Market Overview:

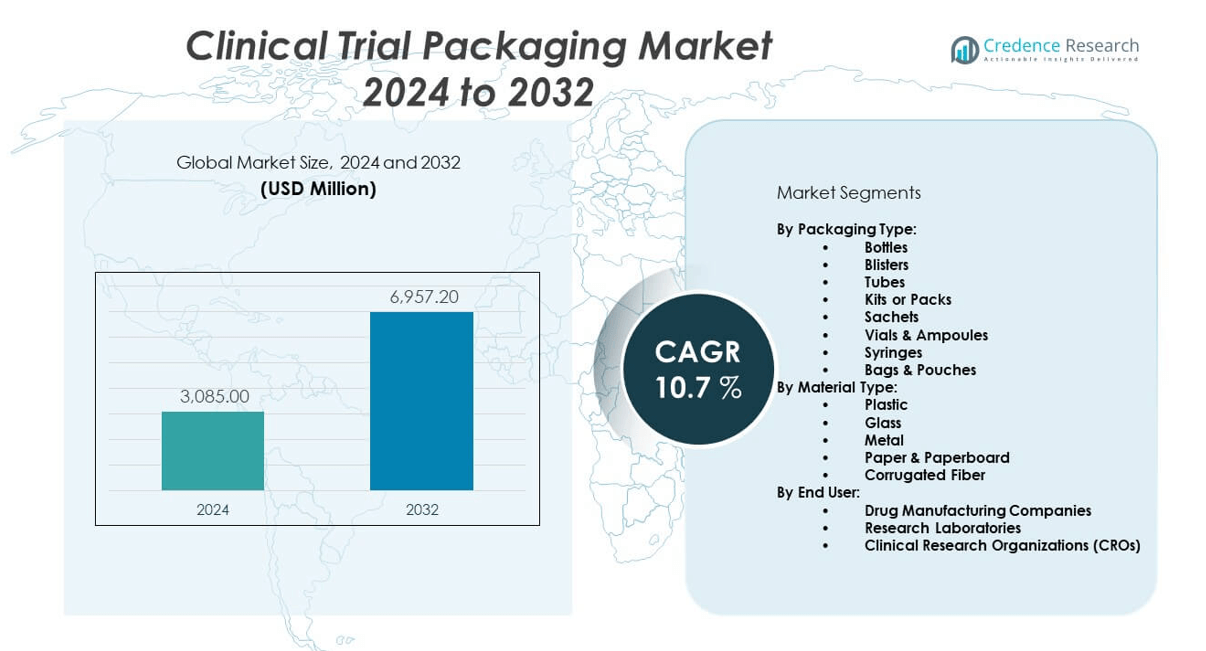

The Clinical trial packaging market is projected to grow from USD 3,085 million in 2024 to an estimated USD 6,957.2 million by 2032, with a compound annual growth rate (CAGR) of 10.7% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Clinical Trial Packaging Market Size 2024 |

USD 3,085 million |

| Clinical Trial Packaging Market, CAGR |

10.7% |

| Clinical Trial Packaging Market Size 2032 |

USD 6,957.2 million |

The market is expanding due to the increasing number of clinical trials, driven by rising drug development activities and the surge in biologics and personalized medicine. Packaging solutions must ensure product integrity, patient safety, and compliance with regulatory standards. Companies are investing in temperature-controlled, tamper-evident, and patient-friendly packaging formats. Outsourcing trends and demand for real-time tracking technologies further contribute to market growth, pushing suppliers to offer integrated, high-performance solutions.

North America leads the clinical trial packaging market due to its advanced pharmaceutical infrastructure, strong R&D investment, and favorable regulatory framework. Europe follows, supported by robust clinical research networks and stringent compliance standards. Asia Pacific is emerging as a high-growth region, driven by cost-efficient manufacturing, expanding clinical trial activity, and increasing government support in countries like India, China, and South Korea. Latin America and the Middle East show gradual growth as improvements in healthcare infrastructure and regulatory alignment open new opportunities for multinational sponsors.

Market Insights:

- The clinical trial packaging market is projected to grow from USD 3,085 million in 2024 to USD 6,957.2 million by 2032, at a CAGR of 10.7%.

