Market Overview:

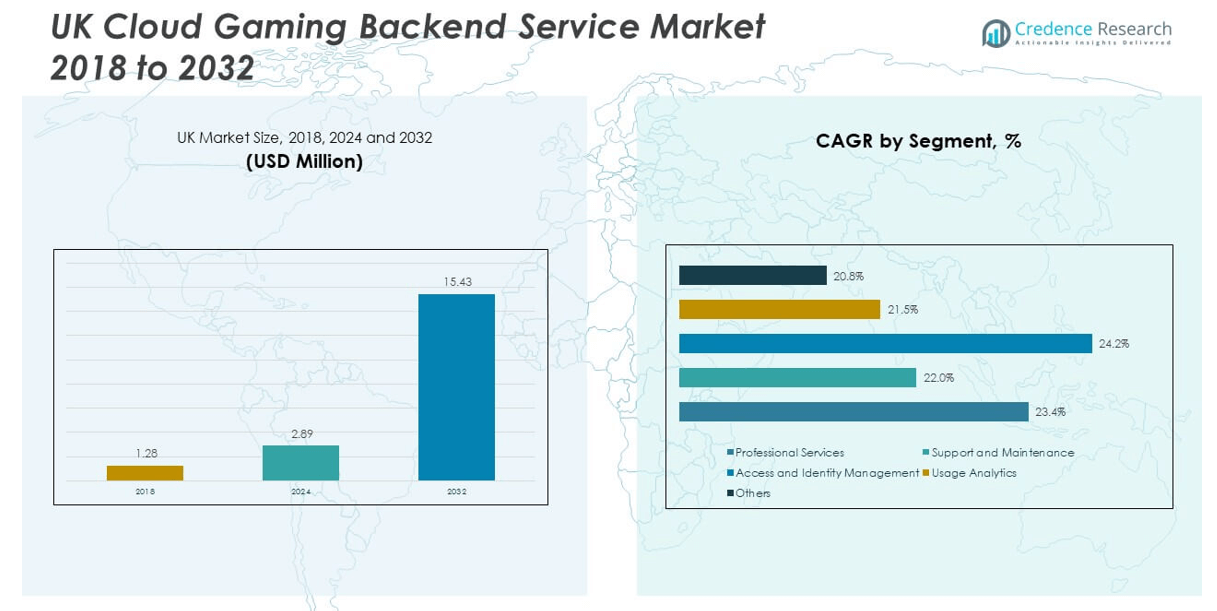

The UK Cloud Gaming Backend Service Market size was valued at USD 1.28 million in 2018 to USD 2.89 million in 2024 and is anticipated to reach USD 15.43 million by 2032, at a CAGR of 22.85% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| U.K. Cloud Gaming Backend Service Market Size 2024 |

USD 2.89 million |

| U.K. Cloud Gaming Backend Service Market, CAGR |

22.85% |

| U.K. Cloud Gaming Backend Service Market Size 2032 |

USD 15.43 million |

The market is driven by the growing adoption of high-speed internet, 5G rollout, and the rising demand for subscription-based gaming services. Cloud-based platforms are enabling gamers to access advanced titles without costly hardware, boosting user engagement across multiple devices. Increasing investment from technology providers and game developers is further expanding the ecosystem, enhancing user experience with low-latency, scalable solutions that support a wider customer base in the UK.

Regionally, Europe holds a strong position in the cloud gaming backend services landscape, with the UK emerging as a key contributor due to its advanced digital infrastructure and high gamer penetration. Countries like Germany and France are also gaining traction, supported by their large gaming communities and network modernization. Meanwhile, Eastern European markets are showing strong growth potential as connectivity improves and consumer adoption increases, indicating opportunities for further expansion across the continent.

Market Insights

- The UK Cloud Gaming Backend Service Market was valued at USD 1.28 million in 2018, reached USD 2.89 million in 2024, and is projected to attain USD 15.43 million by 2032, growing at a CAGR of 22.85%.

- The Global Cloud Gaming Backend Service Market size was valued at USD 93.44 million in 2018 to USD 525.00 million in 2024 and is anticipated to reach USD 3,129.24 million by 2032, at a CAGR of 25.00% during the forecast period.

- England held the largest share with 55% in 2024 due to advanced infrastructure, followed by Scotland at 20% and Wales and Northern Ireland together at 25%, reflecting strong gamer adoption.

- Scotland represents the fastest-growing subregion with 20% share, driven by investments in gaming hubs, broadband expansion, and independent developer adoption of cloud platforms.

