| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Biosimilar Contract Manufacturing Market Size 2024 |

USD 7,658.80 million |

| Biosimilar Contract Manufacturing Market, CAGR |

14.90% |

| Biosimilar Contract Manufacturing Market Size 2032 |

USD 25,072.59 million |

Market Overview

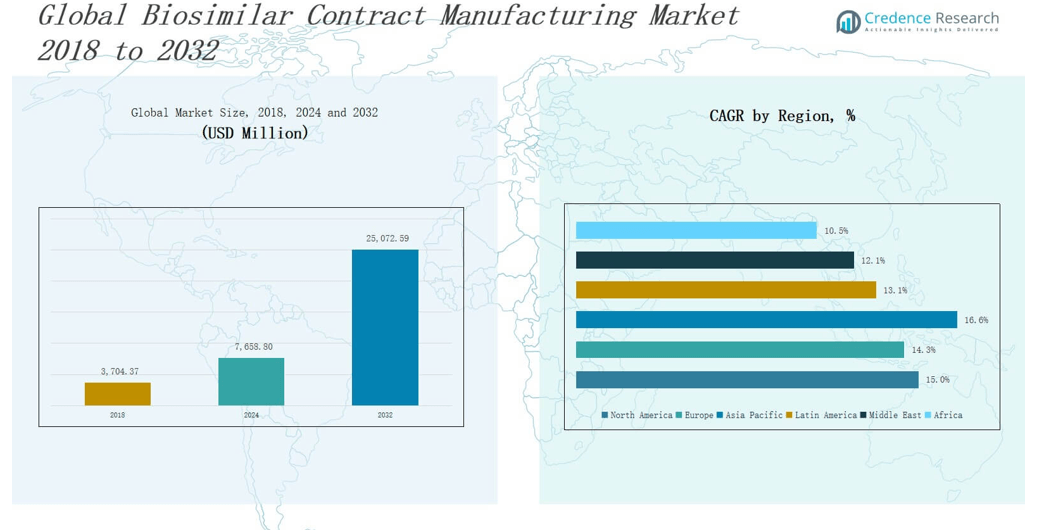

The Biosimilar Contract Manufacturing Market size was valued at USD 3,704.37 million in 2018 to USD 7,658.80 million in 2024 and is anticipated to reach USD 25,072.59 million by 2032, at a CAGR of 14.90 % during the forecast period.

The Biosimilar Contract Manufacturing Market is driven by increasing demand for cost-effective biologics, patent expirations of blockbuster biologic drugs, and the growing acceptance of biosimilars in regulated and emerging markets. Pharmaceutical companies are outsourcing manufacturing to specialized contract manufacturers to reduce operational costs, streamline production, and meet stringent regulatory requirements. Contract manufacturing organizations (CMOs) offer expertise in advanced bioprocessing technologies, scalability, and regulatory compliance, enabling faster time-to-market for biosimilar products. Market trends include rising investment in single-use bioreactors, expansion of GMP-certified facilities, and integration of automation and digital process controls to enhance manufacturing efficiency. Partnerships and strategic alliances between biopharma firms and CMOs are becoming more prevalent, aiming to optimize supply chain logistics and mitigate production risks. Additionally, the trend toward personalized medicine and complex biologics is prompting CMOs to diversify their service portfolios with modular, flexible production capabilities. The global focus on healthcare affordability continues to position biosimilars as a strategic solution, reinforcing the growth of contract manufacturing services.

The Biosimilar Contract Manufacturing Market spans key regions including North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. Europe leads the market with advanced regulatory support and established biomanufacturing infrastructure, followed by North America, which benefits from strong biosimilar uptake and innovation in biologics. Asia Pacific shows rapid growth driven by cost-efficient manufacturing hubs in China, India, and South Korea. Latin America and the Middle East are expanding through local production incentives and rising biosimilar demand, while Africa presents emerging opportunities through healthcare development and donor-funded initiatives. Key players shaping the global landscape include Samsung Biologics, Lonza, Catalent, WuXi Biologics, Boehringer Ingelheim Biopharmaceuticals GmbH, Biocon, AGC Biologics, Rentschler Biopharma SE, IQVIA Inc., Element Materials Technology, and Avid Bioservices. These companies compete through geographic reach, regulatory expertise, and integrated manufacturing solutions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Biosimilar Contract Manufacturing Market was valued at USD 3,704.37 million in 2018 and is projected to reach USD 25,072.59 million by 2032, growing at a CAGR of 14.90%.

