Market Overview:

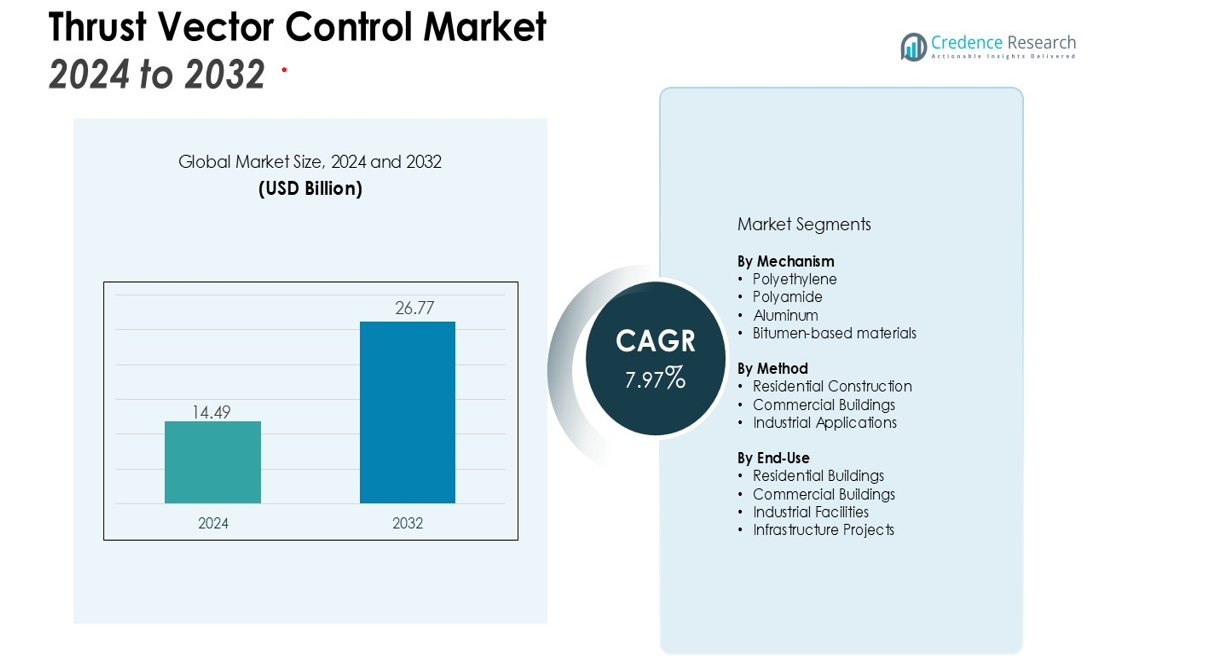

The Thrust Vector Control Market size was valued at USD 14.49 billion in 2024 and is anticipated to reach USD 26.77 billion by 2032, at a CAGR of 7.97% during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Thrust Vector Control Market Size 2024 |

USD 14.49 billion |

| Thrust Vector Control Market, CAGR |

7.97% |

| Thrust Vector Control Market Size 2032 |

USD 26.77 billion |

The primary drivers of the TVC market include the rapid expansion of space missions, particularly satellite launches, and the rising investment in defense and military applications. The need for enhanced precision in controlling missile trajectories and spacecraft during launch and flight is also contributing to market growth. Additionally, the development of reusable launch vehicles (RLVs) and hypersonic technologies is increasing the demand for efficient and reliable thrust vectoring systems, further boosting market expansion.

Regionally, North America dominates the TVC market, accounting for a significant share due to the presence of major players like NASA, SpaceX, and Boeing. Europe and Asia Pacific follow closely, with strong investments in space exploration and defense sectors. The Asia Pacific region is expected to witness the fastest growth due to rising space programs in countries like China and India.

Market Insights:

- The Thrust Vector Control (TVC) market is projected to grow from USD 14.49 billion to USD 26.77 billion by 2032, at a CAGR of 7.97%.

- The expansion of space missions, particularly satellite launches, is driving demand for precise control systems. TVC systems are crucial in ensuring spacecraft maintain accurate trajectories during these missions.

- Military applications are a major growth driver, with the defense sector relying on TVC systems for missile precision and maneuverability. Global defense budgets are increasing, fueling the demand for advanced TVC technologies.

