| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Antidiabetics Market Size 2024 |

USD 86,062.60 Million |

| Antidiabetics Market, CAGR |

9.67% |

| Antidiabetics Market Size 2032 |

USD 1,89,645.41 Million |

Market Overview:

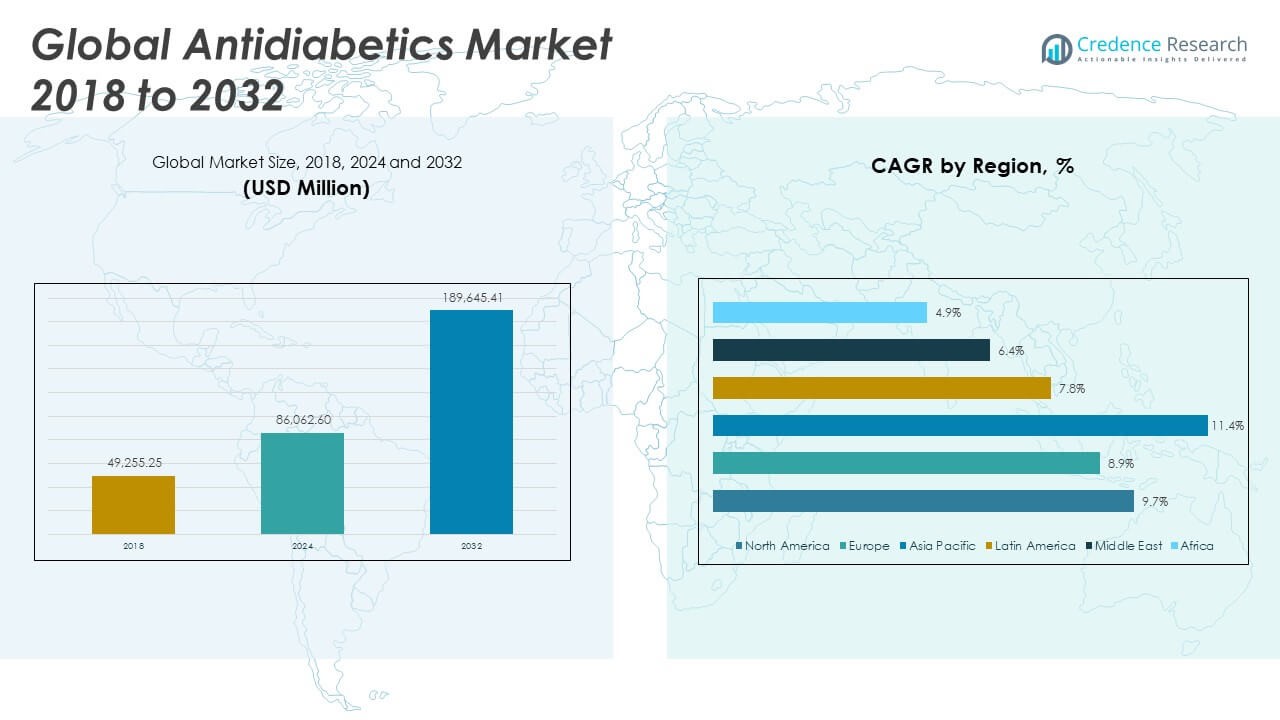

The Global Antidiabetics Market size was valued at USD 49,255.25 million in 2018 to USD 86,062.60 million in 2024 and is anticipated to reach USD 1,89,645.41 million by 2032, at a CAGR of 9.67% during the forecast period.

One of the key drivers of the market is the rising global prevalence of type 1 and type 2 diabetes, largely attributed to factors such as obesity, poor dietary habits, sedentary lifestyles, and increasing life expectancy. The growing patient base is fueling demand for both insulin-based therapies and oral antidiabetic drugs. Innovation in treatment classes especially GLP-1 receptor agonists and SGLT-2 inhibitors—is playing a transformative role in improving patient outcomes while expanding market value. In addition, the patent expiry of several blockbuster drugs has opened the market to cost-effective biosimilars, encouraging broader access to treatment. Government initiatives and improved insurance coverage in many countries are also promoting early diagnosis and treatment, helping to further increase demand. Continuous investment in research and development by pharmaceutical companies is fostering a steady stream of novel therapeutics, delivery devices, and combination treatments that meet the evolving needs of diabetic patients.

