Market Overview

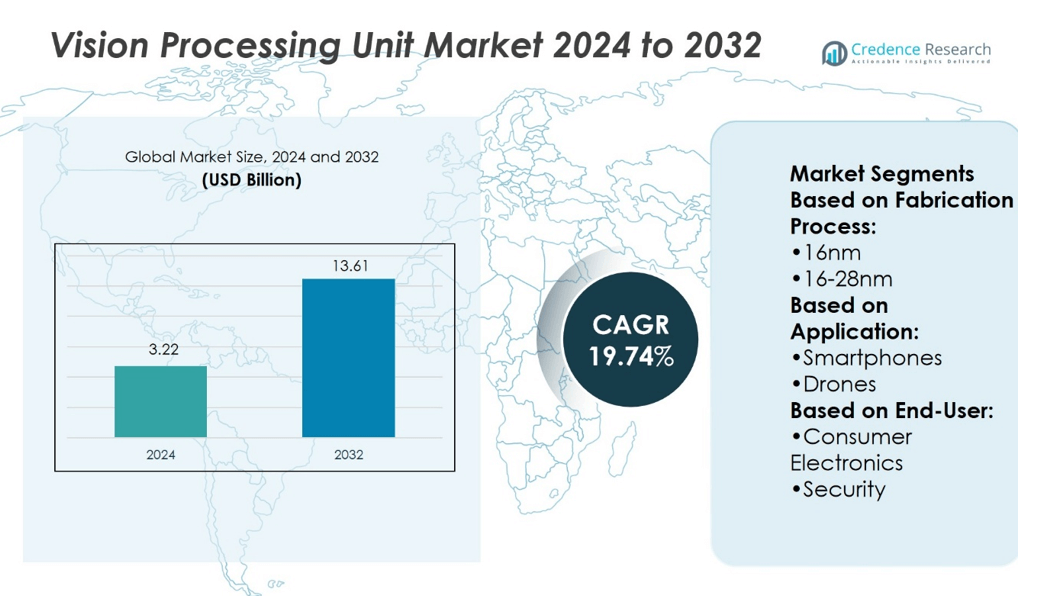

Vision Processing Unit Market size was valued at USD 3.22 billion in 2024 and is anticipated to reach USD 13.61 billion by 2032, at a CAGR of 19.74% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Vision Processing Unit Market Size 2024 |

USD 3.22 billion |

| Vision Processing Unit Market, CAGR |

19.74% |

| Vision Processing Unit Market Size 2032 |

USD 13.61 billion |

The Vision Processing Unit market grows through rising demand for efficient edge AI, autonomous driving, and advanced imaging applications. Increasing use in smartphones, AR/VR, and robotics drives continuous adoption, while integration in ADAS systems strengthens traction in automotive. Expanding smart surveillance and healthcare imaging adds further opportunities. Key trends include a shift toward low-power, high-performance processors, tighter integration with AI frameworks, and wider use of VPUs in edge devices connected to 5G networks. Growing focus on real-time processing, compact chip design, and software ecosystem support continues to shape market direction and future development.

The Vision Processing Unit market shows strong geographical diversity, with North America holding the largest share, followed by Europe and Asia-Pacific, where China, Japan, and South Korea drive rapid growth. Emerging markets in Latin America, the Middle East, and Africa record smaller but expanding adoption through smart-city and surveillance projects. Key players shaping the market include Alphabet, Intel, Huawei, Cadence Design Systems, CEVA, Imagination Technologies, Rockchip Electronics, GEO Semiconductor, Lattice Semiconductor, and Inuitive, each competing through innovation, partnerships, and advanced AI integration.

Market Insights

- Vision Processing Unit Market size was USD 3.22 billion in 2024 and will reach USD 13.61 billion by 2032 at a CAGR of 19.74 %.

- Rising demand for edge AI, autonomous driving, and advanced imaging supports strong market growth.