- Increasing global clinical trial activity and the surge in biologics drive strong demand for specialized, compliant packaging solutions.

- Growth in personalized medicine and decentralized trials accelerates the need for modular, patient-friendly, and tamper-evident packaging formats.

- High customization costs and complex regulatory compliance requirements challenge packaging providers and delay timelines.

- Cold chain logistics and real-time tracking solutions are essential but increase operational complexity and cost.

- North America leads the market due to advanced pharmaceutical R&D infrastructure and strong regulatory frameworks.

- Asia Pacific is the fastest-growing region, supported by cost-effective manufacturing, trial volume expansion, and rising government investments.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Surge in Novel Drug Pipeline Drives Packaging Demand:

Global drug discovery programs accelerate at an unprecedented pace. Sponsors initiate more Phase I and II trials focused on oncology, rare diseases, and gene therapies. These novel molecules often require strict temperature and light control. Packaging vendors must engineer formats that secure stability throughout logistics. The Clinical trial packaging market responds with advanced barrier materials and compact insulation systems. Contract packagers invest in modular cleanrooms to manage small but varied batch sizes. Regulatory agencies approve fast‑track pathways, shrinking timelines and intensifying demand. Speed and reliability in secondary packaging now influence sponsor selection criteria.

- For instance, Catalent’s expansion of its Philadelphia facility in June 2024 added seven new temperature-controlled suites—each certified for operations below –20°C and 2–8°C, as confirmed in the company’s 2024 announcement.

Shift Toward Patient‑Centric Studies Elevates Design Priorities:

Trial protocols increasingly include direct‑to‑patient shipments, self‑administered dosing, and remote data capture. Sponsors demand intuitive packs that simplify adherence without professional supervision. It now features clear graphics, easy‑open seals, and child‑resistant yet senior‑friendly closures. Integrated instructive inserts support multilingual cohorts. The Clinical trial packaging market deploys human‑factors engineering to refine every component. Vendors test prototypes with patient focus groups before scale‑up. Enhanced usability reduces protocol deviations and costly resupply. Sponsors reward suppliers that prove measurable gains in compliance metrics.

- For instance, Almac Group 2024 roll-out of SmartPack clinical kits leverages direct patient and site input collected through structured usability testing .

Expansion of Outsourced Supply Chains Fuels Vendor Growth:

Pharma majors streamline internal operations and delegate packaging tasks to specialized contract service providers. It enables flexible capacity while controlling fixed costs. The outsourcing wave extends to label generation, randomization, and distribution hubs. The Clinical trial packaging market benefits through long‑term master service agreements and strategic alliances. Vendors broaden global footprints to support multi‑region studies under tight delivery windows. Coordinated systems cut transit delays and wastage. Sophisticated demand forecasting tools align production with fluctuating enrollment. Sponsors gain end‑to‑end visibility across the chain.

Digital Traceability Solutions Strengthen Compliance and Security:

Serialization mandates reach investigational products, compelling unique identifiers on every kit. Cloud platforms link each barcode to shipment data, environmental metrics, and patient assignment. It delivers instant recall capability and deters diversion. The Clinical trial packaging market integrates RFID tags, NFC chips, and blockchain‑based audit trails. Real‑time dashboards alert teams to temperature excursions or inventory gaps. Early warnings prevent protocol breaches and safeguard patient safety. Data analytics refine route planning and reduce cold‑chain excursions. Sponsors value such transparency during regulatory inspections.

Market Trends:

Smart Labels Gain Traction for Real‑Time Monitoring:

Continuous sensor technology migrates from commercial pharma into investigational supply chains. Thin electronic labels record temperature, humidity, and shock events. It uploads data via Bluetooth on receipt, giving sites proof of integrity. The Clinical trial packaging market deploys near‑field interfaces that sync with study apps. Sponsors avoid manual loggers and paper forms. Site staff spend less time on reconciliation, improving study efficiency. Aggregated data supports predictive maintenance of cold‑chain assets.

- For instance, Thermo Fisher Scientific’s Smart-Tracker data logger monitors temperature during storage and shipping, recording up to 4,000 readings per device per shipment.