Regionally, North America dominates the global antidiabetics market, driven by high healthcare spending, well-established reimbursement systems, and a significant diabetic population. The region’s early adoption of novel therapies and technologies, along with strong support from healthcare providers and insurers, reinforces its market leadership. Meanwhile, the Asia-Pacific region is expected to record the fastest growth rate over the forecast period, spurred by rapidly increasing diabetes incidence in countries like China and India, urbanization, changing dietary patterns, and improved healthcare access. Europe maintains a steady market presence, benefiting from structured healthcare infrastructure, government-supported treatment protocols, and widespread use of newer drug classes. Other regions, including Latin America and the Middle East & Africa, are gradually emerging, with growth supported by demographic shifts and ongoing improvements in healthcare delivery, although economic constraints and limited infrastructure continue to pose challenges.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Global Antidiabetics Market was valued at USD 86,062.60 million in 2024 and is projected to reach USD 1,89,645.41 million by 2032, growing at a strong CAGR of 9.67%.

- Increasing prevalence of type 1 and type 2 diabetes, fueled by obesity, poor diet, and sedentary lifestyles, is the primary growth driver globally.

- GLP-1 receptor agonists and SGLT-2 inhibitors are transforming treatment protocols with superior cardiovascular and renal outcomes, gaining rapid clinical adoption.

- Expanding access through national health programs, broader insurance coverage, and public health initiatives is widening the patient base, especially in emerging economies.

- Entry of biosimilars and generics following key patent expirations is lowering treatment costs and enabling deeper market penetration in low-income regions.

- Affordability gaps and infrastructure limitations in rural and low-resource settings continue to restrict access to advanced therapies and diagnostics.

- North America leads the market with 35% share due to high healthcare expenditure, while Asia-Pacific records the fastest growth due to rapid urbanization and rising disease burden.

Market Drivers:

Surging Diabetes Prevalence Due to Lifestyle Changes and Aging Populations Across the Globe

The Global Antidiabetics Market is primarily driven by the rising incidence of diabetes, particularly type 2 diabetes, which continues to escalate due to sedentary lifestyles, unhealthy dietary habits, and growing obesity rates. Urbanization and reduced physical activity have contributed to metabolic disorders becoming more prevalent, especially in middle-income and developing countries. Aging populations further compound the issue, with older adults at higher risk of insulin resistance and impaired glucose tolerance. Increasing awareness campaigns and routine health screenings are improving diagnosis rates, pushing more patients into the treatment pipeline. With the World Health Organization projecting diabetes to become one of the leading causes of death globally, demand for antidiabetic drugs and therapies continues to rise sharply. This surge in disease burden creates a continuous and urgent need for effective treatment options, fueling market expansion.

Strong Product Pipeline and Adoption of Next-Generation Drug Classes with Superior Clinical Outcomes

Pharmaceutical innovation is another powerful driver of the Global Antidiabetics Market, with a strong pipeline of novel therapies designed to improve glycemic control and reduce associated complications. The introduction of GLP-1 receptor agonists and SGLT-2 inhibitors has transformed treatment approaches due to their proven cardiovascular and renal benefits, weight reduction properties, and favorable safety profiles. These therapies are being rapidly integrated into treatment guidelines and adopted by healthcare professionals, particularly for patients with comorbidities. Continuous advancements in insulin analogs, including ultra-rapid and ultra-long-acting formulations, are improving adherence and patient convenience. Drug-device combination innovations, such as insulin pens and pumps, also support precision dosing and better patient outcomes. The adoption of these newer classes is reshaping the therapeutic landscape and increasing revenue potential.

- For example, Medtronic’s MiniMed 780G insulin pump, launched in 2023, provides automated insulin delivery with a time-in-range metric of 76% over 90 days, as verified in a 2,500-patient real-world study.

Expansion of Access Through Government Programs, Insurance Coverage, and Public Health Campaigns

Supportive government policies and health coverage programs play a critical role in boosting access to antidiabetic treatments across both developed and emerging economies. National diabetes prevention and control programs are enhancing early detection and ensuring affordable access to essential medications. Reimbursement policies are becoming more inclusive, covering newer drug classes and combination therapies, which drives uptake among patients and healthcare providers. Partnerships between governments, NGOs, and private players are also addressing access challenges through subsidized pricing and supply chain expansion. Educational initiatives that emphasize disease management and lifestyle modification further support sustained treatment engagement. These systemic efforts are broadening the patient base and strengthening market demand.

