CHAPTER NO. 1 : INTRODUCTION 30

1.1. Report Description 30

Purpose of the Report 30

USP & Key Offerings 30

1.2. Key Benefits for Stakeholders 31

1.3. Target Audience 31

CHAPTER NO. 2 : EXECUTIVE SUMMARY 32

CHAPTER NO. 3 : AUTOMOTIVE MOTOR CORE MARKET FORCES & INDUSTRY PULSE 34

3.1. Foundations of Change – Market Overview 34

3.2. Catalysts of Expansion – Key Market Drivers 36

3.2.1. Momentum Boosters – Growth Triggers 37

3.2.2. Innovation Fuel – Disruptive Technologies 37

3.3. Headwinds & Crosswinds – Market Restraints 38

3.3.1. Regulatory Tides – Compliance Challenges 39

3.3.2. Economic Frictions – Inflationary Pressures 39

3.4. Untapped Horizons – Growth Potential & Opportunities and Strategic Navigation – Industry Frameworks 40

3.5. Market Equilibrium – Porter’s Five Forces 41

3.6. Ecosystem Dynamics – Value Chain Analysis 43

3.7. Macro Forces – PESTEL Breakdown 45

3.8. Price Trend Analysis 47

3.8.1. Regional Price Trend 48

3.8.2. Price Trend by Type 48

3.9. Buying Criteria 49

CHAPTER NO. 4 : COMPETITION ANALYSIS 50

4.1. Company Market Share Analysis 50

4.1.1. Global Automotive Motor Core Market Company Volume Market Share 50

4.1.2. Global Automotive Motor Core Market Company Revenue Market Share 52

4.2. Strategic Developments 54

4.2.1. Acquisitions & Mergers 54

4.2.2. New Product Type Launch 55

4.2.3. Agreements & Collaborations 56

4.3. Competitive Dashboard 57

4.4. Company Assessment Metrics, 2024 58

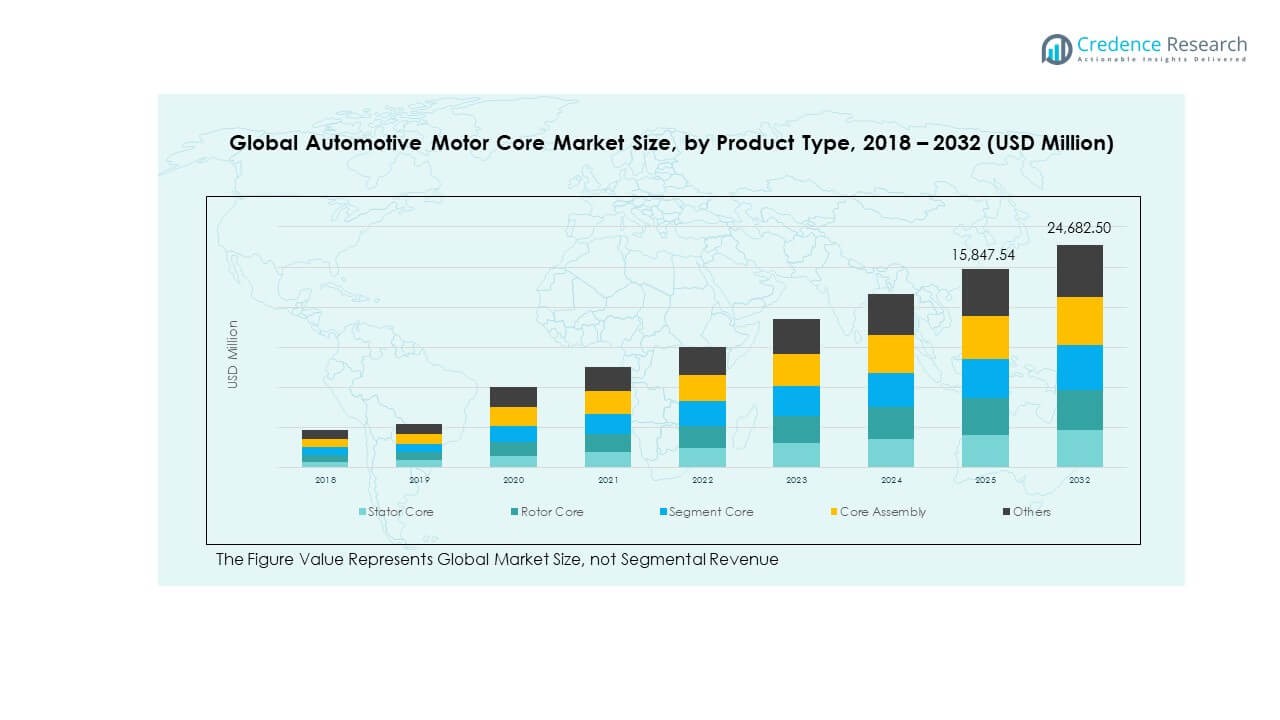

CHAPTER NO. 5 : GLOBAL MARKET ANALYSIS, INSIGHTS & FORECAST, BY PRODUCT TYPE 59

CHAPTER NO. 6 : GLOBAL MARKET ANALYSIS, INSIGHTS & FORECAST, BY APPLICATION 64

CHAPTER NO. 7 : GLOBAL MARKET ANALYSIS, INSIGHTS & FORECAST, BY END-USER 69

CHAPTER NO. 8 : GLOBAL MARKET ANALYSIS, INSIGHTS & FORECAST, BY MATERIAL TYPE 74

CHAPTER NO. 9 : GLOBAL MARKET ANALYSIS, INSIGHTS & FORECAST, BY MANUFACTURING PROCESS 78

CHAPTER NO. 10 : GLOBAL MARKET ANALYSIS, INSIGHTS & FORECAST, BY MOTOR SIZE 82

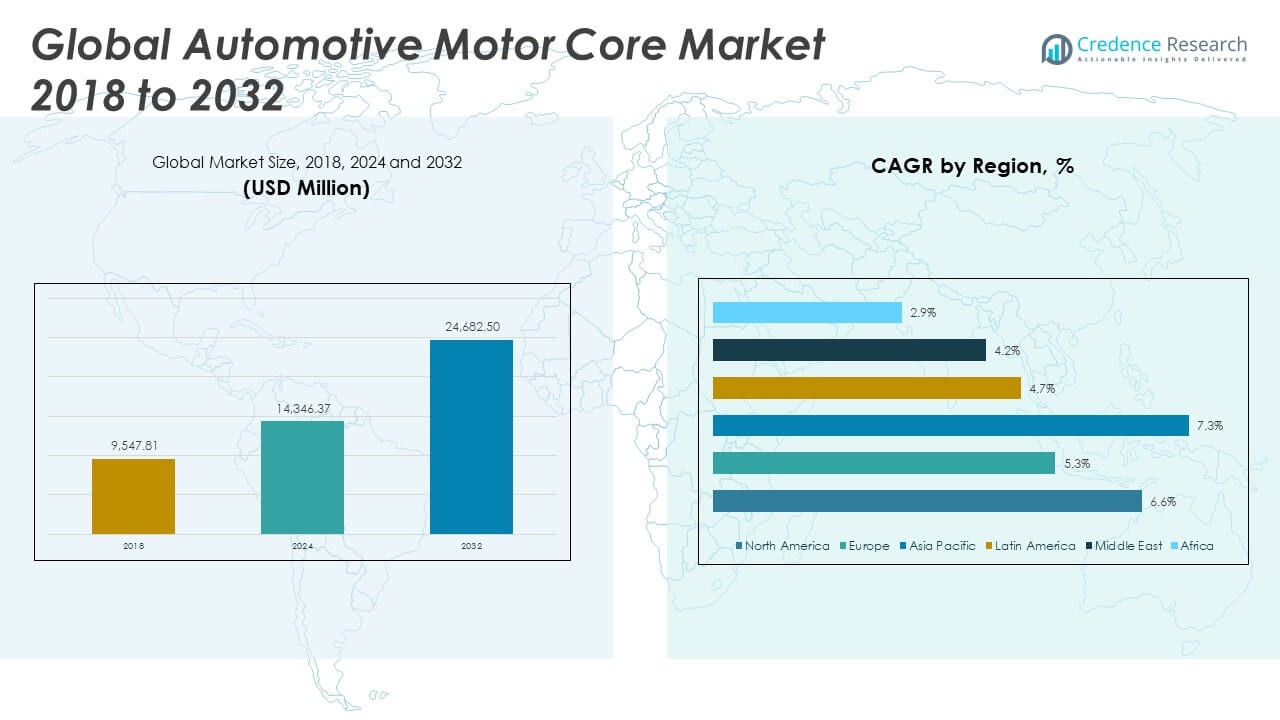

CHAPTER NO. 11 : GLOBAL MARKET ANALYSIS, INSIGHTS & FORECAST, BY REGION 86

CHAPTER NO. 12 : NORTH AMERICA MARKET ANALYSIS, INSIGHTS & FORECAST, BY COUNTRY 91

12.1. North America Market Analysis, Insights & Forecast, by Product Type 94

