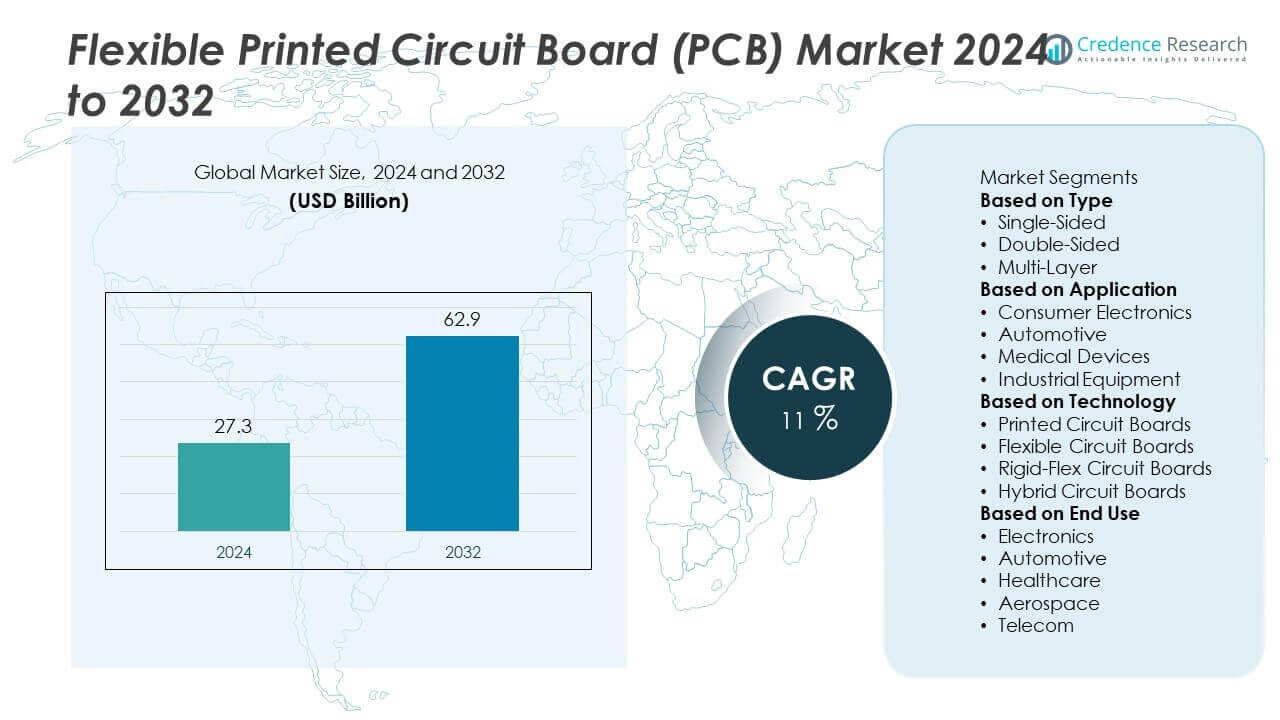

Market Overview

Flexographic Printing Market size was valued at USD 4.2 billion in 2024 and is projected to reach USD 5.7 billion by 2032, growing at a CAGR of 4% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Flexographic Printing Market Size 2024 |

USD 4.2 Billion |

| Flexographic Printing Market, CAGR |

4% |

| Flexographic Printing Market Size 2032 |

USD 5.7 Billion |

The Flexographic Printing Market grows through rising demand for sustainable packaging and advancements in printing efficiency. It benefits from water-based and UV-curable inks that meet regulatory and environmental goals. Automation and digital workflow integration enhance productivity, reduce waste, and support faster turnaround.

