| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Spain Human Insulin Market Size 2023 |

USD 428.04 Million |

| Spain Human Insulin Market, CAGR |

2.65% |

| Spain Human Insulin Market Size 2032 |

USD 541.98 Million |

Market Overview

Spain Human Insulin market size was valued at USD 428.04 million in 2023 and is anticipated to reach USD 541.98 million by 2032, at a CAGR of 2.65% during the forecast period (2023-2032).

The Spain human insulin market is primarily driven by the growing prevalence of diabetes, with an increasing number of patients requiring insulin for effective management. Advances in insulin delivery systems, including insulin pens and pumps, are improving patient convenience and adherence to treatment. Additionally, rising awareness about diabetes management and the importance of timely insulin administration is fueling market growth. The growing focus on personalized medicine and the development of new insulin formulations, such as biosimilars and long-acting insulins, are also contributing to market expansion. Furthermore, the Spanish healthcare system’s strong infrastructure, along with government support for diabetes care, is enhancing access to insulin therapies. As the demand for better diabetes care continues to rise, the market is expected to experience steady growth. Overall, these factors are driving the market, with increased investment in research and development pushing innovation and improving treatment options for diabetes patients.

Geographically, the Spain human insulin market exhibits varied demand across different regions, with urban centers such as Madrid and Barcelona leading in terms of insulin usage due to their higher population densities and advanced healthcare infrastructure. Coastal regions like Valencia and Málaga also show significant demand, driven by an aging population and increasing diabetes prevalence. Rural areas, although facing challenges in healthcare access, are experiencing steady growth as efforts to improve healthcare reach these regions. Key players in the Spain human insulin market include major global pharmaceutical companies like Novo Nordisk, Eli Lilly, and Pfizer, who dominate with their established insulin products and innovative diabetes management solutions. Additionally, companies such as Biocon, Wockhardt, and MannKind Corporation are making their mark with biosimilars and alternative insulin therapies, contributing to the growing variety of treatment options. These key players are focused on expanding their presence and meeting the increasing demand for insulin therapies across the country.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Spain human insulin market was valued at USD 428.04 million in 2023 and is expected to reach USD 541.98 million by 2032, growing at a CAGR of 2.65% during the forecast period.

- The global human insulin market was valued at USD 21,000 million in 2023 and is projected to reach USD 31,208 million by 2032, growing at a CAGR of 4.50% from 2023 to 2032.

- The rising prevalence of diabetes in Spain is driving the demand for insulin therapies, with more patients requiring consistent treatment.

- Technological advancements in insulin delivery systems, such as insulin pens, pumps, and continuous glucose monitoring devices, are fueling market growth.

- The increasing adoption of biosimilars offers cost-effective alternatives, helping to improve the affordability of insulin treatments.

- Key players like Novo Nordisk, Eli Lilly, and Pfizer are dominating the market, focusing on innovative products and expanding their portfolios.

- Regulatory challenges and high insulin costs are significant restraints, impacting patient access to affordable treatment options.

- Urban centers like Madrid and Barcelona dominate the market, while rural and coastal regions show increasing demand due to improved healthcare access.

Report Scope

This report segments the Spain Human Insulin Market as follows:

Market Drivers

Rising Diabetes Prevalence

The growing prevalence of diabetes is one of the primary drivers of the human insulin market in Spain. According to the International Diabetes Federation (IDF), the number of people diagnosed with diabetes in Spain is steadily increasing, largely due to factors such as aging populations, sedentary lifestyles, and poor dietary habits. As more individuals are diagnosed with type 1 and type 2 diabetes, the demand for insulin as a treatment option continues to rise. For instance, the International Diabetes Federation (IDF) reports that the number of adults (20–79 years) with diabetes in Spain has increased from 2.0 million in 2000 to 4.7 million in 2024, making Spain one of the countries with the highest diabetes prevalence in the IDF Europe Region. This trend is expected to persist, given the continued aging of Spain’s population and the increasing risk factors associated with modern lifestyles. Consequently, the need for effective insulin therapies remains a significant factor driving market growth.