- Professional Services accounted for the largest share of the market in 2024, representing 38% of segmental revenue, supported by high demand for integration and implementation.

- Usage Analytics emerged as a rapidly growing segment, capturing 22% in 2024, as providers leverage behavioral insights to optimize user engagement and improve content delivery.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Growing Influence of High-Speed Connectivity and 5G Expansion

The UK Cloud Gaming Backend Service Market is experiencing strong growth driven by the availability of reliable high-speed internet and 5G networks. These technologies ensure faster data transfer, reduced latency, and smoother gameplay, which enhance user satisfaction. It benefits both casual gamers and competitive players seeking uninterrupted experiences. Telecom operators and technology providers are investing heavily in network infrastructure, supporting the scalability of cloud platforms. Widespread adoption of fiber broadband further strengthens backend services. It creates opportunities for developers to design resource-heavy games without hardware limitations. Increasing demand for cross-device accessibility reinforces this trend. Strong government focus on digital infrastructure adds momentum to market growth.

- For example, by mid-2025, BT Group’s 5G Standalone (SA) network covered over 28 million people across 50 UK towns and cities, reaching more than 40 % of the population. Ofcom data shows that 5G SA delivers significantly better performance than non-standalone 5G, with median download speeds around 181.9 Mbps versus 108.6 Mbps, and latency averaging 35 ms on SA compared to 47 ms on older 5G networks.

Rising Popularity of Subscription-Based Gaming Services Among Users

Consumer preference for subscription-based models is shaping the UK Cloud Gaming Backend Service Market. Affordable monthly plans are driving access to large gaming libraries without the need for expensive consoles. It supports a sustainable revenue model for developers and providers while increasing customer retention. These services offer instant access to exclusive titles, strengthening competitive differentiation. Family plans and bundled offers appeal to diverse customer groups, expanding the subscriber base. Major tech companies are building extensive partnerships with gaming studios, enhancing content availability. User convenience across multiple devices adds to the appeal. Growing trust in cloud payment systems fosters further adoption.

Expanding Adoption of Cross-Platform Gaming Experiences in the Market

Cross-platform gaming demand is accelerating the growth of the UK Cloud Gaming Backend Service Market. Players prefer seamless integration across smartphones, tablets, PCs, and consoles. It encourages user engagement by allowing continuity of gameplay across different devices. Developers are optimizing backend services to support these flexible requirements. Game publishers benefit from broader user reach and increased monetization opportunities. Continuous updates and synchronized progress improve loyalty among players. Integration of social features enhances the gaming experience and encourages community building. Expansion of cross-platform esports further boosts this market driver. User demand for uninterrupted cross-device play strengthens the segment’s value.

- For example, Epic Games’ Fortnite remains a leading cross-platform game, with roughly 1.3 million daily active players in the UK and about 650 million registered users globally as of 2025. Fortnite supports synchronized gameplay and progression across PC, consoles, and mobile devices, maintaining its position among the world’s top three most-played games.

Strong Investment from Technology Providers and Game Developers

Large-scale investments by technology firms and gaming studios fuel the UK Cloud Gaming Backend Service Market. These stakeholders recognize the long-term potential of backend services in delivering premium experiences. It supports advanced infrastructure, including low-latency servers and AI-driven optimization tools. Major companies are expanding their presence by collaborating with telecom operators. Partnerships are enabling faster deployment and innovative service delivery. Game studios are leveraging backend services for high-quality launches and immersive experiences. The ecosystem thrives on this continuous investment cycle. Increased R&D spending is generating scalable models that benefit providers and end-users. Competitive intensity drives innovation and market expansion.

Market Trends

Integration of Artificial Intelligence to Enhance Game Personalization

The UK Cloud Gaming Backend Service Market is witnessing a trend toward AI-powered personalization. Developers are integrating advanced algorithms to analyze player behavior and preferences. It enables platforms to provide tailored content recommendations, improving user engagement. AI-driven systems optimize gameplay by adjusting difficulty levels based on skill progression. Adaptive cloud services also enhance server efficiency by predicting peak demand. This technology strengthens user satisfaction and builds stronger loyalty. Predictive insights help developers refine game design and backend functions. Companies adopting AI are gaining a competitive edge in the evolving market landscape.

