Market Overview

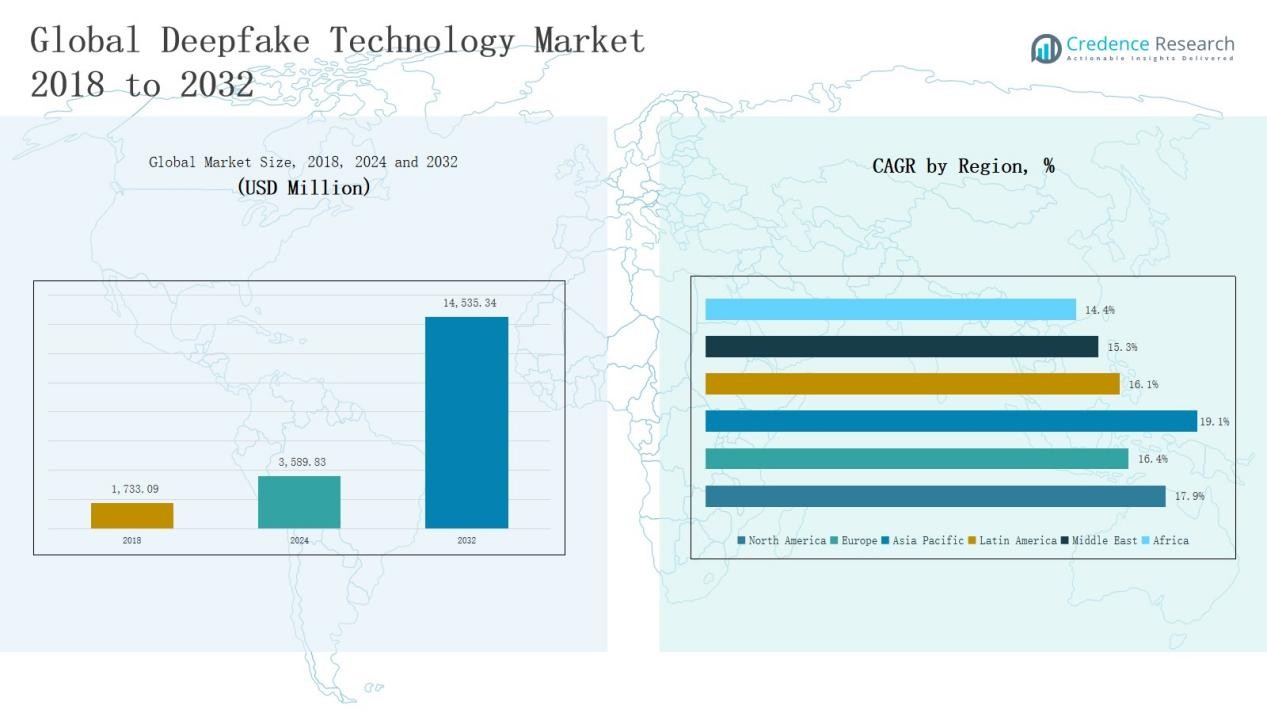

Deepfake Technology Market size was valued at USD 1,733.09 million in 2018 to USD 3,589.83 million in 2024 and is anticipated to reach USD 14,535.34 million by 2032, at a CAGR of 17.81% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Deepfake Technology Market Size 2024 |

USD 3,589.83 Million |

| Deepfake Technology Market, CAGR |

17.81% |

| Deepfake Technology Market Size 2032 |

USD 14,535.34 Million |

The Deepfake Technology Market is shaped by a mix of global tech leaders and specialized innovators. Major companies such as Microsoft, Google (Alphabet), Meta, and Adobe dominate through advanced AI capabilities and integration of deepfake tools into enterprise solutions. Specialized firms including Deeptrace (Sensity AI), Reality Defender, Truepic, DeepBrain AI, Zao, and Synthesia focus on niche areas like detection, authentication, and synthetic media generation, providing agility and innovation in the competitive landscape. Among regions, North America emerged as the leader with a 37% market share in 2024, supported by a strong AI ecosystem, enterprise adoption, and significant government investment in detection and cybersecurity technologies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

