Market Overview:

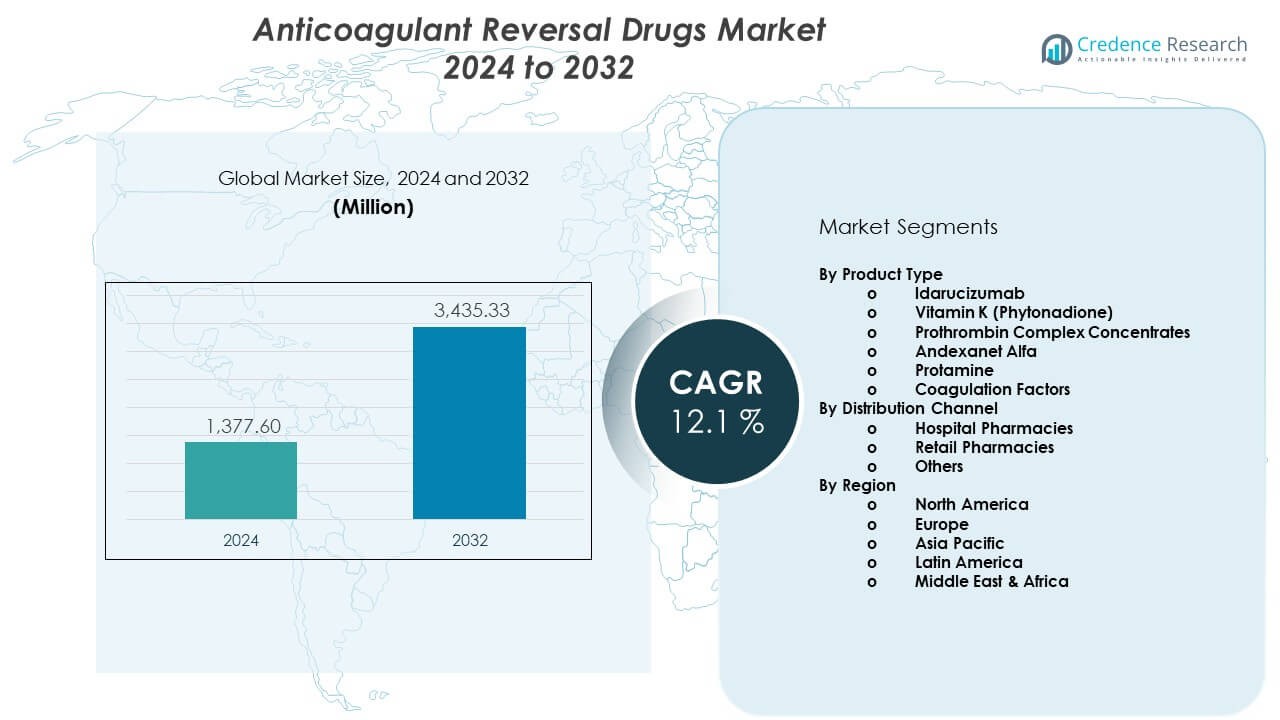

The Anticoagulant Reversal Drugs Market is projected to grow from USD 1377.6 million in 2024 to an estimated USD 3435.33 million by 2032, with a CAGR of 12.1% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Anticoagulant Reversal Drugs Market Size 2024 |

USD 1377.6 Million |

| Anticoagulant Reversal Drugs Market, CAGR |

12.1% |

| Anticoagulant Reversal Drugs Market Size 2032 |

USD 3435.33 Million |

Strong clinical demand drives the Anticoagulant Reversal Drugs Market, with hospitals focusing on drugs that reverse blood-thinning effects quickly during high-risk bleeding events. Doctors rely on targeted agents that work with specific anticoagulants to reduce complications and support fast recovery. Growing surgical loads expand the need for reliable reversal options in emergency rooms and intensive care units. Aging populations increase chronic anticoagulant use, which raises the need for dependable reversal solutions. Drug makers invest in faster, safer molecules that reduce side effects and improve treatment precision.