Sustainability Targets Inspire Material Innovation:

Global climate commitments push sponsors to cut single‑use plastics and carbon footprints. It pursues recyclable polymers, molded pulp shippers, and bio‑based foams. The Clinical trial packaging market partners with material scientists to validate performance under ISTA protocols. Lifecycle assessments guide material selection without risking product stability. Sponsors earn ESG credits and boost corporate reputation. Governments introduce green procurement rules that favor low‑impact suppliers. Early adopters secure competitive bids through certified eco‑designs.

- For instance, SCHOTT Group, a major specialty glass manufacturer, has committed to achieving climate-neutral production by 2030, as confirmed by the Science Based Targets initiative (SBTi).

Modular Kitting Strategies Increase Study Flexibility:

Adaptive trial designs shift dosing schedules mid‑study. Modular kit architectures let sites add or swap components without new master labels. It uses perforated cartons, color‑coded sleeves, and variable‑data printing. The Clinical trial packaging market develops universal inserts that accept vials, syringes, or auto‑injectors. Sites assemble final packs just before dispensing, trimming waste. Sponsors adjust inventory allocations swiftly when cohorts change. Real‑time kit assembly supports complex oncology basket trials.

Decentralized Trials Propel Home‑Delivery Packaging:

Telemedicine visits and remote sample collection change distribution patterns. Couriers deliver investigational drugs directly to participants. It demands discreet, durable parcels that maintain temperature for extended doorsteps waits. The Clinical trial packaging market designs lightweight phase‑change shippers with tamper‑evident seals. Integrated return pouches collect used devices or biologic samples. Sponsors improve recruitment by removing travel burdens. Regulators endorse patient‑centric logistics when security and traceability stay intact.

Market Challenges Analysis:

Regulatory Divergence Across Regions Complicates Standardization:

Authorities in major markets issue distinct rules on labeling language, child resistance, and serial number formats. Sponsors struggle to apply one global kit template. It forces multiple SKU variants, lengthening production queues. The Clinical trial packaging market must track evolving guidelines and adjust artwork rapidly. Errors risk study holds or product recalls. Small biotech firms face steep compliance costs, limiting supplier choices. Vendors invest in robust document control systems yet still navigate approval delays. Harmonized policies remain elusive and prolong market complexity.

Cost Pressures Amid High Customization Limit Margins:

Each protocol stipulates unique blinding schemes, dosing calendars, and patient instructions. Tooling for specialty trays and inserts demands capital outlay. It compresses profit when batch sizes stay small. The Clinical trial packaging market passes some costs to sponsors, yet competition keeps price hikes modest. Rising raw material prices and labor shortages squeeze converters further. Automation offers relief but requires high volume to justify. Suppliers balance innovation with fiscal discipline to stay viable.

Market Opportunities:

Emerging Biologics Create Niche Specialty Packaging Potential:

Complex cell and gene therapies require cryogenic storage and strict chain‑of‑custody. It propels engineers to craft ultra‑low‑temperature shippers, tamper‑proof seals, and validated data loggers. The Clinical trial packaging market gains revenue from premium solutions that command higher margins. Limited manufacturing runs suit agile contract packagers. Early involvement in therapy development secures long contracts. Insurers recognize the value of uncompromised handling, endorsing investment in protective systems.

Growth in Emerging Regions Builds Capacity Investment Paths:

Asia, Latin America, and Eastern Europe attract sponsors seeking diverse populations and faster enrollment. It spurs local demand for compliant blistering, labeling, and distribution hubs. The Clinical trial packaging market expands through joint ventures and greenfield facilities near research clusters. Regulators modernize oversight, bolstering supplier confidence. Investors back cold‑chain networks and digital traceability platforms. Domestic firms upskill to meet GCP standards, creating new partnership opportunities.

Market Segmentation Analysis:

By Packaging Type: Broad Range to Match Complex Trial Needs

The clinical trial packaging market features a diverse range of packaging types tailored to the specific needs of investigational drugs and trial protocols. Bottles and blisters account for a significant portion of the market due to their suitability for solid oral dosage forms and ease of labeling. Vials and ampoules are essential for liquid formulations, particularly biologics and injectables requiring sterile containment. Syringes, especially prefilled variants, are increasingly used in late-phase and direct-to-patient studies. Kits or packs support complex trial designs by bundling multiple components for simplified dosing and improved patient adherence. Sachets, tubes, and bags & pouches offer flexible solutions for topical, unit-dose, and pediatric applications.