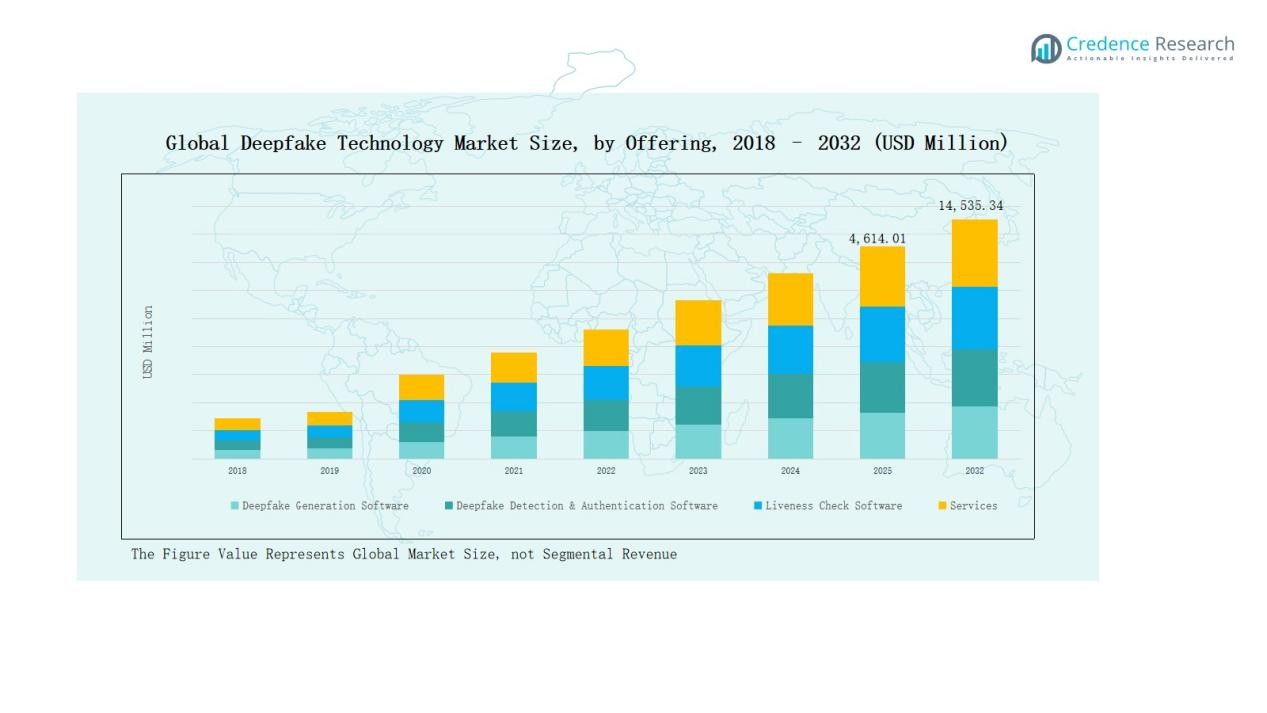

- The Deepfake Technology Market grew from USD 1,733.09 million in 2018 to USD 3,589.83 million in 2024, and is expected to reach USD 14,535.34 million by 2032.

- Deepfake generation software led with 46% share in 2024, driven by rising use in entertainment, social media, and marketing campaigns for creating realistic and personalized content.

- Generative Adversarial Networks (GANs) accounted for 41% share in 2024, remaining the backbone for synthetic content creation, while transformer models gain momentum for real-time voice and video synthesis.

- Enterprises dominated with 49% share in 2024, leveraging deepfake tools for marketing, e-learning, customer engagement, and simulations, with government agencies emerging as a key secondary segment.