- Rising demand for cost-effective biologics and the expiration of major biologic patents are driving contract manufacturing across therapeutic areas.

- Advanced bioprocessing technologies, such as single-use bioreactors and automation, are enhancing production efficiency and scalability among CMOs.

- Regulatory support from agencies like the FDA and EMA is accelerating biosimilar approvals and encouraging outsourcing to specialized manufacturers.

- High regulatory complexity and limited access to originator analytics present challenges, especially for smaller CMOs and new entrants.

- Europe holds the largest market share (32%) followed by North America (28%) and Asia Pacific (20%), with Latin America, the Middle East, and Africa showing steady growth.

- Key players include Samsung Biologics, Lonza, Catalent, WuXi Biologics, Boehringer Ingelheim Biopharmaceuticals, Biocon, AGC Biologics, and others focused on global expansion and regulatory alignment.

Market Drivers

Rising Demand for Affordable Biologics

The increasing need for cost-effective treatment options is a major growth driver for the Biosimilar Contract Manufacturing Market. Biosimilars offer comparable efficacy and safety to originator biologics but at significantly lower costs, attracting healthcare providers and payers worldwide. Governments and insurance bodies actively support biosimilar adoption to manage healthcare expenditures. This shift compels pharmaceutical companies to expand production through outsourcing. Contract manufacturers provide scalable, cost-efficient solutions aligned with regulatory standards. The market benefits from rising approvals of biosimilar products, fueling manufacturing demand. It continues to gain traction in both developed and emerging economies.

- For instance, Samsung Biologics partnered with Biogen to manufacture biosimilar products, leveraging large-scale facilities to meet growing demand.

Patent Expiry of Blockbuster Biologics

A wave of patent expirations for major biologic drugs is creating substantial opportunities in the Biosimilar Contract Manufacturing Market. Blockbusters such as Humira, Enbrel, and Rituxan have either lost exclusivity or face imminent competition. This scenario opens the door for biosimilar developers seeking rapid market entry. Contract manufacturers enable faster commercialization by offering end-to-end solutions, including formulation, cell line development, and aseptic filling. It helps biopharma firms bypass significant capital investment in infrastructure. The resulting competitive landscape accelerates outsourcing contracts for high-volume, compliant production.

- For instance, Coherus Biosciences released Yusimry in July 2023, pricing it at $995 per carton—significantly lower than the originator, aiming to increase patient access through contract manufacturing efficiencies.

Regulatory Support and Streamlined Approval Pathways

Supportive regulatory environments in regions such as the U.S., EU, and Japan drive momentum in the Biosimilar Contract Manufacturing Market. Agencies including the FDA and EMA have established clear biosimilar guidelines, simplifying the approval process and reducing time-to-market. These frameworks encourage manufacturers to invest in biosimilar pipelines and outsource to expert CMOs. It supports consistent compliance with evolving GMP standards. Contract manufacturers with proven regulatory track records gain competitive advantage. The alignment of policy and industry interests strengthens global biosimilar manufacturing initiatives.

Technological Advancements in Biomanufacturing

The adoption of advanced bioprocessing technologies significantly enhances the efficiency and flexibility of the Biosimilar Contract Manufacturing Market. Single-use bioreactors, continuous manufacturing, and automation reduce contamination risks and improve yield. CMOs invest in digitalized production environments that support real-time monitoring and data integrity. It enables scalable, reproducible output critical for biosimilar quality assurance. These innovations allow faster turnaround and cost control. Technology-driven production models are becoming standard among leading biosimilar CMOs, supporting global competitiveness.

Market Trends

Expansion of Strategic Partnerships and Outsourcing Models

Biopharmaceutical companies are increasingly engaging in long-term partnerships with contract manufacturing organizations to reduce capital expenditure and mitigate production risks. These alliances range from development-stage collaborations to full-scale commercial supply agreements. The Biosimilar Contract Manufacturing Market is witnessing heightened activity in co-development and joint venture models. It strengthens supply chains and improves time-to-market. Small and mid-sized biotech firms, in particular, rely on these partnerships to access technical expertise and GMP-certified infrastructure. Outsourcing continues to evolve from transactional relationships to integrated, strategic engagements.