12.2. North America Market Analysis, Insights & Forecast, by Application 96

12.3. North America Market Analysis, Insights & Forecast, by End-user 98

12.4. North America Market Analysis, Insights & Forecast, by Material Type 100

12.5. North America Market Analysis, Insights & Forecast, by Manufacturing Process 102

12.6. North America Market Analysis, Insights & Forecast, by Motor Size 104

CHAPTER NO. 13 : EUROPE MARKET ANALYSIS, INSIGHTS & FORECAST, BY COUNTRY 106

13.1. Europe Market Analysis, Insights & Forecast, by Product Type 111

13.2. Europe Market Analysis, Insights & Forecast, by Application 113

13.3. Europe Market Analysis, Insights & Forecast, by End-user 115

13.4. Europe Market Analysis, Insights & Forecast, by Material Type 117

13.5. Europe Market Analysis, Insights & Forecast, by Manufacturing Process 119

13.6. Europe Market Analysis, Insights & Forecast, by Motor Size 121

CHAPTER NO. 14 : ASIA PACIFIC MARKET ANALYSIS, INSIGHTS & FORECAST, BY COUNTRY 123

14.1. Asia Pacific Market Analysis, Insights & Forecast, by Product Type 128

14.2. Asia Pacific Market Analysis, Insights & Forecast, by Application 130

14.3. Asia Pacific Market Analysis, Insights & Forecast, by End-user 132

14.4. Asia Pacific Market Analysis, Insights & Forecast, by Material Type 134

14.5. Asia Pacific Market Analysis, Insights & Forecast, by Manufacturing Process 136

14.6. Asia Pacific Market Analysis, Insights & Forecast, by Motor Size 138

CHAPTER NO. 15 : LATIN AMERICA MARKET ANALYSIS, INSIGHTS & FORECAST, BY COUNTRY 140

15.1. Latin America Market Analysis, Insights & Forecast, by Product Type 145

15.2. Latin America Market Analysis, Insights & Forecast, by Application 147

15.3. Latin America Market Analysis, Insights & Forecast, by End-user 149

15.4. Latin America Market Analysis, Insights & Forecast, by Material Type 151

15.5. Latin America Market Analysis, Insights & Forecast, by Manufacturing Process 153

15.6. Latin America Market Analysis, Insights & Forecast, by Motor Size 155

CHAPTER NO. 16 : MIDDLE EAST MARKET ANALYSIS, INSIGHTS & FORECAST, BY COUNTRY 157

16.1. Middle East Market Analysis, Insights & Forecast, by Product Type 163

16.2. Middle East Market Analysis, Insights & Forecast, by Application 165

16.3. Middle East Market Analysis, Insights & Forecast, by End-user 167