North America leads the Anticoagulant Reversal Drugs Market due to strong anticoagulant usage, advanced emergency care systems, and high awareness among clinicians. Europe follows with structured clinical guidelines and a wide shift toward specialized reversal therapies. Asia Pacific emerges as the fastest-growing region because expanding cardiac care, rising surgical volumes, and better emergency infrastructure increase adoption in China and India. Latin America and the Middle East show steady growth as healthcare systems improve access to advanced therapies and enhance management of anticoagulant-related complications.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Anticoagulant Reversal Drugs Market is projected to grow from USD 1377.6 million in 2024 to USD 3435.33 million by 2032, advancing at a 1% CAGR, driven by rising anticoagulant usage and stronger emergency care demand.

- North America holds 42%, supported by high anticoagulant use and advanced emergency systems; Europe follows with 30% due to structured clinical protocols; Asia Pacific holds 20%, driven by expanding cardiac care and improving hospital infrastructure.

- Asia Pacific is the fastest-growing region with a 20% share, strengthened by rising surgical volumes, wider adoption of targeted reversal agents, and rapid upgrades in emergency response capacity.

- By distribution channel, hospital pharmacies hold nearly 65% of total share due to the urgent-use nature of reversal therapies and strict stocking requirements in critical care units.

- By product type, prothrombin complex concentrates account for about 35%, supported by strong clinical preference for rapid clotting restoration during high-risk bleeding events.

Market Drivers:

Rising Emergency Bleeding Cases and Growing Dependence on Anticoagulants

The Anticoagulant Reversal Drugs Market grows due to rising emergency bleeding cases linked to widespread anticoagulant use. Hospitals treat more patients who need rapid reversal during trauma or invasive procedures. Doctors depend on agents that deliver quick action to stabilize bleeding. Aging populations increase the need for chronic anticoagulation therapy. Rising cardiovascular disease rates expand use of blood thinners. Emergency care units prepare for high-risk cases that demand instant reversal. New anticoagulants enter practice and require specific reversal agents. Healthcare systems improve readiness to manage life-threatening bleeding events.

- For instance, Boehringer Ingelheim reported in the RE-VERSE AD trial that idarucizumab achieved 100% immediate dabigatran reversal in more than 500 patients requiring urgent control of bleeding or emergency surgery.

Increasing Surgical Procedures and Demand for Rapid-Acting Reversal Therapies

Growing surgical procedures raise the need for fast-acting reversal drugs across operating rooms and critical care units. Surgeons depend on quick neutralization to reduce complications during complex interventions. Hospitals stock advanced reversal products to support emergency surgeries. It strengthens patient safety by reducing bleeding-related risks. Broader use of minimally invasive procedures increases the need for better bleeding control. Surgical teams seek predictable outcomes with reliable drug activity. Regulatory bodies support safer therapies that improve emergency response. Medical teams view rapid reversal as essential in high-risk surgical planning.

- For instance, CSL Behring’s Beriplex/Kcentra demonstrated rapid INR correction within 30 minutes in clinical studies for patients on warfarin requiring urgent reversal.

Strong Shift Toward Target-Specific Reversal Agents in Clinical Settings

Target-specific therapies gain demand as clinicians move toward safer and more predictable treatment pathways. Doctors prefer agents that match the mechanism of each anticoagulant. It improves precision and lowers treatment-related complications. Hospitals evaluate new molecules that offer immediate action. Clinical studies support improved recovery when reversal is targeted. Medical teams trust agents with clear efficacy profiles. On-label approvals strengthen adoption across emergency departments. Targeted reversal aligns with personalized treatment planning.

Growing Pharmaceutical R&D Investments Supporting Faster and Safer Molecules

Drug developers invest in molecules that offer faster onset and fewer adverse effects. Pharmaceutical companies expand pipelines focused on next-generation reversal therapies. New formulations aim for improved stability and controlled activity. It supports better management of severe bleeding episodes. Companies explore recombinant proteins and engineered agents for higher selectivity. Clinical trials validate performance benefits in acute care settings. Rising funding encourages innovation that meets hospital requirements. More players enter the space to gain a share of the expanding demand.

