Market Overview

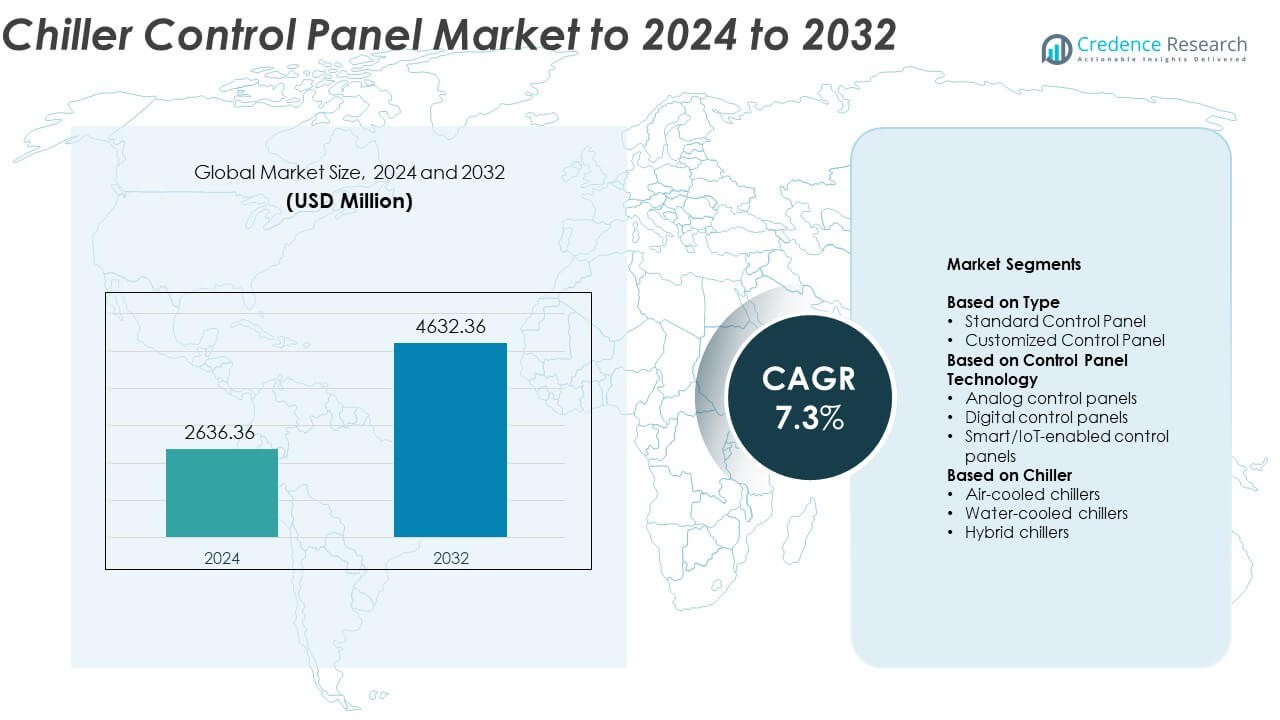

The Chiller Control Panel market size was valued at USD 2636.36 million in 2024 and is anticipated to reach USD 4632.36 million by 2032, at a CAGR of 7.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Chiller Control Panel Market Size 2024 |

USD 2636.36 Million |

| Chiller Control Panel Market, CAGR |

7.3% |

| Chiller Control Panel Market Size 2032 |

USD 4632.36 Million |

The chiller control panel market features prominent players such as Daikin Industries Ltd., Siemens AG, Trane Technologies plc, Johnson Controls International plc, Honeywell International Inc., and Schneider Electric SE. These companies lead through innovation in smart, energy-efficient, and IoT-enabled control solutions designed for precise system performance and sustainability. North America dominates the market with around 37% share in 2024, driven by advanced infrastructure and widespread adoption of automated HVAC systems. Europe follows with nearly 29% share, supported by stringent energy efficiency standards and retrofitting initiatives, while Asia Pacific emerges as the fastest-growing region with about 25% share, fueled by rapid industrialization and smart building expansion.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The chiller control panel market was valued at USD 2636.36 million in 2024 and is projected to reach USD 4632.36 million by 2032, growing at a CAGR of 7.3%.