The Flexographic Printing Market demonstrates strong geographical presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with each region contributing through unique drivers and opportunities. North America benefits from advanced manufacturing capabilities and strict environmental standards that encourage adoption of eco-friendly inks and substrates. Europe emphasizes innovation and sustainability, with strong demand for premium packaging across cosmetics, luxury goods, and food sectors. Asia-Pacific records rapid growth supported by expanding consumer markets, urbanization, and strong manufacturing bases in China, India, and Japan. Latin America and the Middle East & Africa show steady progress, driven by increasing retail, e-commerce, and packaged food demand. Key players actively shaping the market include Bobst, Amcor PLC, Heidelberger Druckmaschinen AG, and Flint Group, all of which focus on advanced printing technologies, sustainable product offerings, and strategic investments to strengthen global competitiveness in diverse packaging applications.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Flexographic Printing Market was valued at USD 4.2 billion in 2024 and is projected to reach USD 5.7 billion by 2032, at a CAGR of 4%.

- Growth is driven by rising demand for sustainable packaging solutions, with industries preferring water-based and UV-curable inks for reduced emissions and compliance with global regulations.

- Emerging trends include adoption of hybrid printing systems that merge flexographic efficiency with digital customization, alongside automation and digital workflows that reduce waste and enhance productivity.

- Competitive dynamics highlight key players such as Bobst, Amcor PLC, Heidelberger Druckmaschinen AG, and Flint Group, which focus on sustainable inks, innovative equipment, and expanded global presence.

- Market restraints include high initial investment costs for modern printing presses, ongoing maintenance expenses, and growing competition from digital printing technologies that offer greater flexibility for short runs.

- Regional growth varies, with North America and Europe leading through strong technological adoption and sustainability focus, while Asia-Pacific shows rapid expansion due to rising packaged goods demand and e-commerce growth.

- Overall, the market demonstrates resilience by adapting to regulatory pressures, evolving consumer expectations, and continuous innovation in printing methods, securing its relevance across global packaging industries.

Market Drivers

Rising Demand for Sustainable Packaging Solutions

The Flexographic Printing Market grows steadily due to rising demand for eco-friendly packaging. Brand owners prefer recyclable materials that align with sustainability goals. Flexography supports water-based inks and low-VOC solutions, which help reduce environmental impact. It enables printing on biodegradable films and papers without losing quality. The market benefits from consumer preference for greener choices across food, beverage, and personal care packaging. Regulations supporting reduced carbon footprint strengthen adoption across industries.

- For instance, Bobst launched its Vision CI flexo press in 2019, which operates at speeds up to 400 meters per minute while enabling the use of water-based inks to reduce VOC emissions.

Advancements in Printing Technology and Efficiency

Technology advancements drive growth by improving efficiency, speed, and precision in flexographic printing. New presses integrate automation features, reducing setup times and minimizing material waste. Innovations in plate-making techniques allow sharper images and consistent quality across large runs. It provides a cost-effective solution for both short and long production cycles. The ability to handle complex designs increases demand from premium product packaging. Integration of digital workflows ensures faster turnaround and streamlined operations.

- For instance, Heidelberger Druckmaschinen AG introduced its Boardmaster flexo press in May 2023, achieving production speeds up to 600 meters per minute with 90% press availability in continuous packaging runs.

Expanding Applications Across End-Use Industries

The market benefits from wide adoption across packaging segments, including food, beverages, pharmaceuticals, and cosmetics. Flexographic printing suits both flexible and rigid packaging substrates, making it versatile for diverse applications. It offers adaptability for corrugated boxes, folding cartons, and flexible pouches. The growing e-commerce sector fuels demand for printed corrugated materials with high-quality graphics. Product differentiation and branding needs push businesses to adopt advanced print solutions. This broad end-user reliance reinforces steady market expansion.

Cost-Effectiveness and High Production Volumes

Flexographic printing provides strong value through cost-effectiveness in high-volume production. It allows efficient use of inks and materials, lowering per-unit costs. Quick drying inks support faster processing and higher production speeds. The technology is suitable for both simple and complex designs, making it attractive to manufacturers. It reduces downtime through easy plate changes and long print runs. These advantages make flexographic printing a preferred choice for large-scale packaging producers.

