Market Overview:

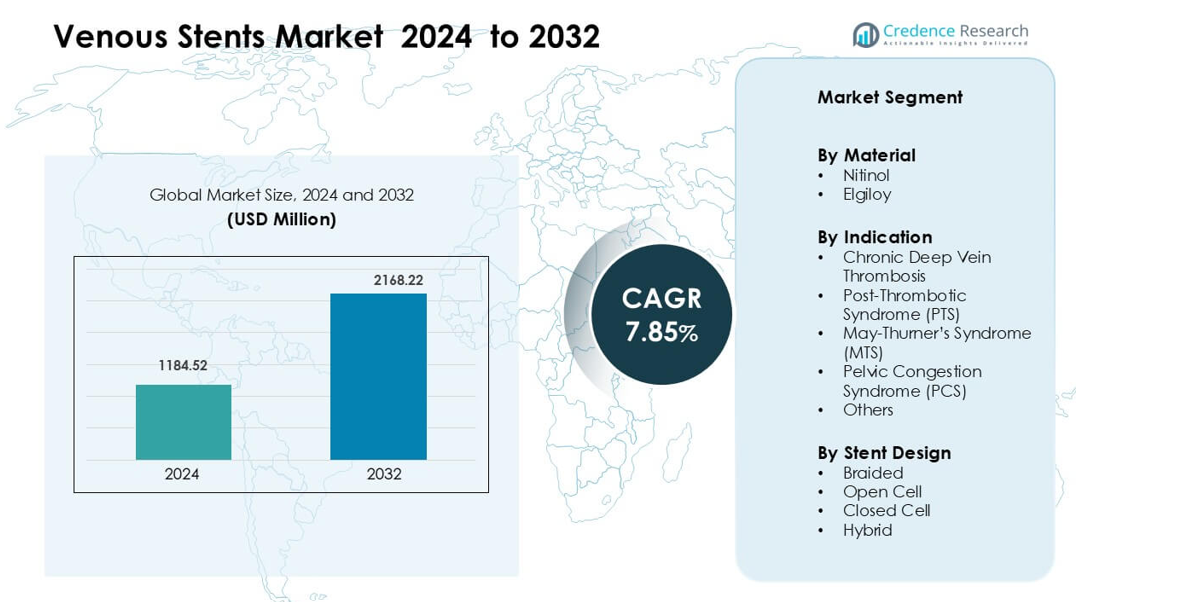

Venous Stents Market was valued at USD 1184.52 million in 2024 and is anticipated to reach USD 2168.22 million by 2032, growing at a CAGR of 7.85 % during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Venous Stents Market Size 2024 |

USD 1184.52 million |

| Venous Stents Market, CAGR |

7.85% |

| Venous Stents Market Size 2032 |

USD 2168.22 million |

The Venous Stents Market is driven by strong competition among major manufacturers, including MicroPort Scientific Corporation, Medtronic Plc, Meril Life Science, Boston Scientific Corporation, Biotronik SE & Co. KG, Abbott Laboratories, Elixir Medical Corporation, Biosensors International Group, B. Braun Melsungen AG, and Becton, Dickinson and Company. These companies strengthen their position through advanced nitinol designs, improved radial force, and optimized delivery systems tailored for complex venous anatomies. North America leads the global market with about 38% share in 2024, supported by high diagnostic accuracy, strong reimbursement, and rapid adoption of minimally invasive venous interventions.

Market Insights

- Venous Stents Market was valued at USD 1184.52 million in 2024 and is anticipated to reach USD 2168.22 million by 2032, growing at a CAGR of 7.85 % during the forecast period.

- Rising cases of Chronic DVT and Post-Thrombotic Syndrome drive higher procedure volumes, with Chronic DVT holding the largest indication share at about 45% due to growing treatment awareness.

- Dedicated nitinol braided stents continue to trend, with braided designs leading the segment at around 52% as hospitals prefer flexible platforms with reliable radial strength for complex venous paths.

- Competition strengthens as major companies enhance stent durability, delivery precision, and long-term patency while pursuing regulatory approvals and clinical partnerships to expand global presence.

- North America leads the market with about 38% share, followed by Europe at around 30%, while Asia-Pacific shows rapid growth with roughly 22% driven by rising healthcare access and increased adoption of minimally invasive venous interventions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Material

Nitinol leads this segment with an estimated about 72% share in 2024. Hospitals prefer nitinol because the alloy offers strong flexibility, kink resistance, and reliable radial force for complex venous anatomies. The material delivers better long-term patency than stainless steel or cobalt-based alloys, which supports wider adoption in chronic obstruction cases. Elgiloy holds a smaller share due to limited elasticity, yet specialists use it in cases requiring high fatigue strength. Strong preference for minimally invasive treatments continues to push nitinol-based venous stents across major vascular centers.

