Market Overview

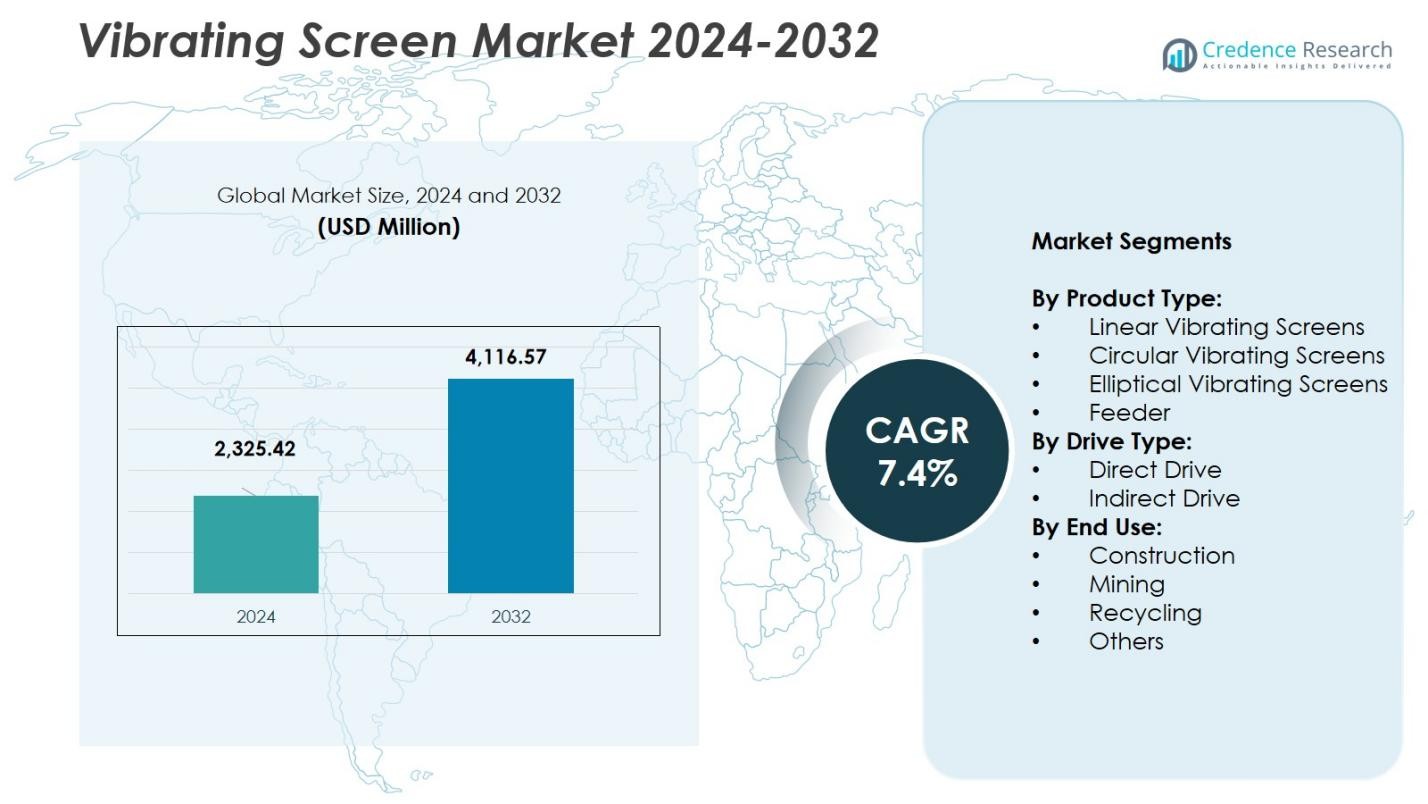

The Vibrating Screen Market size was valued at USD 2,325.42 million in 2024 and is anticipated to reach USD 4,116.57 million by 2032, at a CAGR of 7.4% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Vibrating Screen Market Size 2024 |

USD 2,325.42 Million |

| Vibrating Screen Market, CAGR |

7.4% |

| Vibrating Screen Market Size 2032 |

USD 4,116.57 Million |

Vibrating Screen Market is driven by the strong presence of key players such as Terex Corporation, Haulotte Group, Oshkosh Corporation, Linamar Corporation, Tadano Ltd, Aichi Corporation, MEC Aerial Work Platforms, Palfinger AG, Hunan Sinoboom Heavy Industries Co. Ltd., and Zheijiang Dingli Machinery Co. Ltd., all focusing on advancing screening efficiency, expanding product lines, and integrating digital monitoring systems. Asia-Pacific emerges as the leading regional market with a 34% share, supported by extensive mining activity, rapid industrialization, and large-scale infrastructure projects. North America follows with 32%, driven by equipment modernization and growing demand for high-capacity screening systems across construction and mineral processing industries.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Vibrating Screen Market reached USD 2,325.42 million in 2024 and is forecast to grow at a CAGR of 7.4% through 2032, driven by rising demand across mining and construction industries.