Market Trends

Adoption of Sustainable Printing Inks and Substrates

The Flexographic Printing Market records a strong trend toward sustainable materials and eco-friendly inks. Companies introduce water-based and UV-curable inks that reduce emissions. It supports printing on recyclable and compostable substrates without sacrificing quality. The shift aligns with regulatory mandates focused on lowering environmental impact. Packaging industries favor solutions that meet consumer preference for sustainable choices. This trend strengthens demand across food, retail, and healthcare packaging sectors.

- For instance, Siegwerk has publicly stated that its UniNATURE ink incorporates up to 50% renewable carbon content. This renewable content can be up to nine times more than standard water-based inks.

Integration of Automation and Digital Workflow Solutions

Automation emerges as a key trend, reducing downtime and enhancing operational efficiency. Modern flexographic presses integrate digital workflow systems for seamless pre-press and production management. It enables faster job setup, accurate color matching, and reduced material waste. Automated plate handling and inspection tools further improve consistency in large print runs. These features help producers manage tight deadlines and diverse packaging requirements. The trend reflects strong demand for efficient, smart manufacturing practices.

- For instance, The Windmöller & Hölscher NOVOFLEX II press can reach maximum speeds of 800 m/min, and is compatible with the VISION inspection system, which is designed for high-resolution 100% defect detection.

Growing Use of Hybrid Printing Technologies

Hybrid printing that combines flexography with digital solutions gains traction. It offers the efficiency of flexo for long runs with the customization benefits of digital. It allows high-resolution graphics and variable data printing on the same line. This trend appeals to brand owners seeking personalized packaging with quick turnaround. The capability to balance cost and design flexibility supports broader adoption. Hybrid systems strengthen competitiveness in markets where customization drives value.

Focus on High-Quality Graphics and Premium Packaging

Flexographic printing advances in delivering sharper images and vibrant colors. High-definition plate technology and improved ink formulations enhance final print quality. It supports premium packaging that attracts consumer attention in retail environments. Demand rises for packaging that reflects brand identity through intricate designs and fine details. Growing competition among consumer goods brands fuels this emphasis on visual appeal. The trend highlights flexographic printing’s role in premium and mass-market packaging alike.

Market Challenges Analysis

High Initial Investment and Maintenance Costs

The Flexographic Printing Market faces challenges due to significant capital requirements for modern press installations. Advanced machines demand heavy investment, which restricts adoption among small and mid-scale printers. It requires regular maintenance and skilled operators to ensure consistent performance. High costs related to plate making, upgrades, and automation integration add financial pressure. These expenses limit flexibility for companies with tight budgets. The challenge slows expansion in regions where price sensitivity is high.

Competition from Digital Printing Alternatives

Digital printing technologies create strong competition by offering greater flexibility for short runs and personalization. Many brand owners shift toward digital platforms for customized packaging solutions. It challenges flexography’s dominance in certain applications where quick turnaround and design changes matter. Digital systems require lower setup time, which appeals to businesses with frequent product launches. Advancements in inkjet and electrophotography intensify this competition. The trend forces flexographic printing providers to innovate and enhance cost efficiency.

Market Opportunities

Rising Demand for Flexible and Sustainable Packaging

The Flexographic Printing Market holds strong opportunities in the growing shift toward flexible packaging. Food, beverage, and personal care sectors prefer pouches, wraps, and cartons with high-quality graphics. It supports printing on biodegradable and recyclable substrates, aligning with global sustainability goals. Regulations encouraging eco-friendly materials further strengthen demand for flexographic solutions. Expanding e-commerce trade increases the need for durable and printed corrugated packaging. This trend creates consistent opportunities for producers offering versatile and sustainable print solutions.

Adoption of Hybrid and Smart Printing Technologies

Hybrid systems that combine flexographic and digital technologies present untapped growth potential. It enables cost-efficient large runs while delivering customization and variable data printing. Brand owners see value in combining high-volume efficiency with personalized design features. Rising adoption of automation and IoT-enabled presses creates opportunities for streamlined operations. Investments in advanced plate-making technologies enhance quality and reduce waste. These developments position flexographic printing as a competitive solution for future packaging demands.