- Increasing use in smartphones, AR/VR devices, and robotics drives widespread adoption.

- Key players compete on power efficiency, AI integration, and ecosystem support to gain advantage.

- High design complexity and integration costs remain restraints for broader adoption.

- North America leads the market, followed by Europe and Asia-Pacific with rapid growth in China, Japan, and South Korea.

- Latin America, the Middle East, and Africa show smaller but expanding roles through smart-city and surveillance projects.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Adoption in Consumer Electronics and Smart Devices

The Vision Processing Unit Market expands rapidly with growing demand from consumer electronics. Smartphones, tablets, and smart cameras require VPUs to support real-time image enhancement and recognition. It drives faster adoption of advanced features like face unlock, object detection, and augmented reality. Wearable devices also integrate VPUs to deliver energy-efficient visual intelligence. The capability to process high-resolution images with low latency makes VPUs essential in this segment. Companies leverage these processors to meet rising expectations for superior visual performance in daily-use devices.

- For instance, Intel’s Movidius Myriad X VPU integrates a dedicated Neural Compute Engine and 16 SHAVE vector processors. It delivers up to 1 trillion operations per second (1 TOPS) of compute while consuming just 1.5 W of power.

Growing Role in Automotive Safety and Autonomous Driving

Automotive manufacturers adopt VPUs to enable advanced driver-assistance systems and autonomous navigation. The Vision Processing Unit Market gains traction as vehicles integrate lane detection, collision avoidance, and adaptive cruise control. It ensures real-time visual processing while reducing power consumption in embedded systems. VPUs handle complex tasks such as recognizing pedestrians and traffic signs in milliseconds. This capability improves safety and supports the development of self-driving cars. The automotive sector increasingly relies on VPUs to meet strict regulatory and consumer safety requirements.

- For instance, Rockchip’s RK3588 SoC includes a built-in NPU delivering up to 6 TOPS of compute performance and a hardware-based ISP supporting image sensors up to 48 megapixels, enabling rapid, high-resolution perception for automotive vision applications.

Expanding Applications in Industrial Automation and Robotics

Industries integrate VPUs to enhance automation and robotics functions. The Vision Processing Unit Market benefits from demand in predictive maintenance, quality inspection, and warehouse automation. It supports robotic vision systems to identify defects, track components, and guide machines in real-time. Factories achieve higher productivity by using VPUs for consistent visual monitoring across production lines. Robotics manufacturers prefer VPUs for compact size, efficiency, and high processing accuracy. These advantages strengthen adoption across industrial ecosystems seeking to optimize operations and reduce errors.

Accelerating Growth through AI-Driven Healthcare and Security Solutions

Healthcare and security sectors increasingly depend on VPUs to process visual data efficiently. The Vision Processing Unit Market expands as medical imaging, diagnostics, and surveillance systems adopt these processors. It enables detailed analysis of CT scans, MRIs, and endoscopic visuals with reduced latency. Security applications benefit from VPUs through enhanced facial recognition and behavior analysis. Hospitals, clinics, and smart cities deploy such systems to improve outcomes and safety. The ability of VPUs to support AI-driven, real-time decision-making ensures steady demand across critical sectors.

Market Trends

Integration of AI and Deep Learning Capabilities in VPU Architectures

The Vision Processing Unit Market advances with AI and deep learning integration in chip designs. VPUs now support convolutional neural networks to enable real-time object recognition and analysis. It enhances performance in edge devices where fast processing with minimal latency is critical. Manufacturers design VPUs to deliver higher accuracy in facial recognition, gesture control, and predictive analytics. This trend supports the adoption of intelligent devices across multiple industries. Continuous improvements in AI compatibility make VPUs vital for next-generation computing systems.

- For instance, Alphabet’s Google Cloud introduced the TPU v5e in 2023, designed to balance high performance and energy efficiency for large-scale AI training and inference. Each TPU v5e chip delivers up to 393 trillion INT8 operations per second, while a full TPU pod can scale to 100 peta-ops of compute power.