- For instance, Lonza provides full-cycle, GMP-compliant manufacturing for biologic drug products, including support for primary packaging development, qualification, and manufacturing of both toxicological batches and clinical trial reference materials.

By Material Type: Balancing Performance and Compliance

In terms of material type, plastic remains the dominant choice due to its lightweight nature, flexibility, and adaptability across various packaging forms. It is widely used in bottles, blisters, and secondary containers. Glass holds critical importance for injectable and biologic drugs that require chemical stability and barrier properties. Metal plays a limited but strategic role in protecting high-value shipments. Paper & paperboard are used extensively in outer cartons and instruction leaflets, contributing to sustainable practices. Corrugated fiber supports logistics, particularly in cold-chain shipping, where durability and insulation are essential for maintaining product integrity during transit.

- For instance, SCHOTT’s specialty glass packaging (used, for example, in vials for injectables) applies ISO 14067-certified cradle-to-gate lifecycle analysis, covering greenhouse gas emissions from raw material extraction through to finished product delivery, as independently validated by GUTCert.

By End User: Serving a Spectrum of Clinical Operations

Among end users, drug manufacturing companies lead demand, driven by continuous R&D pipelines and global trial operations. These companies either manage packaging in-house or collaborate with specialized partners. Clinical research organizations (CROs) represent a growing share as they offer integrated packaging and logistics services to sponsors lacking infrastructure. Research laboratories also contribute, particularly in early-stage clinical research where customized, small-batch packaging is essential. The clinical trial packaging market continues to evolve with these end users seeking compliant, cost-effective, and scalable solutions to support global trial execution.

Segmentation:

By Packaging Type:

- Bottles

- Blisters

- Tubes

- Kits or Packs

- Sachets

- Vials & Ampoules

- Syringes

- Bags & Pouches

By Material Type:

- Plastic

- Glass

- Metal

- Paper & Paperboard

- Corrugated Fiber

By End User:

- Drug Manufacturing Companies

- Research Laboratories

- Clinical Research Organizations (CROs)

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America Maintains Dominant Position Due to Strong Clinical Research Infrastructure

North America holds the largest share in the clinical trial packaging market, accounting for approximately 38% of global revenue in 2024. The region benefits from a high volume of clinical trials, especially in the United States, where pharmaceutical R&D investment remains robust. Major packaging vendors and contract development organizations (CDMOs) operate in close proximity to leading biotech and pharmaceutical hubs. Regulatory clarity from the FDA drives consistent demand for compliant, traceable packaging formats. Sponsors in the region prioritize cold-chain logistics and serialization, increasing the need for advanced packaging technologies. Canada contributes to growth with its expanding clinical trial base and favorable regulations for international sponsors.

Europe Secures a Strong Foothold Backed by Regulatory Compliance and R&D Support

Europe ranks second in the clinical trial packaging market, representing around 30% of the global share in 2024. The region’s growth is anchored in high regulatory standards, which encourage the use of secure, standardized packaging across cross-border trials. Countries like Germany, the United Kingdom, and France lead in trial volume, supported by established healthcare systems and academic research institutions. EU serialization mandates push for digital traceability and consistent labeling, driving innovation in packaging solutions. Logistics networks across the continent enable fast, secure shipment of investigational products. Eastern Europe continues to attract sponsors due to lower operational costs and increasing trial enrollments.

Asia Pacific Emerges as the Fastest-Growing Region in Trial Packaging Demand

Asia Pacific commands approximately 22% of the clinical trial packaging market in 2024 and is projected to grow at the highest CAGR through 2032. Growth is fueled by expanding clinical research activity in China, India, South Korea, and Japan. These countries offer cost-effective trial execution, large patient pools, and growing government support. Packaging vendors invest in local production facilities to meet demand and regulatory requirements specific to each country. The region’s rising biologics pipeline and adoption of decentralized trials create opportunities for temperature-controlled and home-delivery packaging. Increasing participation from domestic pharmaceutical companies further drives regional demand.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Almac Group

- PCI Pharma Services

- Fisher Clinical Services

- Catalent, Inc.