Market Segmentation Analysis:

By Offering

The Flexographic Printing Market segments by offering into equipment, consumables, and services. Equipment forms the largest share, supported by demand for advanced presses with automation and high-speed features. It ensures efficiency and precision for both short and long production cycles. Consumables, including printing plates, sleeves, and doctor blades, record steady growth due to repeat purchases. Services such as installation, maintenance, and training provide consistent support, helping operators optimize performance. The combined demand across offerings reinforces market stability and long-term adoption.

- For instance, Mar-Co Harbor Group upgraded to a BOBST VISION CI flexo press. Their press speed increased from 400 ft/min to 1,400 ft/min, while job setup time per color dropped from one hour to just minutes

By Ink Type

Segmentation by ink type highlights water-based, solvent-based, UV-curable, and others. Water-based inks dominate due to compliance with environmental regulations and low VOC emissions. It provides excellent adhesion on paper and corrugated substrates, making it suitable for food and beverage packaging. Solvent-based inks maintain relevance in flexible packaging where strong adhesion and durability are essential. UV-curable inks grow quickly with their fast-drying properties and ability to deliver vibrant colors. Other specialty inks, such as metallic and fluorescent, serve niche packaging needs, adding value to premium products.

- For instance, a test print using a Flint Group ink system on a SOMA CI flexo press ran at 400 m/min and used Expanded Gamut Printing (CMYBGV plus opaque white), demonstrating high stability and effectiveness for high-speed, high-definition work

By Method

The market segments by method into roll-to-roll, sheet-fed, and others. Roll-to-roll printing leads adoption due to its suitability for high-volume production and continuous operations. It supports printing on flexible films, labels, and corrugated materials with strong efficiency. Sheet-fed presses hold demand in applications requiring precision and shorter print runs. It caters to folding cartons, tags, and specialty packaging where flexibility is critical. Other emerging methods integrate hybrid processes, combining flexographic and digital advantages for broader functionality. This diverse segmentation reflects the adaptability of flexographic printing across industries.

Segments:

Based on Offering

- Flexographic printing machine

- Flexographic printing ink

Based on Ink Type

- Water-based inks

- Solvent-based inks

- Energy-curable inks

Based on Method

- Inline-type press

- Central impression press

- Stack-type press

Based on Application

- Corrugated packaging

- Flexible packaging

- Cartons

- Others

Based on End Use

- Food & beverage

- Healthcare

- Others

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Flexographic Printing Market at 32% in 2024. The region benefits from strong adoption across food, beverage, and pharmaceutical packaging industries. Demand for sustainable packaging drives investments in water-based inks and recyclable substrates. It is further supported by regulatory policies that emphasize low-VOC and eco-friendly solutions. The United States dominates the regional market due to advanced manufacturing infrastructure and the presence of global packaging leaders. Canada follows with steady demand from e-commerce and retail packaging sectors. The region’s focus on automation and digital integration enhances efficiency, ensuring continued leadership in the market.

Europe

Europe accounts for 28% of the global market share in 2024. Stringent environmental regulations, including REACH and the EU Packaging Directive, encourage adoption of eco-friendly inks and substrates. The market benefits from growing demand for premium packaging in industries such as cosmetics, personal care, and luxury goods. It shows high adoption of UV-curable inks and hybrid printing solutions to meet design and customization needs. Germany, the United Kingdom, and France lead the region with strong investments in sustainable packaging technologies. Eastern Europe records rising adoption as local manufacturers upgrade to modern printing presses. The region’s emphasis on sustainability and innovation positions it as a critical growth hub.

Asia-Pacific

Asia-Pacific captures 25% of the market share, reflecting rapid industrial growth and expansion of consumer markets. Rising disposable incomes and urbanization increase demand for packaged goods across food, beverage, and healthcare sectors. It benefits from strong manufacturing bases in China, India, and Japan, where both equipment and consumables record high demand. E-commerce growth further fuels packaging needs, particularly in corrugated and flexible packaging. Local players focus on affordable printing solutions, while global companies invest in advanced press installations. The region shows high potential for UV-curable and solvent-based inks, catering to diverse packaging formats. Asia-Pacific is expected to outpace other regions in growth during the forecast period.