- For instance, the BD Venovo™ Venous Stent, which employs a nitinol structure, exhibits a radial resistive force of 0.126 N/mm at a 13 mm crimp diameter, outperforming competing designs.

By Indication

Chronic Deep Vein Thrombosis dominates this segment with nearly 45% share in 2024. Surgeons treat post-thrombotic obstruction more often as patient awareness and diagnostic accuracy improve. Post-Thrombotic Syndrome follows because long-term inflammation and scarring increase the need for durable stenting solutions. May-Thurner’s Syndrome and Pelvic Congestion Syndrome grow steadily with better imaging and higher intervention rates in women. Rising demand for symptom relief, reduced swelling, and improved leg function drives strong placement volumes within the Chronic DVT category.

- For instance, in the ATOMIC registry involving 59 patients with May-Thurner syndrome and acute DVT, primary patency was 84% at 19 months, with a secondary patency rate of 93% at 20 months.

By Stent Design

Braided stents hold the largest share at roughly 52% in 2024. Clinicians choose braided formats because the design provides superior flexibility, conformability, and sustained radial strength in curved venous paths. Open-cell designs grow in adoption for easier vessel access, while closed-cell stents gain use in cases requiring strong scaffolding and reduced migration. Hybrid stents emerge as a balanced option by mixing flexibility and strength. Increased preference for dedicated venous designs and rising interventional cases support continued dominance of braided configurations.

Key Growth Drivers

Growing Burden of Chronic Venous Diseases

The rising prevalence of chronic venous diseases acts as a major growth driver for the Venous Stents Market. More patients experience long-term venous obstruction linked to aging, sedentary lifestyle, obesity, and higher post-thrombotic complications. Hospitals report a steady rise in Chronic DVT and PTS procedures, which expands the candidate pool for venous stenting. Better diagnostic tools such as intravascular ultrasound help physicians detect complex lesions earlier, strengthening treatment adoption. As awareness grows among patients seeking relief from leg pain, swelling, and mobility issues, healthcare systems continue to expand venous intervention programs. This broader clinical acceptance boosts demand for advanced stents across major vascular centers.

- For instance, a large real-world analysis of over 700,000 peripheral vascular patients (arterial and venous) found that when iliofemoral venous stenting was guided by IVUS, there was a 31% reduction in the composite outcome of repeat intervention, hospitalization, or death.

Rapid Shift Toward Minimally Invasive Venous Interventions

Minimally invasive procedures shape strong demand for venous stents as surgeons replace open surgical options with catheter-based repair. These interventions reduce recovery time, shorten hospital stay, and lower complication risks, making them attractive to both patients and hospitals. Dedicated venous stents, especially nitinol braided platforms, support safe placement in tortuous anatomy, which accelerates adoption. Clinical evidence showing improved patency rates and better long-term outcomes continues to boost confidence in the procedure. As reimbursement frameworks support minimally invasive treatment, more vascular centers invest in dedicated venous devices. This shift is expected to sustain long-term growth.

- For instance, Cook Medical’s Zilver Vena® braided nitinol stent reported a Kaplan–Meier patency of 90.3% at 3 years in the VIVO clinical study, with no stent fractures observed over the same period.

Advancements in Stent Design and Material Technologies

Rapid innovation in material science and stent engineering also drives market expansion. Manufacturers develop highly flexible designs, such as braided nitinol stents, that maintain strong radial force in compressed or curved venous segments. Newer solutions offer enhanced durability, improved fracture resistance, and better long-term patency, which increases clinical preference. Digital planning tools and imaging-guided placement improve accuracy, boosting procedural success rates. Companies continue upgrading stents with targeted length options, repositioning features, and improved delivery systems to meet complex anatomical needs. These enhancements strengthen physician confidence and support continuous adoption across global venous intervention clinics.

Key Trend & Opportunities

Expansion of Dedicated Venous Stent Portfolios

A key market trend involves rapid expansion of dedicated venous stent portfolios by major manufacturers. Historically, many vascular centers relied on repurposed arterial stents, but clinical demand now favors purpose-built venous solutions. Companies focus on larger diameters, improved flexibility, and optimized radial strength tailored for iliac and femoral veins. This shift provides major opportunities for product differentiation and premium pricing. As more long-term clinical data validates the benefits of dedicated venous platforms, regulatory agencies accelerate approvals for next-generation designs. The expanding product landscape encourages hospitals to upgrade older devices, strengthening long-term adoption.

