Market Overview

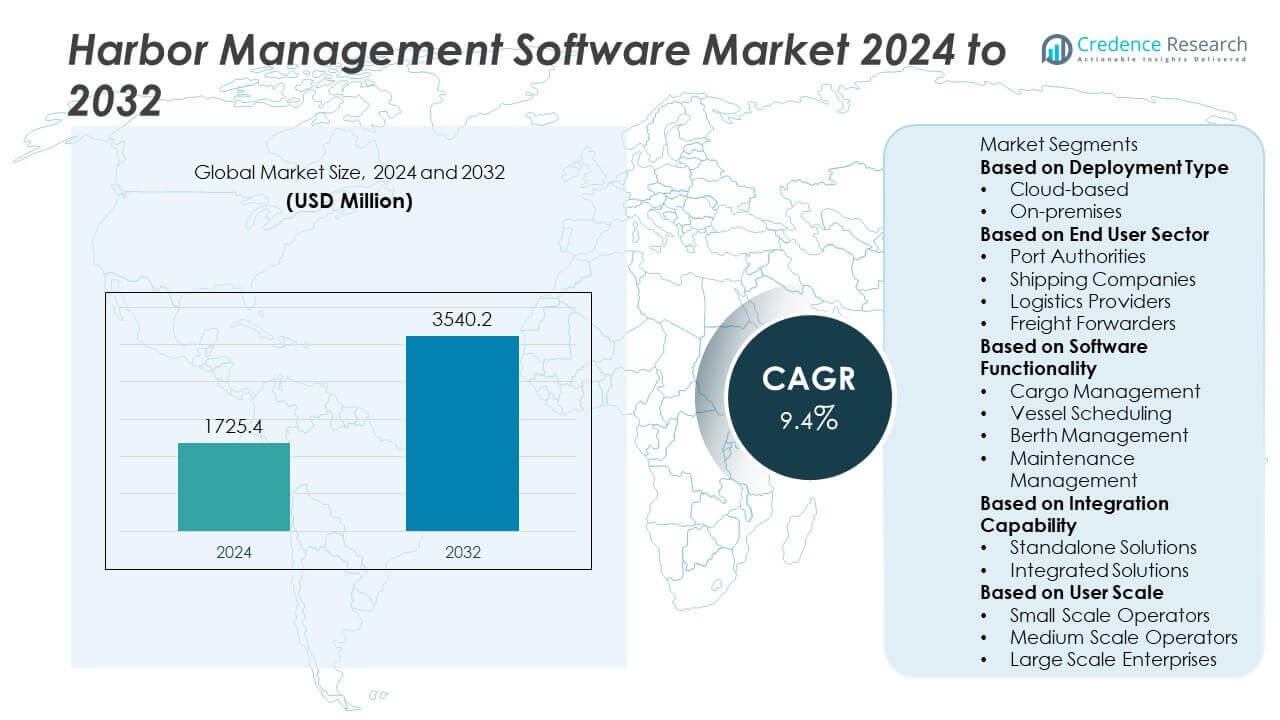

The Harbor Management Software market was valued at USD 1,725.4 million in 2024 and is projected to reach USD 3,540.2 million by 2032, growing at a CAGR of 9.4% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Harbor Management Software Market Size 2024 |

USD 1,725.4 million |

| Harbor Management Software Market , CAGR |

9.4% |

| Harbor Management Software Market Size 2032 |

USD 3,540.2 million |

The Harbor Management Software market grows with increasing demand for efficient port operations, real-time vessel tracking, and optimized resource allocation. Rising global trade volumes and stricter maritime regulations drive adoption across commercial ports, marinas, and naval facilities. It benefits from integration of AI, predictive analytics, IoT, and cloud-based platforms that enhance operational visibility and decision-making. Trends include the shift toward interoperable systems connecting ports with wider supply chain networks.

The Harbor Management Software market has a strong global footprint, with adoption driven by modernization initiatives in ports across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America leads in implementing advanced digital solutions for berth scheduling, cargo tracking, and compliance, supported by well-developed maritime infrastructure. Europe emphasizes environmentally sustainable port operations, integrating emission monitoring and automation. Asia-Pacific experiences rapid adoption through large-scale smart port projects and expanding trade networks, while Latin America and the Middle East & Africa focus on enhancing operational efficiency and connectivity. Key players such as Tideworks Technology, Konecranes, HarborSoft, and Portlink develop innovative, scalable platforms with cloud, IoT, and AI integration to meet diverse operational needs.