Latin America

Latin America holds 9% of the global market share in 2024. The region shows growing adoption of flexographic printing in food and beverage packaging, driven by expanding retail chains and rising consumer demand. It faces challenges from limited infrastructure but benefits from cost-effective roll-to-roll printing applications. Brazil and Mexico dominate the regional landscape with strong packaging exports and increasing industrial capacity. It also gains traction in pharmaceutical labeling and corrugated packaging for logistics. Despite economic constraints, demand for sustainable inks and modern equipment creates opportunities for long-term growth. The region demonstrates steady expansion as multinational companies invest in localized production facilities.

Middle East & Africa

The Middle East & Africa represent the smallest share, at 6% in 2024. The region records rising demand for packaged food and consumer goods, supporting adoption of flexographic printing. It benefits from growing e-commerce activities, particularly in the Gulf countries, where retail packaging standards are evolving. South Africa and the United Arab Emirates lead regional adoption, supported by investments in advanced equipment. It faces challenges from high equipment costs and limited skilled labor but gradually shifts toward eco-friendly solutions. Government initiatives promoting industrial diversification support market expansion. The region continues to emerge as a growth opportunity, particularly for consumables and sustainable ink solutions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Heidelberger Druckmaschinen AG

- Komori Corporation

- Amcor PLC

- Codimag

- Bobst

- Koenig & Bauer AG

- Comexi

- Gallus

- Allstein GmbH

- Flint Group

Competitive Analysis

The competitive landscape of the Flexographic Printing Market features leading players such as Bobst, Amcor PLC, Heidelberger Druckmaschinen AG, Flint Group, Komori Corporation, Gallus, Koenig & Bauer AG, Allstein GmbH, Codimag, and Comexi. These companies focus on advanced flexographic solutions that integrate automation, hybrid capabilities, and sustainable printing technologies. They emphasize the development of eco-friendly inks, recyclable substrates, and digital workflow integration to meet rising global demand for efficiency and sustainability. Strategic collaborations, product launches, and expansion into emerging markets strengthen their market positions. Many invest in R&D to enhance press speed, print quality, and cost efficiency while addressing customization needs. Their presence across diverse geographies enables strong supply networks and customer outreach. Competition remains intense, with players differentiating through technological innovation, end-to-end service offerings, and adaptation to regulatory standards. Together, these strategies reinforce their leadership roles and ensure sustained competitiveness in the evolving flexographic printing industry.

Recent Developments

- In June 2025, Heidelberger Druckmaschinen AG (Heidelberg) Opened “Home of Print,” the largest customer demo center, and added a new VLF press in packaging.

- In May 2025, Komori Chambon Displayed at China Print 2025, showcasing packaging and flexo-enabled hybrid solutions.

- In Jan 2025, Komori Chambon acquired Canadian Primoflex Systems (flexo tech), rebranding it as Komori Primoflex Systems.

- In September 2024, Heidelberger Druckmaschinen AG (Heidelberg) Launched partnership with Solenis to enable barrier coatings via Heidelberg flexo portfolio.

Report Coverage

The research report offers an in-depth analysis based on Offering, Ink Type, Method, Application, End Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with rising demand for sustainable and recyclable packaging solutions.

- Hybrid printing that combines flexographic and digital methods will gain wider adoption.

- Automation and AI-driven workflows will improve efficiency and reduce production errors.

- Premium packaging with high-definition graphics will strengthen demand across consumer goods.

- E-commerce growth will fuel higher use of printed corrugated and flexible packaging.

- Water-based and UV-curable inks will dominate due to regulatory compliance and eco-friendly focus.

- Emerging markets in Asia-Pacific and Latin America will show faster adoption of flexographic solutions.

- Investments in advanced plate-making technologies will enhance print quality and minimize waste.

- Competition from digital printing will push flexographic players to innovate and lower costs.

- Strategic partnerships and acquisitions will shape industry consolidation and global expansion.