Market Overview

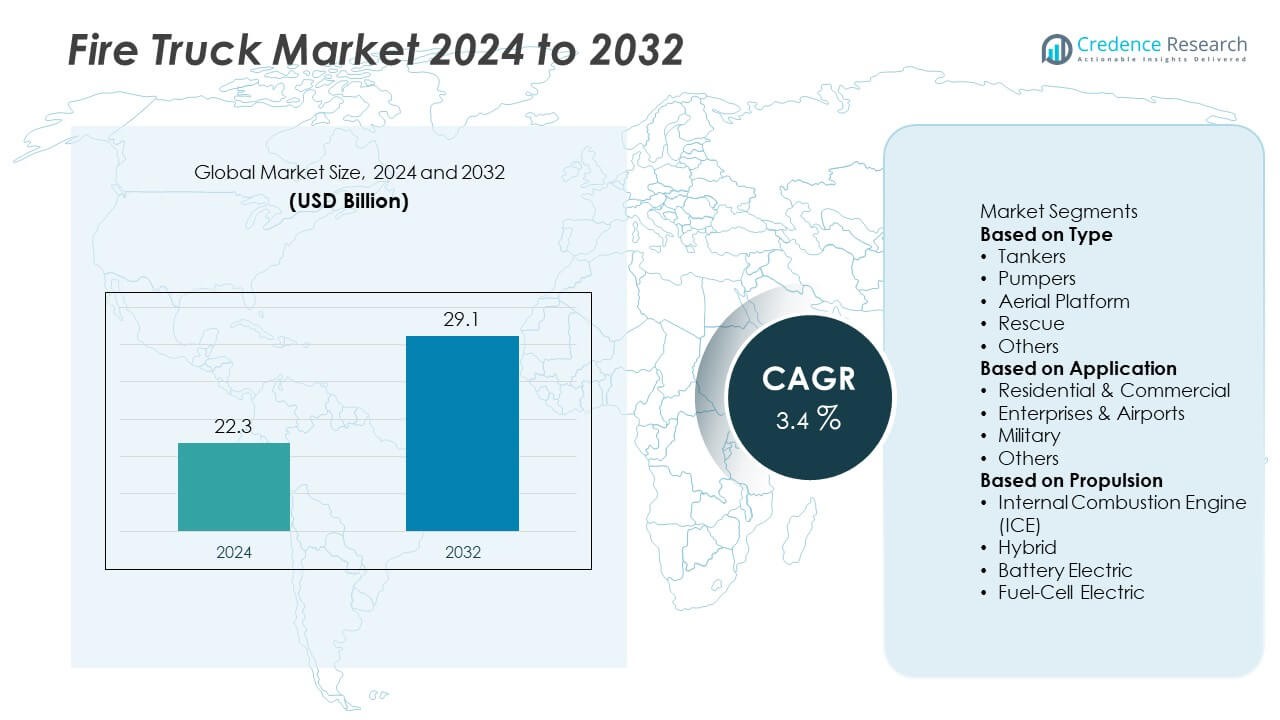

The Fire Truck Market size was valued at USD 22.3 billion in 2024 and is projected to reach USD 29.1 billion by 2032, expanding at a CAGR of 3.4% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Fire Truck Market Size 2024 |

USD 22.3 Billion |

| Fire Truck Market, CAGR |

3.4% |

| Fire Truck Market Size 2032 |

USD 29.1 Billion |

The Fire Truck Market grows steadily with rising urbanization, expanding industrial zones, and stricter fire safety regulations. Municipalities and private sectors invest in modern fleets to improve emergency response and comply with safety standards. It benefits from increasing demand in high-rise construction projects, airports, and petrochemical industries.

The Fire Truck Market demonstrates strong geographical diversity, with Asia-Pacific leading growth through rapid urbanization, large-scale industrial projects, and expanding municipal fleets in China, India, and Southeast Asia. North America maintains steady demand driven by fleet modernization, stringent safety regulations, and early adoption of electric and hybrid fire trucks. Europe emphasizes innovation and sustainability, with countries such as Germany, France, and the United Kingdom focusing on advanced aerial and specialized vehicles to support dense urban environments. Latin America shows gradual expansion supported by industrial growth in Brazil and Mexico, while the Middle East & Africa invest heavily in specialized fire trucks for petrochemical hubs, airports, and urban infrastructure. It benefits from consistent adoption across developed and emerging economies. Key players such as Rosenbauer International AG, Oshkosh Corporation, Magirus GmbH, and Zoomlion strengthen their positions through capacity expansion, technological upgrades, and tailored solutions for regional requirements.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- Fire Truck Market size was valued at USD 22.3 billion in 2024 and is projected to reach USD 29.1 billion by 2032, growing at a CAGR of 3.4%.