- For instance, Biocon Biologics entered a strategic alliance with Serum Institute of India in 2022 to leverage Serum’s manufacturing capacity for global distribution of biosimilar products.

Adoption of Single-Use and Modular Manufacturing Technologies

Single-use bioreactors and modular facilities are transforming the production landscape of the Biosimilar Contract Manufacturing Market. These technologies reduce turnaround time, minimize cross-contamination, and lower upfront investment. It allows contract manufacturers to offer flexible production capacity tailored to client needs. Modular systems support rapid scale-up and multi-product operations without long construction delays. This shift enables manufacturers to handle diverse biosimilar portfolios efficiently. CMOs with advanced, disposable-enabled setups are attracting more business from biosimilar developers.

- For instance, Thermo Fisher Scientific’s HyPerforma DynaDrive single-use bioreactors have been adopted by multiple CMOs to reduce turnaround times and minimize cleaning validation, supporting rapid changeovers between biosimilar products.

Integration of Digitalization and Automation in Production

Digital transformation is reshaping manufacturing processes in the Biosimilar Contract Manufacturing Market. CMOs are implementing automated workflows, real-time process monitoring, and AI-driven analytics to enhance productivity and maintain quality standards. It improves batch-to-batch consistency, reduces manual intervention, and ensures data integrity. These technologies support compliance with evolving regulatory requirements. Digital platforms also streamline documentation, enabling faster audits and reporting. CMOs adopting smart manufacturing systems position themselves as agile partners capable of meeting complex biosimilar production demands.

Growing Focus on Emerging Markets and Regional Hubs

Market participants are expanding biosimilar manufacturing capacity in emerging regions to serve local demand and reduce dependency on global supply chains. The Biosimilar Contract Manufacturing Market benefits from investments in Latin America, Asia-Pacific, and the Middle East, where governments promote local production. It enables faster regulatory approvals and improved market access. Regional hubs also allow CMOs to offer competitive pricing and proximity-based advantages. This trend reflects the global shift toward decentralized, region-specific biosimilar manufacturing strategies.

Market Challenges Analysis

High Regulatory Complexity and Cost of Compliance

Stringent regulatory requirements across multiple jurisdictions remain a key challenge in the Biosimilar Contract Manufacturing Market. Navigating the diverse standards of agencies such as the FDA, EMA, and PMDA demands extensive documentation, validation protocols, and continuous audits. It increases time-to-market and adds substantial compliance costs. Contract manufacturers must invest in advanced quality systems and skilled regulatory personnel to meet expectations. Delays in approvals due to changing biosimilar guidelines can disrupt manufacturing timelines. This complexity often restricts smaller CMOs from entering the market or scaling operations globally.

Limited Access to Innovator Cell Lines and Analytical Data

Biosimilar development relies heavily on reverse engineering, yet limited access to originator product cell lines and proprietary analytics creates technical barriers. The Biosimilar Contract Manufacturing Market must overcome challenges in replicating biologics’ structure, efficacy, and immunogenicity without direct reference to the innovator’s manufacturing process. It requires high-end analytical capabilities, which only a few CMOs possess at scale. Failure to match critical quality attributes can lead to regulatory rejection. These technical hurdles slow down development and raise production risks for biosimilar developers and their contract partners.

Market Opportunities

Rising Demand for Biosimilars in Emerging Economies

Expanding healthcare access and rising chronic disease prevalence are driving biosimilar demand across emerging markets. Countries in Asia-Pacific, Latin America, and the Middle East are implementing favorable regulatory frameworks and pricing policies to encourage biosimilar adoption. The Biosimilar Contract Manufacturing Market has an opportunity to support regional biopharma companies with cost-efficient, scalable manufacturing services. It can offer local production capabilities that align with regional quality and distribution requirements. CMOs with regional presence gain competitive advantage through faster response times and regulatory familiarity. These geographies represent untapped growth potential for contract manufacturing partnerships.

Increased Outsourcing from Mid-Sized Biotech Firms

Mid-sized biopharma companies are shifting toward outsourcing to focus resources on R&D and pipeline expansion. These firms often lack in-house manufacturing capacity or regulatory infrastructure, creating a strong demand for full-service CMOs. The Biosimilar Contract Manufacturing Market can meet this demand by offering flexible production models, accelerated timelines, and technical expertise. It positions CMOs as strategic enablers in bringing biosimilars to market quickly and at scale. Opportunities also arise from growing interest in differentiated biosimilars and value-added formulations. Contract manufacturers capable of supporting development and clinical trial production will capture a larger share of this expanding segment.