- For instance, Medtronic’s Abre™ Venous Stent is available in diameters ranging from 10 mm to 20 mm, and lengths from 40 mm to 150 mm, showing how purpose-built venous stents now match the anatomical demands of large, compressed veins.

Growing Use of Imaging-Guided and Personalized Treatment Approaches

Another major trend is the integration of advanced imaging and personalized planning in venous interventions. Intravascular ultrasound and advanced CT venography enable precise lesion mapping, improving stent placement accuracy and long-term outcomes. AI-assisted planning platforms and digital visualization tools allow physicians to select optimal stent length and diameter for each patient, reducing restenosis risk. This movement toward personalized care creates new opportunities for manufacturers offering integrated digital ecosystems. As global vascular centers adopt these tools, demand rises for stents and imaging systems that support tailored and minimally invasive procedures.

- For instance, in a cohort of 100 patients with suspected iliac vein obstruction, IVUS identified significant lesions in 81% of limbs vs 51% detected by venography alone, and in 60% of the cases, the treatment plan was changed on the basis of IVUS findings.

Rising Adoption Across Emerging Markets

Emerging regions present strong opportunities as healthcare infrastructure improves and vascular specialists increase intervention volumes. Countries in Asia-Pacific, Latin America, and the Middle East expand training programs for endovascular procedures, creating new demand for venous stents. Rising insurance coverage and increased investment in vascular care centers further boost accessibility. Growing awareness of chronic venous disorders leads more patients to seek treatment, while government initiatives encourage adoption of minimally invasive technologies. These trends position emerging markets as high-growth regions for stent manufacturers seeking geographic expansion.

Key Challenges

Risk of Restenosis and Stent-Related Complications

Restenosis remains one of the major clinical challenges limiting broader adoption of venous stents. Venous vessels experience dynamic movement, compression, and high-flow resistance, which can lead to neointimal hyperplasia and recurrent narrowing. Stent fractures, migration, and incomplete wall apposition can further impact long-term patency. These complications require repeat procedures, increasing total treatment costs and deterring some surgeons from early intervention. Manufacturers continue developing stronger materials, improved radial force balance, and fracture-resistant designs, yet long-term durability concerns persist. Addressing these issues remains essential for improving patient outcomes and expanding clinical confidence.

Limited Awareness and Uneven Access to Skilled Venous Intervention Centers

Another significant challenge stems from limited awareness of venous disease treatment options and uneven global access to trained specialists. Many patients with chronic venous obstruction remain undiagnosed or receive delayed care due to low screening rates. In emerging markets, shortages of vascular surgeons, limited imaging capabilities, and slow reimbursement pathways hinder procedure adoption. High device prices further restrict access in low-income regions, where healthcare budgets prioritize acute cardiovascular conditions. Expanding training programs, improving diagnostic accessibility, and establishing reimbursement clarity are essential steps to overcoming adoption barriers and ensuring wider availability of venous stenting solutions.

Regional Analysis

North America

North America leads the Venous Stents Market with about 38% share in 2024. The region benefits from strong adoption of minimally invasive venous interventions, widespread IVUS use, and high diagnostic accuracy for Chronic DVT and PTS. The U.S. drives most procedure volumes due to advanced vascular centers and favorable reimbursement for iliac and femoral stenting. Clinical guidelines support early intervention, which boosts placement rates across hospitals. Growing investment in dedicated venous stent trials and rapid uptake of braided nitinol platforms further reinforce the region’s leadership.

Europe

Europe follows with around 30% share in 2024, supported by strong vascular infrastructure and high awareness of chronic venous obstruction. Countries such as Germany, the U.K., and France adopt dedicated venous designs due to mature endovascular programs and rising PTS treatment demand. Expanded training initiatives and broader reimbursement for minimally invasive venous repair strengthen adoption across major hospitals. Clinical preference for long-term patency and imaging-guided stent placement drives steady usage. The region maintains consistent market growth as physicians shift from repurposed arterial devices to purpose-built venous platforms.