16.4. Middle East Market Analysis, Insights & Forecast, by Material Type 169

16.5. Middle East Market Analysis, Insights & Forecast, by Manufacturing Process 171

16.6. Middle East Market Analysis, Insights & Forecast, by Motor Size 173

CHAPTER NO. 17 : AFRICA MARKET ANALYSIS, INSIGHTS & FORECAST, BY COUNTRY 175

17.1. Africa Market Analysis, Insights & Forecast, by Product Type 180

17.2. Africa Market Analysis, Insights & Forecast, by Application 182

17.3. Africa Market Analysis, Insights & Forecast, by End-user 184

17.4. Africa Market Analysis, Insights & Forecast, by Material Type 186

17.5. Africa Market Analysis, Insights & Forecast, by Manufacturing Process 188

17.6. Africa Market Analysis, Insights & Forecast, by Motor Size 190

CHAPTER NO. 18 : COMPANY PROFILE 192

18.1. Siemens AG 192

18.2. Robert Bosch GmbH 195

18.3. Mitsubishi Electric Corporation 195

18.4. Nidec Corporation 195

18.5. ABB Ltd. 195

18.6. Hitachi Automotive Systems, Ltd. 195

18.7. Johnson Electric Holdings Limited 195

18.8. Toshiba Corporation 195

18.9. Denso Corporation 195

18.10. Continental AG 195

18.11. Valeo SA 195

18.12. Magna International Inc. 195

18.13. Mitsui High‑tec, Inc. 195

18.14. NHK Spring Co., Ltd. 195

18.15. Shinko Electric Industries Co., Ltd. 195

18.16. Brose Fahrzeugteile GmbH & Co. KG 195

18.17. Mahle GmbH 196

18.18. Yaskawa Electric Corporation 196

18.19. Wolong Electric Group Co., Ltd. 196

List of Figures

FIG NO. 1. Automotive Motor Core Market Revenue Share, By Product Type, 2024 & 2032 59

FIG NO. 2. Market Attractiveness Analysis, By Product Type 60

FIG NO. 3. Incremental Revenue Growth Opportunity by Product Type, 2024 – 2032 61

FIG NO. 4. Automotive Motor Core Market Revenue Share, By Application, 2024 & 2032 64

FIG NO. 5. Market Attractiveness Analysis, Application 65

FIG NO. 6. Incremental Revenue Growth Opportunity by Application, 2024 – 2032 66

FIG NO. 7. Automotive Motor Core Market Revenue Share, By End-user, 2024 & 2032 69

FIG NO. 8. Market Attractiveness Analysis, By End-user 70

FIG NO. 9. Incremental Revenue Growth Opportunity by End-user, 2024 – 2032 71

FIG NO. 10. Automotive Motor Core Market Revenue Share, By Material Type, 2024 & 2032 74

FIG NO. 11. Market Attractiveness Analysis, By Material Type 75