Shift Toward Edge Computing for Real-Time Data Processing

The Vision Processing Unit Market benefits from rising adoption of edge computing solutions. VPUs enable localized data processing that reduces reliance on cloud infrastructure. It provides lower latency, stronger privacy, and improved efficiency in connected devices. Industries such as automotive, healthcare, and retail deploy VPUs to manage visual data directly on-site. This trend aligns with demand for real-time analytics in mission-critical applications. Edge computing integration positions VPUs as key enablers of scalable and secure digital ecosystems.

- For instance, Huawei’s Ascend 310 AI edge processor, part of its Atlas 500 AI Edge Station, delivers a typical performance of 16 TOPS (INT8) and 8 TFLOPS (FP16) while consuming only 8 W of power. It utilizes Huawei’s Da Vinci architecture, integrates AI cores and ARM cores, and is fabricated using TSMC’s 12 nm process.

Miniaturization and Power Efficiency Driving Widespread Adoption

The Vision Processing Unit Market grows through innovations in compact design and power optimization. VPUs now deliver higher performance while consuming fewer watts, making them suitable for portable devices. It ensures sustained battery life in smartphones, drones, and wearables without sacrificing processing speed. Chipmakers invest in advanced fabrication techniques to reduce footprint and improve efficiency. This trend allows seamless integration of VPUs into devices with limited space. Growing focus on power-efficient solutions strengthens adoption across both consumer and industrial markets.

Expansion into Emerging Sectors Including Healthcare, AR/VR, and Smart Cities

The Vision Processing Unit Market expands into new industries that demand visual intelligence. Healthcare providers use VPUs in diagnostic imaging systems for faster and more accurate analysis. It supports AR/VR applications by enabling immersive experiences with low latency. Smart city projects deploy VPUs to power surveillance, traffic management, and public safety solutions. These emerging applications highlight the flexibility of VPUs across different environments. The trend reflects a broader shift toward embedding visual intelligence in every connected ecosystem.

Market Challenges Analysis

High Development Costs and Complex Integration Across Applications

The Vision Processing Unit Market faces challenges due to high development expenses and integration complexity. Designing VPUs with advanced AI, deep learning, and low-power features requires significant investment in R&D. It creates barriers for smaller companies that lack financial strength to compete with established players. Integrating VPUs into diverse applications such as automotive systems, healthcare devices, and smart electronics demands compatibility with varied hardware and software environments. This complexity often increases time-to-market and limits widespread adoption. Companies must balance innovation with affordability to address these challenges effectively.

Heat Management, Performance Limitations, and Market Competition

The Vision Processing Unit Market also struggles with thermal management and performance constraints in compact devices. High processing loads in real-time applications generate heat that affects reliability and long-term operation. It requires advanced cooling solutions, which add to cost and design challenges. VPUs also face strong competition from GPUs and CPUs that continue to evolve with AI capabilities. This competitive pressure often influences customer preference and slows VPU adoption. Overcoming these obstacles requires breakthroughs in material design, fabrication, and strategic partnerships to sustain growth.

Market Opportunities

Expanding Adoption in Autonomous Vehicles and Advanced Driver-Assistance Systems

The Vision Processing Unit Market presents opportunities in autonomous driving and ADAS applications. VPUs enable real-time object detection, lane tracking, and collision prevention with high accuracy. It supports integration of AI algorithms in vehicles while reducing power consumption and latency. Automotive manufacturers increasingly invest in VPUs to meet safety standards and enhance user experience. Growth in electric and self-driving vehicles further drives demand for advanced visual processing solutions. Strategic partnerships between chipmakers and automotive companies strengthen adoption. This trend positions VPUs as critical components in next-generation mobility solutions.