Market Insights

- The Harbor Management Software market was valued at USD 1,725.4 million in 2024 and is projected to reach USD 3,540.2 million by 2032, growing at a CAGR of 9.4% during the forecast period.

- The market expands due to rising demand for efficient port operations, real-time vessel tracking, and optimized berth allocation to handle increasing global trade volumes.

- Key trends include the integration of AI, predictive analytics, IoT, and cloud-based platforms to improve decision-making, operational visibility, and resource utilization in harbor management.

- Leading companies such as Tideworks Technology, Konecranes, HarborSoft, and Portlink focus on innovation, offering scalable, interoperable platforms that integrate with wider supply chain networks and meet sustainability goals.

- High implementation costs, complex integration with legacy systems, and cybersecurity risks present restraints, particularly for smaller ports in developing regions with limited budgets and infrastructure.

- North America leads in technology adoption with advanced port automation and compliance systems, Europe prioritizes environmentally sustainable solutions, and Asia-Pacific shows rapid growth through smart port initiatives. Latin America and the Middle East & Africa focus on enhancing operational efficiency, security, and trade connectivity.

- The long-term outlook remains strong, supported by global investment in port modernization, growing emphasis on green port initiatives, and the increasing need for connected, data-driven maritime operations to remain competitive in the evolving shipping industry.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Increasing Demand for Efficient Port Operations and Resource Optimization

The Harbor Management Software market benefits from the growing need to streamline port activities and improve resource utilization. Rising vessel traffic and cargo volumes require advanced tools to manage berthing schedules, cargo handling, and yard operations efficiently. It supports real-time tracking of assets, enabling harbor authorities to optimize docking space and reduce turnaround times. Integration with automated equipment and IoT sensors enhances visibility across operations. This improves decision-making, minimizes delays, and reduces operational costs. The demand for centralized systems that coordinate multiple port functions continues to expand globally.

- For instance, Tideworks Technology deployed its Mainsail 10 terminal operating system at Manzanillo International Terminal, enabling automation of over 1,800 container moves per day and reducing average vessel turnaround time by more than 3.5 hours through integrated berth planning and cargo tracking modules.

Stringent Regulatory Compliance and Safety Standards

Global trade regulations and maritime safety standards drive the adoption of advanced harbor management solutions. The Harbor Management Software market addresses compliance requirements by offering modules for vessel documentation, environmental monitoring, and safety inspections. It ensures adherence to International Maritime Organization (IMO) guidelines and port-specific operational rules. Enhanced record-keeping and automated reporting reduce administrative workload and error risks. Ports using such solutions can mitigate legal liabilities and maintain operational licenses. The ability to quickly adapt to evolving regulatory frameworks makes these systems indispensable.

- For instance, Wärtsilä’s acquisition of PortLink in June 2022 added a port management information system (PMIS) platform serving over 3,500 users across more than 20 countries, enabling efficient handling of vessel documentation and pilotage dispatch in strict regulatory environments.

Growing Adoption of Digitalization in Maritime Logistics

The maritime sector’s digital transformation supports the shift toward fully integrated harbor operations. The Harbor Management Software market benefits from technologies that enable real-time communication between port authorities, shipping companies, and customs. It facilitates electronic data interchange, reducing paperwork and speeding up cargo clearance processes. Cloud-based solutions allow access to operational data from remote locations, improving collaboration. Predictive analytics and AI integration help forecast port traffic and resource demands. This digital connectivity drives competitiveness for modern ports.

Rising Focus on Environmental Sustainability and Green Port Initiatives

Environmental concerns and sustainability goals influence the adoption of harbor management technologies. The Harbor Management Software market offers tools for monitoring emissions, managing waste, and optimizing fuel usage. It enables ports to track and reduce their environmental footprint in line with global decarbonization targets. Real-time environmental data collection supports compliance with emission control area regulations. Energy-efficient scheduling and optimized vessel movements contribute to reduced greenhouse gas emissions. These capabilities align with growing investments in green port infrastructure worldwide.

Market Trends

Integration of AI and Predictive Analytics in Port Operations

he Harbor Management Software market sees rising adoption of AI-driven modules that forecast vessel arrival times, cargo handling requirements, and berth allocation needs. Predictive analytics improves operational planning, reduces congestion, and optimizes workforce deployment. It allows port authorities to respond proactively to changes in shipping schedules or weather conditions. Machine learning models enhance accuracy in traffic predictions and maintenance scheduling. These capabilities help minimize idle times and increase throughput efficiency. The trend supports the transition toward data-driven port management.

- For instance, Tideworks highlighted that its AI‑driven predictive analytics platform forecasts optimal docking and unloading times, helping terminals reduce vessel wait times by an average of 17 minutes per call.