- For example, Sanofi’s 2024 Business Responsibility and Sustainability Report confirms that the company is actively partnering with Indian health authorities and NGOs to improve access to diabetes care. Sanofi collaborates with government programs, including initiatives aligned with the National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke (NPCDCS), to expand screening and provide subsidized insulin to underserved populations in India.

Proliferation of Generic and Biosimilar Products Driving Competitive Pricing and Market Reach

The expiration of patents for several key branded antidiabetics has led to the widespread introduction of generic drugs and biosimilar insulins, making treatment more affordable and accessible. The Global Antidiabetics Market benefits significantly from these lower-cost alternatives, which allow broader penetration into cost-sensitive markets. Pharmaceutical companies are increasingly investing in biosimilar development to capture price-conscious consumer segments and expand into untapped regions. Regulatory approvals are becoming more streamlined, encouraging the availability of high-quality generic formulations that meet safety and efficacy standards. Healthcare systems under budget pressure are also encouraging the use of generics to reduce overall treatment costs. This trend supports volume growth and intensifies market competition, further driving innovation and price efficiency.

Market Trends:

Integration of Digital Health Platforms to Enhance Monitoring and Treatment Adherence

The Global Antidiabetics Market is witnessing a significant shift toward digital health integration, with telemedicine, mobile apps, and remote monitoring tools becoming essential components of diabetes care. Digital platforms support real-time glucose tracking, medication reminders, and remote consultations, which improve treatment adherence and patient engagement. Wearable devices such as continuous glucose monitors (CGMs) are enabling patients and clinicians to monitor glucose trends more accurately and adjust therapy in real time. These tools are particularly effective for managing complex cases and minimizing hospital visits. Startups and established tech firms are increasingly partnering with pharmaceutical companies to create integrated digital-therapeutic solutions. The convergence of data analytics, machine learning, and personalized medicine is reshaping how diabetes is diagnosed, monitored, and managed.

Growing Focus on Patient-Centered Care and Personalized Treatment Protocols

Healthcare providers are increasingly adopting patient-centered models in diabetes management, emphasizing personalized treatment strategies based on genetic, phenotypic, and behavioral profiles. The Global Antidiabetics Market is adapting to this trend by supporting the development of customized therapies and decision-support tools that align with individual needs. This approach enhances treatment efficacy while reducing side effects and improving quality of life. Clinical guidelines are now incorporating risk stratification methods that account for comorbidities, lifestyle patterns, and social determinants of health. Pharmaceutical firms are investing in research that identifies biomarkers and predictive indicators to guide therapy selection. Personalized medicine is becoming central to modern diabetes care and is expected to shape future product development and marketing strategies.

Rising Demand for Combination Therapies for Simplified Disease Management

The complexity of diabetes and the need for multi-targeted intervention have led to a surge in demand for combination therapies that simplify treatment regimens. The Global Antidiabetics Market is seeing a steady rise in fixed-dose combination products that reduce pill burden and improve patient compliance. These formulations integrate different mechanisms of action, offering synergistic benefits such as improved glycemic control and reduced cardiovascular risks. Physicians are increasingly prescribing dual and triple therapy combinations, especially in patients with poor glycemic control despite monotherapy. Regulatory bodies are showing strong support for these products by accelerating approvals and encouraging innovation in fixed-dose development. This trend reflects a shift in clinical practice toward more holistic and streamlined treatment approaches.

- For example, clinical trials show that triple therapy with low-dose dapagliflozin plus saxagliptin and metformin reduces HbA1c by 1.03% compared to 0.63% and 0.69% with dual therapies (P < .0001), with 41.6% of patients achieving HbA1c <7.0% versus 21.8% and 29.8% for dual therapies.

Emphasis on Sustainability and Environmental Responsibility in Manufacturing and Packaging

Sustainability is emerging as a critical trend across pharmaceutical industries, including the Global Antidiabetics Market. Companies are adopting eco-friendly manufacturing practices, reducing carbon footprints, and shifting toward biodegradable or recyclable packaging for insulin pens and drug delivery devices. Regulatory agencies are also encouraging sustainable initiatives by updating compliance standards and rewarding environmentally responsible practices. Pharmaceutical manufacturers are investing in green chemistry, energy-efficient production, and waste reduction technologies to meet both environmental and economic goals. These initiatives appeal to environmentally conscious consumers and investors, aligning market growth with global sustainability efforts. Environmental stewardship is becoming a competitive differentiator in the evolving healthcare landscape.