FIG NO. 12. Incremental Revenue Growth Opportunity by Material Type, 2024 – 2032 76

FIG NO. 13. Automotive Motor Core Market Revenue Share, By Manufacturing Process, 2024 & 2032 78

FIG NO. 14. Market Attractiveness Analysis, By Manufacturing Process 79

FIG NO. 15. Incremental Revenue Growth Opportunity by Manufacturing Process, 2024 – 2032 80

FIG NO. 16. Automotive Motor Core Market Revenue Share, By Motor Size, 2024 & 2032 82

FIG NO. 17. Market Attractiveness Analysis, By Motor Size 83

FIG NO. 18. Incremental Revenue Growth Opportunity by Motor Size, 2024 – 2032 84

FIG NO. 19. Automotive Motor Core Market Revenue Share, By Region, 2024 & 2032 86

FIG NO. 20. Market Attractiveness Analysis, By Region 87

FIG NO. 21. Incremental Revenue Growth Opportunity by Region, 2024 – 2032 88

FIG NO. 22. Automotive Motor Core Market Revenue Share, By Country, 2024 & 2032 91

FIG NO. 23. Automotive Motor Core Market Revenue Share, By Country, 2024 & 2032 106

FIG NO. 24. Automotive Motor Core Market Revenue Share, By Country, 2024 & 2032 123

FIG NO. 25. Automotive Motor Core Market Revenue Share, By Country, 2024 & 2032 140

FIG NO. 26. Automotive Motor Core Market Revenue Share, By Country, 2024 & 2032 157

FIG NO. 27. Automotive Motor Core Market Revenue Share, By Country, 2024 & 2032 175

List of Tables

TABLE NO. 1. : Global Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (USD Million) 62

TABLE NO. 2. : Global Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (USD Million) 62

TABLE NO. 3. : Global Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (K Units) 63

TABLE NO. 4. : Global Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (K Units) 63

TABLE NO. 5. : Global Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (USD Million) 67

TABLE NO. 6. : Global Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (USD Million) 67

TABLE NO. 7. : Global Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (K Units) 68

TABLE NO. 8. : Global Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (K Units) 68

TABLE NO. 9. : Global Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (USD Million) 72

TABLE NO. 10. : Global Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (USD Million) 72

TABLE NO. 11. : Global Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (K Units) 73

