering high overload capacity. The models span ratings from 25 kVA up to 1,500 MVA, and voltage classes from 11 kV to 765 kV.

Rising Preference for Eco-Friendly and Sustainable Designs

The Shell Core Transformer Market advances with the use of eco-friendly materials and insulation. Governments encourage low-loss and energy-efficient transformers to meet emission targets. It creates opportunities for products that comply with strict environmental standards. Manufacturers introduce biodegradable insulating fluids and recyclable components. Demand for green solutions aligns with global decarbonization goals. This trend strengthens the adoption of sustainable shell core models in utility and industrial sectors. It pushes the market toward long-term environmental responsibility.

- For instance, Siemens delivered an 8.8 MVA, 66 kV FITformer® REN transformer filled with biodegradable ester fluid. This unit, designed for wind-turbine nacelle installation, uses ester insulation to enhance safety and thermal performance while reducing environmental risk.

Expansion of Renewable Energy Integration in Grids

The Shell Core Transformer Market adapts to rapid growth in renewable power projects. Wind, solar, and hydro plants require efficient transformers for grid connection. It ensures stable transmission despite the variability of renewable generation. Utilities prefer shell core transformers for handling fluctuating loads and high capacity needs. Renewable integration projects in emerging economies fuel higher demand. This trend highlights the importance of reliable designs that support energy transition. It positions shell core units as critical enablers of clean power distribution.

Increasing Demand for Compact and High-Capacity Models

The Shell Core Transformer Market responds to urbanization and industrial growth with compact solutions. Space-constrained cities adopt smaller transformers without compromising performance. It provides flexibility for installation in dense commercial and residential areas. High-capacity units remain vital for industrial facilities and large-scale projects. This dual demand drives innovations in design, cooling, and insulation. Manufacturers develop versatile products to serve both urban and heavy-duty applications. It ensures the market adapts to diverse infrastructure requirements worldwide.

Market Challenges Analysis

High Manufacturing Costs and Supply Chain Constraints

The Shell Core Transformer Market faces challenges from high production costs and supply chain disruptions. Manufacturing requires advanced materials such as high-grade steel and specialized insulation, which remain expensive. It creates pricing pressure for producers while reducing affordability for utilities. Fluctuations in raw material availability and transportation delays affect delivery schedules. Global supply chain risks also limit timely execution of infrastructure projects. Rising costs for labor and skilled technicians further intensify market pressures. It forces companies to balance profitability with competitive pricing strategies.

Operational Risks and Technical Limitations

The Shell Core Transformer Market encounters challenges linked to technical complexity and operational risks. Transformers demand consistent maintenance to avoid overheating, oil leaks, or insulation failures. It increases operational costs for utilities and industries relying on large networks. Aging infrastructure in many regions struggles to integrate modern shell core designs. Compatibility issues with smart grid systems add further complexity. Downtime from equipment malfunction disrupts power supply and impacts reliability. It underscores the need for continuous innovation to overcome technical and operational hurdles.

Market Opportunities

Expansion of Renewable and Smart Grid Projects

The Shell Core Transformer Market presents strong opportunities through global renewable energy expansion. Wind and solar plants require advanced transformers for efficient integration into grids. It supports the shift toward clean power and strengthens grid resilience. Governments fund large-scale renewable projects, creating sustained demand for modern equipment. Smart grid initiatives expand adoption of digitally enabled transformers with predictive monitoring features. These projects enhance efficiency and align with long-term sustainability goals. It positions shell core technology as a key enabler of future-ready energy systems.

Rising Demand from Emerging Economies and Industrial Growth

The Shell Core Transformer Market benefits from infrastructure development in emerging economies. Rapid urbanization drives investment in reliable power distribution across commercial and residential sectors. It supports industrial growth by supplying stable energy for large manufacturing hubs. Compact and high-capacity models address diverse needs in dense urban areas and heavy industries. Utilities in developing regions prioritize modernization to reduce transmission losses and improve reliability. These conditions create broad opportunities for manufacturers offering adaptable designs. It ensures the market continues to expand into untapped regions worldwide.

Market Segmentation Analysis:

By Product

The Shell Core Transformer Market divides into distribution, power, instrument, and other transformers. Distribution transformers hold a major share due to widespread use in residential and commercial networks. It supports reliable electricity delivery across urban and rural areas. Power transformers dominate large-scale industrial and utility applications, where high capacity is essential. Instrument transformers remain vital for measuring, monitoring, and protecting electrical systems. Other transformer types serve niche applications, contributing to overall flexibility in power infrastructure. It ensures balanced adoption across diverse end-user requirements.

- For instance, ABB also developed the most powerful ultrahigh‑voltage DC (UHVDC) transformer, rated at ±1,100 kV. Testing confirmed this transformer meets the exacting demands of the Changji–Guquan UHVDC link, capable of transmitting 12,000 MW over more than 3,000 km—marking a new global standard in voltage and distance.

By Core

The market segments into closed, shell, and berry core designs. Shell core transformers gain preference for their ability to handle high loads with reduced leakage flux. It enhances efficiency and stability in large installations. Closed core transformers remain relevant for standard distribution and small-scale needs. Berry core designs, though less common, serve specialized applications with circular winding arrangements. Growing demand for shell core types reflects the trend toward high-performance, durable systems. It strengthens the position of shell core units in modern grid architecture.