- Market growth is supported by expanding mineral processing activities and increasing adoption of high-capacity screening systems, with the mining segment holding 36.6% share due to its extensive material classification requirements.

- Key trends include rapid integration of IoT-enabled monitoring, modular screen designs, and energy-efficient direct-drive systems, with Circular Vibrating Screens leading the product segment at 48.8% share.

- Major players such as Terex Corporation, Palfinger AG, Tadano Ltd, and Haulotte Group enhance their presence by focusing on product innovation, advanced drive technologies, and stronger aftermarket networks.

- Asia-Pacific leads regional adoption with 34% share, followed by North America at 32% and Europe at 24%, driven by strong industrial expansion, large-scale mining operations, and increasing infrastructure development.

Market Segmentation Analysis:

Market Segmentation Analysis:

By Product Type

The product type segment of the vibrating screen market is led by Circular Vibrating Screens, holding a precise share of 48.8% in 2025. This segment’s dominance is driven by its versatility across mining, construction, and recycling applications and its proven ability to handle large-volume, coarse material separation with reliable performance. The established process flows, growing infrastructure investment, and preference for robust screening equipment have reinforced its leading position in the market.

- For instance, FLSmidth offers Circular Vibrating Screens used extensively in screening rock, ore, and bulk materials across mining and recycling sectors, emphasizing dependable performance for large-volume processing.

By Drive Type

In the drive type segment, Direct Drive systems command the highest share, measured at 54.3% in the relevant market modelling. The leadership of direct drive units stems from their improved energy efficiency, lower mechanical complexity (eliminating belts or coupling), and greater reliability in heavy-duty screening operations. As key end-users demand higher uptime and reduced maintenance costs, direct drive technology continues to gain rapid adoption over indirect drive alternatives.

- For instance, Mainstream Fluid & Air reports that direct drive fans improve mechanical efficiency by up to 15% by eliminating belt and pulley losses, resulting in significant energy savings and lower maintenance needs.

By End Use

Within the end-use categorisation, the Mining sector is the dominant sub-segment, accounting for 36.6% of the market in 2025. The mining industry’s strong demand for screening and classification of ores, the increasing scale of extraction operations, and implementation of high-throughput equipment in mineral processing circuits drive the large share. Growth in infrastructure raw materials, industrial minerals, and the need for efficient material separation underpins mining as the key end-use for vibrating screens.

Key Growth Drivers

Expansion of Mining and Mineral Processing Activities

The expansion of global mining and mineral processing activities serves as a primary growth driver for the vibrating screen market. Rising demand for metals, minerals, and aggregates—fueled by infrastructure development, energy transition initiatives, and industrial output—has increased the adoption of high-capacity screening equipment. Vibrating screens enable efficient material separation, ore grading, and throughput optimization, making them essential for modern mining operations. Additionally, advancements in extraction technologies and expansion of open-pit and underground mines continue to boost demand for durable and high-performance screening solutions.

- For instance, copper mines utilize vibrating screens to sort crushed ore, enhancing extraction efficiency and product quality.

Growing Infrastructure and Construction Sector

Robust infrastructure development, urban expansion, and rising construction spending are significantly accelerating the need for vibrating screens. These systems play a critical role in processing aggregates, sand, and construction materials used in building roads, railways, commercial structures, and housing projects. The demand for precise material sizing and high-efficiency screening has encouraged construction firms to deploy technologically advanced screens. As emerging economies invest heavily in smart cities, transportation networks, and utility infrastructure, the requirement for reliable screening equipment will continue to strengthen across the construction segment.

- For instance, Haver & Boecker Niagara’s T-Class vibrating screen features innovations like lockbolted frames and a Drop Guard system, enhancing uptime and durability in aggregate processing.