- Key drivers include rising urbanization, stricter fire safety regulations, and increasing demand from industrial, municipal, and airport applications.

- Market trends highlight the adoption of electric and hybrid fire trucks, integration of smart technologies, and growing demand for aerial ladder and specialized vehicles.

- Competitive landscape features leading players such as Rosenbauer International AG, Oshkosh Corporation, Magirus GmbH, and Zoomlion, focusing on innovation, product diversification, and regional expansion.

- Restraints include high manufacturing and maintenance costs, supply chain disruptions, and regulatory complexities that increase procurement challenges for municipalities.

- Asia-Pacific leads demand with rapid urbanization, industrial growth, and strong municipal investments, while North America emphasizes modernization of fleets and early adoption of sustainable vehicles.

- Europe focuses on regulatory compliance and advanced technologies, while Latin America and the Middle East & Africa show gradual but rising opportunities through industrial expansion and petrochemical projects.

Market Drivers

Rising Urbanization and Infrastructure Development

The Fire Truck Market grows steadily with rising urbanization and expansion of modern infrastructure. Rapid population growth in metropolitan areas increases demand for advanced firefighting systems. It creates the need for well-equipped fire stations capable of responding quickly to emergencies. High-rise construction projects and industrial zones further drive adoption of specialized fire trucks. Governments invest heavily in safety infrastructure to meet regulatory requirements and safeguard communities. These factors strengthen consistent demand for reliable fire truck fleets worldwide.

- For instance, Rosenbauer International AG received a significant order for 22 Panther 6×6 airport firefighting vehicles from the Spanish airport operator AENA, with delivery completed by the end of 2022. Each vehicle was equipped with tanks holding 10,000 liters of water and 1,200 liters of foam concentrate, and was capable of accelerating from 0 to 80 km/h in less than 31 seconds. The Panther’s unique capabilities are essential for safety at airports, where it is primarily deployed.

Stringent Fire Safety Regulations and Standards

Regulatory authorities play a major role in shaping the Fire Truck Market. Strict safety standards in North America, Europe, and Asia-Pacific require municipalities and private organizations to maintain modern firefighting equipment. It compels fleet upgrades and replacement cycles to ensure compliance with evolving standards. Specialized trucks with improved water capacity, foam systems, and rescue equipment meet diverse safety codes. Increased inspection and enforcement activities accelerate the adoption of advanced models. Compliance pressures remain a significant driver for steady market growth.

- For instance, E-ONE, a subsidiary of REV Group, introduced a version of the Cyclone II pumper, which can be equipped with an optional Hale Qmax-XS pump featuring an NFPA 1901-rated flow rate of up to 8,515 L/min (2,250 GPM) and an optional compressed air foam system (CAFS), in response to customer demand and industry requirements enforced by U.S. fire departments.

Increasing Industrialization and Risk of Fire Hazards

Industrial development and rising fire incidents in manufacturing facilities contribute to the growth of the Fire Truck Market. Industries handling chemicals, oil, and gas require specialized firefighting vehicles equipped with advanced suppression systems. It helps prevent large-scale losses by ensuring rapid response in critical environments. Expansion of warehouses and logistics hubs also adds to the demand for fire trucks. Insurance companies emphasize safety compliance, encouraging businesses to invest in modern fleets. These factors create a strong link between industrial expansion and fire truck adoption.

Technological Advancements and Modernization of Fleets

Innovation in design and technology drives progress in the Fire Truck Market. Manufacturers focus on integrating GPS systems, digital monitoring, and automated water control features. It enhances operational efficiency and response speed during emergencies. Growing interest in electric and hybrid fire trucks addresses environmental concerns and reduces fuel costs. Advanced materials improve durability while reducing vehicle weight. Municipalities and private operators adopt modern fleets to improve safety and reduce long-term operating expenses. This technological evolution ensures the fire truck industry adapts to global safety and sustainability demands.

Market Trends

Adoption of Electric and Hybrid Fire Trucks

The Fire Truck Market shows a growing trend toward electric and hybrid models. Cities and municipalities focus on reducing emissions and fuel costs through clean-energy vehicles. It drives investment in battery technology and charging infrastructure tailored for emergency fleets. Electric fire trucks also offer quieter operation and lower maintenance requirements. Hybrid models provide flexibility in both urban and rural environments. This trend reflects the global shift toward sustainability in heavy-duty vehicles.

