Adeno-Associated Virus (AAV) CDMO Market Overview:

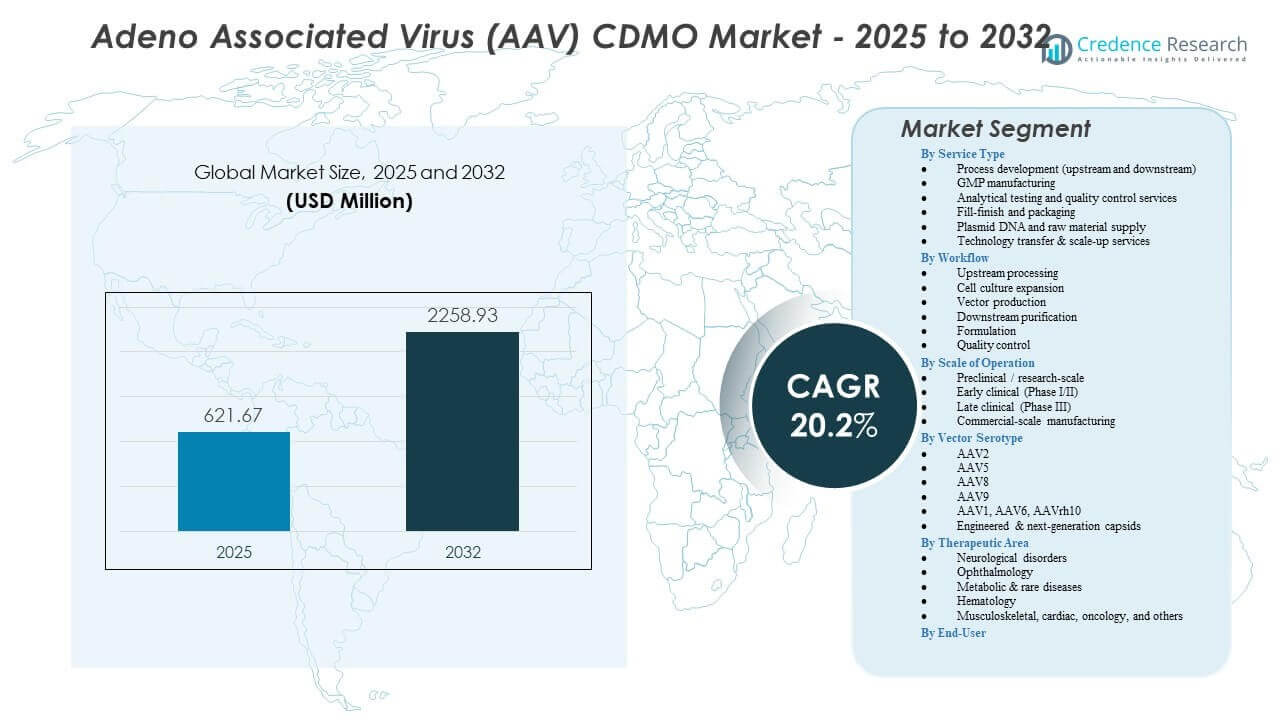

The Adeno Associated Virus (AAV) CDMO Market is projected to grow from USD 621.67 million in 2025 to an estimated USD 2,258.93 million by 2032, with a compound annual growth rate (CAGR) of 20.2% from 2025 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Adeno-Associated Virus (AAV) CDMO Market Size 2025 |

USD 621.67 million |

| Adeno-Associated Virus (AAV) CDMO Market, CAGR |

20.2% |

| Adeno-Associated Virus (AAV) CDMO Market Size 2032 |

USD 2,258.93 million |

Adeno-Associated Virus (AAV) CDMO Market Insights:

- Strong market drivers include expanding gene therapy pipelines, rising demand for scalable AAV vector production, and increasing dependence on CDMOs for process development, GMP manufacturing, and analytical services.

- Market restraints include limited global manufacturing capacity, high production complexity, and regulatory pressures that require advanced quality systems and skilled technical expertise.

- North America leads the market due to well-established infrastructure and a high concentration of clinical programs, while Europe maintains a strong position through advanced R&D ecosystems and robust regulatory frameworks.