- For example, industry-wide, reusable insulin pens are being promoted to reduce the approximately 79 tonnes of plastic waste and 1,000 tonnes of CO₂ generated annually by disposable pens in England alone.

Market Challenges Analysis:

High Treatment Costs and Limited Access in Low-Income and Rural Populations

Affordability and accessibility remain major challenges within the Global Antidiabetics Market, especially in low-income countries and underserved rural areas. Despite the growing availability of generics and biosimilars, the cost of advanced therapies such as GLP-1 receptor agonists, SGLT-2 inhibitors, and insulin analogs remains prohibitively high for large segments of the global population. Many healthcare systems lack adequate reimbursement frameworks or subsidized programs to make these treatments accessible to economically disadvantaged patients. In regions with limited healthcare infrastructure, patients face delays in diagnosis and inconsistent access to essential medicines and monitoring tools. The lack of trained medical professionals further restricts the delivery of effective diabetes care in remote areas. This disparity in treatment availability and affordability undermines the potential of the Global Antidiabetics Market to fully address the global diabetes burden.

Complex Regulatory Pathways and Safety Concerns Related to Emerging Therapies

The regulatory environment presents significant hurdles, particularly for new drug approvals and biosimilar entries in the Global Antidiabetics Market. Companies face lengthy and costly approval processes that vary across regions, creating delays in product launches and market penetration. Concerns over long-term safety and side effects of newer classes, including reports of gastrointestinal disturbances, pancreatitis, or cardiovascular risks, have prompted stricter scrutiny from regulatory agencies. Post-marketing surveillance requirements and adverse event reporting add to operational burdens for manufacturers. Inconsistencies in regulatory standards between countries can also hinder international expansion and limit product availability in emerging markets. These complexities challenge innovation and increase the cost and time needed to bring novel therapies to market.

Market Opportunities:

Expansion into Emerging Economies with Untapped Patient Populations and Growing Healthcare Infrastructure

The Global Antidiabetics Market has significant growth potential in emerging economies where large undiagnosed and untreated diabetic populations remain. Rising healthcare investments, urbanization, and greater awareness of chronic diseases are improving diagnosis rates and increasing demand for treatment. Governments are introducing national diabetes programs and expanding health insurance coverage, creating favorable conditions for market entry. Pharmaceutical companies can capitalize on these opportunities by offering affordable drug formulations, building local partnerships, and investing in region-specific supply chains. The growing penetration of telemedicine and mobile health platforms further enhances access in remote areas. This expansion into underserved regions can substantially increase revenue while improving global diabetes management outcomes.

Innovation in Oral Biologics, Smart Delivery Systems, and Personalized Medicine

Technological innovation presents strong opportunities for differentiation and market leadership. The Global Antidiabetics Market stands to benefit from the development of oral insulin and other non-invasive delivery methods, which can improve patient compliance and convenience. Smart insulin pens, wearable glucose monitors, and AI-based treatment optimization platforms offer advanced solutions that align with personalized care models. Investment in pharmacogenomics and biomarker-driven therapy selection can create precision treatment strategies tailored to individual patient profiles. These innovations open new avenues for premium product segments and enhance therapeutic outcomes. Companies focusing on patient-centric technologies and adaptive care models can build lasting competitive advantages.

Market Segmentation Analysis:

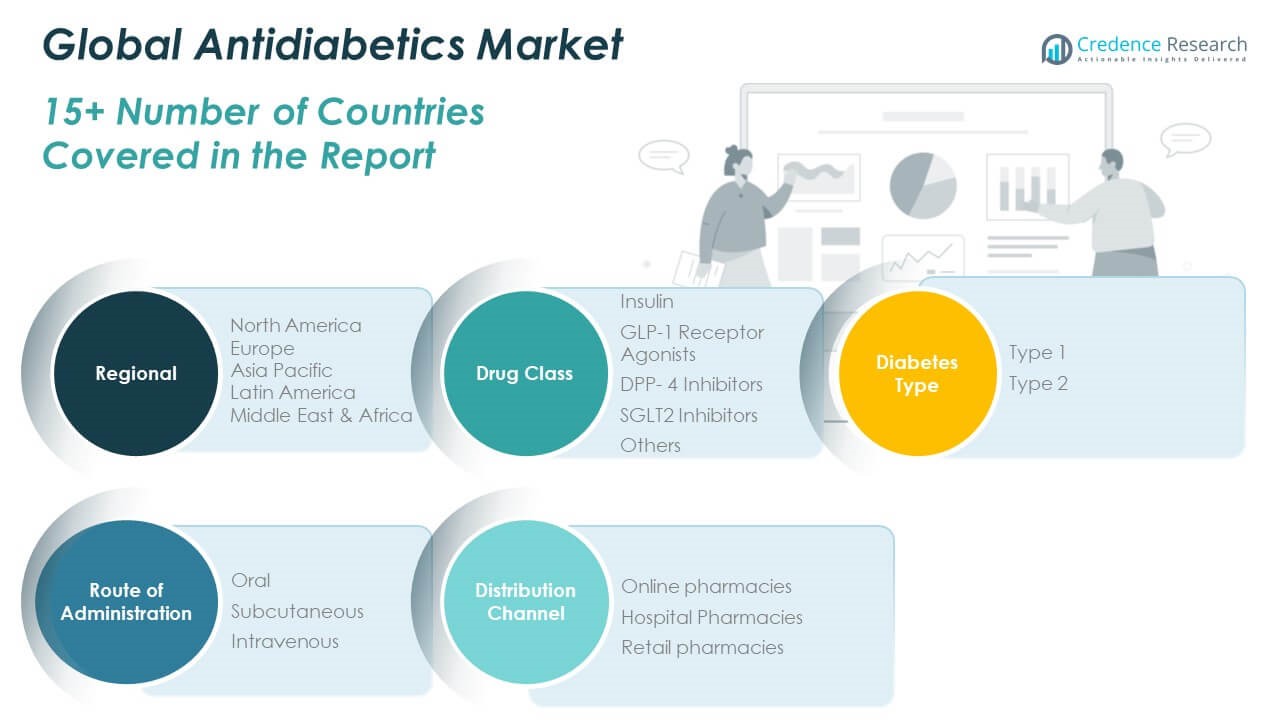

The Global Antidiabetics Market is segmented by drug class, diabetes type, route of administration, and distribution channel.

By drug class, insulin holds a major share due to its essential role in type 1 and advanced type 2 diabetes. GLP-1 receptor agonists and SGLT2 inhibitors are gaining rapid traction due to their cardiovascular and renal benefits, while DPP-4 inhibitors continue to offer value through moderate efficacy and safety. The “Others” category includes alpha-glucosidase inhibitors, thiazolidinediones, and newer pipeline drugs that serve niche demands.

- For example, according to Sanofi’s 2024 annual report, Lantus® recorded global sales of €1.6 billion (USD 1.7 billion), with dominant usage through subcutaneous prefilled pens.

By diabetes type, type 2 diabetes dominates the market, driven by its high global prevalence and rising obesity rates. Type 1 diabetes represents a smaller but significant share that continues to grow with advancements in insulin therapies and monitoring technologies.

By route of administration, subcutaneous drugs lead due to the widespread use of insulin and injectable GLP-1s. Oral formulations are expanding rapidly with the growing adoption of DPP-4 and SGLT2 inhibitors. Intravenous options remain limited to clinical settings.

- For example, Novo Nordisk’s FlexTouch® delivery system, used in insulin pens, enhances ease of use and is adopted in over 100 countries, supporting widespread penetration.

By distribution channel, retail pharmacies account for the largest share due to accessibility and high patient footfall. Hospital pharmacies serve acute and inpatient needs, while online pharmacies are growing swiftly due to convenience and expanding digital health adoption.

Segmentation:

By Drug Class:

- Insulin

- GLP-1 Receptor Agonists

- DPP-4 Inhibitors

- SGLT2 Inhibitors

- Others

By Diabetes Type:

- Type 1 Diabetes

- Type 2 Diabetes

By Route of Administration:

- Oral

- Subcutaneous

- Intravenous

By Distribution Channel:

- Online Pharmacies

- Hospital Pharmacies

- Retail Pharmacies

By Region:

- North America (U.S., Canada, Mexico)

- Europe (Germany, UK, France, Italy, Spain, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Southeast Asia, Rest of Asia Pacific)

- Latin America (Brazil, Argentina, Rest of Latin America)

- Middle East (GCC Countries, Israel, Turkey, Rest of Middle East)