Adoption of Edge Computing to Reduce Latency in Gaming Services

Edge computing deployment is transforming the UK Cloud Gaming Backend Service Market by reducing latency. Service providers are placing servers closer to end-users to minimize data travel distance. It ensures smoother streaming and faster response times critical for immersive experiences. Cloud platforms are increasingly adopting hybrid infrastructure models blending edge and central servers. This approach provides flexibility while maintaining high performance. Gaming companies are also forming alliances with edge computing providers to expand coverage. Enhanced quality of service attracts more gamers to cloud platforms. Growing demand for low-latency esports streaming underscores this rising trend.

- For example, Xbox Cloud Gaming leverages Microsoft’s Azure infrastructure to bring servers closer to players, improving responsiveness and lowering latency. In the UK, users generally experience smooth gameplay when latency is kept below 60 milliseconds, with Microsoft continuing to optimize performance through ongoing backend and network enhancements.

Emergence of Cloud-Native Game Development Practices in the Market

The UK Cloud Gaming Backend Service Market is shifting toward cloud-native game development. Studios are building games optimized for cloud platforms rather than traditional hardware. It reduces constraints on performance and enhances creative possibilities. Cloud-native design supports real-time updates and continuous delivery models. This trend also encourages faster scalability and smoother patch rollouts. Developers are leveraging microservices architecture to increase efficiency and flexibility. Players benefit from quicker access to new features and seamless updates. This shift is reshaping the industry by prioritizing agility and customer-centric design.

Increasing Integration of Social Features and In-Game Community Building

Social integration is becoming a defining trend in the UK Cloud Gaming Backend Service Market. Platforms are embedding community tools, live chat, and shared achievements to increase engagement. It creates immersive multiplayer environments that extend beyond gameplay. Gaming is evolving into a social experience that strengthens user loyalty. Developers are investing in features that encourage collaboration and competitive interaction. These tools also drive higher in-game spending through peer influence. Stronger communities increase platform stickiness and attract new users. Enhanced social integration is turning games into digital ecosystems that support long-term growth.

- For example, Samsung’s Gaming Hub in the UK now includes partners like Volley, PHȲND, and GameLoop, bringing voice-AI trivia, instant-access cloud games, and live-hosted party titles directly to Smart TVs. The platform combines casual interactive entertainment with access to premium streaming services, offering a seamless, social-first gaming experience no console required.

Market Challenges Analysis

High Infrastructure Costs and Complexity in Service Deployment

The UK Cloud Gaming Backend Service Market faces challenges due to high infrastructure costs and complex service deployment requirements. Providers need to invest heavily in advanced servers, data centers, and network optimization. It increases operational expenses and delays scalability for smaller companies. Meeting latency requirements demands significant investment in edge computing and distributed systems. Integration with existing telecom networks further adds to the complexity. Service providers also face difficulties ensuring consistent quality during peak usage. Limited resources among smaller firms reduce competitive balance. These barriers slow market entry and limit overall ecosystem expansion.

Concerns Over Data Security, Content Rights, and Regulatory Compliance

Data privacy and content ownership are critical challenges in the UK Cloud Gaming Backend Service Market. Platforms handle sensitive user data, making them targets for cyberattacks and breaches. It requires strong security frameworks and constant monitoring to ensure compliance. Licensing agreements with developers and publishers are often complex and costly. Regulatory pressures on data localization and digital rights management add more hurdles. The need to balance user trust, legal compliance, and service quality increases operational strain. Providers must also address piracy risks tied to cloud content. Failure to resolve these issues may limit adoption and trust among users.

Market Opportunities

Growing Demand for Esports and Interactive Gaming Communities

The UK Cloud Gaming Backend Service Market holds opportunities in esports and interactive communities. Competitive gaming is driving demand for seamless, low-latency platforms. It encourages providers to innovate backend systems that support large-scale tournaments. Social features integrated with live-streaming tools create engaging ecosystems. These advancements attract sponsors, advertisers, and new revenue streams. Expanding esports popularity among younger demographics supports long-term market sustainability. Backend services that enhance spectator experiences can differentiate providers. Emerging partnerships with broadcasters and gaming influencers highlight this growth opportunity.

Expansion Potential Across Untapped Consumer Segments and Devices

The UK Cloud Gaming Backend Service Market has strong potential in reaching untapped segments. Affordable mobile devices and smart TVs are opening access for broader audiences. It reduces dependency on high-cost consoles and PCs. Service providers can target casual gamers with flexible subscription models. Integration with AR and VR devices offers future growth paths. Opportunities exist for partnerships with device manufacturers to bundle services. Expanding rural broadband coverage also supports inclusion of new users. These factors collectively open pathways for growth in underrepresented markets.