- Asia Pacific emerges as the fastest-growing region, strengthened by rapid facility expansion, improving technical capabilities, and government-backed efforts to build competitive viral vector manufacturing hubs.

Adeno-Associated Virus (AAV) CDMO Market Drivers

Strong Growth of Gene Therapy Pipelines Driving CDMO Dependency

Rising investment in gene therapy programs strengthens outsourcing needs across early and late development stages. The Adeno Associated Virus (AAV) CDMO Market gains momentum because developers seek partners with scalable cGMP expertise. Rapid expansion of rare disease research encourages sponsors to secure reliable manufacturing slots. High vector demand pushes CDMOs to upgrade upstream and downstream systems. Sponsors value strong regulatory support and proven quality systems. Many companies choose external partners to reduce operational risks. Rapid shifts in clinical timelines keep capacity utilization high. Each driver supports stable growth patterns.

- For instance, Forge Biologics expanded its Columbus facility to 200,000 sq. ft. with a 50L–5,000L AAV production range, supporting over 40 active gene therapy programs.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Advancements in AAV Vector Engineering Increasing Project Complexity

Emerging vector engineering methods require experienced CDMO teams that manage complex design and production cycles. Developers explore capsid optimization and promoter refinement to improve therapeutic outcomes. These strategies raise the need for integrated analytical support. The market gains traction when sponsors depend on CDMOs to validate process steps. High genetic modification complexity raises demand for controlled workflows. Many programs need specialized potency and purity assays. CDMOs expand teams to support rising technical needs. High specialization improves the value of outsourcing partnerships. This trend improves overall process control.

Shift Toward Large-Scale Manufacturing Platforms Supporting Commercialization

Growing interest in commercial-scale therapies encourages CDMOs to invest in high-volume bioreactors. Many programs move from small clinical batches to larger production cycles. Rising capacity needs push companies to shift toward platform processes. The shift helps improve reproducibility and accelerate timelines. The market benefits when sponsors avoid delays linked to limited in-house capability. Large-scale systems support stable vector yields. CDMOs implement automation to maintain high batch success. Sponsors choose partners with cross-site redundancy. The shift shapes long-term production models.

Rising Regulatory Pressure Encouraging Outsourcing of Quality-Control Activities

Strict regulatory expectations push sponsors to partner with CDMOs that maintain advanced analytical suites. The Adeno Associated Virus (AAV) CDMO Market grows when developers outsource tests that ensure purity, potency, and safety. Many companies avoid internal investment in high-cost equipment. CDMOs with deep regulatory experience help reduce compliance gaps. High documentation requirements push demand for expert-driven support. Many clients rely on standardized quality templates. Developers seek partners that manage audits with strong consistency. Analytical capacity growth improves confidence. Each factor strengthens outsourcing decisions.

- For instance, Lonza’s Portsmouth, New Hampshire site provides GMP-certified analytical release testing for viral vectors, supported by regulatory-compliant QC platforms that are routinely audited by U.S. and European authorities, as documented in Lonza’s regulatory quality disclosures.

Adeno-Associated Virus (AAV) CDMO Market Trends

Growth of Modular and Flexible Manufacturing Facilities to Support Rapid Scale Needs

CDMOs adopt modular facilities that support fast setup and scale transitions. Many sites deploy single-use systems to reduce downtime between batches. Flexible layouts allow quicker project onboarding. The Adeno Associated Virus (AAV) CDMO Market benefits when sponsors secure rapid access to capacity. Modular plants help maintain predictable scheduling. Many developers select partners with adaptive footprints. Rapid technology turnover raises interest in flexible suites. This trend reshapes expansion strategies in the sector. Market readiness improves across regions.

Increased Use of Digital Tools and Automation for Process Optimization

Automation improves vector yield consistency and reduces manual errors across production workflows. AI and machine learning support predictive adjustments in upstream and downstream operations. Many CDMOs integrate digital twins to refine process parameters. Sponsors value data-rich environments that improve oversight. Strong digital adoption strengthens project reliability. The market becomes more competitive when CDMOs deploy automated batch-release systems. Advanced control systems support stronger decision-making. These tools help stabilize timelines. Each trend supports operational efficiency.