Technological Advancements in Insulin Delivery Systems

Technological innovations in insulin delivery systems are also playing a crucial role in the expansion of the human insulin market. Devices such as insulin pens, insulin pumps, and continuous glucose monitoring (CGM) systems have revolutionized diabetes management. These advancements provide greater convenience and precision, making it easier for patients to manage their blood sugar levels. Insulin pens, for example, are increasingly preferred over traditional vials and syringes due to their ease of use and reduced risk of dosing errors. Similarly, insulin pumps offer more consistent insulin delivery, while CGM systems help patients track real-time glucose levels, improving treatment outcomes. As these devices become more accessible and affordable, they are expected to further drive the demand for human insulin.

Government Initiatives and Healthcare Infrastructure

The Spanish government plays a key role in supporting diabetes care, contributing significantly to the growth of the human insulin market. Spain’s robust healthcare system provides subsidized access to essential medications and therapies, including insulin, which ensures that diabetes patients receive the necessary treatment. For instance, the European Observatory on Health Systems and Policies reports that Spain’s National Health System (SNS) provides virtually universal coverage, with healthcare primarily funded through taxes. Additionally, the government’s focus on improving healthcare infrastructure and increasing awareness of diabetes management further supports market expansion. Policies promoting early detection and prevention of diabetes, as well as initiatives to reduce healthcare costs, are expected to increase the number of patients receiving insulin therapies. This growing support and improved access to healthcare services are key market drivers.

Innovations in Insulin Formulations and Biosimilars

Ongoing research and development in the field of human insulin are paving the way for new insulin formulations and biosimilars, which are expected to fuel market growth. Long-acting insulins, rapid-acting insulins, and combinations of different insulin types are becoming more widely available, offering patients more tailored treatment options based on their specific needs. Additionally, the emergence of biosimilars is contributing to greater affordability and availability of insulin therapies. These biologically similar alternatives to branded insulin products are expected to drive down treatment costs while maintaining the same therapeutic benefits. As innovation continues to progress, new insulin formulations and biosimilars are likely to attract more patients, thereby expanding the market.

Market Trends

Shift Towards Biosimilar Insulins

One of the most significant trends in the Spain human insulin market is the growing adoption of biosimilar insulins. These insulin products are designed to be highly similar to existing biologic insulin therapies, providing comparable therapeutic outcomes at a more affordable price. The increased availability of biosimilars presents a cost-effective alternative to traditional insulin therapies, which is crucial as the diabetes burden continues to rise. With the pressure on healthcare systems to control spending, biosimilars offer an opportunity to maintain high-quality care while reducing treatment costs for both patients and providers. The Spanish government’s support for biosimilars, including their reimbursement and inclusion in national treatment guidelines, further drives this trend. As the acceptance of biosimilars grows, they are expected to become a dominant segment within the insulin market, contributing to enhanced accessibility and sustainability of diabetes care in Spain.

Technological Advancements in Insulin Delivery Systems

Technological innovations in insulin delivery systems have also significantly shaped the Spanish human insulin market. Insulin pens have become particularly popular in Spain due to their ease of use, portability, and reduced dosing errors compared to traditional syringes. Insulin pumps, which deliver a continuous supply of insulin, allow for a more controlled and personalized approach to diabetes management. For instance, the Spain Diabetes Care Devices Market report highlights the growing adoption of continuous glucose monitoring (CGM) systems and smart insulin delivery devices, which offer real-time data and improved patient convenience. Moreover, CGM systems, which monitor glucose levels in real time, have gained significant traction among patients and healthcare providers alike, facilitating more dynamic and accurate insulin dosing. These advancements improve patient adherence to insulin regimens, leading to better control of blood glucose levels and reduced complications. As technology continues to evolve, the demand for such insulin delivery devices is expected to drive further growth in the market.

Personalized Insulin Therapies

Another emerging trend in the Spain human insulin market is the increasing focus on personalized insulin therapies. As research in the field of diabetes advances, healthcare providers are placing more emphasis on tailoring insulin treatment to individual patient needs. Personalized insulin therapies take into account factors such as a patient’s age, lifestyle, activity levels, genetic predisposition, and the specific type and progression of diabetes. This approach allows for more effective and precise insulin dosing, resulting in better blood sugar control and reduced risk of complications such as hypoglycemia and hyperglycemia. By moving away from a one-size-fits-all approach, personalized insulin therapies aim to optimize treatment regimens and improve the overall quality of life for diabetes patients. The growing availability of rapid-acting and long-acting insulin formulations further supports this trend, offering patients more flexibility and control over their diabetes management. As the demand for customized diabetes care rises, personalized insulin therapies are likely to become an integral part of the Spanish insulin market.