- North America led with 37% share in 2024, followed by Asia Pacific at 26% and Europe at 15%, while Latin America, the Middle East, and Africa collectively represented 22% of the global market.

Market Segment Insights

By Offering

Deepfake generation software dominated the market with a 46% share in 2024. The segment’s growth is driven by rising adoption in entertainment, social media, and marketing campaigns for creating hyper-realistic content. Increasing accessibility of open-source platforms and demand for personalized video content further strengthen its dominance. Detection and authentication software is expanding steadily as organizations invest in tools to combat misinformation and fraud.

- For instance, DeepFaceLab, an open-source tool widely adopted by creators, has become one of the most downloaded frameworks for training deepfake models.

By Technology

Generative Adversarial Networks (GANs) led the technology segment with a 41% share in 2024. GANs remain the backbone of most deepfake applications due to their ability to create highly convincing synthetic images and videos. Their scalability and integration into cloud-based AI platforms drive wider usage across industries. Transformer models are gaining traction, especially for real-time voice and video synthesis, highlighting strong growth potential.

- For insatnce, NVIDIA’s StyleGAN3 can generate hyper-realistic faces and has been used in creative fields for virtual avatars, but it functions more as a research tool and foundational technology rather than a widely adopted, out-of-the-box solution.

By End User

Enterprises accounted for the largest share, holding 49% of the market in 2024. Businesses leverage deepfake tools for marketing, customer engagement, training simulations, and virtual assistants. The surge in demand for synthetic media in advertising and e-learning platforms fuels enterprise adoption. Government agencies are increasingly investing in detection technologies to address national security and cybersecurity risks, marking them as a critical secondary segment.

Key Growth Drivers

Rising Adoption in Entertainment and Marketing

The entertainment and marketing industries are driving deepfake technology adoption with innovative applications. Studios and brands increasingly use synthetic media for personalized content, dubbing, and advertising campaigns, reducing production costs and timelines. Demand for immersive experiences and consumer engagement fuels investment in generation software. Global streaming platforms and gaming companies are exploring AI-based avatars and visual effects, accelerating usage. These factors collectively strengthen the role of deepfake solutions as a mainstream tool in creative industries, ensuring consistent revenue growth across this segment.

- For instance, Metaphysic partnered with Creative Artists Agency (CAA) to provide generative AI and face‑swap tools for talent in film, TV, and branded content, enabling more flexible production workflows.

Increasing Demand for Cybersecurity and Fraud Detection

The rise in digital fraud, misinformation, and identity manipulation is boosting demand for deepfake detection tools. Governments, financial institutions, and enterprises are prioritizing investments in authentication and liveness check software. Solutions that verify digital identities and detect manipulated content are gaining prominence in banking, e-commerce, and regulatory sectors. This growing need to safeguard systems from reputational and financial risks accelerates the adoption of AI-driven monitoring solutions. The increasing reliance on digital services and stricter compliance standards further reinforce the significance of detection technologies.

- For instance, Intel’s FakeCatcher technology, unveiled in 2022, detects deepfakes in real time with 96% accuracy by analyzing subtle blood flow changes in pixels.

Advancements in AI and Computing Infrastructure

Continuous advancements in artificial intelligence, cloud computing, and machine learning frameworks are enhancing deepfake technology. Improved training models, particularly GANs and transformer architectures, are enabling more realistic and faster synthetic content creation. Accessible open-source libraries and scalable cloud platforms reduce barriers to adoption for individuals and small enterprises. High-performance GPUs and AI accelerators provide the computational power required for real-time applications. These advancements not only broaden use cases but also expand opportunities for innovation across industries, strengthening overall market growth.

Key Trends & Opportunities

Expansion of Enterprise Applications

Enterprises are adopting deepfake tools for training, advertising, and customer interaction. Virtual assistants and digital avatars powered by synthetic media improve engagement while lowering operational costs. E-learning platforms are leveraging deepfakes for localized and interactive training material. Opportunities also exist in corporate communication, where AI-driven content enhances brand outreach. With enterprises accounting for nearly half of the market share, demand for enterprise-focused solutions will continue rising, making this segment one of the most lucrative opportunities for vendors.

