Market Overview:

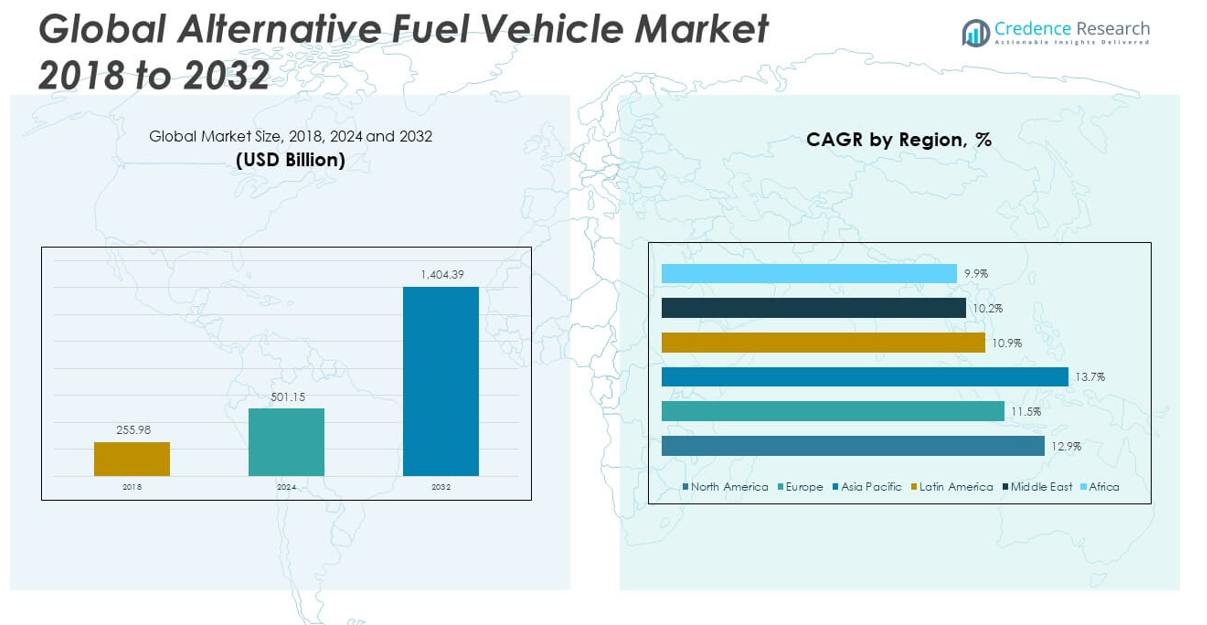

The Global Alternative Fuel Vehicle Market size was valued at USD 255.98 million in 2018 to USD 501.15 million in 2024 and is anticipated to reach USD 1,404.39 million by 2032, at a CAGR of 12.81% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Alternative Fuel Vehicle Market Size 2024 |

USD 501.15 million |

| Alternative Fuel Vehicle Market, CAGR |

12.81% |

| Alternative Fuel Vehicle Market Size 2032 |

USD 1,404.39 million |

Several factors are propelling the growth of the AFV market. Firstly, escalating environmental concerns and stringent emission regulations are compelling governments and consumers to seek alternatives to traditional internal combustion engine vehicles. Policies such as tax incentives, subsidies, and zero-emission mandates are accelerating the adoption of electric vehicles (EVs), hybrid electric vehicles (HEVs), plug-in hybrid electric vehicles (PHEVs), and hydrogen fuel cell vehicles. Secondly, advancements in battery technology and charging infrastructure are enhancing the performance and convenience of EVs, making them more appealing to consumers. Additionally, the rising cost of fossil fuels and the desire for energy independence are driving the demand for alternative fuels like compressed natural gas (CNG), biofuels, and hydrogen. Collectively, these factors are fostering a conducive environment for the proliferation of AFVs globally.