Government Initiatives and Healthcare Infrastructure

The Spanish government’s ongoing initiatives to support diabetes care are a critical factor influencing the human insulin market. Spain boasts a strong and accessible healthcare system that provides subsidized access to essential medications, including insulin. For instance, the European Observatory on Health Systems and Policies reports that Spain’s National Health System (SNS) provides virtually universal coverage, with healthcare primarily funded through taxes. This ensures that patients, particularly those with low-income backgrounds, are able to receive the necessary treatment for diabetes management. Furthermore, the Spanish government has implemented policies to promote early detection, prevention, and management of diabetes, which has led to increased awareness and better disease control across the population. These policies include national screening programs and campaigns aimed at educating the public about healthy lifestyles and the risks associated with diabetes. As Spain continues to invest in healthcare infrastructure and increase funding for diabetes-related research, the market for human insulin is expected to grow steadily. Additionally, efforts to streamline the distribution of insulin and related devices, along with favorable reimbursement policies, are further driving market expansion.

Market Challenges Analysis

High Cost of Insulin and Associated Therapies

A major challenge facing the Spain human insulin market is the high cost of insulin and associated diabetes therapies. Despite the availability of biosimilars and technological advancements in insulin delivery systems, insulin remains a significant financial burden for many patients, especially those without adequate insurance coverage or financial support. The high costs of insulin, coupled with the need for ongoing monitoring and specialized devices such as insulin pumps and continuous glucose monitors (CGMs), can strain both patients and healthcare systems. Although the Spanish government subsidizes a portion of these costs, there are concerns about the sustainability of these subsidies as the number of diabetic patients continues to rise. The financial burden on patients can lead to medication non-adherence or improper management of diabetes, which in turn results in higher healthcare costs due to complications. Addressing these cost-related barriers is critical for improving access to care and ensuring better patient outcomes.

Regulatory Hurdles and Market Entry Barriers

Another challenge for the Spain human insulin market is the complex regulatory environment and market entry barriers faced by new insulin products. While the approval process for insulin formulations is generally well-established, the stringent regulatory requirements imposed by the European Medicines Agency (EMA) and other local regulatory bodies can slow down the introduction of new products, including biosimilars and innovative insulin formulations. The lengthy approval process can delay market access for new therapies that might offer better efficacy or affordability. For instance, the OECD Regulatory Policy Outlook 2025 highlights Spain’s efforts to improve regulatory impact assessments (RIA) and streamline approval processes. Additionally, competition in the insulin market, particularly from established multinational pharmaceutical companies, creates barriers for smaller players looking to enter the market with new alternatives. Regulatory challenges, coupled with the competitive nature of the market, can limit the diversity of insulin products available to patients and hinder the development of more cost-effective solutions. Streamlining the approval process and reducing market entry barriers would help alleviate some of these challenges and foster greater innovation within the insulin market.

Market Opportunities

The Spain human insulin market presents significant opportunities driven by a growing diabetic population and increasing demand for innovative treatment options. As the number of people diagnosed with diabetes continues to rise, there is a pressing need for more affordable, accessible, and effective insulin therapies. The increasing focus on biosimilars in Spain offers a key opportunity for market growth. Biosimilars provide cost-effective alternatives to traditional insulin products, making diabetes treatment more affordable for patients and healthcare systems alike. With biosimilars gaining regulatory approval and increasing acceptance among healthcare providers, their expanded use is expected to drive market expansion. Furthermore, advancements in insulin formulations, such as long-acting and rapid-acting insulin options, offer patients more flexibility in managing their blood glucose levels, creating new market opportunities for both established and emerging companies.

Additionally, the integration of new technologies into diabetes care presents considerable growth potential in the Spanish market. The widespread adoption of insulin pumps, continuous glucose monitoring (CGM) systems, and smart insulin pens is transforming how patients manage their condition, improving both the convenience and accuracy of insulin delivery. These devices enable better glucose control and personalized treatment, fostering improved patient outcomes. As patients increasingly seek more advanced and convenient diabetes management solutions, the demand for technologically enhanced insulin therapies will rise. Additionally, the Spanish government’s ongoing support for diabetes care, coupled with public awareness campaigns aimed at early detection and prevention, further boosts market opportunities. The combination of technological advancements, government initiatives, and the growing demand for affordable, personalized insulin therapies positions the Spain human insulin market for sustained growth in the coming years.