Expansion of Cloud-Based and SaaS Deployment Models

Cloud technology is transforming how ports deploy and manage software systems. The Harbor Management Software market benefits from scalable, subscription-based solutions that lower upfront investment and simplify upgrades. It enables multi-location access to operational data, allowing stakeholders to collaborate in real time. Cloud hosting also supports disaster recovery and secure data backup. Flexible deployment models make advanced harbor management tools accessible to both major ports and smaller terminals. The shift toward SaaS offerings reflects growing demand for agility and cost efficiency.

- For instance, Tideworks launched its “Forecast by Tideworks” web portal, enabling terminals to seamlessly communicate schedule forecasts with shipping lines, trucking companies, and brokers via cloud, with deployments reported across more than 30 ports globally

Adoption of IoT and Sensor-Based Monitoring Systems

Ports are increasingly implementing IoT-enabled systems to capture real-time data from vessels, cranes, and cargo yards. The Harbor Management Software market integrates these inputs to provide a unified operational view. It supports asset tracking, environmental monitoring, and equipment maintenance planning. Sensors detect anomalies that could affect safety or efficiency, triggering automated alerts. This integration reduces downtime and enhances operational transparency. The IoT-driven approach strengthens the ability to manage complex harbor environments effectively.

Focus on Interoperability and Integration with Supply Chain Platforms

Port management systems are evolving to seamlessly connect with broader supply chain technologies. The Harbor Management Software market incorporates APIs and integration frameworks to link with customs, shipping lines, and inland logistics platforms. It enables end-to-end visibility from cargo arrival to final delivery. Enhanced interoperability reduces data silos and accelerates information exchange across multiple stakeholders. Ports leveraging these capabilities improve coordination and throughput. This trend aligns with the industry’s move toward holistic and connected logistics ecosystems.

Market Challenges Analysis

High Implementation Costs and Infrastructure Limitations

The Harbor Management Software market faces adoption challenges due to significant upfront investment requirements for software licensing, customization, and integration with existing port infrastructure. Smaller ports and terminals often lack the budget to deploy advanced solutions, limiting market penetration. It requires compatible hardware, reliable internet connectivity, and trained personnel to operate efficiently. Many developing regions face infrastructural constraints that delay full-scale implementation. Complex integration with legacy systems further increases project timelines and costs. These barriers can slow the modernization efforts of ports aiming to improve operational efficiency.

Cybersecurity Risks and Data Privacy Concerns

Growing digitalization in port operations heightens exposure to cyber threats targeting critical maritime infrastructure. The Harbor Management Software market must address vulnerabilities that could disrupt operations, compromise vessel data, or expose sensitive trade information. It demands robust encryption, multi-layer security protocols, and compliance with global data protection regulations. The interconnected nature of modern ports means a single breach can have cascading impacts across supply chains. Rising cyberattack sophistication requires continuous investment in security updates and monitoring systems. Ensuring data integrity and operational resilience remains a top priority for software providers and port operators.

Market Opportunities

Rising Demand for Smart Port Infrastructure Development

The Harbor Management Software market can capitalize on the growing investment in smart port initiatives worldwide. Governments and port authorities are funding modernization projects that prioritize automation, sustainability, and digital connectivity. It supports integration with automated cranes, intelligent traffic systems, and real-time environmental monitoring tools. The ability to centralize operations and optimize berth allocation offers clear efficiency gains for expanding ports. Emerging markets are investing in technology to handle increasing cargo volumes and compete globally. This demand creates significant opportunities for solution providers to offer tailored, scalable platforms.

Expansion Potential in Emerging Maritime Economies

Rapid trade growth and infrastructure expansion in Asia-Pacific, Latin America, and Africa open new avenues for harbor management software adoption. The Harbor Management Software market can address operational inefficiencies in developing ports by introducing modular solutions that adapt to varying capacity levels. It enables smaller ports to adopt advanced capabilities without large-scale infrastructure overhauls. The rise in regional trade agreements and free trade zones further strengthens the case for digitalized port management. Vendors that offer localized support, multilingual interfaces, and integration with regional logistics networks can gain a competitive advantage. These opportunities align with the global push toward efficient and connected maritime trade hubs.

Market Segmentation Analysis:

By Deployment Type

The Harbor Management Software market segments by deployment type into on-premises and cloud-based solutions. On-premises deployments remain relevant in ports with strict data control requirements and dedicated IT infrastructure. They offer high customization levels and integration with legacy port systems, making them suitable for complex operations. Cloud-based solutions are gaining momentum due to their scalability, lower upfront costs, and remote accessibility. It enables stakeholders to access real-time operational data from any location, improving collaboration between port authorities, shipping lines, and logistics providers. Cloud platforms also simplify software updates and maintenance, making them attractive for ports seeking faster technology adoption. The flexibility of hybrid deployment models further supports diverse operational needs.