- Africa (South Africa, Egypt, Rest of Africa)

Regional Analysis:

The North America Antidiabetics Market size was valued at USD 20,895.55 million in 2018 to USD 36,120.04 million in 2024 and is anticipated to reach USD 79,820.81 million by 2032, at a CAGR of 9.7% during the forecast period. North America holds the largest share in the Global Antidiabetics Market, accounting for 35% of the total revenue. It benefits from a well-established healthcare infrastructure, early adoption of advanced therapies, and high per capita healthcare spending. The region’s strong demand is fueled by the high prevalence of obesity and type 2 diabetes, particularly in the United States. Pharmaceutical companies operating in the region continue to invest heavily in R&D and digital diabetes management tools. Government support through Medicare and Medicaid coverage also enhances access to newer drug classes and monitoring devices. The market continues to grow steadily with increased use of GLP-1 receptor agonists and SGLT-2 inhibitors.

The Europe Antidiabetics Market size was valued at USD 15,482.89 million in 2018 to USD 26,172.73 million in 2024 and is anticipated to reach USD 54,639.24 million by 2032, at a CAGR of 8.9% during the forecast period. Europe contributes 25% to the Global Antidiabetics Market and maintains steady growth through its universal healthcare systems and established treatment protocols. Countries like Germany, France, and the UK lead regional adoption, supported by structured reimbursement mechanisms and high awareness of diabetes-related risks. Physicians widely prescribe modern insulin analogs and combination therapies to manage complications and improve patient compliance. Governments continue to promote early screening and chronic disease management programs. The growing elderly population and rise in lifestyle-related diseases sustain demand. It remains a mature but evolving market with a strong regulatory framework.

The Asia Pacific Antidiabetics Market size was valued at USD 9,232.90 million in 2018 to USD 17,521.05 million in 2024 and is anticipated to reach USD 43,850.76 million by 2032, at a CAGR of 11.4% during the forecast period. Asia Pacific is the fastest-growing region in the Global Antidiabetics Market, currently holding a 22% market share. Rapid urbanization, increasing disposable income, and westernized diets are contributing to a sharp rise in diabetes cases in countries like China and India. Governments are investing in healthcare infrastructure, screening programs, and national diabetes policies. The demand for affordable generics and biosimilars is strong, especially in rural areas. International and local pharmaceutical firms are expanding their presence through joint ventures and pricing strategies tailored for low- and middle-income populations. Rising digital adoption also supports remote care and glucose monitoring in underserved areas.

The Latin America Antidiabetics Market size was valued at USD 2,090.89 million in 2018 to USD 3,602.82 million in 2024 and is anticipated to reach USD 6,922.59 million by 2032, at a CAGR of 7.8% during the forecast period. Latin America holds a 7% share in the Global Antidiabetics Market and shows stable growth driven by rising disease awareness and healthcare reforms. Brazil and Mexico lead regional demand, supported by expanding access to public healthcare and increasing urbanization. Treatment coverage is improving, though access disparities remain between urban and rural areas. Multinational drug manufacturers are focusing on launching cost-effective insulin and oral antidiabetics to meet growing demand. Regulatory pathways are becoming more transparent, encouraging new market entrants. Government partnerships with private players are enhancing diabetes care outreach and education.

The Middle East Antidiabetics Market size was valued at USD 1,045.89 million in 2018 to USD 1,620.34 million in 2024 and is anticipated to reach USD 2,811.97 million by 2032, at a CAGR of 6.4% during the forecast period. The Middle East accounts for 6% of the Global Antidiabetics Market and is expanding due to lifestyle changes, dietary habits, and genetic predisposition to metabolic disorders. Countries such as Saudi Arabia and the UAE are witnessing an increase in diabetes prevalence, leading to higher demand for insulin and modern oral therapies. Government-led national health strategies are focused on screening, prevention, and treatment programs. Healthcare systems are integrating digital tools to manage diabetes more effectively. Pharmaceutical companies are also targeting the region with tailored products and pricing strategies. While market size remains smaller, growth prospects are promising due to rising awareness and healthcare investment.