TABLE NO. 12. : Global Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (K Units) 73

TABLE NO. 13. : Global Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (USD Million) 77

TABLE NO. 14. : Global Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (USD Million) 77

TABLE NO. 15. : Global Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (USD Million) 81

TABLE NO. 16. : Global Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (USD Million) 81

TABLE NO. 17. : Global Automotive Motor Core Market Revenue, By Motor Size , 2018 – 2024 (USD Million) 85

TABLE NO. 18. : Global Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (USD Million) 85

TABLE NO. 19. : Global Automotive Motor Core Market Revenue, By Region, 2018 – 2024 (USD Million) 89

TABLE NO. 20. : Global Automotive Motor Core Market Revenue, By Region, 2025– 2032 (USD Million) 90

TABLE NO. 21. : North America Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (USD Million) 92

TABLE NO. 22. : North America Automotive Motor Core Market Revenue, By Country, 2025– 2032 (USD Million) 92

TABLE NO. 23. : North America Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (K Units) 93

TABLE NO. 24. : North America Automotive Motor Core Market Revenue, By Country, 2025– 2032 (K Units) 93

TABLE NO. 25. : North America Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (USD Million) 94

TABLE NO. 26. : North America Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (USD Million) 94

TABLE NO. 27. : North America Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (K Units) 95

TABLE NO. 28. : North America Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (K Units) 95

TABLE NO. 29. : North America Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (USD Million) 96

TABLE NO. 30. : North America Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (USD Million) 96

TABLE NO. 31. : North America Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (K Units) 97

TABLE NO. 32. : North America Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (K Units) 97

TABLE NO. 33. : North America Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (USD Million) 98

TABLE NO. 34. : North America Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (USD Million) 98

TABLE NO. 35. : North America Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (K Units) 99

TABLE NO. 36. : North America Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (K Units) 99

TABLE NO. 37. : North America Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (USD Million) 100

TABLE NO. 38. : North America Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (USD Million) 100

TABLE NO. 39. : North America Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (K Units) 101

TABLE NO. 40. : North America Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (K Units) 101

TABLE NO. 41. : North America Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (USD Million) 102

TABLE NO. 42. : North America Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (USD Million) 102

TABLE NO. 43. : North America Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (K Units) 103

TABLE NO. 44. : North America Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (K Units) 103

TABLE NO. 45. : North America Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (USD Million) 104

TABLE NO. 46. : North America Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (USD Million) 104

TABLE NO. 47. : North America Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (K Units) 105

TABLE NO. 48. : North America Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (K Units) 105

TABLE NO. 49. : Europe Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (USD Million) 107

TABLE NO. 50. : Europe Automotive Motor Core Market Revenue, By Country, 2025– 2032 (USD Million) 108

TABLE NO. 51. : Europe Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (K Units) 109

TABLE NO. 52. : Europe Automotive Motor Core Market Revenue, By Country, 2025– 2032 (K Units) 110

TABLE NO. 53. : North America Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (USD Million) 111

TABLE NO. 54. : North America Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (USD Million) 111

TABLE NO. 55. : Europe Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (K Units) 112

TABLE NO. 56. : Europe Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (K Units) 112

TABLE NO. 57. : Europe Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (USD Million) 113

TABLE NO. 58. : Europe Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (USD Million) 113

TABLE NO. 59. : Europe Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (K Units) 114

TABLE NO. 60. : Europe Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (K Units) 114

TABLE NO. 61. : Europe Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (USD Million) 115

TABLE NO. 62. : Europe Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (USD Million) 115

TABLE NO. 63. : Europe Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (K Units) 116

TABLE NO. 64. : Europe Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (K Units) 116

TABLE NO. 65. : Europe Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (USD Million) 117

TABLE NO. 66. : Europe Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (USD Million) 117

TABLE NO. 67. : Europe Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (K Units) 118

TABLE NO. 68. : Europe Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (K Units) 118

TABLE NO. 69. : Europe Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (USD Million) 119

TABLE NO. 70. : Europe Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (USD Million) 119

TABLE NO. 71. : Europe Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (K Units) 120

TABLE NO. 72. : Europe Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (K Units) 120

TABLE NO. 73. : Europe Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (USD Million) 121

TABLE NO. 74. : Europe Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (USD Million) 121

TABLE NO. 75. : Europe Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (K Units) 122

TABLE NO. 76. : Europe Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (K Units) 122

TABLE NO. 77. : Asia Pacific Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (USD Million) 124