- For instance, Tideworks delivered a fully hosted deployment of its Mainsail 10 terminal operating system at Port Lafito in December 2021, giving the terminal access to a modern platform without needing on-site infrastructure upgrades.

By End User Sector

The Harbor Management Software market serves end users in commercial ports, fishing harbors, marinas, and naval bases. Commercial ports represent the largest segment, driven by the need to manage high vessel traffic, cargo volumes, and intermodal connections. Fishing harbors require specialized tools for vessel scheduling, catch documentation, and compliance with fisheries regulations. Marinas focus on berth management, customer reservations, and maintenance scheduling. Naval bases adopt advanced harbor management systems to enhance security, track vessel movements, and coordinate defense logistics. It addresses the operational priorities of each sector, ensuring optimized resource use and compliance with relevant regulations. The ability to cater to both large-scale and niche harbor environments strengthens the market’s versatility.

- For instance, The Maritime and Port Authority of Singapore describes digitalPORT@SG as a one-stop clearance portal that consolidates regulatory applications and anchorage management to streamline port calls, forecasts to support planning across terminals and landside partners.

By Software Functionality

Software functionality in the Harbor Management Software market includes berth management, vessel tracking, cargo and inventory management, billing and invoicing, and environmental monitoring. Berth management modules improve port utilization by optimizing docking schedules and reducing vessel wait times. Vessel tracking systems integrate with AIS (Automatic Identification System) data to provide accurate real-time movement updates. Cargo and inventory management tools streamline logistics, reduce bottlenecks, and enhance transparency. Billing and invoicing functionalities automate fee collection and improve revenue accuracy for port authorities. Environmental monitoring capabilities support compliance with emission control regulations and sustainability goals. It offers a unified platform that integrates these functionalities to improve operational efficiency, safety, and environmental performance.

Segments:

Based on Deployment Type

Based on End User Sector

- Port Authorities

- Shipping Companies

- Logistics Providers

- Freight Forwarders

Based on Software Functionality

- Cargo Management

- Vessel Scheduling

- Berth Management

- Maintenance Management

Based on Integration Capability

- Standalone Solutions

- Integrated Solutions

Based on User Scale

- Small Scale Operators

- Medium Scale Operators

- Large Scale Enterprises

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for 33.4% of the Harbor Management Software market share, driven by advanced port infrastructure, high digital adoption rates, and strong investment in maritime modernization projects. The United States leads the region with significant implementation of integrated port management platforms in major coastal hubs such as Los Angeles, Long Beach, and New York/New Jersey. It benefits from federal funding programs that support automation and real-time data exchange in port operations. Canada demonstrates steady growth, with ports like Vancouver and Halifax investing in cloud-based solutions for berth scheduling, cargo tracking, and environmental monitoring. The region’s competitive advantage lies in its focus on interoperability between harbor management systems and broader supply chain networks. The combination of regulatory compliance, security priorities, and efficiency-driven initiatives sustains robust market adoption.

Europe

Europe holds 29.1% of the Harbor Management Software market share, supported by strong environmental regulations, high trade volumes, and the modernization of port operations. Leading countries such as the Netherlands, Germany, and the United Kingdom deploy advanced software solutions to manage complex logistics, reduce vessel turnaround times, and optimize berth usage. It aligns with the European Union’s goals for greener ports through integration of emission tracking and sustainability modules. Scandinavian countries lead in adopting AI-based scheduling and predictive analytics for ice navigation and seasonal cargo flow adjustments. Mediterranean ports, including those in Spain and Italy, focus on integrating passenger terminal operations alongside cargo handling systems. Cross-border digital collaboration between European ports further drives efficiency and competitiveness.

Asia-Pacific

Asia-Pacific captures 26.7% of the Harbor Management Software market share, fueled by rapid port infrastructure expansion, industrial growth, and increasing trade volumes. China dominates the region with large-scale smart port projects in Shanghai, Ningbo-Zhoushan, and Shenzhen, integrating IoT, AI, and cloud-based platforms. Japan and South Korea lead in automation of container handling and real-time vessel tracking, ensuring efficiency in high-density maritime zones. India is expanding adoption through initiatives under the Sagarmala Program, aimed at modernizing key ports with digital management tools. Southeast Asian nations such as Singapore and Malaysia invest heavily in integrated port community systems to enhance competitiveness. It benefits from rising demand for efficient cargo handling to meet the needs of fast-growing economies.