- For instance, BMW used a hyper-realistic digital avatar in its CES 2023 showcase to present vehicle features through an interactive AI assistant.

Growth of Regulatory and Ethical Frameworks

The rapid spread of deepfakes has prompted governments and global organizations to establish ethical standards and regulatory frameworks. These initiatives create opportunities for companies providing detection, authentication, and compliance solutions. As regulations mandate monitoring tools in sectors like media, finance, and security, adoption of responsible deepfake technologies will accelerate. Vendors that align their offerings with transparency and ethical AI practices will benefit from increasing trust. This regulatory momentum represents a long-term growth opportunity in building safe and accountable ecosystems.

- For instance, Adobe’s Content Authenticity Initiative (CAI), backed by partners like The New York Times and Twitter, is embedding provenance and attribution metadata to ensure transparency in digital media.

Key Challenges

Ethical Concerns and Misuse Risks

The misuse of deepfake technology for spreading misinformation, creating fake identities, or producing malicious content remains a major challenge. Growing concerns around privacy violations, political manipulation, and reputational harm have triggered global debate. The lack of clear ownership rights over synthetic content further complicates the issue. Companies face significant reputational risks if their tools are linked to unethical practices. Addressing these challenges requires strong safeguards, transparent frameworks, and cross-industry collaboration to ensure responsible development and deployment.

High Computational and Resource Requirements

Deepfake creation and detection technologies demand significant computing power, advanced GPUs, and storage capacity. These requirements raise costs for both enterprises and individual users, limiting adoption in resource-constrained regions. Training large AI models consumes vast energy, adding to environmental concerns and operational expenses. Smaller organizations struggle to compete with tech giants that dominate the infrastructure landscape. This challenge slows down scalability and increases entry barriers, requiring innovation in cost-efficient algorithms and optimized computing solutions.

Regulatory Uncertainty and Legal Risks

The absence of globally consistent regulations on deepfake usage and ownership poses risks for technology providers. While some regions enforce strict compliance measures, others lack clear frameworks, creating uncertainty for businesses. This fragmented regulatory environment complicates global expansion and adoption strategies. Companies face potential liabilities if their solutions are misused in jurisdictions with evolving laws. Developing flexible compliance approaches and proactive legal safeguards will be crucial for vendors to sustain growth in a rapidly shifting legal landscape.

Regional Analysis

North America

North America dominated the deepfake technology market with a 37% share in 2024, supported by its advanced AI ecosystem and strong adoption across media, entertainment, and cybersecurity sectors. The U.S. remains the largest contributor, driven by heavy investment from tech giants and government initiatives to combat misinformation. The region’s market size grew from USD 750.83 million in 2018 to USD 1,538.96 million in 2024, and it is expected to reach USD 6,248.73 million by 2032, expanding at a CAGR of 17.9%. Demand for detection and authentication tools continues to rise, ensuring sustained market leadership.

Europe

Europe accounted for a 15% share of the global market in 2024, driven by regulatory focus and adoption in creative industries. Countries such as Germany, the UK, and France are investing in both generation and detection technologies, with strong emphasis on ethical AI practices. The market grew from USD 326.61 million in 2018 to USD 639.81 million in 2024, with projections to reach USD 2,358.05 million by 2032, at a CAGR of 16.4%. Europe’s regulatory push and cultural adoption of AI-generated content make it a critical region for balanced growth.

Asia Pacific

Asia Pacific emerged as the fastest-growing region, holding a 26% share in 2024. Growth is fueled by rapid digital adoption, large user bases in China and India, and investments in AI infrastructure. Media, gaming, and social media applications drive demand, while governments in countries like Japan and South Korea explore deepfake detection for security. The regional market expanded from USD 498.19 million in 2018 to USD 1,089.84 million in 2024, with forecasts of USD 4,814.56 million by 2032, reflecting a CAGR of 19.1%. Strong technology ecosystems ensure Asia Pacific remains the leading growth hub.

