Market Overview

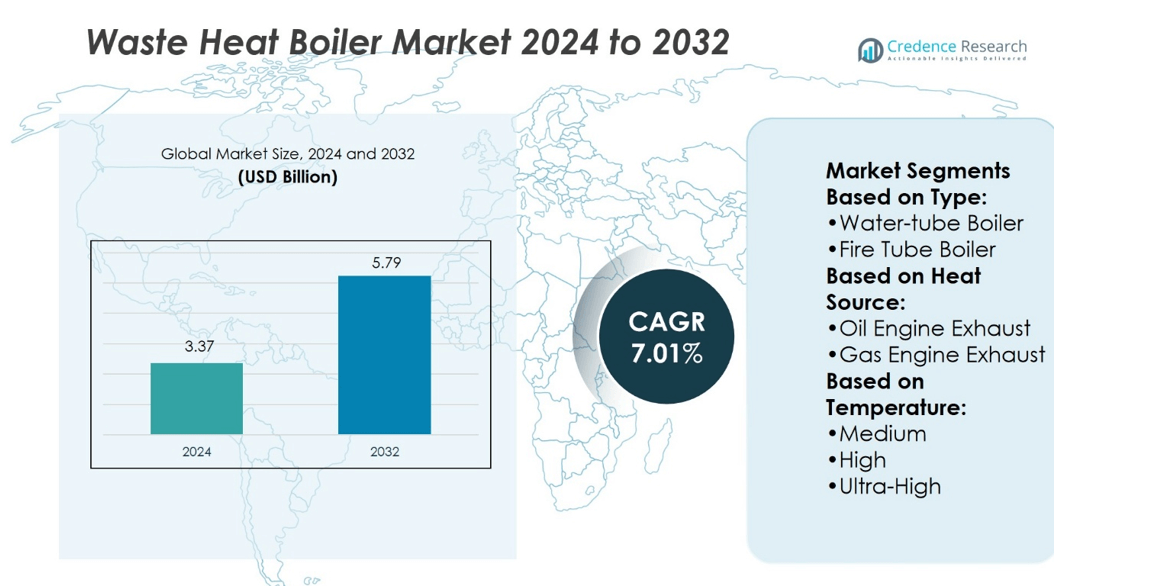

Waste Heat Boiler Market size was valued at USD 3.37 billion in 2024 and is anticipated to reach USD 5.79 billion by 2032, at a CAGR of 7.01% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Waste Heat Boiler Market Size 2024 |

USD 3.37 billion |

| Waste Heat Boiler Market, CAGR |

7.01% |

| Waste Heat Boiler Market Size 2032 |

USD 5.79 billion |

The Waste Heat Boiler Market grows through strong drivers and evolving trends linked to energy efficiency and sustainability. Rising demand from power, cement, steel, and petrochemical industries fuels adoption as companies focus on cutting fuel costs and meeting emission targets. Governments worldwide enforce stricter regulations, creating steady demand for advanced systems. The market also benefits from the shift toward combined heat and power projects and waste-to-energy plants. Trends highlight growing use of digital monitoring, IoT integration, and predictive maintenance solutions. Modular and compact designs gain popularity, while new materials support durability and long-term performance across diverse industrial applications.

The Waste Heat Boiler Market shows strong geographical diversity, with Asia-Pacific leading due to rapid industrial growth in China and India, followed by North America and Europe supported by strict energy regulations. Latin America and the Middle East & Africa record smaller but rising shares through refinery, cement, and power projects. Key players include Bosch Thermotechnology, Siemens Energy, Thermax Limited, General Electric (GE), Forbes Marshall, Alfa Laval AB, Thyssenkrupp Industrial Solutions, Babcock & Wilcox Enterprises, BHEL, and Nooter/Eriksen.

Market Insights

- Waste Heat Boiler Market size was valued at USD 3.37 billion in 2024 and is projected to reach USD 5.79 billion by 2032 at a CAGR of 7.01%.