The Africa Antidiabetics Market size was valued at USD 507.13 million in 2018 to USD 1,025.61 million in 2024 and is anticipated to reach USD 1,600.05 million by 2032, at a CAGR of 4.9% during the forecast period. Africa holds a 5% share of the Global Antidiabetics Market and represents an emerging growth frontier with significant challenges. Limited healthcare infrastructure, low screening rates, and affordability issues hinder widespread treatment adoption. Nonetheless, rising urbanization, changing diets, and increased awareness are pushing diabetes prevalence higher. International health organizations and donor-funded programs are supporting outreach and medication access. Governments are gradually expanding public health services and chronic disease management strategies. Long-term growth will depend on infrastructure development, regulatory improvements, and sustained investment in healthcare access.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Boehringer Ingelheim

- Novartis AG

- Takeda Pharmaceutical Company

- Merck & Co., Inc.

- AstraZeneca plc

- Johnson & Johnson Services Inc.

- Novo Nordisk

- Bayer AG

- Eli Lilly and Company

- Sanofi

Competitive Analysis:

The Global Antidiabetics Market features a highly competitive landscape led by multinational pharmaceutical companies focused on innovation, product expansion, and strategic collaborations. It includes major players such as Novo Nordisk, Sanofi, Eli Lilly, Merck & Co., AstraZeneca, and Boehringer Ingelheim, all actively investing in advanced insulin formulations and novel oral therapies. The market is seeing a surge in biosimilar launches, intensifying competition and driving price-based strategies in emerging regions. Companies are strengthening portfolios with GLP-1 receptor agonists, SGLT-2 inhibitors, and fixed-dose combinations to address evolving patient needs. It continues to attract new entrants offering digital diabetes management solutions and smart drug delivery systems. Strategic partnerships with healthcare providers and governments support broader access and distribution. The market’s competitive intensity is further shaped by continuous R&D, regulatory approvals, and global expansion efforts aimed at capturing untapped populations and reinforcing therapeutic leadership.

Recent Developments:

- In June 2025, Eli Lilly agreed to acquire gene-editing company Verve Therapeutics for up to $1.3 billion. The deal supports Lilly’s strategy in cardiometabolic medicine, with Verve’s lead candidate, VERVE‑102, aiming to deliver a lifelong reduction in cardiovascular risk through PCSK9 gene editing.

- In April 2025, Johnson & Johnson Services Inc.completed the acquisition of Intra-Cellular Therapies adding CAPLYTA® to its portfolio. While primarily a neuroscience asset, this acquisition reflects J&J’s broader strategy to strengthen its therapeutic offerings, though no direct antidiabetic product launch was noted.

- In June 2024, AstraZeneca plcreceived FDA approval for Farxiga (dapagliflozin) to treat pediatric type 2 diabetes patients aged 10 and older in the US, broadening treatment options for younger populations.

Market Concentration & Characteristics:

The Global Antidiabetics Market is moderately concentrated, with a few dominant players accounting for a significant share of total revenue. It features a mix of patented branded drugs and an expanding portfolio of generics and biosimilars. Leading companies focus on continuous innovation, extensive R&D, and strategic alliances to maintain competitive advantage. It exhibits high product differentiation, particularly across drug classes such as insulin analogs, GLP-1 receptor agonists, and SGLT-2 inhibitors. Regulatory complexity, pricing pressures, and patent expirations influence market dynamics and entry barriers. The market favors companies with strong global distribution networks, advanced manufacturing capabilities, and diverse therapeutic pipelines. It is characterized by evolving treatment protocols, growing digital integration, and rising demand for personalized medicine.

Report Coverage:

The research report offers an in-depth analysis based on drug class, diabetes type, route of administration, and distribution channel. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising global diabetes prevalence will continue to drive sustained demand for both insulin and oral antidiabetic therapies.

- Increased adoption of GLP-1 receptor agonists and SGLT-2 inhibitors is expected to reshape treatment protocols.

- Biosimilar insulin products will expand access in cost-sensitive markets and intensify competition.

- Digital health tools and connected drug delivery systems will improve patient adherence and monitoring.

- Personalized medicine and biomarker-based treatment strategies will gain wider clinical application.

- Emerging markets, especially in Asia and Latin America, will offer high-growth opportunities due to improving healthcare infrastructure.

- Strategic collaborations between pharma and tech firms will accelerate innovation in smart diabetes care.

- Environmental sustainability in drug manufacturing and packaging will influence purchasing decisions and compliance.

- Regulatory alignment and faster approval processes will support quicker market entry for new therapies.

- Investments in oral biologics and non-invasive delivery methods will enhance patient convenience and expand therapeutic options.