Market Segmentation Analysis:

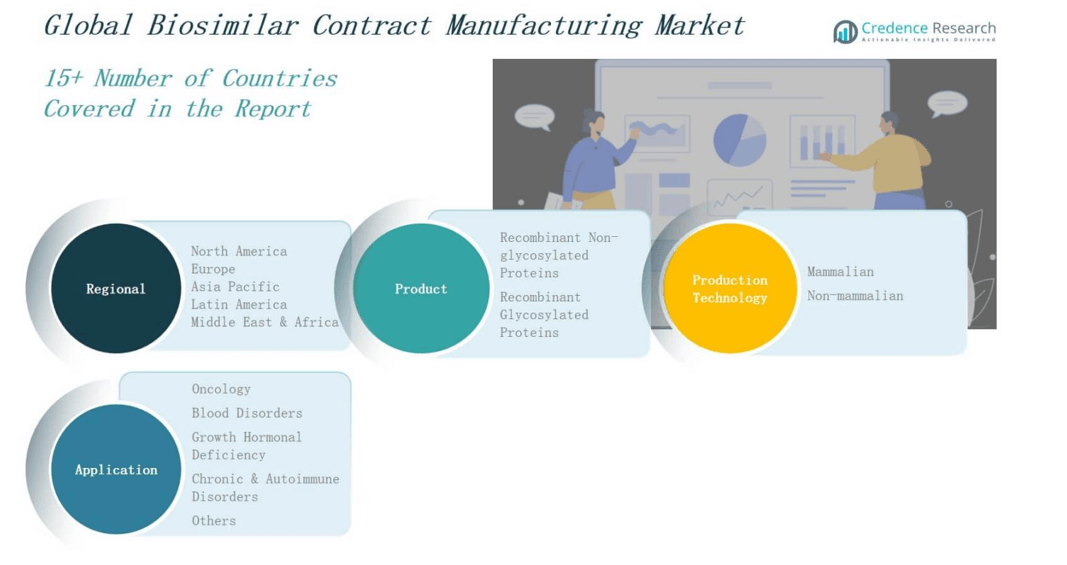

By Product

The Biosimilar Contract Manufacturing Market includes recombinant non-glycosylated and recombinant glycosylated proteins. Non-glycosylated proteins such as insulin, growth hormone, and interferons hold significant share due to simpler manufacturing requirements and high demand in chronic disease treatments. Glycosylated proteins, including monoclonal antibodies and erythropoietin, require complex production processes but dominate revenue generation due to their clinical importance in oncology and autoimmune therapies. It continues to see rising outsourcing for glycosylated protein production owing to increased technical demands.

- For instance, Lonza collaborated with Celltrion in 2024 to provide large-scale production support for erythropoietin biosimilars using its mammalian cell culture platform, with batch capacity exceeding 20,000 liters.

By Production Technology

Based on production technology, the Biosimilar Contract Manufacturing Market is segmented into mammalian and non-mammalian systems. Mammalian cell culture, particularly CHO cell lines, is the preferred platform for glycosylated protein manufacturing due to its ability to perform complex post-translational modifications. It drives higher demand for mammalian-based CMO services. Non-mammalian systems, such as bacterial and yeast platforms, support cost-effective and rapid production for simpler biosimilars like insulin and growth hormone. The technology choice depends on product complexity and cost efficiency.

- For instance, Samsung Biologics manufactures biosimilar trastuzumab using CHO cells, enabling production of complex monoclonal antibodies with human-like glycosylation patterns.

By Application

Application-wise, oncology dominates the Biosimilar Contract Manufacturing Market due to widespread use of monoclonal antibodies and rising cancer prevalence. Blood disorders follow, driven by erythropoietin and related biosimilars. Growth hormonal deficiency applications maintain steady demand, supported by pediatric and adult patient needs. Chronic and autoimmune disorders show strong growth potential due to increasing biologic prescriptions. It also sees expanding opportunities in other applications, including fertility treatments and metabolic conditions, broadening the scope of contract manufacturing engagements.