- Advancements in hypersonic technologies and the development of reusable launch vehicles (RLVs) are pushing the need for more efficient and reliable TVC systems. These innovations require precise control over flight paths at high speeds.

- Increased global investment in space infrastructure, such as satellite constellations and space stations, is contributing to the growth of the TVC market. Both governmental and private players are developing advanced propulsion systems that depend on TVC.

- High development and manufacturing costs for TVC systems remain a challenge. Precision engineering and testing requirements make TVC technologies expensive, limiting adoption among smaller organizations.

- Technological complexity and integration issues complicate the widespread use of TVC systems. Integration with other aerospace platforms, such as hypersonic vehicles, presents significant technical barriers that need addressing for smoother deployment.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Growing Demand for Advanced Space Exploration Technologies

The increasing demand for advanced space exploration technologies is a key driver of the Thrust Vector Control (TVC) market. With an expanding number of satellite launches and interplanetary missions, the need for precise control systems is more critical than ever. TVC systems enable spacecraft to maintain accurate trajectories and orientations during launches and flight, ensuring the success of complex missions. The rise in space exploration activities by both governmental space agencies and private space companies is fueling this demand, particularly in regions like North America and Asia.

- For instance, NASA’s Space Launch System (SLS) utilizes four RS-25 engines, with the TVC system on each engine providing up to 512,000 pounds of vacuum thrust to steer the rocket.

Surge in Military and Defense Applications

The defense sector’s growing reliance on TVC systems for missiles and precision-guided munitions is another significant market driver. TVC systems enhance missile maneuverability, offering better guidance and control, especially during high-speed, high-altitude missions. With increasing defense budgets globally, especially in countries like the United States and China, the market for TVC systems is expected to continue expanding. The need for advanced missile systems with higher accuracy is pushing the adoption of Thrust Vector Control technologies in military applications.

Advancements in Hypersonic and Reusable Launch Vehicles

Advancements in hypersonic technologies and the development of reusable launch vehicles (RLVs) are further driving the demand for TVC systems. Hypersonic flight, which requires high maneuverability and control, depends heavily on thrust vectoring for stability and navigation. Similarly, RLVs, which are designed for cost-effective space missions, require reliable TVC systems to ensure reusability and precision. These technological innovations are expected to significantly contribute to the market’s growth.

- For instance, in March 2025, Stratolaunch’s reusable Talon-A2 (TA-2) vehicle successfully completed its second hypersonic flight, exceeding speeds of Mach 5.

Increased Investments in Space Infrastructure

Increased global investment in space infrastructure is helping drive the growth of the Thrust Vector Control market. With countries investing in satellite constellations, space stations, and new launch vehicles, there is a growing need for TVC systems to ensure the efficient operation of these platforms. Private players in the space industry, such as SpaceX and Blue Origin, are also contributing to market growth by developing advanced propulsion and guidance systems that rely on TVC technology to meet the evolving demands of space exploration.

Market Trends:

Increasing Integration of Thrust Vector Control in Reusable Launch Systems

One of the key trends in the Thrust Vector Control (TVC) market is the growing integration of these systems into reusable launch vehicles (RLVs). As the space industry moves towards more sustainable and cost-effective missions, the ability to reuse launch vehicles becomes critical. TVC systems are vital for the controlled descent and landing of these vehicles, ensuring that they can return to Earth safely and be reused for future launches. Companies like SpaceX have pioneered this trend with their Falcon 9 rockets, which rely on TVC to adjust flight paths during re-entry. The success of these missions has highlighted the importance of TVC systems in both commercial and government-funded space missions, driving further innovation and adoption in the space exploration sector.

- For instance, Blue Origin’s New Shepard rocket utilizes TVC for its vertical landings, enabling the booster to be reused for subsequent missions, with each suborbital flight lasting approximately 11 minutes.

Adoption of Advanced TVC Technologies for Hypersonic and Defense Applications

Another significant trend is the adoption of advanced Thrust Vector Control technologies in hypersonic flight and defense applications. The increasing demand for high-performance missile systems, capable of reaching hypersonic speeds, has led to innovations in TVC technology that offer enhanced maneuverability and stability during flight. TVC systems allow for precise control of these high-speed vehicles, which is crucial for avoiding interception and ensuring mission success. Furthermore, the growing geopolitical tensions and military developments globally are pushing defense contractors to integrate more sophisticated TVC systems in their products. This trend supports the need for higher accuracy in defense systems, including missiles and aerospace defense platforms, further expanding the TVC market.