Emerging Applications in Healthcare, Robotics, and Smart Infrastructure

The Vision Processing Unit Market offers opportunities in healthcare diagnostics, industrial robotics, and smart city infrastructure. VPUs facilitate precise medical imaging, predictive maintenance, and intelligent surveillance systems. It enhances operational efficiency by enabling real-time analysis of visual data across multiple sectors. AR/VR adoption in education, entertainment, and training also creates demand for VPUs with low latency and high processing power. Expansion into IoT-enabled smart devices further broadens market potential. Companies that develop scalable, energy-efficient VPUs can capture emerging segments. This trend highlights the versatility of VPUs in addressing diverse industry needs.

Market Segmentation Analysis:

By Fabrication Process

The Vision Processing Unit Market divides into 16nm and 16–28nm fabrication nodes. The 16nm segment leads adoption due to superior power efficiency and faster processing speeds. It supports AI-driven workloads in compact devices where energy conservation is critical. Chipmakers focus on 16nm for high-performance VPUs in premium smartphones and autonomous driving systems. The 16–28nm category continues to find use in cost-sensitive devices where performance requirements are moderate. It enables manufacturers to balance affordability with functionality across mid-range electronics. This segmentation reflects the dual demand for cutting-edge efficiency and mainstream accessibility.

- For instance, Inuitive’s NU4100 vision-on-chip SoC, built on an advanced 12 nm silicon process, integrates the following high-performance components 2 vector cores delivering 350 Giga-OPS, supporting both floating and fixed-point operations.

By Application

Applications diversify the Vision Processing Unit Market across multiple device categories. Smartphones remain the dominant application, using VPUs for facial recognition, computational photography, and AR functions. Drones adopt VPUs for obstacle detection, navigation, and real-time video analytics. It enhances drone efficiency by processing visual data onboard with minimal latency. Cameras integrate VPUs to support advanced autofocus, low-light performance, and smart image recognition. AR/VR systems rely on VPUs to deliver immersive, low-latency experiences critical for gaming and enterprise training. Automotive ADAS and robotics also emerge as high-growth areas due to the need for rapid decision-making and safety compliance.

- For instance, Cadence’s Vision 230 DSP, based on the Xtensa NX architecture, achieves up to 2.18 TOPS—2.6× more than its predecessor, the Vision 130 DSP—making it ideal for SLAM, mobile, drone, automotive, and AR/VR vision tasks.

By End-User

End-user segmentation highlights three major sectors driving adoption. Consumer electronics lead demand with widespread use in smartphones, wearables, and home devices. It enables improved visual intelligence for entertainment and communication. Security and surveillance solutions integrate VPUs for facial recognition, crowd monitoring, and anomaly detection. The need for accurate, real-time data analysis strengthens this segment. Automotive emerges as a key growth driver, leveraging VPUs for autonomous vehicles and advanced safety features. Each end-user segment demonstrates distinct adoption priorities that expand the role of VPUs across industries.

Segments:

Based on Fabrication Process:

Based on Application:

Based on End-User:

- Consumer Electronics

- Security

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share at 37 % of the Vision Processing Unit (VPU) market. The United States leads adoption with strong integration in automotive, healthcare, and consumer electronics. Edge AI, autonomous driving systems, and smart surveillance drive continuous growth. Canada contributes with healthcare imaging and robotics applications. Strong R&D spending and early commercialization of advanced chips secure North America’s leadership.

Europe

Europe represents 29 % share of the market. Germany, France, and the UK are major hubs where automotive and industrial sectors dominate adoption. VPUs power advanced driver-assistance systems, factory automation, and healthcare solutions. The EU’s strict regulations on data privacy and digital security strengthen demand for trusted AI hardware. Collaborative projects between automakers and chipmakers maintain Europe’s strong position.

Asia-Pacific

Asia-Pacific accounts for 24 % share and posts the highest growth rate globally. China, Japan, South Korea, and India lead the region’s expansion. In 2024, China alone contributed 32.4 % of APAC revenue, driven by smartphone production and AI investment. Japan and South Korea are leaders in semiconductor manufacturing and robotics adoption. India grows quickly in surveillance, retail, and healthcare imaging. Strong government support for 5G, AI, and digital infrastructure ensures long-term dominance in growth.