Market Segmentation Analysis:

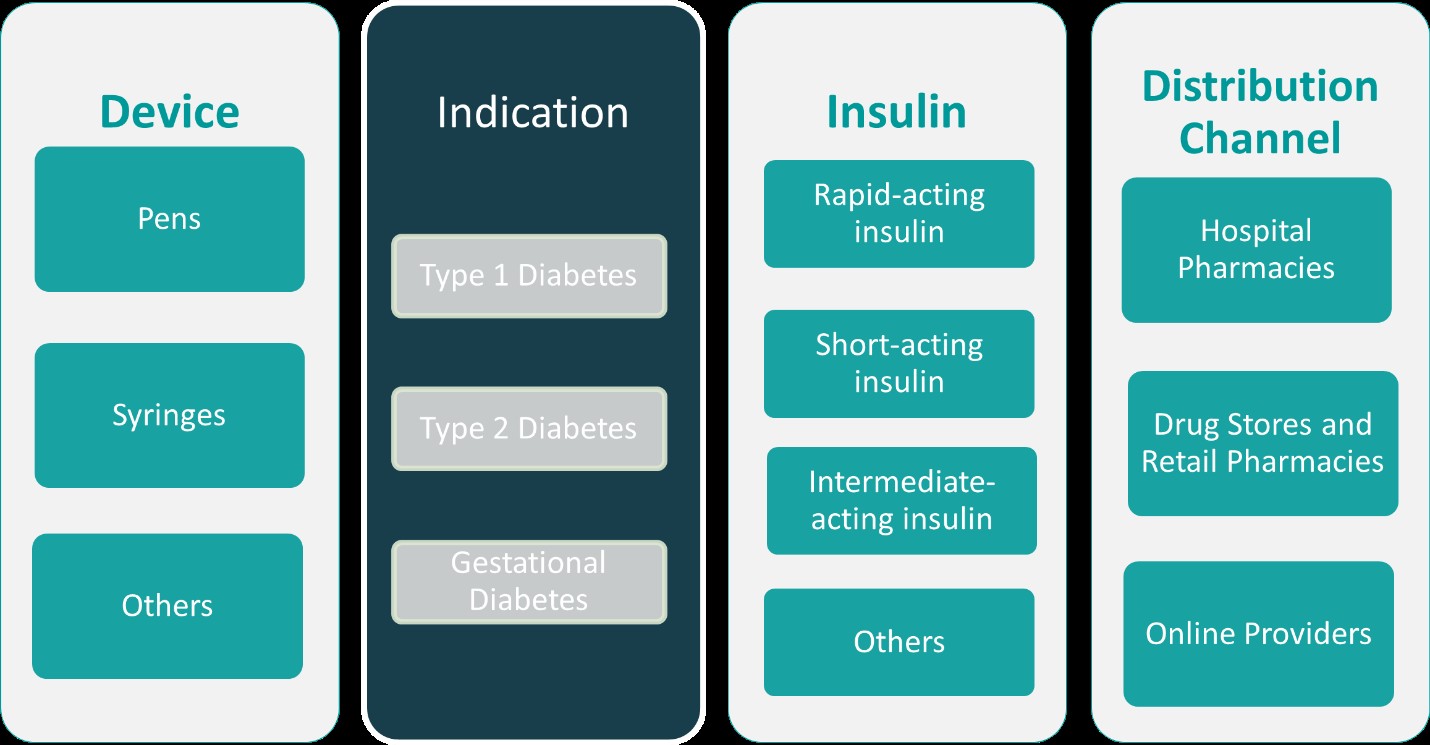

By Device:

The Spain human insulin market can be segmented based on the type of device used for insulin delivery, including pens, syringes, and other devices such as insulin pumps and continuous glucose monitoring (CGM) systems. Insulin pens have become the dominant delivery method in Spain due to their user-friendly design, portability, and improved accuracy compared to traditional syringes. The convenience of insulin pens, which allow for precise dosing and ease of use, has led to their increasing adoption among both patients and healthcare providers. Syringes, though still in use, are less preferred due to their more complex administration and higher risk of dosing errors. However, they remain relevant in certain patient populations, especially those who prefer lower-cost alternatives. Other devices, such as insulin pumps and CGMs, are becoming increasingly popular, particularly for patients with more complex diabetes management needs, offering continuous insulin delivery and real-time blood glucose monitoring. These devices are expected to experience strong growth, driven by technological advancements and greater patient awareness of their benefits.