- For instance, the Scania hybrid airport fire truck integrates a Scania DC16 V8 engine with 770 hp combined with a 380 hp electric motor, delivering a total of 1,150 hp and utilizing a lithium-ion battery with 104 kWh capacity.

Integration of Smart Technologies and Digital Systems

Smart technologies play an increasing role in shaping the Fire Truck Market. Modern vehicles incorporate GPS navigation, telematics, and real-time communication systems. It improves coordination between teams and accelerates emergency response times. Digital water control and automated pumps enhance accuracy in firefighting operations. Sensors and monitoring systems support predictive maintenance, reducing fleet downtime. Integration of connected technologies ensures fire departments achieve higher operational efficiency.

- For instance, TSI Flowmeters equips fire trucks with electromagnetic flow meters that provide real-time, accurate water usage readings, supporting modern firefighting tactics and system integration, with every unit featuring calibration traceable to an INAB-approved laboratory.

Rising Demand for Aerial and Specialized Fire Trucks

Demand for aerial platforms and specialized fire trucks continues to grow across the Fire Truck Market. High-rise buildings in urban centers require advanced aerial ladder trucks with extended reach. It ensures fire safety in densely populated areas where standard vehicles are insufficient. Chemical plants, airports, and oil refineries invest in customized vehicles with foam and dry chemical systems. Specialized models improve performance in unique environments with high fire risk. Growing infrastructure complexity increases reliance on advanced firefighting equipment.

Focus on Lightweight Materials and Ergonomic Design

The Fire Truck Market experiences a clear trend toward lightweight materials and ergonomic vehicle designs. Manufacturers adopt high-strength composites and advanced alloys to reduce vehicle weight. It improves fuel efficiency and enhances maneuverability in tight urban spaces. Ergonomic cabin designs provide comfort and safety for firefighters during long operations. Modular construction allows easier upgrades and customization. These innovations align with the growing demand for efficient, durable, and user-friendly fire trucks in global markets.

Market Challenges Analysis

High Costs of Manufacturing and Maintenance

Fire Truck Market faces challenges from the high costs associated with manufacturing and fleet maintenance. Specialized equipment, safety systems, and advanced technologies raise the overall production cost of fire trucks. It creates financial pressure for municipalities and developing regions with limited budgets. Maintenance costs also increase due to complex mechanical and electronic systems that require skilled technicians. Smaller fire departments struggle to replace aging fleets because of restricted funding. High acquisition and operating costs limit adoption in cost-sensitive regions, slowing overall market penetration.

Regulatory Barriers and Supply Chain Disruptions

Strict regulations and global supply chain issues also challenge the Fire Truck Market. Regional safety standards differ widely, making it difficult for manufacturers to standardize products across markets. It increases development expenses and delays procurement cycles. Supply chain disruptions, such as shortages of semiconductors and raw materials, affect timely production and delivery of vehicles. Rising costs of steel and advanced components further burden manufacturers. Long lead times create procurement challenges for emergency services that require timely fleet upgrades. These factors continue to pressure both producers and end users in sustaining efficient operations.

Market Opportunities

Growing Demand in Emerging Economies and Urban Areas

The Fire Truck Market presents significant opportunities in emerging economies experiencing rapid urbanization and industrial growth. Expanding metropolitan areas require modern firefighting fleets to manage increasing risks in high-density regions. It benefits from government investments in safety infrastructure and smart city projects. Industrial zones, logistics hubs, and expanding airports in Asia-Pacific, Latin America, and the Middle East fuel demand for specialized trucks. Rising public awareness of fire safety strengthens municipal procurement initiatives. These conditions create a favorable environment for global manufacturers to expand their presence in fast-developing markets.

Innovation in Sustainable and Customized Firefighting Solutions

Technological advancements create strong opportunities for growth in the Fire Truck Market. Manufacturers investing in electric and hybrid fire trucks can meet rising environmental standards and reduce long-term operating costs. It also opens opportunities for adoption in cities aiming for carbon-neutral operations. Demand for customized vehicles, including aerial ladder trucks and chemical fire engines, continues to grow with infrastructure complexity. Integration of digital technologies such as telematics and predictive maintenance systems enhances fleet efficiency. These innovations position manufacturers to secure contracts with municipalities and private organizations seeking modern and sustainable solutions.