- For instance, Lonza adopted its MODA®-ES electronic batch record system across global viral vector and cell therapy facilities, enabling automated data capture and real-time QC documentation, a capability publicly detailed in Lonza’s digital transformation and Informatics platform announcements.

Growing Demand for Specialized Fill-Finish Capabilities for Viral Vector Products

CDMOs expand fill-finish lines that support high-precision handling of sensitive vectors. Many projects require low-volume formats tailored for clinical dosing. Demand rises as complex gene therapy products enter late-stage trials. The Adeno Associated Virus (AAV) CDMO Market gains traction when CDMOs offer integrated sterile operations. Strict aseptic needs influence facility design. Many companies depend on advanced inspection systems. Specialized equipment reduces contamination risks. Late-stage programs improve outsourcing volume. This trend strengthens downstream specialization.

- For instance, Catalent’s Harmans, Maryland campus includes multiple commercial-scale viral vector suites and cGMP fill–finish capabilities, supported by 10 manufacturing suites that operate single-use bioreactors up to 2,000 liters, as publicly confirmed in Catalent’s facility disclosures.

Rise of Strategic Long-Term CDMO Partnerships to Secure Manufacturing Capacity

Sponsors establish multi-year agreements to ensure uninterrupted access to production slots. High demand levels push developers to lock capacity early. Many CDMOs prefer long-term partnerships that support resource planning. Clear collaboration models reduce project uncertainty. The market grows when supply chains stabilize under structured commitments. Companies gain stronger visibility into development timelines. Many sponsors prefer integrated services that reduce transfer risks. Long-term relationships improve global expansion strategies. This trend shapes competitive positioning across the sector.

Adeno-Associated Virus (AAV) CDMO Market Challenges Analysis

Capacity Limitations and High Production Costs Creating Bottlenecks

Limited capacity at major CDMOs slows the expansion of gene therapy programs. Many sites struggle to meet high demand linked to growing pipelines. The Adeno Associated Virus (AAV) CDMO Market faces pressure to shorten wait times for clinical and commercial slots. High production costs reduce accessibility for small developers. Many companies find it difficult to secure consistent process yields. Complex analytical requirements increase operational burdens. CDMOs manage strict regulatory controls that raise compliance expenses. Cost-heavy purification steps add further constraints. Each challenge affects project continuity.

Complex Regulatory Requirements and Process Variability Creating Operational Risk

Stringent documentation and validation rules make AAV production challenging for developers. Many programs fail to maintain stable critical quality attributes. High variability across cell lines and workflows increases uncertainty. CDMOs must manage frequent regulatory updates across regions. Many sponsors depend on partners to navigate process qualifications. Technical complexities increase audit intensity. Limited global standardization creates confusion for new entrants. These conditions raise development risks. Operational oversight becomes essential for sustained growth.

Adeno-Associated Virus (AAV) CDMO Market Opportunities

Expansion of Commercial Gene Therapies Creating Long-Term Production Potential

Growing approval rates for gene therapies open strong prospects for scaling commercial output. Many developers shift from clinical to commercial needs across multiple pipelines. The Adeno Associated Virus (AAV) CDMO Market can gain from rising interest in full-scale supply chains. Demand grows for stable manufacturing agreements that support global distribution. Many companies need turnkey solutions from vector design to fill-finish. CDMOs with integrated models gain competitive strength. Strong commercialization momentum attracts new clients. This opportunity reinforces steady revenue planning.

Growing Investments in Emerging Markets Supporting New Facility Development

Rapid expansion of biotech ecosystems strengthens opportunities in Asia Pacific, Latin America, and the Middle East. Many governments support biomanufacturing through funding programs and facility incentives. CDMOs explore regional footprints to reach global clients. Many sponsors seek lower-cost environments without losing quality. Developers benefit from rising talent pools within emerging clusters. Strong infrastructure upgrades improve operational readiness. Investment momentum helps reduce geographic concentration. These regions create new outsourcing pathways that broaden market growth.