- Rising demand from power, cement, steel, and petrochemical industries drives market growth.

- Strong trends include digital monitoring, IoT integration, predictive maintenance, and modular compact designs.

- Competition remains high with global players focusing on advanced technology, sustainability, and service networks.

- High capital cost and complex installation act as restraints, limiting adoption for smaller firms.

- Asia-Pacific leads the market with rapid industrialization in China and India, while North America and Europe follow with strict energy regulations.

- Latin America and Middle East & Africa show smaller but rising shares through refining, cement, and new power projects.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Energy Efficiency Requirements in Industrial Operations

The Waste Heat Boiler Market grows with stricter global energy efficiency regulations. Industries face rising pressure to optimize fuel use and reduce emissions. Waste heat boilers capture exhaust gases from turbines, engines, and furnaces, converting them into usable energy. This process helps plants reduce fuel dependency while meeting environmental targets. It supports continuous power generation in sectors like chemicals, oil and gas, and steel. Industrial firms adopt these systems to improve overall energy utilization.

- For instance, at the Cengiz Enerji plant in Turkey, Alfa Laval added seven Aalborg AV‑6N boilers and superheaters. This upgrade raised steam‑cycle output by 40%, adding 8 MW electrical output via the steam turbine. It strengthened energy use while helping meet environmental targets.

Expansion of Power Generation and Cogeneration Facilities

Power generation companies drive demand for waste heat boilers due to their efficiency benefits. Combined heat and power (CHP) systems integrate them to maximize energy recovery. By producing electricity and thermal energy simultaneously, plants reduce operating costs and carbon footprints. The Waste Heat Boiler Market benefits from wider use in both small-scale and large-scale cogeneration facilities. Countries promoting renewable and hybrid energy models increase system installations. It becomes essential equipment for meeting modern power sector efficiency targets.

- For instance, Bharat Heavy Electricals Limited (BHEL) delivered a 12 MW Steam Turbine Generator (STG) unit to the Finchaa Sugar Factory in Ethiopia. This unit, part of a 2×12 MW cogeneration project, provides both process steam and power—excess energy is supplied to the national grid.

Growth of Heavy Industries and Rising Emissions Reduction Goals

Heavy industries like cement, glass, and petrochemicals generate substantial heat loss during operations. The Waste Heat Boiler Market provides a direct solution for converting lost heat into power or steam. Governments worldwide enforce emission limits, boosting adoption in emission-intensive sectors. Companies implement waste heat recovery units to comply with carbon regulations and lower operating expenses. It supports the development of green manufacturing strategies across industries. Investments in cleaner technologies create long-term growth opportunities for the market.

Technological Advancements and Digital Integration in Waste Heat Recovery

New technologies strengthen the appeal of waste heat boilers in modern industries. Smart monitoring systems and IoT integration improve performance and predictive maintenance. Advanced materials enhance durability and efficiency, enabling longer operational lifespans. The Waste Heat Boiler Market evolves through automation, real-time monitoring, and optimized thermal recovery designs. Manufacturers introduce modular systems for flexible installations in diverse industrial setups. It enhances operational reliability and strengthens the role of waste heat boilers in sustainable industrial ecosystems.

Market Trends

Integration of Waste Heat Recovery in Renewable and Hybrid Energy Systems

The Waste Heat Boiler Market shows strong alignment with renewable and hybrid systems. Energy producers use waste heat boilers to improve efficiency in biomass, solar thermal, and combined renewable plants. It supports sustainable energy transition by reducing reliance on conventional fuels. Hybrid models that integrate waste heat recovery with renewables lower overall emissions. Countries with renewable adoption targets create opportunities for wider deployment. Demand for greener power solutions drives continuous system innovation and adoption.

- For instance, Babcock & Wilcox deployed two waste-to-energy plants in Nuuk and Sisimiut, Greenland. Each plant can process 2.95 t/h of municipal waste. The systems deliver district heating output of 6.18 MWt at 140 °C.