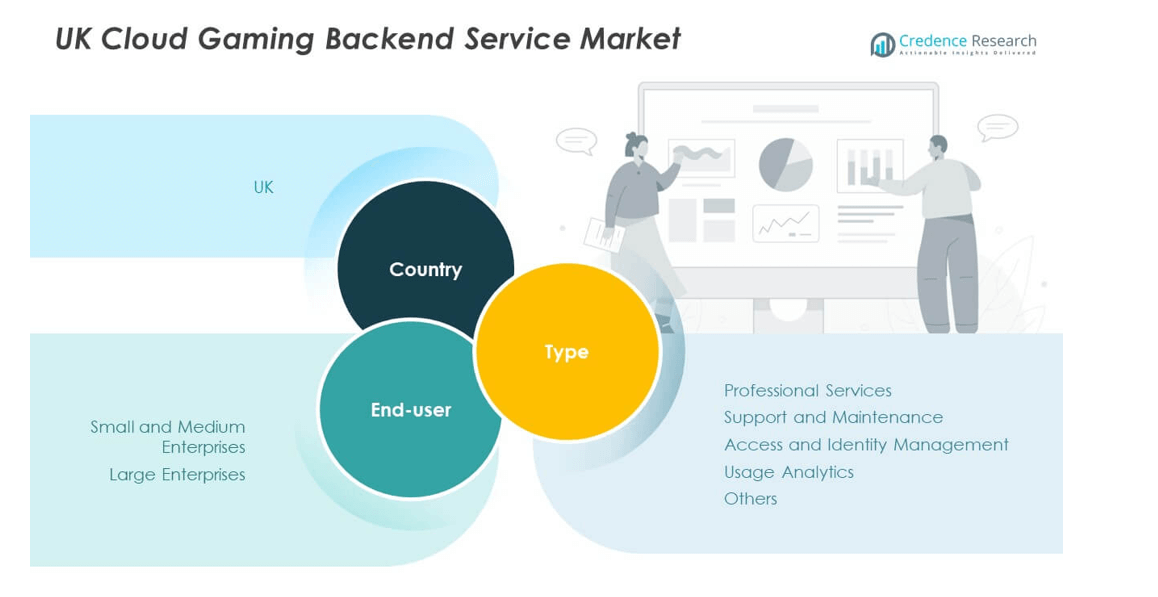

Market Segmentation Analysis

By type, professional services hold the largest share in the UK Cloud Gaming Backend Service Market, supported by strong demand for consulting, integration, and implementation services. It ensures that enterprises adopt scalable and low-latency platforms efficiently. Support and maintenance are gaining traction as companies prioritize reliable backend systems for uninterrupted gaming experiences. Access and identity management play a vital role in securing user data and preventing unauthorized access, reflecting rising concerns around digital safety. Usage analytics is emerging as an important segment, enabling providers to track gamer behavior and optimize content delivery. Others, including custom backend tools, cater to niche requirements and specialized services.

- For example, Ubisoft’s Rainbow Six Siege, leveraging PlayFab, supports over 30 million players with elastic scalability and robust backend services as of 2025.

By end-user, large enterprises dominate the UK Cloud Gaming Backend Service Market due to their investments in advanced infrastructure and extensive partnerships with global providers. It allows them to deliver enhanced gaming ecosystems and retain competitive advantage. Small and medium enterprises are expanding their adoption of backend services, driven by subscription-based models and cloud-native technologies that reduce capital costs. This group benefits from easier entry into the gaming ecosystem and flexible service delivery. Both enterprise categories are contributing to the steady growth of the market, with SMEs representing a strong potential for future expansion.

- For instance, Microsoft’s partnership with Unity utilizes Azure cloud services to enable real-time 3D experiences and simplify game publishing for independent creators, benefiting from scalable backend services and cloud infrastructure.

Segmentation

By Type

- Professional Services

- Support and Maintenance

- Access and Identity Management

- Usage Analytics

- Others

By End-User

- Small and Medium Enterprises

- Large Enterprises

Regional Analysis

England holds the largest share of the UK Cloud Gaming Backend Service Market with 55%. Strong digital infrastructure, advanced broadband coverage, and the presence of leading technology companies support its dominance. It benefits from high gamer penetration and rapid adoption of subscription-based models. London serves as a hub for innovation, attracting investments from global cloud service providers. Partnerships between gaming studios and telecom firms further strengthen growth. England’s focus on edge computing solutions is improving latency performance and enhancing user experiences.