Adeno-Associated Virus (AAV) CDMO Market Segmentation Analysis:

By Service Type

Service offerings define capability strength in the Adeno Associated Virus (AAV) CDMO Market, with process development supporting optimization of upstream and downstream operations. GMP manufacturing drives the highest demand because sponsors prioritize reliability and regulatory alignment. Analytical testing and quality control services reinforce product safety, while fill-finish and packaging ensure sterile delivery formats. Plasmid DNA supply supports vector production workflows and removes sourcing constraints. Technology transfer and scale-up services help streamline movement from small batches to commercial runs. Each service type supports program continuity. The segment holds strong relevance across clinical pipelines.

By Workflow

Workflow segmentation highlights technical maturity within the Adeno Associated Virus (AAV) CDMO Market, where upstream processing and cell culture expansion shape vector yield potential. Vector production remains central due to high demand for scalable systems. Downstream purification improves product purity and consistency. Formulation stabilizes vector integrity across storage and transport. Quality control validates every batch before release. Each workflow step influences production timelines. The workflow structure supports process reliability for clients.

By Scale of Operation

Scale segmentation reflects the path from research to commercialization within the Adeno Associated Virus (AAV) CDMO Market. Preclinical and early clinical programs create strong demand for flexible capacity. Late clinical stages require higher volumes and stronger compliance documentation. Commercial-scale manufacturing depends on long-term agreements and validated processes. Each stage shapes resource planning. Sponsors rely on CDMOs to reduce development risks. The segment highlights the shift toward larger batch needs.

By Vector Serotype

Serotype selection influences project design within the Adeno Associated Virus (AAV) CDMO Market. AAV2, AAV5, AAV8, and AAV9 remain widely used due to strong safety profiles. Serotypes such as AAV1, AAV6, and AAVrh10 support targeted delivery. Engineered capsids enable improved tissue specificity and reduced immunogenicity. Each serotype requires tailored production and analytical workflows. Developers choose variants based on therapeutic goals. The segment supports ongoing innovation in gene therapy.

- For instance, Aldevron publicly reports GMP production of multiple AAV serotypes, including AAV2, AAV5, AAV8, and AAV9, supported by validated plasmid manufacturing platforms used across global clinical programs.

By Therapeutic Area

Therapeutic demand guides production priorities within the Adeno Associated Virus (AAV) CDMO Market. Neurological disorders dominate due to strong research investment. Ophthalmology benefits from established clinical success. Metabolic and rare diseases continue to expand pipeline activity. Hematology programs require precise vector engineering. Musculoskeletal, cardiac, oncology, and other areas expand usage diversity. Each therapeutic field relies on strong vector quality. The segment supports broad application growth.

By End-User

End-user segmentation reflects the client landscape within the Adeno Associated Virus (AAV) CDMO Market. Biopharmaceutical companies drive the largest share due to strong clinical pipelines. Academic institutes support early discovery work and technology innovation. CROs provide project management and trial support. Non-profits and government laboratories contribute to foundational research. Each end-user group depends on external manufacturing expertise. The segment strengthens outsourcing trends across the sector.

- For instance, WuXi Advanced Therapies supports more than 100 global biopharma and academic clients with integrated viral vector development and GMP manufacturing services, as documented in its annual operational reports.

Segmentation:

By Service Type

- Process development (upstream and downstream)

- GMP manufacturing

- Analytical testing and quality control services

- Fill-finish and packaging

- Plasmid DNA and raw material supply

- Technology transfer & scale-up services

By Workflow

- Upstream processing

- Cell culture expansion

- Vector production

- Downstream purification

- Formulation

- Quality control

By Scale of Operation

- Preclinical / research-scale

- Early clinical (Phase I/II)

- Late clinical (Phase III)

- Commercial-scale manufacturing

By Vector Serotype

- AAV2

- AAV5

- AAV8

- AAV9

- AAV1, AAV6, AAVrh10

- Engineered & next-generation capsids

By Therapeutic Area

- Neurological disorders

- Ophthalmology

- Metabolic & rare diseases

- Hematology

- Musculoskeletal, cardiac, oncology, and others

By End-User

- Biopharmaceutical and biotechnology companies

- Academic and research institutes

- Contract research organizations (CROs)