Market Trends:

Expansion of Recombinant and Bioengineered Reversal Molecules Across Hospitals

The Anticoagulant Reversal Drugs Market observes steady growth in recombinant and engineered molecules. Hospitals favor therapies designed with high purity and controlled action. Developers design molecules that deliver rapid neutralization with lower toxicity. It supports advanced emergency care planning. Researchers evaluate new biological platforms for higher efficacy. Bioengineered agents gain attention for targeted response. Hospitals integrate these solutions into critical care pathways. Drug companies scale production to meet rising clinical adoption.

- For instance, andexanet alfa (Andexxa), developed by Portola Pharmaceuticals, showed a 92% reduction in anti-Xa activity within minutes in the ANNEXA-4 study, confirming the effectiveness of its recombinant structure.

Increasing Adoption of Personalized Reversal Protocols in Acute Care Settings

Clinicians adopt personalized dosing to optimize reversal outcomes. Hospitals rely on patient-specific parameters to guide therapy decisions. Individualized care reduces complications linked to bleeding or under-reversal. It improves treatment precision during emergencies. Monitoring systems help clinicians track drug response in real time. Personalized models guide safer intervention for high-risk patients. Hospitals refine protocols to match patient profiles. Medical teams value reversal pathways built around precision care.

- For instance, Octapharma reported that individualized dosing of its Octaplex PCC improved hemostatic control in over 90% of emergency bleeding cases in published multicenter studies.

Integration of Point-of-Care Diagnostics to Support Real-Time Treatment Decisions

Point-of-care diagnostics enter emergency settings to guide faster reversal therapy. Clinicians gain immediate insight into coagulation status. Rapid testing supports quick decision-making during critical events. It lowers delays linked to laboratory confirmation. Advanced devices measure clotting parameters with higher accuracy. Emergency units combine diagnostics with targeted reversal strategies. Hospitals benefit from reduced procedural risks. Diagnostic integration improves workflow efficiency across care teams.

Growing Use of Digital Decision Support Systems for Reversal Management

Digital decision tools assist clinicians in selecting appropriate reversal strategies. Hospitals use clinical algorithms that reduce human error. Electronic systems offer guidance on dose optimization. It strengthens adherence to approved guidelines. Digital workflows improve coordination between emergency teams. Automated alerts support safe prescribing practices. Hospitals implement systems that merge patient data with evidence-based protocols. Technology adoption supports better patient outcomes.

Market Challenges Analysis:

High Treatment Costs and Limited Access in Resource-Constrained Healthcare Systems

The Anticoagulant Reversal Drugs Market faces challenges linked to high treatment costs across hospitals. Advanced reversal agents require significant spending for stocking and administration. Smaller facilities struggle to maintain adequate supplies. It impacts timely access during emergencies. Reimbursement limitations restrict adoption in certain regions. Patients in lower-income countries face barriers to advanced therapies. Healthcare budgets constrain broader distribution of modern reversal drugs. Uneven affordability slows expansion in emerging regions.

Complex Regulatory Requirements and Safety Risks Linked to High-Potency Molecules

Regulatory pathways for high-potency reversal agents remain complex and time-intensive. Drug approvals require extensive safety validation. Manufacturers adjust development plans to meet strict clinical standards. It delays launch timelines across global markets. Safety risks linked to powerful reversal activity limit aggressive adoption. Doctors monitor adverse effects with closer supervision. Companies face pressure to maintain strict manufacturing consistency. Regulatory demands add cost and complication to global expansion.

Market Opportunities:

Expansion of Emergency Care Infrastructure and Rising Investments in Acute Care Capacity

Growing investment in emergency infrastructure expands opportunities for the Anticoagulant Reversal Drugs Market. Governments upgrade trauma centers and critical care units. Hospitals adopt modern therapies to improve bleeding management. It supports higher use of targeted and rapid-acting agents. Training programs strengthen professional expertise in reversal care. More facilities prepare for rising cardiovascular procedures. Demand increases as emergency networks expand. Market participants develop partnerships to improve distribution efficiency.