Regionally, the AFV market exhibits diverse dynamics influenced by local policies, infrastructure, and consumer preferences. In 2023, the Asia Pacific region dominated the global market primarily driven by China’s aggressive EV policies, substantial investments in charging infrastructure, and a burgeoning domestic EV manufacturing sector. Europe follows closely, with countries like Germany, France, and the UK implementing stringent emission standards and offering substantial incentives for EV adoption. The United States is also witnessing significant growth, bolstered by federal and state-level policies promoting EVs and the expansion of charging networks. Emerging markets in Latin America and the Middle East are gradually increasing their share in the AFV market, supported by government initiatives aimed at reducing carbon footprints and diversifying energy sources.

Market Insights:

- The Global Alternative Fuel Vehicle Market is projected to reach USD 1,404.39 million by 2032, growing at a CAGR of 12.81% during the forecast period, driven by rising demand for sustainable transportation options.

- Environmental Concerns and stringent emission regulations are pushing governments and businesses toward electric vehicles (EVs), hydrogen fuel cell vehicles, and hybrids, accelerating market growth globally.

- Technological advancements in battery and fuel cell technology, particularly lithium-ion and solid-state batteries, are enhancing the performance, range, and efficiency of EVs, making them more accessible to consumers.

- Government incentives and policies, such as tax rebates and zero-emission mandates, are encouraging the adoption of alternative fuel vehicles, particularly in markets like the U.S., China, and Europe.

- Rising fuel prices and the desire for energy independence are driving consumers and businesses toward alternative fuels like CNG, biofuels, and hydrogen, presenting cost-effective solutions compared to traditional fuels.

- High initial costs of alternative fuel vehicles, particularly EVs, remain a challenge, though subsidies and advancements in technology are gradually making them more affordable.

- Insufficient charging and refueling infrastructure continues to be a significant barrier, particularly in emerging markets, limiting the widespread adoption of EVs and hydrogen vehicles in regions with less-developed infrastructure.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Growing Environmental Concerns and Stringent Emission Regulations

Environmental sustainability remains a key driver in the growth of the Global Alternative Fuel Vehicle Market. Increasing concerns over air pollution, climate change, and the depletion of natural resources are prompting governments and businesses to transition from conventional fuel-powered vehicles to alternatives. With the automotive industry being a significant contributor to greenhouse gas emissions, policies are being implemented worldwide to reduce carbon footprints. The introduction of stringent emission standards such as Euro 6 in Europe, and the Clean Air Act in the United States, compels automakers to adopt cleaner technologies. These regulations push for the development and widespread adoption of electric vehicles (EVs), hydrogen-powered vehicles, and hybrids. Automakers face substantial penalties for non-compliance, which further accelerates the shift towards alternative fuel vehicles. The drive for cleaner air and energy security fuels the rapid growth of the alternative fuel vehicle market.

- For example, the Euro 6/VI vehicle emission standards require up to a 99% reduction in fine particulate matter (PM2.5) emissionscompared to earlier standards, achieved through a combination of diesel particulate filters (DPF), selective catalytic reduction (SCR) systems with zeolite catalysts, and advanced onboard diagnostics (OBD) for real-time emissions monitoring.

Technological Advancements in Battery and Fuel Cell Technology

Technological innovations in battery and fuel cell technology are accelerating the adoption of alternative fuel vehicles globally. Battery advancements, particularly in lithium-ion and solid-state batteries, significantly enhance the range and efficiency of EVs. With continuous improvements in charging infrastructure and faster charging technologies, consumer concerns regarding the practicality of electric vehicles are gradually diminishing. In parallel, hydrogen fuel cell vehicles are benefiting from improved fuel cell technology that offers higher energy density and shorter refueling times compared to traditional battery systems. The increasing efficiency of these technologies is driving down production costs, making alternative fuel vehicles more affordable for consumers. As technology continues to improve, the market for alternative fuel vehicles will expand, offering viable alternatives to traditional vehicles.