Latin America

Latin America contributes 3.8 % share of the global VPU market. Brazil is the largest market, supported by demand in healthcare, smart retail, and public safety. Argentina, Mexico, and Chile also show rising interest in AI-enabled surveillance and consumer electronics. VPUs help improve facial recognition, automated monitoring, and medical diagnostics in the region. Governments are investing in smart-city and digital transformation projects, which accelerates adoption. Although small today, Latin America shows one of the fastest growth outlooks, with projected CAGR above 20 % through 2033.

Middle East & Africa

The Middle East & Africa together hold 6.2 % share. In the Middle East, the UAE, Saudi Arabia, and Qatar invest heavily in smart-city projects, connected vehicles, and industrial automation. Africa is growing steadily, with South Africa and Nigeria leading adoption in agriculture, logistics, and digital healthcare. Infrastructure challenges remain, but both subregions show high growth rates. Government diversification strategies in the Middle East and digital adoption in African urban centers are key drivers of expansion.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The Vision Processing Unit market players such as Alphabet Inc., Cadence Design Systems Inc., CEVA Inc., Rockchip Electronics Co. Ltd., GEO Semiconductor Inc., Huawei Technologies Co. Ltd., Imagination Technologies Ltd., Intel Corp., Inuitive Ltd., and Lattice Semiconductor Corp. The Vision Processing Unit market shows strong competition shaped by innovation in AI, low-power design, and integration. Companies focus on delivering higher performance per watt, compact form factors, and better software ecosystems to support applications in automotive, consumer electronics, and industrial automation. Advancements in ADAS, AR/VR, robotics, and edge devices push vendors to strengthen partnerships with device makers and system integrators. Competitive differentiation often comes from combining hardware with AI frameworks, offering end-to-end solutions, and ensuring reliable scalability for mass production. Firms that succeed in balancing power efficiency, performance, and adaptability are gaining an edge, while those with strong licensing models or niche technologies continue to expand their presence.

Recent Developments

- In June 2024, Intel Core Ultra processors, featuring advanced Neural Processing Units (NPUs), are revolutionizing HP AI-powered laptops by enhancing speed, efficiency, and AI task handling. These processors optimize performance for tasks like 3D modeling, machine learning, and real-time video enhancements.

- In January 2024, VeriSilicon unveiled its latest VC9800 series Video Processor Unit (VPU) IP with enhanced video processing performance to strengthen its presence in the data center applications. The newly launched series IP caters to the advanced requirements of next-generation data centers including video transcoding servers, AI servers, virtual cloud desktops, and cloud gaming.

- In October 2023, Lenskart, a glasses company, has completed buying Tango Eye. This is a computer vision start-up that uses artificial intelligence (AI). This smart step targets to improve in-store and product reviews by using powerful visual AI time.

- In October 2023, Advantech, A major player in Industrial Internet of Things across the globe, has announced it is buying BitFlow. This American business specializes in high-quality image and AI machine vision technology for computers.

Report Coverage

The research report offers an in-depth analysis based on Fabrication Process, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for VPUs will rise with wider adoption of autonomous vehicles.

- Growth in AR and VR devices will create strong opportunities for VPU integration.

- Edge AI applications will drive need for low-power and efficient vision processors.

- Robotics adoption in manufacturing and logistics will increase VPU deployment.

- Healthcare imaging and diagnostics will rely more on VPU-based solutions.

- Smartphone makers will continue embedding VPUs to enhance camera performance.

- Security and surveillance systems will expand use of vision processing hardware.

- Integration with 5G networks will boost real-time AI processing on devices.

- Partnerships between chipmakers and system integrators will strengthen innovation pipelines.

- Advances in AI software ecosystems will improve efficiency and adoption of VPUs.