TABLE NO. 78. : Asia Pacific Automotive Motor Core Market Revenue, By Country, 2025– 2032 (USD Million) 125

TABLE NO. 79. : Asia Pacific Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (K Units) 126

TABLE NO. 80. : Asia Pacific Automotive Motor Core Market Revenue, By Country, 2025– 2032 (K Units) 127

TABLE NO. 81. : Asia Pacific Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (USD Million) 128

TABLE NO. 82. : Asia Pacific Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (USD Million) 128

TABLE NO. 83. : Asia Pacific Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (K Units) 129

TABLE NO. 84. : Asia Pacific Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (K Units) 129

TABLE NO. 85. : Asia Pacific Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (USD Million) 130

TABLE NO. 86. : Asia Pacific Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (USD Million) 130

TABLE NO. 87. : Asia Pacific Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (K Units) 131

TABLE NO. 88. : Asia Pacific Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (K Units) 131

TABLE NO. 89. : Asia Pacific Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (USD Million) 132

TABLE NO. 90. : Asia Pacific Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (USD Million) 132

TABLE NO. 91. : Asia Pacific Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (K Units) 133

TABLE NO. 92. : Asia Pacific Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (K Units) 133

TABLE NO. 93. : Asia Pacific Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (USD Million) 134

TABLE NO. 94. : Asia Pacific Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (USD Million) 134

TABLE NO. 95. : Asia Pacific Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (K Units) 135

TABLE NO. 96. : Asia Pacific Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (K Units) 135

TABLE NO. 97. : Asia Pacific Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (USD Million) 136

TABLE NO. 98. : Asia Pacific Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (USD Million) 136

TABLE NO. 99. : Asia Pacific Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (K Units) 137

TABLE NO. 100. : Asia Pacific Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (K Units) 137

TABLE NO. 101. : Asia Pacific Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (USD Million) 138

TABLE NO. 102. : Asia Pacific Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (USD Million) 138

TABLE NO. 103. : Asia Pacific Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (K Units) 139

TABLE NO. 104. : Asia Pacific Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (K Units) 139

TABLE NO. 105. : Latin America Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (USD Million) 141

TABLE NO. 106. : Latin America Automotive Motor Core Market Revenue, By Country, 2025– 2032 (USD Million) 142

TABLE NO. 107. : Latin America Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (K Units) 143

TABLE NO. 108. : Latin America Automotive Motor Core Market Revenue, By Country, 2025– 2032 (K Units) 144

TABLE NO. 109. : Latin America Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (USD Million) 145

TABLE NO. 110. : Latin America Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (USD Million) 145

TABLE NO. 111. : Latin America Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (K Units) 146

TABLE NO. 112. : Latin America Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (K Units) 146

TABLE NO. 113. : Latin America Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (USD Million) 147

TABLE NO. 114. : Latin America Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (USD Million) 147

TABLE NO. 115. : Latin America Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (K Units) 148

TABLE NO. 116. : Latin America Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (K Units) 148

TABLE NO. 117. : Latin America Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (USD Million) 149

TABLE NO. 118. : Latin America Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (USD Million) 149

TABLE NO. 119. : Latin America Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (K Units) 150

TABLE NO. 120. : Latin America Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (K Units) 150

TABLE NO. 121. : Latin America Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (USD Million) 151

TABLE NO. 122. : Latin America Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (USD Million) 151

TABLE NO. 123. : Latin America Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (K Units) 152

TABLE NO. 124. : Latin America Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (K Units) 152

TABLE NO. 125. : Latin America Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (USD Million) 153

TABLE NO. 126. : Latin America Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (USD Million) 153

TABLE NO. 127. : Latin America Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (K Units) 154

TABLE NO. 128. : Latin America Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (K Units) 154

TABLE NO. 129. : Latin America Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (USD Million) 155

TABLE NO. 130. : Latin America Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (USD Million) 155

TABLE NO. 131. : Latin America Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (K Units) 156

TABLE NO. 132. : Latin America Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (K Units) 156

TABLE NO. 133. : Middle East Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (USD Million) 158

TABLE NO. 134. : Middle East Automotive Motor Core Market Revenue, By Country, 2025– 2032 (USD Million) 159

TABLE NO. 135. : Middle East Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (K Units) 160

TABLE NO. 136. : Middle East Automotive Motor Core Market Revenue, By Country, 2025– 2032 (K Units) 161