• Rising demand for energy-efficient HVAC systems and smart automation technologies is driving market growth across industrial, commercial, and institutional sectors.

• Integration of IoT-enabled and digital control panels is a key trend, improving operational efficiency, predictive maintenance, and remote system management.

• The market is moderately consolidated, with global players focusing on digital innovation, modular designs, and strategic partnerships to expand their regional presence.

• North America leads with a 37% share, followed by Europe with 29%, and Asia Pacific with 25%, while the customized control panel segment holds about 57% share in 2024, reflecting growing adoption of tailored and high-performance chiller control solutions.

Market Segmentation Analysis:

By Type

The customized control panel segment dominates the chiller control panel market with about 57% share in 2024. This leadership is due to its flexibility in meeting varied operational requirements across large-scale commercial and industrial setups. Customized panels allow integration with specific chiller configurations and automation systems, improving energy management and control accuracy. The growing trend of tailored HVAC solutions and demand for intelligent system design across smart buildings and green infrastructure projects continue to drive the segment’s expansion.

- For instance, Johnson Controls released a major update to its Metasys Building Automation System (BAS) in September 2024, Metasys 14.0, which added new next-generation analytics tools and preconfigured energy dashboards.

By Control Panel Technology

The digital control panels segment leads the market, accounting for roughly 49% share in 2024. Their dominance is driven by precise temperature regulation, easy configuration, and compatibility with automated chiller systems. Digital control panels enhance system performance through real-time data tracking and adaptive controls. The rising shift from analog to microprocessor-based solutions, combined with predictive maintenance and touchscreen functionality, strengthens digital panel adoption in commercial and industrial environments.

- For instance, Danfoss reports adaptive case control delivering energy savings of up to 33% versus basic TXV systems through real-time digital control.

By Chiller

Air-cooled chillers hold the largest market share of nearly 52% in 2024. Their dominance is supported by lower maintenance requirements, compact design, and suitability for regions with limited water resources. These systems are increasingly preferred for data centers, offices, and manufacturing plants due to quick installation and stable operation. The demand for energy-efficient air-cooled chillers integrated with advanced control panels for optimized load management and performance monitoring continues to accelerate their market growth.

Key Growth Drivers

Rising Demand for Energy-Efficient HVAC Systems

The growing adoption of energy-efficient HVAC systems is a primary driver of the chiller control panel market. Organizations are focusing on reducing energy consumption and carbon emissions, which boosts the integration of intelligent control systems. Advanced chiller control panels allow precise monitoring of cooling loads and optimize compressor operation, resulting in lower operational costs. The increasing emphasis on green building certifications and energy management standards further accelerates demand for high-performance, automated control solutions across industrial and commercial sectors.

- For instance, Siemens’ Cooling Plant Optimization cut chiller-plant energy by 3,753,617 kWh in one year, a 22% reduction.

Integration of Smart and IoT-Enabled Technologies

The expansion of IoT-enabled chiller control panels significantly drives market growth. Smart control systems enhance operational transparency, enabling real-time monitoring and predictive maintenance. These systems improve reliability and reduce downtime through data-driven decision-making. The growing shift toward digitalization in building automation and industrial processes promotes the adoption of connected control systems. As businesses prioritize remote operation and performance analytics, the integration of IoT platforms continues to strengthen chiller system efficiency and lifecycle management.

- For instance, Johnson Controls’ OpenBlue study found up to 67% reduction in chiller maintenance and up to 10% energy savings with smart building analytics.

Rapid Growth in Data Centers and Commercial Infrastructure

The increasing number of data centers and large-scale commercial buildings worldwide contributes to market expansion. Data centers require precise temperature management to maintain equipment performance and uptime, which drives demand for advanced control panels. The rising investment in IT infrastructure and cloud services further boosts installations of efficient chiller systems. Additionally, urbanization and the construction of energy-optimized office complexes, hospitals, and retail spaces support steady growth for intelligent and scalable chiller control solutions.