Shift Toward Automation and Energy-Efficient Screening Equipment

The increasing shift toward automation and energy-efficient industrial machinery is driving widespread adoption of advanced vibrating screens. Modern plants prioritize operational efficiency, reduced downtime, and improved process accuracy, leading to growing demand for automated monitoring, adjustable vibration frequency, and low-energy drive technologies. Intelligent screening systems equipped with sensors and condition-based monitoring support predictive maintenance, improving productivity while lowering operational costs. As industries aim to optimize workflows and comply with sustainability goals, automated and energy-efficient vibrating screens are becoming essential components in material processing environments.

Key Trends & Opportunities

Integration of IoT and Predictive Maintenance Technologies

A major trend reshaping the vibrating screen market is the integration of IoT-enabled sensors and predictive maintenance tools. Real-time tracking of vibration patterns, load distribution, and machine health enables operators to identify faults early and minimize unplanned downtimes. Manufacturers are increasingly offering digitalized screening systems that support cloud-based analytics and remote diagnostics. This shift not only enhances operational reliability but also creates opportunities for value-added service models. As industries modernize production lines, the demand for intelligent, data-driven screening equipment is expected to grow rapidly.

- For instance, NCD’s Industrial IoT wireless vibration and temperature sensor transmits accurate 3-axis vibration data up to 2 miles away using a wireless mesh network, allowing real-time machine health monitoring and early fault detection.

Rising Adoption of Customized and Modular Screening Solutions

Growing preference for customized and modular vibrating screens presents a significant market opportunity. Industries require tailored solutions to manage varying feed types, particle sizes, moisture levels, and throughput demands. Modular screen decks, replaceable panels, and adjustable vibration mechanisms allow users to optimize performance across changing applications. Manufacturers offering configurable screening systems gain a competitive edge by reducing installation time and improving operational flexibility. As sectors like recycling, aggregate processing, and specialty minerals expand, the demand for adaptable screening equipment will continue to rise.

- For instance, Shanbao Machinery’s S5X series incorporates modular vibrators and screen mesh tension plates that can be quickly replaced, reducing maintenance downtime and operational costs.

Key Challenges

High Maintenance Requirements and Downtime Concerns

Frequent maintenance needs and downtime pose major challenges for vibrating screen users. Continuous exposure to heavy loads, abrasive materials, and dynamic vibration forces accelerates wear on screen decks, bearings, and drive components. Maintenance interruptions can lead to productivity losses and increased operational costs, especially in mining and industrial plants operating around the clock. Ensuring reliable performance requires consistent inspection, lubrication, and component replacement, which can strain operational budgets. Overcoming this challenge depends on improved durability, predictive maintenance systems, and robust aftermarket support.

Volatility in Raw Material Prices and Manufacturing Costs

Fluctuations in steel, alloys, and industrial component prices significantly impact the manufacturing cost of vibrating screens. Economic uncertainties, supply chain disruptions, and geopolitical tensions contribute to unstable raw material prices, making cost planning difficult for both manufacturers and end users. Rising production expenses often lead to higher equipment prices, affecting procurement decisions in cost-sensitive sectors. Additionally, the need for high-quality materials to ensure durability further increases manufacturing complexity. Managing cost pressure while maintaining performance standards remains a key challenge for industry participants.

Regional Analysis

North America

North America holds 32% market share in the Vibrating Screen Market, driven by strong demand from mining, aggregates, and construction sectors. The United States leads regional adoption, supported by large-scale mineral processing operations, modernization of screening equipment, and replacement of legacy systems with energy-efficient technologies. Infrastructure refurbishment programs and the expansion of metal extraction activities continue to boost equipment procurement. Additionally, the region’s focus on automated process control and advanced material-handling systems strengthens the demand for high-performance vibrating screens across industrial segments, ensuring continued market leadership.

Europe

Europe accounts for 24% market share, supported by well-established industrial manufacturing, recycling infrastructure, and aggregate production activities. Countries such as Germany, the UK, and France continue to invest in advanced screening technologies to meet stringent environmental regulations and efficiency standards. Demand is further driven by growth in metal recycling and quarrying operations, where precision material separation is essential. The region’s focus on sustainable production, equipment digitalization, and high-quality industrial machinery reinforces the adoption of technologically enhanced vibrating screens. Strong aftermarket services and OEM presence also contribute to steady regional growth.