Development of Next-Generation Targeted Therapies and Broader Clinical Research Activity

Growing research on next-generation and ultra-specific reversal agents creates strong market opportunities. Developers explore novel biologics for improved precision. Clinical trials evaluate safer and faster-acting candidates. It helps expand the treatment portfolio across hospitals. Pharmaceutical companies invest in innovative approaches that reduce side effects. Opportunities rise in specialized segments such as surgery, trauma, and intensive care. Broader acceptance of new therapies strengthens long-term growth potential. Industry players gain competitive advantages through continuous research activity.

Market Segmentation Analysis:

By Product Type

The Anticoagulant Reversal Drugs Market includes a diverse range of product types that address different anticoagulant mechanisms. Idarucizumab holds strong demand due to its targeted use for dabigatran reversal and its rapid action in emergency care. Vitamin K (phytonadione) remains widely used for warfarin reversal because doctors trust its long-established clinical profile. Prothrombin complex concentrates gain momentum for rapid correction of clotting factors during major bleeding events. Andexanet alfa sees rising adoption for reversing factor Xa inhibitors in life-threatening situations. Protamine retains relevance for heparin reversal in surgical and procedural settings. Coagulation factors support broader clinical scenarios where immediate clot restoration is required. Each product contributes to the market by addressing a specific therapeutic need, and it supports flexible treatment pathways across emergency care units.

- For instance, clinical data showed idarucizumab restored normal coagulation in 88–100% of patients within minutes. Vitamin K (phytonadione) remains widely used for warfarin reversal because doctors trust its long-established clinical profile.

By Distribution Channel

Distribution across the Anticoagulant Reversal Drugs Market is driven mainly by hospital pharmacies due to the urgent-care nature of these therapies. Hospitals maintain priority access because critical cases require immediate availability and controlled storage conditions. Retail pharmacies contribute to outpatient management where long-term anticoagulation support is needed. Other distribution channels serve specialized clinics and emergency centers that rely on faster procurement cycles. Hospital networks continue to dominate due to higher case volumes and strict clinical protocols. Retail penetration grows as more patients seek guidance outside hospital settings. The combined distribution framework ensures steady product access across varied treatment environments.

- For instance, market analyses and supply chain information indicate that Fresenius Kabi is a key global supplier of vitamin K and protamine sulfate, with an established generic portfolio and active participation in hospital-focused distribution channels in the U.S..

Segmentation:

By Product Type

- Idarucizumab

- Vitamin K (Phytonadione)

- Prothrombin Complex Concentrates

- Andexanet Alfa

- Protamine

- Coagulation Factors

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Regional Analysis:

North America

North America holds the largest share of the Anticoagulant Reversal Drugs Market, accounting for roughly 42% of global revenue. Strong anticoagulant usage across cardiovascular and stroke patients drives steady demand. Hospitals maintain advanced emergency systems that support immediate access to reversal therapies. It benefits from structured clinical guidelines that encourage rapid adoption of targeted agents. Major pharmaceutical companies operate extensive distribution networks across the region. Doctors rely on fast-acting products to manage high-risk bleeding events. Regulatory clarity also supports wider availability of approved therapies.

Europe

Europe represents about 30% of the global market and maintains strong growth driven by advanced healthcare infrastructure. Hospitals follow strict clinical protocols for bleeding management, which supports consistent uptake of modern reversal drugs. Countries strengthen national programs that improve patient safety during emergency interventions. The Anticoagulant Reversal Drugs Market benefits from rising anticoagulant use across aging populations. Doctors prefer therapies with clear clinical evidence and predictable outcomes. It gains further traction through expanded access in major economies like Germany, France, and the United Kingdom. Regional research programs foster innovation and evaluation of new therapeutic options.