By Indication:

The human insulin market in Spain is also segmented by the type of diabetes for which the insulin is prescribed: Type 1, Type 2, and gestational diabetes. Type 1 diabetes, typically diagnosed in childhood or adolescence, requires insulin for life, making it a key segment of the market. The demand for insulin in Type 1 diabetes is stable and remains significant due to the lifelong dependence on insulin therapy. Type 2 diabetes, which is more prevalent in adults and is often linked to lifestyle factors, is the largest segment in the market. Type 2 patients may require insulin as the disease progresses, particularly if oral medications are no longer effective. This segment is experiencing growth due to the rising incidence of obesity and sedentary lifestyles. Gestational diabetes, though less common, represents a critical segment as it affects pregnant women and requires careful management to avoid complications. The increasing awareness and early detection of gestational diabetes in Spain are expected to drive demand for insulin therapies in this group.

Segments:

Based on Device:

Based on Indication:

- Type 1 Diabetes

- Type 2 Diabetes

- Gestational Diabetes

Based on Insulin:

- Rapid-acting insulin

- Short-acting insulin

- Intermediate-acting insulin

- Others

Based on Distribution Channel:

- Hospital Pharmacies

- Drug Stores and Retail Pharmacies

- Online Providers

Based on the Geography:

- Urban Centers (Madrid, Barcelona)

- Rural Areas

- Coastal regions

Regional Analysis

Urban Centers (Madrid, Barcelona)

Urban centers such as Madrid and Barcelona represent the largest portion of the Spain human insulin market, accounting for approximately 60% of the total market share. These areas have high population densities, with a significant proportion of individuals diagnosed with diabetes. Urban centers are home to well-developed healthcare infrastructures, including access to specialized diabetes care, advanced insulin delivery systems, and insulin prescriptions. Additionally, these regions see higher adoption rates of innovative diabetes management technologies, such as insulin pumps and continuous glucose monitoring (CGM) systems. With greater access to healthcare professionals and better awareness of diabetes management, urban centers continue to drive the majority of the market’s growth.

Rural Areas

Rural areas, while contributing to a smaller market share, account for roughly 25% of the Spain human insulin market. These regions often face challenges related to healthcare accessibility and lower levels of healthcare infrastructure. Patients living in rural areas may experience limited access to specialized care and cutting-edge diabetes management technologies, which can impact insulin treatment outcomes. However, despite these challenges, rural regions exhibit steady demand for insulin, as the prevalence of diabetes continues to rise across the country. Government initiatives aimed at improving healthcare access in these regions, along with mobile healthcare units and telemedicine services, are expected to help expand insulin availability in rural areas over time.

Coastal Regions

Coastal regions in Spain, such as Valencia, Málaga, and the Canary Islands, hold a market share of approximately 15%. These regions have seen an increase in diabetes prevalence, partly due to their aging populations and rising lifestyle-related risk factors. Healthcare access in coastal areas is generally better than in rural regions, with several major cities and hospitals providing specialized care. The demand for human insulin is growing as more residents, including both local populations and expatriates, require diabetes management. The popularity of advanced insulin delivery systems is also rising in these regions, with more patients turning to insulin pens, pumps, and CGMs for improved blood sugar control.

Key Player Analysis

- Novo Nordisk A/S

- MannKind Corporation

- Pfizer

- Wockhardt

- Biocon

- Lupin

- Tonghua Dongbao Pharmaceutical Co

- Eli Lilly and Company

- Dexcom

Competitive Analysis

The Spanish human insulin market is highly competitive, with several key players dominating the sector. These companies include Novo Nordisk, Sanofi, Boehringer Ingelheim, Lilly, and Bayer, which are notable for their established presence in the industry. Key market dynamics include the increasing prevalence of diabetes, which drives the demand for insulin products, and the growing adoption of biosimilars, which is influencing pricing and competition. The market is also shaped by the need for continuous research and development to create advanced insulin formulations that offer improved control over blood sugar levels with fewer side effects. Companies are also focusing on expanding their portfolios to cover both short-acting and long-acting insulin to meet the diverse needs of patients with Type 1 and Type 2 diabetes.