TABLE NO. 137. : Middle East Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (USD Million) 163

TABLE NO. 138. : Middle East Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (USD Million) 163

TABLE NO. 139. : Middle East Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (K Units) 164

TABLE NO. 140. : Middle East Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (K Units) 164

TABLE NO. 141. : Middle East Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (USD Million) 165

TABLE NO. 142. : Middle East Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (USD Million) 165

TABLE NO. 143. : Middle East Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (K Units) 166

TABLE NO. 144. : Middle East Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (K Units) 166

TABLE NO. 145. : Middle East Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (USD Million) 167

TABLE NO. 146. : Middle East Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (USD Million) 167

TABLE NO. 147. : Middle East Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (K Units) 168

TABLE NO. 148. : Middle East Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (K Units) 168

TABLE NO. 149. : Middle East Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (USD Million) 169

TABLE NO. 150. : Middle East Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (USD Million) 169

TABLE NO. 151. : Middle East Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (K Units) 170

TABLE NO. 152. : Middle East Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (K Units) 170

TABLE NO. 153. : Middle East Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (USD Million) 171

TABLE NO. 154. : Middle East Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (USD Million) 171

TABLE NO. 155. : Middle East Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (K Units) 172

TABLE NO. 156. : Middle East Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (K Units) 172

TABLE NO. 157. : Middle East Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (USD Million) 173

TABLE NO. 158. : Middle East Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (USD Million) 173

TABLE NO. 159. : Middle East Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (K Units) 174

TABLE NO. 160. : Middle East Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (K Units) 174

TABLE NO. 161. : Africa Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (USD Million) 176

TABLE NO. 162. : Africa Automotive Motor Core Market Revenue, By Country, 2025– 2032 (USD Million) 177

TABLE NO. 163. : Africa Automotive Motor Core Market Revenue, By Country, 2018 – 2024 (K Units) 178

TABLE NO. 164. : Africa Automotive Motor Core Market Revenue, By Country, 2025– 2032 (K Units) 179

TABLE NO. 165. : Africa Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (USD Million) 180

TABLE NO. 166. : Africa Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (USD Million) 180

TABLE NO. 167. : Africa Automotive Motor Core Market Revenue, By Product Type, 2018 – 2024 (K Units) 181

TABLE NO. 168. : Africa Automotive Motor Core Market Revenue, By Product Type, 2025 – 2032 (K Units) 181

TABLE NO. 169. : Africa Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (USD Million) 182

TABLE NO. 170. : Africa Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (USD Million) 182

TABLE NO. 171. : Africa Automotive Motor Core Market Revenue, By Application, 2018 – 2024 (K Units) 183

TABLE NO. 172. : Africa Automotive Motor Core Market Revenue, By Application, 2025 – 2032 (K Units) 183

TABLE NO. 173. : Africa Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (USD Million) 184

TABLE NO. 174. : Africa Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (USD Million) 184

TABLE NO. 175. : Africa Automotive Motor Core Market Revenue, By End-user, 2018 – 2024 (K Units) 185

TABLE NO. 176. : Africa Automotive Motor Core Market Revenue, By End-user, 2025 – 2032 (K Units) 185

TABLE NO. 177. : Africa Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (USD Million) 186

TABLE NO. 178. : Africa Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (USD Million) 186

TABLE NO. 179. : Africa Automotive Motor Core Market Revenue, By Material Type, 2018 – 2024 (K Units) 187

TABLE NO. 180. : Africa Automotive Motor Core Market Revenue, By Material Type, 2025 – 2032 (K Units) 187

TABLE NO. 181. : Africa Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (USD Million) 188

TABLE NO. 182. : Africa Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (USD Million) 188

TABLE NO. 183. : Africa Automotive Motor Core Market Revenue, By Manufacturing Process, 2018 – 2024 (K Units) 189

TABLE NO. 184. : Africa Automotive Motor Core Market Revenue, By Manufacturing Process, 2025 – 2032 (K Units) 189

TABLE NO. 185. : Africa Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (USD Million) 190

TABLE NO. 186. : Africa Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (USD Million) 190

TABLE NO. 187. : Africa Automotive Motor Core Market Revenue, By Motor Size, 2018 – 2024 (K Units) 191

TABLE NO. 188. : Africa Automotive Motor Core Market Revenue, By Motor Size, 2025 – 2032 (K Units) 191