Asia-Pacific

Asia-Pacific accounts for roughly 22% share in 2024 and grows rapidly with expanding healthcare access and rising awareness of venous disorders. China, Japan, South Korea, and India increase procedure adoption as more vascular specialists receive endovascular training. Government investments in imaging and catheter-based treatments improve diagnostic rates for May-Thurner Syndrome and PTS. Hospitals favor nitinol venous stents as demand for minimally invasive vascular solutions rises. Large patient pools with lifestyle-driven venous issues support future market expansion, making Asia-Pacific one of the fastest-growing regions.

Latin America

Latin America holds about 6% share in 2024, driven by gradual improvements in vascular care capacity. Brazil and Mexico lead the region as hospitals adopt modern imaging tools and expand endovascular service lines. Rising treatment awareness for chronic venous insufficiency encourages more patients to seek intervention. However, uneven access to advanced devices and limited reimbursement frameworks slow broader uptake. As training programs grow and minimally invasive procedures become more affordable, the region shows steady but moderate growth for venous stent adoption.

Middle East & Africa

The Middle East & Africa represent around 4% share in 2024, supported by improving vascular facilities in GCC nations. UAE and Saudi Arabia increase procedure volumes as hospitals adopt dedicated venous stents and strengthen endovascular programs. Access remains limited in many African regions due to cost, low diagnostic rates, and shortage of trained specialists. Private-sector investment, technology upgrades, and medical tourism in the Gulf help drive localized growth. As awareness of chronic venous obstruction rises, the region is expected to post gradual improvements in venous stent usage.

Market Segmentations:

By Material

By Indication

- Chronic Deep Vein Thrombosis

- Post-Thrombotic Syndrome (PTS)

- May-Thurner’s Syndrome (MTS)

- Pelvic Congestion Syndrome (PCS)

- Others

By Stent Design

- Braided

- Open Cell

- Closed Cell

- Hybrid

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Venous Stents Market features strong competition led by global and regional manufacturers that develop dedicated devices for chronic venous obstruction. Key players such as MicroPort Scientific Corporation, Medtronic Plc, Meril Life Science, Boston Scientific Corporation, Biotronik SE & Co. KG, Abbott Laboratories, Elixir Medical Corporation, Biosensors International Group, B. Braun Melsungen AG, and Becton, Dickinson and Company focus on advanced nitinol platforms with improved flexibility, radial strength, and long-term patency. Companies expand their portfolios with braided and hybrid designs optimized for iliac and femoral veins, while clinical trials support product credibility. Many vendors invest in imaging-guided solutions and enhanced delivery systems to improve placement accuracy. Partnerships with vascular centers allow firms to strengthen surgeon engagement and accelerate adoption. Continuous innovation, geographic expansion, and regulatory approvals remain central to sustaining competitiveness in this growing market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- MicroPort Scientific Corporation

- Medtronic Plc

- Meril Life Science

- Boston Scientific Corporation

- Biotronik SE & Co. KG

- Abbott Laboratories

- Elixir Medical Corporation

- Biosensors International Group

- Braun Melsungen AG

- Becton, Dickinson and Company

Recent Developments

- In February 2025, MicroPort Scientific Corporation China’s NMPA approved the Vflower® Venous Stent System for marketing, allowing MicroPort Endovastec/Bluevastec to commercialize a dedicated iliac/iliofemoral venous stent in the Chinese market and expanding locally made options for venous outflow obstruction therapy.

- In October 2024, Meril Life Science Meril inaugurated a new advanced medical device manufacturing facility in Vapi, Gujarat, under India’s Production Linked Incentive scheme, expanding capacity for vascular-intervention products such as stents and scaffolds and indirectly strengthening its position in the broader venous and vascular stents.

- In 2022, Medtronic Plc the FDA Post-Approval Studies database lists the ABRE Continued Follow-up Study for the Abre Venous Self-expanding Stent System as completed, adding long-term real-world safety and performance evidence for the device in deep venous obstruction treatment

Report Coverage

The research report offers an in-depth analysis based on Material, Indication, Stent Design and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for venous stents will rise as chronic venous diseases become more common.

- Dedicated venous stent designs will replace repurposed arterial devices across major hospitals.

- Braided nitinol platforms will gain stronger adoption due to better flexibility and patency.

- Imaging-guided placement using IVUS and advanced CT will become standard practice.

- Emerging markets will expand procedure volumes as vascular training programs grow.

- Long-term clinical data will support wider approval of next-generation venous stents.

- Hybrid stent designs will gain traction for complex iliac and femoral anatomies.

- Digital planning tools and AI-based sizing systems will improve treatment precision.

- Reimbursement frameworks will strengthen as venous disease awareness improves.

- Manufacturers will focus on fracture-resistant, durable stents to reduce restenosis risk.