Segments:

Based on Product

- Recombinant Non-glycosylated Proteins

- Recombinant Glycosylated Proteins

Based on Production Technology

Based on Application

- Oncology

- Blood Disorders

- Growth Hormonal Deficiency

- Chronic & Autoimmune Disorders

- Others

Based on Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

The North America Biosimilar Contract Manufacturing Market size was valued at USD 1,064.41 million in 2018 to USD 2,165.95 million in 2024 and is anticipated to reach USD 7,120.74 million by 2032, at a CAGR of 15.0% during the forecast period. North America holds approximately 28% of the global market share, supported by strong biopharmaceutical infrastructure and high biosimilar adoption in the U.S. It benefits from early regulatory clarity provided by the FDA and growing pressure to reduce biologic therapy costs. Contract manufacturing organizations (CMOs) in this region are expanding capacity and investing in advanced cell-line development platforms. It supports rapid commercial-scale production of complex biosimilars. The region also sees increased outsourcing by small and mid-sized biotech firms focused on oncology and autoimmune disorders.

Europe

The Europe Biosimilar Contract Manufacturing Market size was valued at USD 1,601.16 million in 2018 to USD 3,232.06 million in 2024 and is anticipated to reach USD 10,179.64 million by 2032, at a CAGR of 14.3% during the forecast period. Europe accounts for the largest global market share at nearly 32%, driven by early biosimilar adoption and supportive regulatory policies from the European Medicines Agency (EMA). It hosts several established CMOs with GMP-certified facilities and proven experience in monoclonal antibody manufacturing. Biosimilar demand across Germany, France, and the UK continues to rise, creating sustained production contracts. The presence of strong public healthcare systems accelerates procurement of biosimilars through regional tenders. It promotes cost savings and widens access across chronic care applications.

Asia Pacific

The Asia Pacific Biosimilar Contract Manufacturing Market size was valued at USD 731.02 million in 2018 to USD 1,634.96 million in 2024 and is anticipated to reach USD 6,045.38 million by 2032, at a CAGR of 16.6% during the forecast period. Asia Pacific contributes around 20% of global revenue, driven by its rapidly expanding pharmaceutical industry and government efforts to localize biologic drug production. It benefits from lower manufacturing costs and strong clinical trial infrastructure in countries like India, China, and South Korea. Regional CMOs are investing in mammalian cell culture facilities to meet rising demand from global clients. It also attracts outsourcing due to competitive pricing and regulatory alignment with international standards. The region supports contract manufacturing growth through favorable biosimilar pricing and patient access policies.

Latin America

The Latin America Biosimilar Contract Manufacturing Market size was valued at USD 171.27 million in 2018 to USD 349.60 million in 2024 and is anticipated to reach USD 1,010.09 million by 2032, at a CAGR of 13.1% during the forecast period. Latin America holds around 5% of the global market and is gaining traction through rising biosimilar demand in Brazil, Argentina, and Colombia. Governments are adopting cost-control policies and reforming public healthcare procurement to include biosimilars. It drives regional manufacturers and international CMOs to expand operations or form local partnerships. The regulatory environment is evolving to streamline biosimilar approvals and ensure quality standards. Contract manufacturing helps regional biopharma firms overcome infrastructure limitations and scale production efficiently.

Middle East

The Middle East Biosimilar Contract Manufacturing Market size was valued at USD 93.48 million in 2018 to USD 174.83 million in 2024 and is anticipated to reach USD 472.05 million by 2032, at a CAGR of 12.1% during the forecast period. The region accounts for roughly 3% of global revenue and is seeing growing interest from multinational CMOs and investors. It benefits from healthcare modernization programs in countries like Saudi Arabia and the UAE. National health authorities are pushing for domestic biomanufacturing capacity to reduce import dependence. It creates new contract manufacturing opportunities aligned with local regulations and price controls. Biosimilars for oncology and chronic conditions represent key focus areas across hospital and retail segments.

Africa

The Africa Biosimilar Contract Manufacturing Market size was valued at USD 43.04 million in 2018 to USD 101.40 million in 2024 and is anticipated to reach USD 244.68 million by 2032, at a CAGR of 10.5% during the forecast period. Africa represents the smallest share of the global market at approximately 2%, but it holds long-term potential due to unmet medical needs and expanding healthcare infrastructure. Biosimilar adoption is rising through donor-funded programs and public-private partnerships. It enables CMOs to support cost-efficient production for high-burden diseases. Countries like South Africa and Egypt are leading early adoption and local manufacturing initiatives. It reflects the region’s growing interest in building self-sufficiency in biologic medicines.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- WuXi Biologics

- Avid Bioservices, Inc.