Asia-Pacific

Asia-Pacific leads global growth momentum with a 34% market share, driven by rapid industrialization, large-scale mining activity, and expanding construction markets in China, India, and Southeast Asia. Massive infrastructure investments, including transport corridors, housing development, and energy projects, continue to increase the need for high-capacity screening equipment. The region’s mineral extraction sector, particularly coal, iron ore, and industrial minerals, significantly boosts equipment demand. Additionally, growing manufacturing output and accelerated urbanization promote extensive adoption of vibrating screens. The emergence of local OEMs offering cost-competitive machinery further strengthens regional market expansion.

Latin America

Latin America holds 6% market share, supported primarily by mining-driven economies such as Brazil, Chile, and Peru. The region’s vast reserves of copper, iron ore, lithium, and precious metals sustain continuous investment in mineral screening and material-handling equipment. Vibrating screens are widely used in beneficiation plants and aggregate processing, driven by rising export demand for minerals. Infrastructure development initiatives and quarrying activities add to market opportunities. However, economic fluctuations and inconsistent industrial spending remain challenges. Despite these constraints, ongoing mining modernization efforts help maintain steady demand across the region.

Middle East & Africa

The Middle East & Africa region accounts for 4% market share, with growth anchored in expanding mining operations, quarrying activities, and construction developments across Gulf countries and Sub-Saharan Africa. Increased extraction of gold, diamonds, phosphates, and industrial metals drives the adoption of vibrating screens in mineral processing. Infrastructure expansion—including roads, commercial construction, and industrial projects—further supports equipment usage. Although political and economic instability impacts some markets, rising foreign investments in mining and ongoing resource exploration initiatives contribute to gradual but consistent regional market growth.

Market Segmentations:

By Product Type:

- Linear Vibrating Screens

- Circular Vibrating Screens

- Elliptical Vibrating Screens

- Feeder

By Drive Type:

- Direct Drive

- Indirect Drive

By End Use:

- Construction

- Mining

- Recycling

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the Vibrating Screen Market is shaped by leading players such as Terex Corporation, Haulotte Group, Oshkosh Corporation, Linamar Corporation, Tadano Ltd, Aichi Corporation, MEC Aerial Work Platforms, Palfinger AG, Hunan Sinoboom Heavy Industries Co. Ltd., and Zheijiang Dingli Machinery Co. Ltd. These companies focus on expanding product portfolios, improving screening efficiency, and integrating digital monitoring technologies to strengthen market presence. Innovation in drive mechanisms, modular screen designs, and high-capacity equipment remains central to competitive differentiation. Strategic initiatives such as mergers, facility expansions, and regional distribution enhancements enable stronger global reach. Key players also invest in R&D to develop energy-efficient, low-maintenance systems tailored for mining, construction, and recycling industries. Moreover, partnerships with end-use industries help enhance performance customization and service capabilities. Overall, competition intensifies as manufacturers prioritize technological advances, cost optimization, and aftermarket service expansion to capture greater market share.

Key Player Analysis

- Zheijiang Dingli Machinery Co. Ltd.

- Terex Corporation

- MEC Aerial Work Platforms

- Tadano Ltd

- Hunan Sinoboom Heavy Industries Co. Ltd.

- Linamar Corporation

- Palfinger AG

- Haulotte Group

- Oshkosh Corporation

- Aichi Corporation

Recent Developments

- In October 2025, Finlay launched new inclined screeners (models 693 and 694).

- In July 2024, Weir introduced the ENDURON Orbital vibrating screens (elliptical motion horizontal + circular motion inclined types) for sand, aggregates and mining applications.

- In 2025, Galaxy SIVTEK Pvt. Ltd. launched a new tumbler screen as part of its product expansion in the vibrating screen market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Product Type, Drive Type, End Use and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will experience steady demand growth driven by expanding mining, construction, and infrastructure development activities.

- Adoption of energy-efficient vibrating screens will increase as industries prioritize sustainability and operational cost reduction.

- Integration of IoT, automation, and predictive maintenance features will become standard in modern screening equipment.

- Demand for modular and customizable screen designs will rise to support diverse material-processing requirements.

- The recycling and waste management sector will generate new opportunities for advanced screening solutions.

- Manufacturers will strengthen aftermarket services to enhance uptime, maintenance efficiency, and equipment longevity.

- Emerging economies in Asia-Pacific and Africa will drive high-volume equipment procurement through industrial expansion.

- Hybrid and smart drive technologies will gain prominence for improving machine performance and reliability.

- Increased focus on occupational safety will encourage adoption of low-noise and vibration-controlled screen systems.

- Strategic collaborations and capacity expansions will shape competitive positioning and global market penetration.