- For instance, Mitsubishi Electric manufactured a three-phase generator step-up transformer for the world’s largest-capacity nuclear power plant, rated at 1,510 MVA.

By Winding

The Shell Core Transformer Market further segments into two winding and auto transformer types. Two winding transformers dominate due to their wide use in transmission and distribution systems. It allows isolation between primary and secondary circuits, improving safety and reliability. Auto transformers attract demand for cost efficiency and compact design, especially in industrial applications. Their smaller size reduces material costs while maintaining functional performance. Utilities deploy both designs based on application-specific needs and operational priorities. It highlights the adaptability of transformer technology to varying load conditions.

Segments:

Based on Product:

- Distribution Transformer

- Power Transformer

Based on Core:

Based on Winding:

- Two Winding

- Auto Transformer

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for about 25% of the Shell Core Transformer Market. The U.S. and Canada focus on grid modernization and renewable energy adoption. It drives strong demand for efficient and reliable transformers. Growing data centers also add pressure on energy networks, increasing the need for advanced units. Utilities adopt smart monitoring features to improve reliability and reduce losses. It keeps North America a key market for modern shell core designs.

Europe

Europe contributes about 20% of the Shell Core Transformer Market. The region invests in replacing aging grids and meeting strict energy-efficiency standards. It drives steady adoption of low-loss and eco-friendly shell core models. Renewable projects, especially wind and solar, further support demand. Utilities across Europe prefer compact and durable designs for reliable performance. It ensures Europe maintains a stable and consistent share of the market.

Asia-Pacific

Asia-Pacific holds the largest share with around 40% of the Shell Core Transformer Market. China, India, and Southeast Asia lead demand due to urbanization and industrial growth. It supports electrification projects, renewable power integration, and smart city development. Compact transformers gain popularity in space-constrained urban centers. High-capacity models serve factories and heavy industries across the region. It remains the fastest-growing regional market with strong government investments in energy.

Latin America

Latin America represents nearly 8% of the Shell Core Transformer Market. Countries such as Brazil, Mexico, and Chile expand renewable projects and urban power systems. It creates opportunities for both compact distribution units and larger industrial transformers. Rural electrification programs also drive adoption. The region shows gradual but steady growth with rising infrastructure investment. It builds demand for reliable and cost-effective transformer solutions.

Middle East & Africa

The Middle East & Africa hold about 7% of the Shell Core Transformer Market. Gulf nations invest heavily in infrastructure and renewable power, especially solar projects. It supports growth in demand for large-capacity transformers. African countries expand grid coverage to meet growing electricity needs. Utilities prioritize durable and efficient designs to handle rising consumption. It highlights the growing role of shell core technology in regional power systems.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The Shell Core Transformer Market players such as such as Hyundai Heavy Industries Co. Ltd., Kirloskar Electric, GE Co, Crompton Greaves, Siemens, ABB, Mitsubishi Electric Corporation, Schneider Electric, BHEL, and Alstom SA. The Shell Core Transformer Market is shaped by rising demand for efficient, reliable, and sustainable power distribution solutions. Companies emphasize advanced designs that support grid modernization, renewable energy integration, and urban infrastructure growth. Innovation in smart monitoring, eco-friendly insulation, and high-capacity performance drives adoption across utilities and industries. The market also reflects strong competition, with firms investing in R&D, expanding global presence, and targeting diverse end-user needs. Growing focus on digitalization and predictive maintenance further accelerates transformation in this sector. It ensures the market continues evolving to meet both present and future energy challenges.

Recent Developments

- In October 2024, IMEFY Group secured an 8-year contract with Enedis, France’s leading energy distribution company, for the supply of over 12,000 oil and resin-based transformers. This milestone strengthened IMEFY’s footprint in the French market and deepened its collaboration with Enedis, a company committed to modernizing sustainable energy infrastructure.

- In July 2024, Hyosung Heavy Industries secured a contract to supply 420 kV high-voltage transformers to Norway’s Statnett. The project aimed to enhance renewable energy infrastructure and replace aging facilities by 2029. Featuring advanced technology, the transformers are designed for efficient energy transmission over long distances while reducing energy loss.

- In July 2024, CG Power announced investment to complete its capacity expansion within 18 months, focusing on scaling up production for transformers, motors, and switchgears. The company also ventured into semiconductor manufacturing and initiated development of an Outsourced Assembly and Testing (OSAT) facility in Gujarat, reinforcing its strategic growth in high-demand sectors.

- In January 2024, ABB launched over 20 new products during its Electrification Innovation Week, including a next‑generation solid‑state DC circuit breaker and smart grid components.

Report Coverage

The research report offers an in-depth analysis based on Product, Core, Winding and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Shell Core Transformer Market will grow with rising demand for efficient power distribution.

- Renewable energy expansion will increase adoption of high-capacity and durable shell core designs.

- Smart grid integration will drive demand for transformers with digital monitoring features.

- Eco-friendly insulation materials will gain importance under stricter environmental regulations.

- Compact models will see higher use in space-constrained urban and commercial areas.

- Industrial growth will create steady demand for large-capacity shell core units.

- Utilities will invest more in predictive maintenance and advanced monitoring technologies.

- Emerging economies will offer strong opportunities through infrastructure expansion and electrification.

- Replacement of aging grid infrastructure will continue to support market growth.

- Continuous innovation will enhance transformer efficiency, safety, and long-term reliability.