- For instance, DARPA’s OpFires hypersonic missile program uses a throttleable TVC-enabled rocket motor to strike targets up to 1,000 miles away in approximately 20 minutes.

Market Challenges Analysis:

High Development and Manufacturing Costs

One of the key challenges facing the Thrust Vector Control (TVC) market is the high development and manufacturing costs associated with these advanced systems. TVC technology requires precision engineering, complex materials, and extensive testing to ensure reliability and performance under extreme conditions. This makes it a costly investment for both commercial and military applications. Smaller players or organizations with limited budgets may struggle to adopt or scale TVC systems, leading to a concentration of expertise and resources among a few leading companies. High upfront costs can hinder the widespread adoption of TVC technologies, especially in the defense and commercial aerospace sectors.

Technological Complexity and Integration Issues

Another challenge is the technological complexity and integration difficulties associated with TVC systems. As aerospace missions become more sophisticated, integrating TVC systems into various platforms—such as hypersonic vehicles or reusable launch systems—requires overcoming technical barriers. Ensuring that TVC works seamlessly with other guidance and propulsion systems can be difficult, especially with the development of new propulsion methods. Any failure in the integration of these systems can lead to mission delays or failures, increasing the risks and uncertainty associated with their deployment. This complexity poses a significant challenge to companies seeking to expand their use of TVC in advanced aerospace and defense applications.

Market Opportunities:

Expansion of Commercial Space Missions and Satellite Constellations

The growing commercial space industry presents significant opportunities for the Thrust Vector Control (TVC) market. As private companies like SpaceX and Blue Origin expand their satellite constellations and space exploration missions, the demand for efficient propulsion and control systems is increasing. TVC systems are essential for precise navigation and maneuvering of satellites during launch and orbit insertion. These developments in commercial space missions offer a promising growth avenue, as TVC plays a crucial role in ensuring the success and safety of these missions, particularly with the rise of low-cost, high-frequency satellite launches.

Advancements in Hypersonic and Defense Technologies

Another key opportunity lies in the rapid advancements in hypersonic technologies and defense applications. The demand for high-speed, maneuverable vehicles, including missiles and spacecraft, is pushing the need for advanced TVC systems. As countries increase investments in defense capabilities, especially in hypersonic weapons and missile defense systems, the TVC market stands to benefit from the integration of these systems into next-generation aerospace technologies. The increasing emphasis on national security and defense preparedness across various regions will drive continued adoption and innovation in TVC, positioning it as a critical component of military aerospace technology.

Market Segmentation Analysis:

By Mechanism

The Thrust Vector Control (TVC) market is segmented by mechanism into two main types: gimbaled nozzles and jet vanes. Gimbaled nozzles dominate the market due to their ability to provide precise thrust direction control, making them suitable for large-scale space missions and military applications. They offer high maneuverability, making them essential in spacecraft, missiles, and launch vehicles. Jet vanes are also growing in demand, particularly for smaller and mid-sized applications due to their simplicity and cost-effectiveness.

By Method

The TVC market is also segmented by method, with the two primary types being mechanical and fluidic methods. Mechanical methods, which include gimbaled nozzles and jet vanes, remain the dominant choice due to their proven reliability and precision. Fluidic methods, which use aerodynamic control, are gaining traction in specialized applications where weight reduction and fuel efficiency are key priorities. These methods are increasingly being adopted in next-generation hypersonic systems and small satellite platforms.

- For instance, in a study of a fluidic thrust vectoring nozzle, researchers achieved a maximum flow deflection angle of 21.86 degrees, demonstrating a significant control effect without mechanical parts.

By End-User

The Thrust Vector Control market is driven by applications in aerospace and defense sectors. Aerospace leads the market, with demand for TVC systems in satellite launches, interplanetary missions, and reusable launch vehicles. The defense sector also contributes significantly, as TVC systems enhance missile precision, maneuverability, and control in high-speed operations. Both commercial and military applications continue to push innovation in TVC systems, particularly in the context of hypersonic technologies and advanced missile defense.

- For instance, the Space Shuttle’s flight control system utilized thrust vectoring from its three main engines and also controlled the nozzles of its two Solid Rocket Boosters for steering during ascent.