- Non-profits, foundations, and government laboratories

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds the largest share of the Adeno Associated Virus (AAV) CDMO Market, accounting for nearly 45% of global activity. Strong biotech funding, mature CDMO networks, and consistent regulatory alignment help maintain regional leadership. The region benefits from concentration of commercial gene therapy programs that depend on high-capacity vector manufacturing. Many sponsors secure long-term contracts to protect supply continuity. The Adeno Associated Virus (AAV) CDMO Market gains steady demand from U.S. and Canadian innovators. It continues to expand footprint across clinical and commercial pipelines. Regional strength remains stable across the forecast period.

Europe captures around 30% of the global market and maintains a broad presence across clinical development hubs. Strong academic-industry partnerships drive vector demand, and regulatory frameworks reinforce quality expectations. Many facilities across Western Europe hold advanced GMP capabilities that attract multinational sponsors. Growing investment in gene therapy clusters supports steady project flow. The region gains momentum from cross-border collaborations. It benefits from rising interest in scaled manufacturing. Europe continues to strengthen its technical standing in viral vector production.

Asia Pacific holds nearly 20% of the market and ranks as the fastest-growing region due to expanding biomanufacturing infrastructure. Many countries invest in large-scale facilities to support domestic gene therapy pipelines and international outsourcing demand. Regional CDMOs gain traction by offering competitive turnaround times and lower operational costs. Governments support capacity building to accelerate technology adoption. The Adeno Associated Virus (AAV) CDMO Market grows quickly in China, South Korea, and Singapore. It attracts global clients looking for scalable production networks. The region is emerging as a strong alternative supply base.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

Competitive Analysis:

The competitive landscape of the Adeno Associated Virus (AAV) CDMO Market reflects a mix of established global manufacturers and specialized vector-focused providers. Large CDMOs maintain strong advantage through integrated service platforms that cover development, GMP manufacturing, analytical testing, and fill-finish operations. Smaller specialist firms compete by offering advanced capsid engineering, rapid process development, and flexible project structures. Competitive pressure increases as new facilities expand capacity across key regions. The Adeno Associated Virus (AAV) CDMO Market also sees rising interest in long-term capacity reservation agreements that secure production slots for late-stage programs. Many providers invest in automation and digital quality systems to reduce batch variability. Competition focuses on technical depth, regulatory performance, and scalability. It continues to intensify as global demand for clinical and commercial AAV programs grows.

Recent Developments:

- In August 2025, Avista Therapeutics partnered with Forge Biologics for AAV process development, cGMP manufacturing, and analytical services to advance AVST-101 gene therapy for X-linked retinoschisis (XLRS), leveraging Forge’s proprietary FUEL™ platform at its Ohio facility.

- In May 2024, Catalent entered a strategic partnership with Siren Biotechnology to support the development and cGMP manufacturing of AAV vector-based immuno-gene therapies for clinical trials at its Baltimore, MD facility.

Report Coverage:

The research report offers an in-depth analysis based on Service Type, Workflow, Scale of Operation, Vector Serotype, Therapeutic Area, End-User, and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for outsourced vector manufacturing will strengthen as more gene therapy programs move toward late-stage development within the Adeno Associated Virus (AAV) CDMO Market.

- CDMOs will expand automated upstream and downstream systems to improve batch reliability and shorten project cycles.

- Growing interest in engineered capsids will increase investment in advanced analytical and characterization capabilities.

- Expansion of commercial-scale capacity will support broader therapy launches and long-term supply agreements.

- Global regulatory alignment will drive higher compliance expectations and reinforce the importance of quality-focused CDMOs.

- Partnerships between biotech firms and CDMOs will deepen to secure production continuity for pipeline growth.

- Asia Pacific will rise as a competitive outsourcing hub due to rapid facility expansion and strong technology adoption.

- Integrated CDMO platforms will gain preference as sponsors seek end-to-end development and manufacturing solutions.

- Demand for plasmid DNA and raw material support will increase, strengthening upstream supply chains.

- Digital tools and AI-driven optimization will reshape production design and enhance process control across all stages.