Latin America

Latin America captured a 9% share of the global market in 2024, with Brazil and Mexico leading adoption. Entertainment, social media engagement, and political monitoring applications drive market growth. Increasing demand for fraud detection tools also adds momentum. The market expanded from USD 83.79 million in 2018 to USD 171.44 million in 2024, and it is expected to reach USD 616.27 million by 2032, at a CAGR of 16.1%. While adoption is moderate compared to other regions, digital transformation and expanding AI investments position Latin America for steady long-term growth.

Middle East

The Middle East held a 7% share in 2024, with GCC countries and Israel driving adoption. Rising demand for AI-based surveillance, fraud prevention, and media applications supports market growth. Investments in advanced technologies are accelerating regional development, particularly in digital identity verification. The market increased from USD 47.57 million in 2018 to USD 89.90 million in 2024, with expectations to reach USD 305.87 million by 2032, reflecting a CAGR of 15.3%. Strong government support for digital innovation enhances adoption across security and enterprise applications.

Africa

Africa represented the smallest market with a 6% share in 2024, but it shows gradual growth due to rising internet penetration and smartphone adoption. Applications in political monitoring, education, and fraud prevention are emerging as key use cases. The market grew from USD 26.10 million in 2018 to USD 59.88 million in 2024, with projections to reach USD 191.87 million by 2032, at a CAGR of 14.4%. Limited infrastructure and high costs remain challenges, yet rising digital adoption positions Africa as an emerging opportunity for long-term development.