Segmentations:

By Mechanism:

- Gimbaled Nozzles

- Jet Vanes

By Method:

- Mechanical Method

- Fluidic Method

By End-User:

By Application:

- Spacecraft

- Missiles

- Reusable Launch Vehicles

- Hypersonic Systems

By Region:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

North America: Leading the Global Thrust Vector Control Market

North America holds the largest share of the Thrust Vector Control (TVC) market, accounting for 40%. The region benefits from the presence of leading aerospace and defense companies, such as NASA, SpaceX, and Boeing. Strong government funding and private sector investments drive innovation in advanced aerospace technologies. The demand for TVC systems in both commercial space exploration and defense applications continues to grow, driven by increasing satellite launches and the expansion of military capabilities. North America’s established aerospace infrastructure and expertise ensure its dominant position in the global TVC market.

Europe: Significant Contributor to the Thrust Vector Control Market

Europe holds a 30% share of the global TVC market, driven by its strong aerospace and defense sectors. Major aerospace manufacturers, including Airbus and Rolls-Royce, are integrating advanced TVC systems into their spacecraft and missile programs. Government-backed initiatives and private investments in space exploration, coupled with increasing defense budgets, further contribute to the market’s growth. The demand for TVC technology in satellite launches, hypersonic research, and military applications positions Europe for continued market expansion, particularly in countries like the UK, Germany, and France.

Asia Pacific: Fastest Growing Market for Thrust Vector Control

The Asia Pacific region holds a 20% share of the global TVC market and is expected to witness the fastest growth in the coming years. Countries like China and India are investing heavily in space programs, including satellite constellations, lunar missions, and reusable launch vehicles, creating significant demand for TVC systems. The rise in defense budgets, particularly in China and Japan, is also fueling the market’s expansion, with increasing adoption of advanced missile systems. As the region strengthens its aerospace and defense infrastructure, the demand for precise and reliable TVC systems will continue to grow.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- AE Systems

- Moog Inc

- Honeywell International Inc

- Parker-Hannifin Corporation

- Northrop Grumann Corporation

- United Technologies Inc

- Jansen Aircraft Systems Control Inc

- Woodward, Inc

Competitive Analysis:

The Thrust Vector Control (TVC) market is competitive, with key players like NASA, SpaceX, Boeing, and Lockheed Martin leading the industry. These companies dominate through their expertise in aerospace and defense, focusing on advanced TVC systems for satellite launches, reusable launch vehicles, and missile guidance. Smaller players, such as Orbital ATK and Rocket Lab, are capitalizing on niche applications like hypersonic systems and small satellite platforms, offering cost-effective solutions. The market remains dynamic, with increasing competition driven by demand for advanced defense technologies and space infrastructure. Innovation, performance, and cost-efficiency are essential factors for success in this rapidly evolving sector.

Recent Developments:

- In September 2025, BAE Systems and Forterra announced a partnership to develop a prototype of an autonomous Armored Multi-Purpose Vehicle.

- In May 2025, Honeywell partnered with Nutanix to modernize the infrastructure for its Integrated Control and Safety System.

- In September 2025, Woodward announced plans for a new 300,000-square-foot precision manufacturingring facility in South Carolina with a nearly $200 million investment.

Report Coverage:

The research report offers an in-depth analysis based on Mechanism, Method, End-User, Application and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The demand for Thrust Vector Control (TVC) systems will continue to grow with the expansion of space exploration missions and satellite launches.

- Advancements in reusable launch vehicles will drive the need for more reliable and efficient TVC systems, particularly in cost-effective space missions.

- The growing focus on hypersonic technologies will increase the adoption of TVC systems for precise control and maneuverability at high speeds.

- Military applications, including precision-guided missiles and defense systems, will continue to be a significant driver for TVC technology.

- Increasing global investments in space infrastructure, including satellite constellations and space stations, will enhance the demand for TVC systems.

- The Asia Pacific region will see rapid growth, driven by rising investments in space programs and defense sector developments in countries like China and India.

- The integration of TVC systems with advanced propulsion methods will push innovation in both aerospace and defense sectors.

- Small and medium-sized enterprises will increasingly adopt TVC solutions for emerging technologies like small satellite systems and lightweight space vehicles.

- Environmental concerns and sustainability initiatives will encourage the development of eco-friendly TVC systems with reduced fuel consumption and lower environmental impact.

- Strategic partnerships and collaborations among aerospace and defense companies will shape the future development of TVC systems, fostering innovation and market expansion.