Key Trends & Opportunities

Advancement in Automation and Cloud-Based Control

Automation and cloud integration are emerging as major trends in the chiller control panel market. Cloud-based systems allow centralized monitoring and remote adjustments, providing higher efficiency and control flexibility. Automation also facilitates demand-based cooling, minimizing energy wastage. With manufacturers incorporating machine learning algorithms and advanced analytics, end-users benefit from real-time diagnostics and system optimization. The growing deployment of smart building ecosystems offers a significant opportunity for scalable, cloud-connected chiller control systems.

- For instance, Honeywell’s SMARTenergy OPS® optimization at Rocky Mount cut chiller-plant energy use by 25% and delivered a 39% operating improvement from optimized sequencing.

Focus on Modular and Retrofit Solutions

The market is witnessing a shift toward modular and retrofit-compatible control panels. Many end-users are upgrading legacy systems to meet modern performance and sustainability standards without replacing entire chillers. Modular designs simplify installation and maintenance while offering scalability for future capacity expansion. This trend is particularly strong in the commercial and industrial segments, where efficiency upgrades and lifecycle cost reduction remain top priorities. The growing focus on retrofit projects presents a lucrative opportunity for manufacturers worldwide.

- For instance, Trane’s integrated high-performance plant for a Beijing data center reduced equipment space by 1/3rd while improving efficiency and cutting power consumption.

Key Challenges

High Initial Cost and Integration Complexity

The high upfront cost of advanced control panels and integration with existing HVAC infrastructure pose challenges for small and medium enterprises. Smart and IoT-enabled panels require specialized installation and calibration, increasing total system cost. Additionally, integration across multiple legacy systems can be technically complex, often demanding skilled professionals. These cost and compatibility issues hinder wider adoption, especially in developing markets with limited digital infrastructure investment.

Cybersecurity Risks in Connected Systems

The growing use of IoT and cloud-based control systems raises cybersecurity concerns in the chiller control panel market. Unauthorized access or data breaches can disrupt operations and compromise sensitive industrial information. As connected systems handle real-time operational data, ensuring secure communication networks and strong encryption protocols becomes crucial. Manufacturers and operators face increasing pressure to implement robust cybersecurity frameworks, compliance measures, and regular system updates to safeguard against evolving cyber threats.

Regional Analysis

North America

North America leads the chiller control panel market with about 37% share in 2024. The region’s growth is driven by the strong presence of data centers, healthcare facilities, and commercial complexes that demand efficient HVAC automation. The United States dominates the regional landscape due to high adoption of smart and IoT-enabled control systems. Stringent energy efficiency regulations, such as ASHRAE standards, and increasing investments in sustainable building infrastructure continue to boost demand. Canada’s expansion in cold storage and manufacturing facilities further supports steady market development across the region.

Europe

Europe accounts for nearly 29% share of the global chiller control panel market in 2024. The region’s growth is fueled by strong emphasis on environmental sustainability and energy optimization across industrial and commercial applications. Countries such as Germany, the United Kingdom, and France are leading adopters of digital and smart HVAC solutions. The implementation of strict energy performance directives and retrofit programs in existing buildings drives new installations. Growing focus on reducing carbon emissions and integrating renewable-powered chillers also strengthens Europe’s position in the market.

Asia Pacific

Asia Pacific holds around 25% share of the global chiller control panel market in 2024, emerging as one of the fastest-growing regions. Rapid industrialization, urbanization, and large-scale commercial construction projects in China, India, and Japan are key drivers. Expanding data center networks and manufacturing facilities are increasing the demand for precise temperature management systems. Governments in the region are promoting energy-efficient infrastructure and smart city projects, further accelerating adoption. Rising investments from HVAC manufacturers and local production capabilities enhance market competitiveness and accessibility across the region.