Market Segmentation Analysis:

By Type

The Fire Truck Market is segmented by type into pumpers, aerial ladder trucks, rescue trucks, and others. Pumpers dominate demand due to their versatility in municipal firefighting, offering strong pumping capacity for both urban and rural operations. It supports everyday emergencies and remains the most widely deployed vehicle across fire stations. Aerial ladder trucks hold significant demand in metropolitan areas with high-rise buildings, ensuring extended reach and effective firefighting in dense environments. Rescue trucks are increasingly adopted for specialized missions such as disaster relief and hazardous material control. Other categories include wildland trucks and airport crash tenders that address specific regional and industrial needs. Each type reflects the expanding complexity of modern fire and rescue operations.

- For instance, a Rosenbauer 100 Viper aerial ladder truck typically features a 100-foot 4-section ladder, a 300–500 gallon water tank capacity, and a fire pump capable of delivering 1,500 GPM or more. An optional wireless radio remote control is available, which allows an operator to control aerial and outrigger functions from up to 500 feet away.

By Application

Applications of the Fire Truck Market include municipal, industrial, airport, and defense sectors. Municipal applications dominate with widespread demand from cities, towns, and rural communities seeking fleet modernization. It remains critical to support growing urban populations and the increasing incidence of fire hazards. Industrial applications rise with expansion in oil, gas, chemicals, and manufacturing, where specialized trucks equipped with foam systems are required. Airports represent another major application, relying on rapid-response vehicles capable of handling aviation-related emergencies. Defense forces also adopt fire trucks to secure bases, facilities, and military infrastructure. These diverse applications highlight the necessity of customized fire trucks across sectors.

- For instance, Rosenbauer’s Massport Fire-Rescue Truck 1 for Boston-Logan International Airport is a 101-foot Cobra aerial platform, built to serve complex airport emergency requirements.

By Propulsion

The Fire Truck Market is segmented by propulsion into diesel, electric, and hybrid models. Diesel-powered trucks dominate globally due to their reliability, fuel availability, and capacity to support heavy-duty operations. It remains the most widely used option, especially in regions with limited charging infrastructure. Electric fire trucks emerge as a growing segment, driven by sustainability goals and municipal interest in reducing emissions. Hybrid trucks also gain traction, offering operational flexibility by combining traditional engines with battery technology. Early adoption of electric and hybrid propulsion is concentrated in North America and Europe, supported by government incentives and stricter emission policies. This transition reflects a long-term shift toward greener and more efficient firefighting solutions.

Segments:

Based on Type

- Tankers

- Pumpers

- Aerial Platform

- Rescue

- Others

Based on Application

- Residential & Commercial

- Enterprises & Airports

- Military

- Others

Based on Propulsion

- Internal Combustion Engine (ICE)

- Hybrid

- Battery Electric

- Fuel-Cell Electric

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for a 27% share of the Fire Truck Market in 2024, supported by advanced firefighting infrastructure and strong municipal funding. The United States dominates demand, driven by modernization of fleets in urban and suburban fire departments. It benefits from strict safety regulations that require regular fleet upgrades and replacement cycles. Canada also contributes through investments in advanced fire safety vehicles to support industrial and municipal needs. Technological innovation, including early adoption of electric and hybrid fire trucks, strengthens regional leadership. Industrial zones, airports, and defense facilities add to consistent procurement. North America’s focus on safety compliance and sustainability secures its role as a steady growth hub.

Europe

Europe holds a 24% share of the Fire Truck Market, shaped by strict safety standards and emphasis on environmental sustainability. Germany, France, and the United Kingdom lead regional demand, supported by high investments in municipal fleets. It benefits from strong adoption of aerial ladder trucks to meet safety requirements in high-rise urban environments. Scandinavian countries emphasize electric and hybrid models to align with emission reduction policies. Eastern Europe shows growing demand driven by industrial expansion and modernization of outdated fleets. European manufacturers also play a key role in supplying advanced fire trucks globally. The region maintains its competitive edge through innovation, sustainability, and regulatory-driven growth.

Asia-Pacific

Asia-Pacific dominates with a 35% share of the Fire Truck Market, reflecting the largest consumption base worldwide. China leads demand with rapid urbanization, industrial growth, and massive infrastructure projects fueling procurement of advanced fire trucks. India follows with rising municipal investment and growing adoption in industrial zones and airports. It benefits from large populations and government-backed programs that strengthen fire safety infrastructure. Southeast Asian countries including Indonesia, Vietnam, and Thailand contribute to demand with industrialization and expanding urban centers. Japan and South Korea emphasize technological integration and advanced fleet management systems. Asia-Pacific’s dominance is reinforced by rising public awareness of fire safety and strong support for local manufacturing capacity.