Latin America

Latin America represents 6.1% of the Harbor Management Software market share, with Brazil and Mexico leading adoption due to trade expansion and port infrastructure modernization. Brazilian ports like Santos are integrating real-time cargo tracking and automated billing systems to reduce delays and improve transparency. Mexican ports focus on security, compliance, and integration with customs systems to accelerate cross-border trade. It is seeing increased deployment of cloud-based solutions to address budget constraints while improving scalability. The emphasis on modernizing export-oriented port facilities is expected to drive steady growth in this region.

Middle East & Africa

The Middle East & Africa account for 4.7% of the Harbor Management Software market share, driven by major investments in port infrastructure, especially in the Gulf Cooperation Council (GCC) countries. UAE ports such as Jebel Ali adopt advanced vessel scheduling and integrated cargo handling platforms to maintain global competitiveness. Saudi Arabia invests in smart port initiatives under Vision 2030, aiming to streamline logistics and improve efficiency in Red Sea and Gulf ports. In Africa, South Africa leads with adoption in Durban and Cape Town, focusing on improving operational safety and cargo throughput. It benefits from ongoing efforts to enhance trade connectivity, reduce congestion, and improve port service delivery.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The competitive landscape of the Harbor Management Software market features established technology providers and niche solution developers competing on innovation, integration capabilities, and service quality. Leading players include Tideworks Technology, Konecranes, HarborSoft, Portlink, DigiFleet, and Interswitch. These companies focus on delivering scalable platforms that support berth scheduling, vessel tracking, cargo management, and environmental monitoring. Tideworks Technology leverages decades of maritime software expertise to provide fully integrated terminal operating systems. Konecranes combines harbor software with advanced port automation and crane control solutions, enhancing operational efficiency. HarborSoft specializes in customizable harbor management platforms tailored for marinas, fishing ports, and small to mid-sized commercial harbors. Portlink emphasizes interoperability, connecting port systems to wider logistics and supply chain networks. DigiFleet integrates IoT-enabled fleet and asset management features into harbor operations, while Interswitch offers robust billing, invoicing, and compliance modules. Continuous R&D, AI and cloud integration, and a strong focus on cybersecurity position these players to address evolving market demands and regulatory requirements effectively.

Recent Developments

- In July 2025, Karpowership launched Africa’s first LNG-to-power project in Senegal, featuring a floating storage and regasification unit (FSRU) delivering gas to a powership.

- In July 2025, Karpowership signed an MOU with MOL and Kinetics to develop the world’s first floating data center platform on a retrofitted vessel.

- In September 2024, Tideworks unveiled a new data platform with a flexible architecture for near-real-time data movement and third-party system integration.

Market Concentration & Characteristics

The Harbor Management Software market demonstrates a moderately fragmented structure, with a mix of global technology providers, specialized maritime software developers, and regional solution vendors competing on innovation, integration capabilities, and service quality. It is characterized by high technological intensity, driven by the integration of AI, IoT, predictive analytics, and cloud-based platforms to optimize berth scheduling, vessel tracking, cargo management, and environmental monitoring. Leading players focus on developing interoperable systems that connect port operations with wider supply chain networks, enhancing efficiency and transparency. Smaller vendors target niche markets such as marinas, fishing harbors, and regional terminals with cost-effective, customizable solutions. The market serves diverse end-user segments, each requiring tailored functionalities to address specific operational demands, compliance needs, and infrastructure readiness. It is shaped by increasing digital transformation in maritime logistics, evolving regulatory frameworks, and the growing emphasis on sustainability, creating continuous opportunities for innovation and competitive differentiation

Report Coverage

The research report offers an in-depth analysis based on Deployment Type, End User Sector, Software Functionality, Integration Capability, User Scale and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with the growing need for efficient port operations and real-time visibility.

- Adoption of AI and predictive analytics will enhance decision-making and resource optimization.

- Cloud-based platforms will gain wider acceptance for scalability and remote accessibility.

- Integration with IoT devices will improve asset tracking and environmental monitoring.

- Demand for interoperable systems will increase to connect ports with global supply chain networks.

- Sustainability initiatives will drive the use of software for emission tracking and green port operations.

- Emerging markets will adopt modular solutions to modernize port infrastructure.

- Cybersecurity measures will become a critical focus for software providers.

- Automation in cargo handling and berth scheduling will accelerate deployment.

- Strategic partnerships between technology vendors and port authorities will strengthen market penetration.