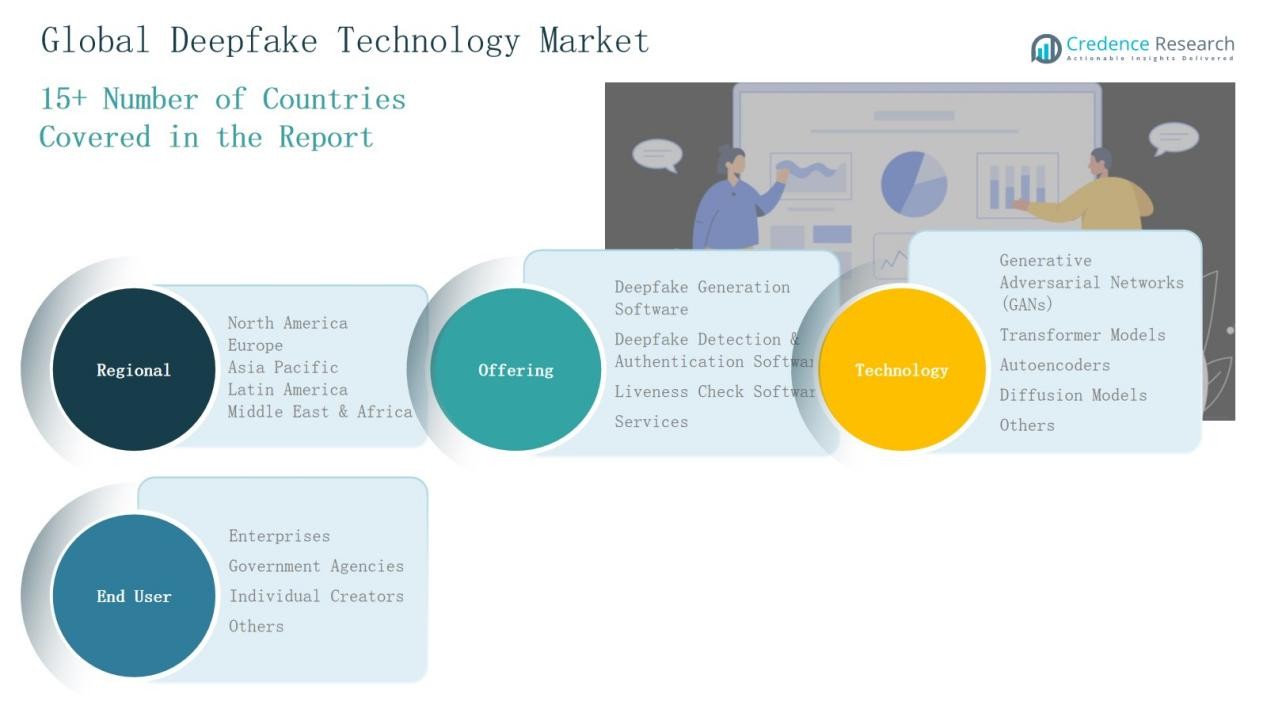

Market Segmentations:

By Offering

- Deepfake Generation Software

- Deepfake Detection & Authentication Software

- Liveness Check Software

- Services

By Technology

- Generative Adversarial Networks (GANs)

- Transformer Models

- Autoencoders

- Diffusion Models

- Others

By End User

- Enterprises

- Government Agencies

- Individual Creators

- Others

By Region

North America

Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

Latin America

- Brazil

- Argentina

- Rest of Latin America

Middle East

- GCC Countries

- Israel

- Turkey

- Rest of Middle East

Africa

- South Africa

- Egypt

- Rest of Africa

Competitive Landscape

The deepfake technology market is moderately consolidated, with global tech giants and specialized startups shaping competition. Leading players such as Microsoft, Google (Alphabet), Meta, and Adobe dominate through advanced AI research, strong financial resources, and integration of deepfake tools into enterprise solutions. Specialized firms like Deeptrace (Sensity AI), Reality Defender, Truepic, and Synthesia focus on niche applications, particularly in detection, authentication, and content generation, offering agile innovation. Companies are actively pursuing strategic partnerships, product launches, and regulatory collaborations to strengthen their market positions. Startups in Asia Pacific, including DeepBrain AI and Zao, are expanding rapidly, leveraging strong regional adoption in social media and entertainment. Competition is further influenced by the dual demand for generation and detection solutions, creating both growth opportunities and reputational risks. Vendors that align with ethical AI practices, regulatory compliance, and enterprise-focused solutions are expected to gain a sustainable edge in this evolving landscape.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Players

- Microsoft

- Google (Alphabet)

- Meta (Facebook)

- Adobe Inc.

- Deeptrace (Sensity AI)

- Reality Defender

- DeepBrain AI

- Zao

- Truepic

- Synthesia

Recent Developments

- In April 2025, Accops partnered with pi-labs to integrate facial authentication with AI-based deepfake detection, strengthening real-time fraud prevention.

- In July 2025, Reality Defender launched a public API and free tier, giving developers enterprise-grade deepfake detection tools.

- In August 2025, Innovatrics launched a new deepfake-detection feature. The tool works via API and pairs with their biometric liveness and injection-attack detection systems.

- In early August 2025, Reality Defender struck a deal with ActiveFence. This allowed ActiveFence clients to detect deepfake video, audio, image, and text content via Reality Defender’s API.

Report Coverage

The research report offers an in-depth analysis based on Offering, Technology, End User and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Enterprises will increasingly adopt deepfake tools for marketing, training, and customer engagement.

- Detection and authentication solutions will see rising demand from governments and financial institutions.

- Advancements in AI models will enhance content realism and reduce generation time.

- Social media platforms will strengthen integration of detection systems to counter misinformation.

- Regulatory frameworks will become stricter, driving adoption of compliance-focused solutions.

- Gaming and entertainment industries will expand use of deepfakes for immersive experiences.

- Voice-based deepfakes will gain traction in virtual assistants and customer service applications.

- Cloud-based platforms will make deepfake tools more accessible to small and mid-sized enterprises.

- Ethical AI practices will play a critical role in building consumer and enterprise trust.

- Regional startups, particularly in Asia Pacific, will emerge as strong innovation drivers.