- Piramal Pharma Solutions

- Sharp Clinical Services

- WuXi AppTec

- Lonza Group Ltd

- Gerresheimer AG

Competitive Analysis:

The clinical trial packaging market is highly competitive, with several global and regional players offering specialized solutions tailored to complex trial protocols. Leading companies such as Almac Group, PCI Pharma Services, and Catalent, Inc. maintain strong market positions due to their end-to-end packaging, labeling, and logistics capabilities. These firms invest in advanced technologies, including cold chain systems, tamper-evident packaging, and smart labels. Smaller companies and CROs compete by offering flexible, customized services and faster turnaround times. The market rewards vendors that maintain regulatory compliance across global jurisdictions and ensure scalability in packaging formats. Strategic partnerships, M&A activities, and facility expansions continue to shape the competitive landscape. It reflects high demand for agile and secure packaging solutions that support patient-centric and decentralized trials.

Recent Developments:

- On July 16, 2025, Fisher Clinical Services’ parent company, Thermo Fisher Scientific, announced it will acquire Sanofi’s sterile manufacturing site in Ridgefield, New Jersey. The new site will expand Thermo Fisher’s drug product manufacturing and clinical trial packaging capabilities in the US as part of a strategic partnership, with the transaction expected to be completed in the second half of 2025.

- On June 25, 2025, Piramal Pharma Solutions broke ground on a $90 million expansion of its US operations in Lexington, Kentucky, and Riverview, Michigan. The Lexington site will more than double its sterile injectables manufacturing capacity by late 2027, while Riverview will provide expanded commercial capabilities for antibody-drug conjugates with new payload-linker manufacturing expected online by the end of 2025.

- In May 2025, Almac Group entered a global licensing agreement for ALM-401, a novel bispecific antibody-drug conjugate, with Formosa Pharmaceuticals. This partnership will drive ALM-401 through clinical development phases, leveraging Almac’s OmniaScape platform for protein engineering and medicinal chemistry.

- In May 2025, PCI Pharma Services completed its acquisition of Ajinomoto Althea, a US-based sterile fill-finish CDMO. This move strengthens PCI’s offering for advanced drug delivery and combination products, expanding their capacity for injectable formats and clinical trial packaging services.

- In January 2025, WuXi AppTec agreed to sell its US medical device testing facilities to NAMSA, closing the transaction on February 28, 2025. This divestiture sharpens WuXi AppTec’s focus on its core contract research, development, and manufacturing services for pharmaceutical products worldwide.

Market Concentration & Characteristics:

The clinical trial packaging market is moderately concentrated, with a mix of dominant global providers and niche specialists serving diverse trial demands. It demonstrates high regulatory sensitivity, requiring strict adherence to labeling, serialization, and cold-chain guidelines. The market is service-oriented and driven by customization, short lead times, and trial complexity. Outsourcing is prevalent, with sponsors relying heavily on third-party vendors for packaging design, production, and logistics. Innovation centers on usability, sustainability, and data integration to support decentralized and adaptive trials. It remains dynamic, shaped by therapeutic pipelines, trial globalization, and evolving patient engagement models.

Report Coverage:

The research report offers an in-depth analysis based on packaging type, material type, and end user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Growth in clinical trials globally will continue to fuel demand for advanced, compliant packaging solutions.

- Increasing adoption of decentralized and patient-centric trials will push packaging innovation.

- Demand for temperature-controlled packaging will rise with the expansion of biologics and gene therapies.

- Real-time tracking and serialization features will become standard in packaging formats.

- Outsourcing to specialized service providers will grow, especially among mid-sized and virtual biotech firms.

- Sustainability pressures will drive material innovation, especially in secondary and tertiary packaging.

- Customization needs for adaptive and personalized trial designs will boost modular packaging demand.

- Investment in automated, high-throughput packaging facilities will improve scalability and turnaround.

- Asia Pacific will gain momentum as a preferred hub for clinical packaging due to cost and volume advantages.

- Regulatory harmonization and digital compliance tools will streamline cross-border packaging operations.