The presence of biosimilars is creating an environment of price competition, which pressures both established and newer entrants to offer cost-effective solutions while maintaining high-quality standards. Patient education and accessibility to insulin therapy are also key factors that companies are leveraging to gain a competitive edge. In addition, strategic partnerships and collaborations with healthcare professionals and diabetic care organizations are becoming an essential component for players looking to strengthen their market presence and improve patient outcomes. Regulatory frameworks and pricing policies also significantly impact competitive strategies in the Spanish market.

Recent Developments

- In April 2025, Novo Nordisk announced the discontinuation of Human Mixtard, India’s largest-selling human insulin brand, as part of a global strategy to prioritize newer, patented diabetes and weight loss therapies such as Ozempic and Wegovy. While vial forms of Mixtard, Actrapid, and Insulatard will remain available, pen devices (Penfills and FlexPens) are being phased out, which is expected to disrupt patient access and preference in India.

- In April 2025, Pfizer discontinued the development of danuglipron, its once-daily oral GLP-1 receptor agonist for obesity and type 2 diabetes, following a case of drug-induced liver injury and after reviewing clinical and regulatory feedback. This decision halts further clinical development for both obesity and diabetes indications.

- In March 2025, Biocon Biologics entered a strategic collaboration with Civica, Inc. to expand access to Insulin Aspart in the United States. Biocon will supply the drug substance, which Civica will formulate and commercialize after completing development and clinical trials.

- In December 2024, Lupin acquired the Huminsulin® portfolio in India from Eli Lilly and Company. The range includes Insulin Human (Huminsulin R, NPH, 50/50, and 30/70) and is indicated for type 1 and type 2 diabetes. Lupin had previously marketed these products under a distribution agreement, and the acquisition is aimed at strengthening its diabetes portfolio.

- In November 2024, MannKind’s Afrezza® (insulin human) Inhalation Powder received approval from India’s CDSCO. MannKind expects to ship product to its partner Cipla by the end of 2025.

- In October 2024, Wockhardt filed for approval of its fast-acting insulin analog, Aspart injection (ASPARAPID™), with the Drugs Controller General of India (DCGI). The product, developed indigenously, will be offered in cartridges, vials, and prefilled disposable pens. This expands Wockhardt’s diabetes biosimilars portfolio and addresses a market with limited competition.

Market Concentration & Characteristics

The Spanish human insulin market exhibits a moderate to high level of concentration, with a few dominant players controlling a significant share of the market. These companies leverage their established brand recognition, extensive distribution networks, and ongoing research and development to maintain a strong foothold. The market is characterized by a steady demand driven by the rising prevalence of diabetes, alongside an increasing shift towards more affordable biosimilar insulin options. As such, competition is intensifying, particularly in the biosimilars segment, where price sensitivity plays a crucial role in market dynamics. Additionally, there is a growing emphasis on offering innovative insulin formulations with improved efficacy and patient comfort. The market is also influenced by stringent regulatory requirements, which ensure high standards of safety and efficacy. Patient access, education, and support programs are becoming integral to company strategies, contributing to the overall competitive landscape and shaping future growth in the sector.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Device, Indication, Insulin, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The demand for human insulin in Spain is expected to rise due to the growing prevalence of diabetes.

- Biosimilars will continue to gain market share, offering more affordable insulin options for patients.

- Companies will focus on developing long-acting insulin formulations for better blood sugar control.

- The Spanish government’s pricing and reimbursement policies will influence market dynamics.

- Innovation in insulin delivery methods, such as insulin pumps and pens, will drive patient convenience.

- There will be an increasing emphasis on personalized diabetes treatment approaches.

- Digital health tools, such as apps and continuous glucose monitors, will complement insulin therapies.

- Strategic partnerships and collaborations between companies and healthcare providers will enhance market access.

- The rise of telemedicine and remote monitoring will facilitate better management of diabetes.

- Regulatory approval processes will likely become more streamlined to expedite the availability of new insulin products.