Asia Pacific, Latin America, and Middle East & Africa

Asia Pacific holds around 20% of the global share and emerges as the fastest-growing region due to rising surgical volumes and expanding critical care capacity. Growing adoption of factor-specific reversal agents supports stronger penetration in China, India, and Japan. Latin America contributes close to 5% of the market, reflecting steady improvements in hospital readiness and emergency care funding. The Anticoagulant Reversal Drugs Market gains visibility in countries enhancing cardiovascular treatment programs. The Middle East & Africa regions together account for roughly 3%, supported by selective investments in advanced therapies. It benefits from growing awareness of bleeding risks linked to anticoagulant therapy. Expansion of tertiary care centers strengthens adoption across urban hubs.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Pfizer Inc.

- AstraZeneca plc

- Reddy’s Laboratories Ltd.

- Boehringer Ingelheim International GmbH

- CSL Behring LLC

- Takeda Pharmaceutical Company Limited

- Octapharma AG

- Grifols S.A.

- LFB S.A.

- Covis Pharma Group

- Bausch Health Companies

- Amneal Pharmaceuticals

- Fresenius Kabi AG

- Portola Pharmaceuticals

- Perosphere Pharmaceuticals

Competitive Analysis:

The Anticoagulant Reversal Drugs Market features strong competition driven by global pharmaceutical companies that focus on safety, speed of action, and product reliability. Leading players invest in specialized reversal agents tailored for distinct anticoagulant classes, which strengthens clinical trust across hospitals. Companies expand manufacturing capacity to support growing emergency care needs. It benefits from broader research pipelines that introduce more selective and faster-acting molecules. Firms seek regulatory approvals across key regions to expand commercial reach. Strategic collaborations help improve access in developing markets. Competitors refine distribution networks to ensure rapid delivery to critical care units. Market differentiation rests on clinical performance, product stability, and robust safety profiles.

Recent Developments:

- In November 2025, Grifols Biotest received its first regulatory approval for a new Fibrinogen Concentrate (likely marketed as AdFIrstor similar). This approval marks a major milestone in the company’s “hemostasis and sealing” portfolio, offering a specific therapy for acquired fibrinogen deficiency, which is often a critical component of coagulopathy requiring reversal in surgical and trauma settings. The product is designed to reduce blood loss and the need for allogeneic blood products.

- In March 2025, Azurity Pharmaceuticals announced the successful completion of its acquisition of Covis Pharma Group from existing investors. This acquisition integrates Covis’s portfolio, including its cardiovascular and critical care assets, into Azurity’s operations. The deal strengthens the combined entity’s presence in the acute care market, potentially enhancing the commercial reach of Covis’s legacy products utilized in hospital settings.

- In January 2024, Octapharma USA announced the official commercial launch of Balfaxar (prothrombin complex concentrate, human-lans) in the United States. Approved by the FDA for the urgent reversal of acquired coagulation factor deficiency induced by Vitamin K antagonist (e.g., warfarin) therapy, Balfaxar offers a new non-activated 4-factor PCC option for adult patients requiring urgent surgery or invasive procedures. This launch represents the first major direct competition to the long-standing market leader, Kcentra.

Report Coverage:

The research report offers an in-depth analysis based on Product Type and Distribution Channel. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market. [replace all segments in report coverage].

Future Outlook:

- Rising adoption of targeted reversal agents will strengthen clinical outcomes across emergency departments.

- Hospitals will expand stock levels of rapid-acting drugs to support critical care readiness.

- Pharmaceutical companies will invest in safer biologics that reduce adverse-event risks.

- Personalized reversal protocols will gain traction across advanced healthcare systems.

- Digital decision tools will support faster dose adjustments and improved treatment precision.

- Growing anticoagulant use among aging populations will increase long-term demand.

- Regulatory agencies will accelerate approvals for therapies backed by strong clinical evidence.

- Emerging markets will expand access through better emergency infrastructure.

- Strategic partnerships will improve global supply chain efficiency.

- Research programs will explore novel mechanisms to improve reversal speed and stability.