Latin America

Latin America represents a 7% share of the Fire Truck Market, supported by gradual urbanization and growing awareness of fire safety. Brazil leads regional demand, with municipalities and industries investing in new fleets to replace aging vehicles. Mexico follows with rising adoption in industrial zones, airports, and urban firefighting systems. It benefits from increasing foreign investments and government programs that emphasize emergency preparedness. Other countries such as Argentina, Chile, and Colombia show steady adoption, supported by infrastructure development and safety reforms. Limited budgets remain a challenge, but international suppliers are expanding presence through partnerships. Latin America remains an emerging but promising market for fire truck manufacturers.

Middle East & Africa

The Middle East & Africa account for a 7% share of the Fire Truck Market, driven by petrochemical hubs, urban development, and rising safety regulations. Saudi Arabia and the United Arab Emirates dominate demand, supported by large-scale industrial projects and growing municipal infrastructure. It benefits from procurement of specialized fire trucks designed for oil, gas, and aviation sectors. Africa shows gradual adoption, with South Africa leading due to industrial expansion and modernization of municipal fleets. Nigeria and Egypt demonstrate rising demand with urban growth and safety reforms. The region also benefits from foreign investments in emergency response systems. Although infrastructure challenges persist, growing economic development and petrochemical projects position the Middle East & Africa as a vital emerging market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Zoomlion

- Oshkosh Corporation

- Weihai Guangtai

- Bronto Skylift Oy Ab

- Rosenbauer International AG

- Spartan Motors

- Magirus GmbH

- Xuzhou Handler Special Vehicle Co. Ltd.

- E-One Inc.

- Danko Emergency Equipment Co.

Competitive Analysis

The competitive landscape of the Fire Truck Market includes Zoomlion, Oshkosh Corporation, Weihai Guangtai, Bronto Skylift Oy Ab, Rosenbauer International AG, Spartan Motors, Magirus GmbH, Xuzhou Handler Special Vehicle Co. Ltd., E-One Inc., and Danko Emergency Equipment Co. These companies compete through advanced product portfolios, global distribution networks, and technological innovation. It is shaped by increasing demand for aerial platforms, rescue trucks, and electric or hybrid fire trucks to meet sustainability goals. Leading players focus on integrating smart systems such as telematics, GPS navigation, and automated water control to enhance operational efficiency. Strong investment in research and development supports development of lightweight materials and ergonomic designs that improve vehicle performance. Regional expansion strategies and partnerships with municipalities, airports, and industrial sectors strengthen their market presence. Companies also prioritize compliance with stringent fire safety regulations, ensuring fleets meet international standards. The Fire Truck Market remains highly competitive, with global leaders balancing innovation, efficiency, and tailored solutions to secure long-term contracts and sustain growth across diverse regions.

Recent Developments

- In August 2025, Zoomlion announced the delivery of its 82.3-meter straight boom aerial work platform (AWP). The ZT82J, the AWP in question, is the world’s tallest of its kind and was delivered to the UK to fill a gap in the global aerial work platform market.

- In July 2025, Zoomlion introduced the DG45 climbing platform fire truck, offering a 45-meter working height, 300 kg bucket load capacity for six people, 35 s deployment time, and an 80 s full extension capability.

- In March 2025, Rosenbauer International AG delivered the first fully electric rescue fire engine (eHLF 20) to the Hamburg Fire Department. The model includes an electric drive, integrated energy backup system, and adjustable height for effective performance in extreme situations.

- In January 2025, Zoomlion also showcased an 80-meter aerial jetting fire truck, receiving the Innovation Product Award from China’s Fire Protection Association.

Report Coverage

The research report offers an in-depth analysis based on Type, Application, Propulsion and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for modern fire trucks will grow with rising urbanization and industrial expansion.

- Municipalities will continue upgrading fleets to comply with stricter fire safety regulations.

- Electric and hybrid fire trucks will gain traction with increasing focus on sustainability.

- Smart technologies such as telematics and automated water systems will enhance efficiency.

- Aerial and specialized fire trucks will see higher demand in high-rise and industrial areas.

- Asia-Pacific will strengthen its position as the fastest-growing regional market.

- North America and Europe will lead adoption of advanced and sustainable fire truck models.

- Latin America will expand gradually with urban growth and industrial development.

- Middle East & Africa will invest in specialized fleets for petrochemical and airport safety.

- Manufacturers will focus on lightweight materials, ergonomic design, and digital integration to stay competitive.