Government Incentives and Policies Promoting Clean Transportation

Government policies and incentives are crucial drivers for the Global Alternative Fuel Vehicle Market. In many regions, governments provide tax credits, rebates, and grants to encourage the purchase of alternative fuel vehicles. These policies aim to reduce dependence on fossil fuels, lower carbon emissions, and improve air quality. For example, in countries like the United States, China, and several European nations, subsidies and tax breaks for electric vehicle buyers make alternative fuel vehicles more attractive. These incentives, coupled with growing infrastructure for charging and refueling stations, create a favorable environment for consumers to make the transition to cleaner vehicle options. The active role of governments in setting ambitious targets for reducing emissions also drives market demand by pushing for a higher percentage of alternative fuel vehicles on the road.

- For example, in the United States, the federal government provides up to $7,500 in income tax creditsfor all-electric, plug-in hybrid, and fuel cell vehicles

Rising Fuel Prices and Energy Independence

The rising cost of conventional fuels like gasoline and diesel is contributing to the growth of the Global Alternative Fuel Vehicle Market. As global energy markets fluctuate and oil prices increase, consumers and businesses are seeking alternative options to mitigate their dependency on fossil fuels. AFVs, particularly electric vehicles, provide an economical alternative by offering lower fuel and maintenance costs over their lifespan. In addition, alternative fuels like natural gas, biofuels, and hydrogen present viable options to diversify energy sources and reduce reliance on oil imports. With energy security becoming a central issue for many nations, the push for alternative fuel vehicles is also driven by the desire for greater control over energy production and consumption. These factors contribute to the market’s expansion, as both individual consumers and businesses shift towards more sustainable and cost-effective transportation solutions.

Market Trends:

Shift Towards Electric and Hybrid Vehicles in the Global Market

The Global Alternative Fuel Vehicle Market is witnessing a marked shift towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) as the demand for zero-emission transportation continues to rise. Consumers and businesses alike are increasingly prioritizing eco-friendly and cost-efficient transportation options. EVs are gaining popularity due to advancements in battery technology that extend their range and reduce charging times. Simultaneously, hybrid vehicles, which combine conventional combustion engines with electric motors, are seeing strong growth, offering consumers the benefits of both fuel efficiency and reduced environmental impact. This shift is being driven by technological innovations and improvements in charging infrastructure, which make it easier for consumers to adopt these vehicles on a large scale. The ongoing development of both vehicle types indicates a promising future for clean energy transportation solutions.

Integration of Autonomous Technology with Alternative Fuel Vehicles

The integration of autonomous driving technology into the Global Alternative Fuel Vehicle Market is gaining traction, contributing to the evolution of modern vehicles. Automakers are increasingly focusing on developing self-driving electric vehicles that not only reduce the carbon footprint but also enhance driving safety and efficiency. Autonomous systems, when paired with alternative fuels, offer the potential for more efficient energy usage, reduced road congestion, and improved traffic flow. This integration can also lead to a significant reduction in accidents caused by human error. The market for autonomous electric and hybrid vehicles is projected to grow as further advancements in artificial intelligence, sensors, and machine learning increase the reliability and safety of these vehicles, making them an attractive option for both consumers and fleet operators.

- For example, at CES 2025, Aptera Motors unveiled a production-ready solar electric vehicle (sEV) equipped with self-driving features and a carbon fiber composite body, claiming up to 400 miles of range per chargeand up to 40 miles of daily solar-powered driving a direct result of integrating lightweight materials, solar technology, and autonomous systems

Expansion of Charging and Refueling Infrastructure Globally

The growth of alternative fuel vehicles heavily depends on the expansion of charging and refueling infrastructure, which is a growing trend within the Global Alternative Fuel Vehicle Market. As governments and private sectors invest in developing widespread, accessible charging networks, consumers become more confident in adopting EVs and other alternative fuel vehicles. Key markets, including Europe, North America, and Asia Pacific, are seeing increased investment in electric vehicle charging stations, hydrogen refueling stations, and compressed natural gas (CNG) outlets. The availability of fast-charging options and well-distributed refueling networks ensures that consumers can rely on alternative fuel vehicles for long-distance travel and daily commuting, contributing to the overall market growth.