Latin America

Latin America represents approximately 6% share of the chiller control panel market in 2024. Growth in the region is supported by the expansion of commercial construction, retail infrastructure, and hospitality sectors. Brazil and Mexico are leading markets due to increasing adoption of energy-efficient HVAC systems in urban areas. The growing presence of global chiller manufacturers and supportive government energy policies are also contributing to market penetration. However, high equipment costs and limited availability of advanced automation technologies slightly restrain faster adoption rates.

Middle East & Africa

The Middle East and Africa account for about 3% share of the global chiller control panel market in 2024. The region’s growth is primarily driven by rising infrastructure projects and the expansion of commercial facilities in the Gulf countries. The increasing need for efficient cooling systems in high-temperature environments, particularly in Saudi Arabia and the United Arab Emirates, supports market demand. Investments in sustainable construction and smart building technologies are fostering adoption of intelligent chiller control solutions. However, lower awareness and slower technology diffusion restrain broader market penetration.

Market Segmentations:

By Type

- Standard Control Panel

- Customized Control Panel

By Control Panel Technology

- Analog control panels

- Digital control panels

- Smart/IoT-enabled control panels

By Chiller

- Air-cooled chillers

- Water-cooled chillers

- Hybrid chillers

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The chiller control panel market is highly competitive, with leading companies such as Daikin Industries Ltd., Siemens AG, Carel Industries S.p.A., Trane Technologies plc, Honeywell International Inc., Delta Electronics Inc., Johnson Controls International plc, Danfoss A/S, Ingersoll Rand Inc., Mitsubishi Electric Corporation, Emerson Electric Co., Carrier Global Corporation, Lennox International Inc., Chillitron Controls Pvt. Ltd., and Schneider Electric SE driving innovation and market consolidation. The competitive landscape is defined by continuous advancements in energy-efficient technologies, IoT integration, and intelligent control solutions. Companies are focusing on enhancing automation, connectivity, and predictive maintenance features to improve operational reliability. Strategic collaborations, product differentiation, and investment in digital platforms are strengthening their market positions. The rising demand for modular, retrofit, and smart control systems across industrial and commercial sectors is prompting firms to expand manufacturing capabilities and service networks. Increasing focus on sustainability and regulatory compliance continues to shape competition in the global market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Daikin Industries Ltd.

- Siemens AG

- Carel Industries S.p.A.

- Trane Technologies plc

- Honeywell International Inc.

- Delta Electronics, Inc.

- Johnson Controls International plc

- Danfoss A/S

- Ingersoll Rand Inc.

- Mitsubishi Electric Corporation

- Emerson Electric Co.

- Carrier Global Corporation

- Lennox International Inc.

- Chillitron Controls Pvt. Ltd.

- Schneider Electric SE

Recent Developments

- In May 2024, Carrier India introduced the 30RB Air-Cooled Modular Scroll Chiller, which includes integrated control systems

- In 2024, Daikin Industries Ltd. Announced the Smart Control System (SCS) for hydronic HVAC plants including chillers, launching availability in January 2025.

- In 2024, Danfoss A/S Launched the Alsmart programmable controller portfolio tailored for HVAC systems, featuring modular hardware, advanced cybersecurity, and extensive protocol support to enhance energy efficiency and operational flexibility.

Report Coverage

The research report offers an in-depth analysis based on Type, Control Panel Technology, Chiller and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Growing adoption of IoT-enabled control panels will improve efficiency and predictive maintenance.

- Rising data center construction will continue to drive demand for precise temperature control systems.

- Increasing focus on energy optimization will promote integration of AI-driven control algorithms.

- Modular and retrofit panel designs will gain traction for system upgrades and cost savings.

- Expansion of green buildings will boost demand for low-energy and smart HVAC solutions.

- Government incentives for sustainable infrastructure will accelerate digital control panel installations.

- Emerging economies will witness faster adoption of automated chiller systems in industrial sectors.

- Manufacturers will focus on cybersecurity solutions to protect connected control systems.

- Remote monitoring and cloud connectivity will become standard in commercial chiller systems.

- Partnerships between HVAC manufacturers and technology providers will shape future innovation and service models.