Rising Use of Modular and Compact Boiler Designs Across Industries

Manufacturers develop modular designs that allow easy installation and scalability. Industries prefer compact boilers for space-constrained facilities and faster deployment. The Waste Heat Boiler Market benefits from modular systems that reduce downtime and increase flexibility. It enables industries to expand capacity without replacing entire setups. Modular systems also allow phased investments, supporting cost control for operators. Growing preference for flexible and space-efficient designs influences global adoption rates.

- For instance, the Benson heat recovery steam generator (HRSG) can operate at supercritical pressure, up to 310 bar, boosting steam parameters beyond traditional limits. The technology is modular and has been widely adopted globally, demonstrating its effectiveness in combined cycle power plants.

Adoption of Smart Technologies and IoT-Based Monitoring Solutions

Digitalization shapes the future of industrial boiler operations. Companies integrate IoT-enabled sensors for real-time monitoring of temperature, pressure, and energy efficiency. The Waste Heat Boiler Market grows with adoption of predictive maintenance and automated performance tracking. It helps operators extend equipment lifespan while reducing unexpected failures. Data-driven insights improve decision-making for energy recovery and operational optimization. Rising digital integration strengthens competitiveness for both manufacturers and end users.

Focus on Low Emission Solutions and Compliance with Stringent Regulations

Stringent carbon reduction policies drive adoption of advanced boiler technologies. Industries implement boilers designed to minimize nitrogen oxide and particulate emissions. The Waste Heat Boiler Market evolves with innovations in materials and low-emission combustion techniques. It enables industries to meet strict emission standards without compromising output. Regulatory bodies in Europe, North America, and Asia push compliance-driven investments. Commitment to sustainability ensures steady demand for environmentally compliant waste heat boilers.

Market Challenges Analysis

High Capital Costs and Complex Installation Requirements

The Waste Heat Boiler Market faces significant hurdles due to high upfront costs. Large-scale industrial setups require substantial investments in design, engineering, and installation. It often involves integration with existing infrastructure, making projects technically challenging and time-consuming. Small and medium enterprises hesitate to adopt due to limited financial capacity. Complex installation further demands skilled labor, which increases overall project expenses. High entry costs restrict adoption, especially in regions with limited capital availability.

Maintenance Demands and Operational Reliability Concerns

Frequent maintenance needs create barriers for industries relying on continuous operations. The Waste Heat Boiler Market requires regular inspection and upkeep to prevent breakdowns. It demands skilled technicians and access to specialized spare parts, raising operational costs. Unexpected downtime reduces efficiency benefits and discourages investment from resource-constrained firms. Aging equipment in heavy industries complicates integration with modern waste heat recovery systems. Reliability concerns limit acceptance, especially in industries with strict production schedules.

Market Opportunities

Expansion in Emerging Economies and Industrial Growth

The Waste Heat Boiler Market gains strong opportunities in fast-developing economies with rising industrialization. Sectors such as cement, steel, and petrochemicals expand rapidly in Asia-Pacific, Latin America, and the Middle East. It creates a strong need for energy-efficient solutions that cut fuel costs and reduce emissions. Governments in these regions promote clean energy projects, providing incentives for waste heat recovery systems. Industrial growth supports large-scale deployment, especially in heavy manufacturing clusters. Increasing investment in infrastructure and energy projects strengthens the adoption potential across emerging economies.

Technological Advancements and Shift Toward Sustainability

Innovations in boiler materials, design, and digital integration open new market avenues. The Waste Heat Boiler Market benefits from adoption of IoT-enabled monitoring, predictive maintenance, and automation. It enhances system efficiency while lowering operational risks for industries. Global focus on net-zero targets encourages adoption of solutions that reduce greenhouse gas emissions. New low-emission boiler designs support compliance with evolving environmental regulations. Growing emphasis on sustainable manufacturing creates long-term opportunities for advanced waste heat recovery technologies.