Emerging Focus on Sustainable and Green Mobility Solutions

A growing emphasis on sustainability and green mobility solutions is shaping the trends within the Global Alternative Fuel Vehicle Market. Cities around the world are increasingly prioritizing sustainable transportation options as part of their urban planning and smart city initiatives. Electric and hydrogen-powered vehicles, being central to this vision, are receiving strong governmental support through subsidies and infrastructure development. Alongside, there is a rising demand for vehicle-to-grid (V2G) technology, which allows EVs to interact with the power grid, providing additional benefits such as energy storage and grid stabilization. With environmental sustainability at the forefront, this trend towards greener mobility solutions is expected to continue, driven by regulatory incentives, environmental awareness, and technological innovation.

- For example, in June 2023, Mobilize, the Renault Group’s mobility services brand, introduced the Mobilize PowerBox bidirectional charging station alongside the upcoming Renault 5 electric vehicle.This system enables the Renault 5 to act as an energy supplier by allowing two-way energy flow; the vehicle can not only charge from the grid but also supply electricity back to it.This integration of Vehicle-to-Grid (V2G) technology allows users to sell excess electricity back to the grid, potentially reducing their overall electricity bills.

Market Challenges Analysis:

High Initial Cost and Limited Affordability

One of the primary challenges facing the Global Alternative Fuel Vehicle Market is the high initial cost of alternative fuel vehicles, particularly electric vehicles (EVs) and hydrogen-powered vehicles. Despite decreasing production costs, these vehicles remain more expensive than their internal combustion engine counterparts. The high upfront costs, driven by the expense of advanced batteries and fuel cells, deter a significant portion of potential buyers, especially in developing regions. Although subsidies and tax incentives are available in some countries, they are often insufficient to offset the price difference for many consumers. Until the production cost of batteries and fuel cell technology continues to fall, this challenge will persist, limiting widespread adoption and slowing the growth of the alternative fuel vehicle market.

Insufficient Charging and Refueling Infrastructure

The lack of adequate charging and refueling infrastructure remains another significant challenge for the expansion of the Global Alternative Fuel Vehicle Market. Despite improvements in infrastructure in key markets such as Europe, North America, and parts of Asia Pacific, many regions still face a shortage of accessible and reliable charging stations for electric vehicles and refueling stations for hydrogen and CNG-powered vehicles. The inconvenience of locating a charging or refueling station, coupled with the uncertainty of availability, deters potential buyers from transitioning to alternative fuel vehicles. This infrastructure gap hampers the market’s potential, especially in rural areas and emerging economies, where such facilities are even more limited. The expansion of refueling networks requires substantial investment, making it a challenge for governments and private companies to keep up with the increasing demand for alternative fuel vehicles.

Market Opportunities:

Government Initiatives and Policy Support

The Global Alternative Fuel Vehicle Market presents significant opportunities due to the growing number of government initiatives and policy support aimed at promoting clean transportation solutions. Many countries are setting ambitious goals for reducing greenhouse gas emissions, and providing financial incentives such as tax rebates, subsidies, and grants to accelerate the adoption of alternative fuel vehicles. These policies are particularly impactful in key regions like Europe, North America, and China, where regulatory frameworks are increasingly favoring electric vehicles (EVs) and hydrogen-powered vehicles. Such government backing provides a strong growth impetus for manufacturers and investors, creating favorable conditions for market expansion.

Technological Innovations and Advancements in Energy Solutions

The Global Alternative Fuel Vehicle Market also benefits from ongoing technological innovations that create new opportunities for market growth. Advancements in battery technology, such as improved energy density and reduced charging times, enhance the attractiveness of electric vehicles for consumers. Furthermore, the development of hydrogen fuel cell technology and improved infrastructure for EV charging stations are opening doors to broader adoption. As automakers and energy companies invest heavily in research and development, these technological advancements will not only drive down costs but also enhance the overall efficiency of alternative fuel vehicles, paving the way for sustained market growth in the coming years.