Scotland accounts for 20% of the market share, driven by rising investments in gaming hubs and technology centers. The region benefits from supportive government initiatives for digital transformation and broadband expansion. It has a growing ecosystem of independent game developers adopting cloud solutions to scale faster. Demand for cross-platform gaming services is increasing across both urban and rural areas. It is also witnessing the development of cloud-native gaming practices that reduce hardware dependency. Local universities and research centers are contributing to talent growth and industry support.

Wales and Northern Ireland collectively represent 25% of the UK Cloud Gaming Backend Service Market. These regions are showing strong adoption trends due to improving internet infrastructure and growing gamer communities. It is also supported by investments in 5G connectivity, which is expanding access to cloud platforms. Small and medium enterprises are playing a vital role in driving backend service demand. Regional growth is further boosted by collaborations with global cloud providers entering these markets. Strong consumer interest in mobile-based gaming services is reinforcing adoption. Wales and Northern Ireland continue to emerge as important contributors to overall market expansion.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- NVIDIA GeForce Now

- Blacknut

- Shadow (Blade SAS)

- Ubitus

- Google Cloud Platform

- Amazon Web Services (AWS)

- Microsoft Azure

- IBM Cloud

- Scaleway

- GameSparks

Competitive Analysis

The UK Cloud Gaming Backend Service Market is highly competitive, with global technology firms and specialized providers competing for share. Key players include NVIDIA GeForce Now, Google Cloud Platform, Amazon Web Services, Microsoft Azure, IBM Cloud, Blacknut, Ubitus, Shadow (Blade SAS), Scaleway, and GameSparks. It is shaped by strategic alliances, mergers, and product innovations that enhance backend efficiency and user experience. Market leaders focus on reducing latency, expanding data center networks, and strengthening subscription models. Smaller firms leverage niche solutions such as usage analytics and identity management to differentiate offerings. Competitive intensity remains strong, with companies investing heavily in edge computing, AI-driven optimization, and cross-platform integration. The market’s future direction will depend on how effectively players adapt to evolving user needs and technological advancements.

Recent Developments

- In September 2025, Samsung Electronics announced the expansion of its mobile cloud gaming platform into the UK, marking a significant move in the UK cloud gaming backend service market. The beta rollout brought Galaxy device users instant access to premium mobile titles without downloads, and was accompanied by a strategic partnership with AI advertising firm Moloco to optimize user acquisition and monetization for partners and developers.

- In September 2025, NVIDIA launched the Blackwell RTX upgrade for GeForce NOW, bringing RTX 5080-class power streaming to the cloud. This update enables higher gaming resolutions and frame rates, new competitive high-performance modes, and access to over 2,200 titles, further solidifying NVIDIA’s presence in the North American cloud gaming backend service market.

- In March 2025, Xsolla and AWS entered into a key partnership designed to empower game developers with the latest advancements in cloud gaming and LiveOps solutions. The collaboration leverages AWS’s cloud infrastructure and Xsolla’s developer platform to create scalable, flexible backend solutions, further strengthening their positions in the expanding global cloud gaming backend service sector.

- In July 2024, Xsolla announced the acquisition of LF.Group to enhance gaming connectivity and commerce, empower creators, and improve user engagement across multiple platforms. This strategic move aims to give Xsolla a stronger foothold in the global cloud gaming backend service market by integrating LF.Group’s technology stack and community features into its existing offerings, driving forward innovation in backend solutions for cloud gaming environments.

Report Coverage

The research report offers an in-depth analysis based on type and end-user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The UK Cloud Gaming Backend Service Market will continue to expand, supported by rapid 5G deployment.

- Rising demand for subscription-based gaming models will drive consistent revenue growth across the sector.

- Edge computing adoption will enhance performance by minimizing latency and improving user satisfaction.

- Cross-platform gaming support will strengthen user loyalty by enabling seamless access across devices.

- Investment from technology giants will fuel infrastructure advancements and backend scalability.

- Cloud-native game development will reshape design processes and enable faster feature rollouts.

- AI-powered personalization will elevate user engagement by offering tailored recommendations and adaptive gameplay.

- Esports expansion will generate new opportunities for backend service optimization and community building.

- Strong digital adoption across smaller regions will unlock untapped market potential within the UK.

- Competitive intensity will push providers to innovate continuously and strengthen their market positioning.