Market Segmentation Analysis:

By Type

The Waste Heat Boiler Market divides into water-tube boilers and fire-tube boilers. Water-tube boilers dominate due to their ability to handle high pressure and large steam capacities. They are widely used in heavy industries such as oil and gas, steel, and power generation. Fire-tube boilers hold steady demand in smaller facilities that require lower steam capacity and simpler operation. It provides cost advantages and easier maintenance for medium-scale applications. Both types remain essential, with water-tube units favored for large industrial plants and fire-tube models suited for compact installations.

- For instance, Nooter/Eriksen has delivered over 20 waste heat boiler units specifically tailored for coke‑oven applications. These BWBs feature radiant chambers and waterwall designs to manage high exhaust temperatures between 2,000 °F and 2,400 °F, and include sootblower integration to maintain boiler cleanliness under difficult ash conditions.

By Heat Source

The market segments by heat source into oil engine exhaust, gas engine exhaust, gas turbine exhaust, incinerator exit gases, and kiln and furnace gases. Gas turbine exhaust systems account for a significant share due to their wide use in power and cogeneration plants. Oil and gas engine exhausts also play a critical role in marine, refinery, and chemical industries. Kiln and furnace gases drive demand in cement, glass, and metal production, where energy efficiency remains a priority. Incinerator exit gases expand opportunities in waste-to-energy plants supported by sustainability policies. The Waste Heat Boiler Market grows steadily as industries integrate recovery systems across diverse processes.

- For instance, Forbes Marshall offers fully packaged, smoke‑tube waste heat recovery boilers (WHRBs). These units feature a modulating diverter damper with a sealing efficiency of 99.9 % and deliver a dryness fraction of 98.5% on the steam output.

By Temperature

Segmentation by temperature includes medium, high, and ultra-high ranges. Medium temperature boilers serve industries with moderate heat recovery requirements, such as food processing and textiles. High-temperature boilers dominate applications where large volumes of steam are needed for turbines or chemical processes. Ultra-high temperature systems gain momentum in sectors with extreme energy demands, such as steel and petrochemicals. It supports industries in reducing carbon footprints while meeting efficiency targets. Growth in high and ultra-high temperature segments reflects the rising push toward advanced energy recovery.

Segments:

Based on Type:

- Water-tube Boiler

- Fire Tube Boiler

Based on Heat Source:

- Oil Engine Exhaust

- Gas Engine Exhaust

Based on Temperature:

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds about 37% of the Waste Heat Boiler Market in 2024. Growth comes from strict energy rules and strong focus on reducing carbon emissions. Industries such as refining, chemicals, and steel are leading users. Power plants also install waste heat boilers to support combined heat and power systems. The United States makes up most of the regional share. Companies in this region invest in modern boilers with digital monitoring to improve efficiency and reduce downtime. Supportive policies and rising energy costs keep demand strong.

Asia-Pacific

Asia-Pacific is the largest region with nearly 47% share of the market. Strong growth in China, India, Japan, and South Korea drives demand. Heavy industries such as cement, steel, and petrochemicals are the main users. Governments in the region encourage companies to save energy and reduce emissions. Local manufacturing by suppliers makes projects cost-effective and easier to maintain. High-temperature and ultra-high-temperature boilers are in strong demand. Rapid industrial growth and government support make Asia-Pacific the most important region for this market.

Europe

Europe accounts for about 20% of the global Waste Heat Boiler Market. Strict rules on energy efficiency and emission limits push industries to adopt modern boilers. Cement, glass, and metals are major industries that use these systems. District heating projects in Northern and Central Europe also add demand. Companies invest in low-emission and modular designs to meet regional standards. High energy prices encourage faster adoption of energy recovery systems. Europe is expected to maintain steady growth under strong climate policies.