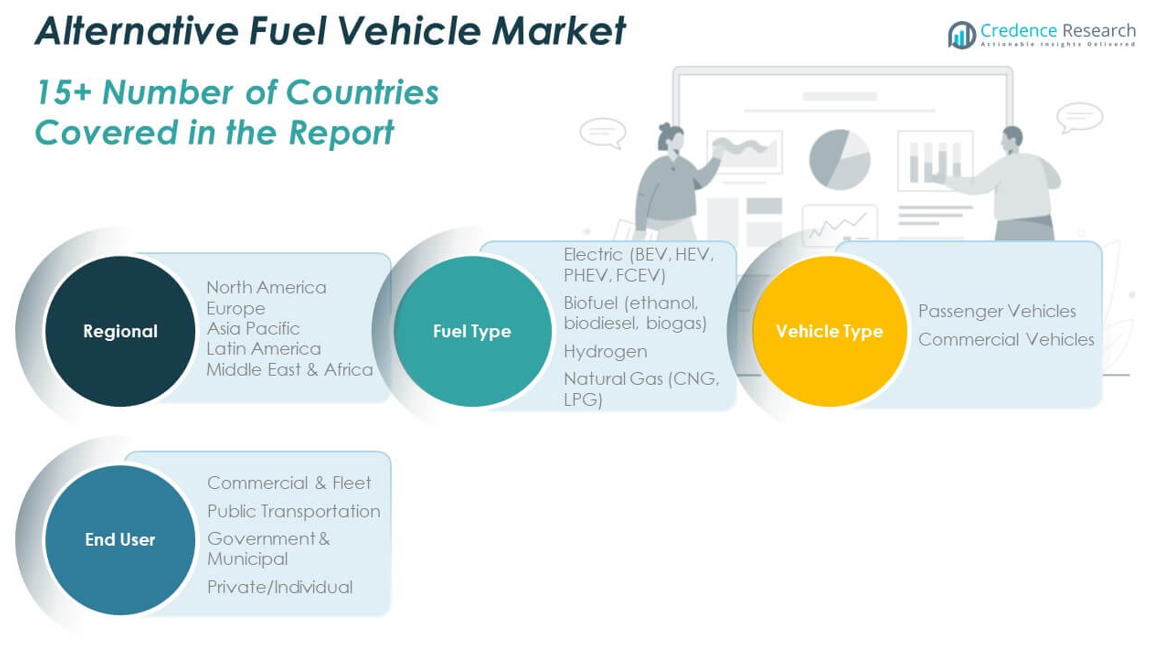

Market Segmentation Analysis:

The Global Alternative Fuel Vehicle Market is characterized by several key segments, each contributing to its overall growth.

By fuel type segment includes electric vehicles (BEVs, HEVs, PHEVs, FCEVs), which dominate due to growing demand for sustainable transport solutions. Biofuels such as ethanol, biodiesel, and biogas are emerging as viable alternatives, particularly in regions with strong agricultural bases. Hydrogen fuel cell vehicles are gaining traction in the commercial sector, while natural gas vehicles (CNG and LPG) continue to see adoption in both passenger and commercial categories, driven by cost-efficiency and lower emissions.

- For instance, Tesla Model 3offers a range of 358 miles per charge with a battery energy density of 250 Wh/kg

By vehicle type segment includes passenger vehicles and commercial vehicles. Passenger vehicles are the largest market segment, benefiting from increasing consumer demand for eco-friendly transportation options. Commercial vehicles, which include trucks and buses, are also growing, driven by the need for greener logistics and public transportation solutions.

By end-user segment is diverse, with significant adoption in commercial and fleet operations, where cost-efficiency and environmental regulations play a crucial role. Public transportation systems, especially in urban centers, are increasingly transitioning to alternative fuel vehicles to reduce air pollution. Government and municipal entities are also contributing to market growth by adopting alternative fuel solutions for their fleets. The private/individual segment is expanding, particularly in developed markets, as consumers become more environmentally conscious and seek sustainable mobility solutions. These segments together are shaping the future of the Global Alternative Fuel Vehicle Market.

- For example, Amazon operates a fleet of 20,000 electric delivery vans, achieving a 30% emission reduction.