- Biocon

- Element Materials Technology

- Rentschler Biopharma SE

- Samsung Biologics

- AGC Biologics

- Boehringer Ingelheim Biopharmaceuticals GmbH

- IQVIA Inc.

- Catalent, Inc.

- Lonz

Competitive Analysis

The Biosimilar Contract Manufacturing Market features a competitive landscape dominated by global CDMOs with extensive biologics capabilities. Leading players such as Samsung Biologics, Lonza, WuXi Biologics, and Catalent offer end-to-end services across cell line development, process optimization, and commercial-scale production. It sees increased investments in mammalian cell culture facilities, single-use technologies, and regulatory compliance infrastructure. Mid-sized firms like AGC Biologics, Rentschler Biopharma SE, and Avid Bioservices compete by offering flexible capacity and specialized expertise in biosimilar development. Boehringer Ingelheim Biopharmaceuticals maintains a strong position through its integrated biomanufacturing platform. IQVIA supports contract manufacturing strategies with data-driven insights and clinical integration. Biocon enhances its global footprint through biosimilar production partnerships. Companies differentiate based on speed to market, cost efficiency, and ability to manage complex regulatory pathways. The market rewards firms that deliver scalable, compliant, and high-quality manufacturing services aligned with evolving client and therapeutic needs. Strategic collaborations and geographic expansion remain central to sustaining competitiveness.

Recent Developments

- In June 2025, Dr. Reddy’s Laboratories entered a strategic partnership with Alvotech to co-develop and commercialize a biosimilar of Keytruda (pembrolizumab), combining Alvotech’s development expertise with Dr. Reddy’s global reach in oncology markets.

- In 2025, Tanvex BioPharma completed the acquisition of Bora Biologics, strengthening its capabilities in biologics and biosimilar contract manufacturing.

- In October 2024, Teva Pharmaceuticals expanded its partnership with mAbxience by adding an oncology biosimilar candidate to their existing collaboration, aiming to address the growing demand for affordable cancer biologics.

- In April 2024, Alvotech signed an agreement with Teva Pharmaceuticals to manufacture a high-concentration interchangeable biosimilar of Humira (adalimumab) for Quallent Pharmaceuticals in the U.S.

Market Concentration & Characteristics

The Biosimilar Contract Manufacturing Market demonstrates moderate to high market concentration, with a few global players holding significant share due to advanced infrastructure, regulatory expertise, and global reach. Companies such as Samsung Biologics, Lonza, WuXi Biologics, and Catalent dominate based on their ability to offer end-to-end biologics services from cell line development to commercial manufacturing. It exhibits characteristics of high entry barriers, driven by capital-intensive facilities, complex regulatory requirements, and technical expertise in protein expression systems. The market favors firms with GMP-certified production sites, experience with mammalian cell cultures, and established client relationships. CMOs differentiate based on speed-to-market, capacity flexibility, and compliance with international standards. It also supports strategic partnerships, long-term contracts, and geographic diversification to mitigate risk and meet global demand. The growing trend toward outsourcing among small and mid-sized biopharma companies enhances competition among mid-tier players, while innovation and service integration shape the competitive dynamics of the market.

Report Coverage

The research report offers an in-depth analysis based on Product, Product Technology, Application and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for biosimilar contract manufacturing will rise due to increasing approvals of biosimilars across global markets.

- Biopharma companies will continue to outsource production to reduce costs and focus on core R&D.

- Single-use technologies and modular facilities will become standard in biosimilar manufacturing.

- Regulatory frameworks will evolve to support faster biosimilar approvals and promote outsourcing.

- Asia Pacific will attract more international outsourcing contracts due to cost-efficient manufacturing capabilities.

- CMOs will invest in capacity expansion and digital infrastructure to handle complex biologics.

- Strategic alliances between CDMOs and biosimilar developers will increase to accelerate time-to-market.

- Regional production hubs will emerge to reduce dependency on centralized manufacturing and ensure supply chain resilience.

- Technical expertise in mammalian cell culture will remain critical to support high-value biosimilars.

- Competition among mid-sized CMOs will intensify as they scale capabilities to serve growing demand.