Latin America

Latin America holds 5–8% of the market share. Growth comes from industries such as cement, refining, and mining. Countries like Brazil, Mexico, and Chile encourage the use of clean and efficient technologies. Waste-to-energy and biomass projects also create opportunities for suppliers. Older plants are being upgraded with waste heat boilers to cut energy use. Partnerships between global suppliers and local firms help expand projects. Although growth is slower than in other regions, steady progress is expected.

Middle East & Africa

The Middle East & Africa make up 4–6% of the Waste Heat Boiler Market. Oil refineries, petrochemicals, and new gas-turbine plants drive most demand. Steel and cement industries are also increasing adoption to save energy and meet emission goals. Governments encourage efficiency as part of industrial diversification plans. International suppliers often work with local engineering firms for installation and services. Though smaller in size, the region shows strong potential for future growth.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Alfa Laval AB

- Bharat Heavy Electricals Limited (BHEL)

- Babcock & Wilcox Enterprises, Inc.

- Siemens Energy

- Nooter/Eriksen

- Forbes Marshall

- Bosch Thermotechnology

- Thyssenkrupp Industrial Solutions

- General Electric (GE)

- Thermax Limited

Competitive Analysis

The Waste Heat Boiler Market players such as Bosch Thermotechnology; Siemens Energy; Thermax Limited; General Electric (GE); Forbes Marshall; Alfa Laval AB; Thyssenkrupp Industrial Solutions; Babcock & Wilcox Enterprises; Bharat Heavy Electricals Limited (BHEL); Nooter/Eriksen. The Waste Heat Boiler Market focuses on efficiency, advanced design, and regulatory compliance. Companies invest in digital monitoring and predictive maintenance to improve performance and reduce downtime. Regional firms compete through cost advantages, localized engineering, and faster project execution. Global manufacturers emphasize modular designs, durable materials, and low-emission technologies to meet stricter energy and climate regulations. Service networks and long-term maintenance contracts strengthen customer trust and repeat business. The market remains highly competitive, with innovation, customization, and sustainability shaping long-term positioning.

Recent Developments

- In February 2025, Siemens Energy, and NEM Energy signed a new deal in order to deliver two horizontal Heat Recovery Steam Generators (HRSGs) for a new combined cycle power plant in Texas, USA. An estimated 1.2 GW will be produced by the facility when it is finished.

- In January 2025, Thermax has commissioned a 10 TPH biomass-fired hybrid boiler for a US-based pharmaceutical company in western India. Managed by Thermax Onsite Energy Solutions Limited (TOESL) under a build-own-operate model, the solution ensures efficient operations, reliable biomass fuel supply, and aligns with sustainability goals.

- In November 2023, Solex acquired Econotherm Ltd., a UK-based leader in waste heat recovery technology. With the acquisition, Solex was aimed to be in a better position to assist its clients in lowering the amount of primary energy used to generate industrial goods. The business is an expert in gas, liquid, and solid-to-solid heat exchange.

- In June 2023, Harvest Power Systems, introduced its novel waste heat recovery system within the Hamilton and Greater Toronto Area. The company’s clean technology solution, which has been set up and put into service at three Pizza locations, allows restaurants to effectively manage their energy consumption, lower operating expenses, and lower emissions.

Report Coverage

The research report offers an in-depth analysis based on Type, Heat Source, Temperature and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with rising demand for energy efficiency in industries.

- Governments will push adoption through stricter emission rules and efficiency targets.

- Digital monitoring and IoT integration will become standard in new systems.

- Modular and compact boiler designs will see higher demand for flexible projects.

- Heavy industries like cement, steel, and chemicals will continue to drive installations.

- Waste-to-energy and biomass projects will open new growth opportunities.

- Asia-Pacific will remain the fastest-growing region due to rapid industrialization.

- North America and Europe will focus on upgrades to meet sustainability goals.

- Partnerships between global suppliers and local firms will improve service and reach.

- Innovation in materials and low-emission technologies will shape long-term competitiveness.