Segmentation:

By Fuel Type Segment

- Electric (BEV, HEV, PHEV, FCEV)

- Biofuel (ethanol, biodiesel, biogas)

- Hydrogen

- Natural Gas (CNG, LPG)

By Vehicle Type Segment

- Passenger Vehicles

- Commercial Vehicles

By End User Segment

- Commercial & Fleet

- Public Transportation

- Government & Municipal

- Private/Individual

By Regional Segment

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America Alternative Fuel Vehicle Market

The North America Alternative Fuel Vehicle Market size was valued at USD 76.40 billion in 2018, reaching USD 147.30 billion in 2024, and is anticipated to reach USD 414.47 billion by 2032, at a CAGR of 12.9% during the forecast period. The region holds a significant share of the global market, driven by the United States, which is at the forefront of adopting electric vehicles (EVs) and hybrid electric vehicles (HEVs). The U.S. government offers extensive subsidies, tax incentives, and grants to consumers and manufacturers to accelerate the transition to clean vehicles. The region’s strong infrastructure for EV charging stations and ongoing investments in green technology make it an attractive market for EV manufacturers. The growing awareness of climate change and the need for energy-efficient solutions further propels market growth.

Europe Alternative Fuel Vehicle Market

The Europe Alternative Fuel Vehicle Market size was valued at USD 49.78 billion in 2018, reaching USD 92.33 billion in 2024, and is anticipated to reach USD 236.26 billion by 2032, at a CAGR of 11.5% during the forecast period. Europe is one of the largest markets for alternative fuel vehicles, driven by stringent emissions regulations and ambitious environmental targets set by the European Union. Countries such as Germany, France, and the UK are leading the transition to electric vehicles, supported by extensive charging infrastructure and government incentives. European automakers are also investing heavily in electric and hydrogen fuel cell technologies, contributing to the region’s dominance in the global market.

Asia Pacific Alternative Fuel Vehicle Market

The Asia Pacific Alternative Fuel Vehicle Market size was valued at USD 107.83 billion in 2018, reaching USD 219.18 billion in 2024, and is anticipated to reach USD 653.05 billion by 2032, at a CAGR of 13.7% during the forecast period. Asia Pacific holds the largest share of the global market, driven primarily by China, which is the world’s largest market for electric vehicles. The Chinese government’s policies, including subsidies for electric vehicle purchases, incentives for manufacturing, and investments in EV infrastructure, are key contributors to the region’s growth. Japan and South Korea are also leading players in electric and hybrid vehicle adoption. The expanding middle class and growing environmental awareness across countries like India and China are fueling the demand for alternative fuel vehicles in the region.

Latin America Alternative Fuel Vehicle Market

The Latin America Alternative Fuel Vehicle Market size was valued at USD 10.84 billion in 2018, reaching USD 20.92 billion in 2024, and is anticipated to reach USD 51.11 billion by 2032, at a CAGR of 10.9% during the forecast period. In Latin America, Brazil and Mexico dominate the market due to their large automotive industries and the rising demand for energy-efficient vehicles. Government incentives and growing consumer awareness of environmental issues support the adoption of alternative fuel vehicles. Additionally, the shift toward biofuels, particularly ethanol in Brazil, plays a vital role in driving the regional market’s growth. The expansion of EV charging infrastructure and cleaner energy initiatives further supports market development.

Middle East Alternative Fuel Vehicle Market

The Middle East Alternative Fuel Vehicle Market size was valued at USD 6.74 billion in 2018, reaching USD 12.00 billion in 2024, and is anticipated to reach USD 28.00 billion by 2032, at a CAGR of 10.2% during the forecast period. The Middle East region is gradually adopting alternative fuel vehicles, with significant growth seen in the UAE, Saudi Arabia, and Qatar. The governments in these countries are increasingly investing in clean energy technologies and offering incentives for electric and hybrid vehicle purchases. The UAE, in particular, has taken steps to promote EV adoption through infrastructure development and sustainability initiatives. The region’s efforts to diversify energy sources, reduce dependency on oil, and improve air quality contribute to the market’s expansion.

Africa Alternative Fuel Vehicle Market

The Africa Alternative Fuel Vehicle Market size was valued at USD 4.40 billion in 2018, reaching USD 9.42 billion in 2024, and is anticipated to reach USD 21.51 billion by 2032, at a CAGR of 9.9% during the forecast period. While the market for alternative fuel vehicles in Africa remains relatively small compared to other regions, it is showing signs of significant growth. South Africa leads the region in the adoption of electric vehicles, supported by government policies and incentives. The growing focus on renewable energy, particularly solar and wind, presents opportunities for integrating sustainable transportation solutions. As the need for cost-effective and environmentally friendly mobility options rises, the market for alternative fuel vehicles in Africa is expected to grow steadily over the next decade.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Tesla, Inc.

- BYD Company Ltd.

- Toyota Motor Corporation

- Volkswagen Group

- General Motors

- BMW Group

- Nissan Motor Co., Ltd.

- Hyundai Motor Company

- Ford Motor Company

- Honda Motor Co., Ltd.

Competitive Analysis:

The Global Alternative Fuel Vehicle Market is highly competitive, with key players striving to maintain their market share through technological advancements, strategic partnerships, and strong brand presence. Major automotive manufacturers such as Tesla, Nissan, General Motors, BMW, and Toyota lead the market, offering a wide range of electric and hybrid vehicles. These companies invest heavily in research and development to improve battery technology, enhance vehicle performance, and reduce costs. New entrants, particularly from China, such as BYD and NIO, are also expanding their presence globally with innovative electric vehicles at competitive prices. Governments worldwide are increasingly offering incentives, which further intensifies competition, pushing manufacturers to innovate and provide sustainable solutions. Charging infrastructure providers, such as ChargePoint and Tesla’s Supercharger network, also play a crucial role in shaping the market by ensuring the accessibility and convenience of alternative fuel vehicles. This competitive landscape fosters continuous innovation.

Recent Developments:

- In June 2025, General Motors announced a $4 billion investment in its U.S. manufacturing facilities to boost the production of both gasoline and electric vehicles.This strategic move underscores GM’s commitment to an all-electric future while maintaining a diverse vehicle portfolio.

Market Concentration & Characteristics:

The Global Alternative Fuel Vehicle Market is moderately concentrated, with a few key players dominating the market share while numerous smaller players contribute to innovation and regional growth. Leading automotive manufacturers such as Tesla, General Motors, Toyota, and BMW control a significant portion of the market, driven by their established brand presence and extensive investment in electric and hybrid vehicles. The market also includes emerging players, particularly from China, such as BYD and NIO, which offer competitively priced electric vehicles and are expanding globally. The increasing focus on sustainability, government incentives, and technological advancements in battery and charging infrastructure have created a dynamic and competitive environment. While large companies dominate in terms of volume and infrastructure, smaller players and new entrants continue to challenge the market by focusing on innovation, cost reduction, and regional customization. This dynamic fosters healthy competition and continued market evolution.

Report Coverage:

The research report offers an in-depth analysis based on Fuel Type, Vehicle Type and End User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The Global Alternative Fuel Vehicle Market will continue to experience rapid growth, driven by increasing demand for sustainable transportation.

- Electric vehicles (EVs) are expected to lead the market, with advancements in battery technology and charging infrastructure making them more affordable and convenient.

- Governments will impose stricter emission regulations, encouraging the transition to zero-emission vehicles.

- Hydrogen fuel cell vehicles will expand, particularly in heavy-duty sectors like trucks and buses.

- Biofuels and natural gas vehicles will see consistent growth, especially in regions with established infrastructure and support.

- Automakers will target global expansion, with increased focus on emerging markets.

- Investment in autonomous and connected vehicle technologies will rise, integrating alternative fuel solutions with smart capabilities.

- The growth of charging and refueling infrastructure will support broader adoption, particularly in urban areas.

- Consumer awareness about environmental sustainability will continue to drive demand for cleaner mobility options.

- Strategic collaborations between automakers, governments, and technology providers will be crucial for shaping the market’s future.