Autonomous Tractors Market Overview:

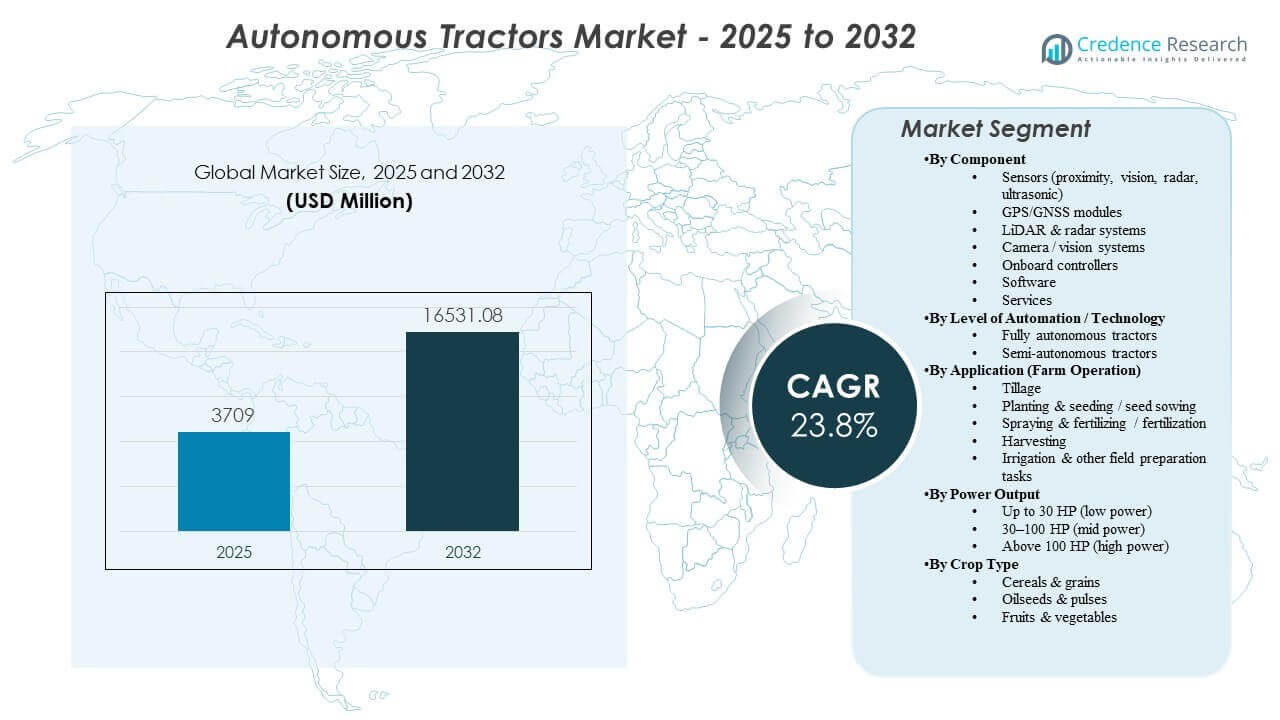

The global Autonomous Tractors Market size was estimated at USD 3709 million in 2025 and is expected to reach USD 16531.08 million by 2032, growing at a CAGR of 23.8% from 2025 to 2032. Demand is being strengthened by farm labor constraints and the need to complete time-sensitive field operations with higher consistency, encouraging adoption of supervised autonomy, retrofit kits, and autonomy-ready tractor platforms. Expansion of precision-ag ecosystems, improving connectivity on farms, and OEM-led commercialization through dealer networks are also supporting wider deployment across multiple farm sizes and crop systems.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Autonomous Tractors Market Size 2025 |

USD 3709 million |

| Autonomous Tractors Market, CAGR |

23.8% |

| Autonomous Tractors Market Size 2032 |

USD 16531.08 million |

Key Market Trends & Insights

- Asia Pacific accounted for the largest regional share of 44.6% in 2025, supported by accelerating mechanization and scaling adoption of precision-ag toolchains.

- Semi-autonomous systems held 66.8% share in 2025, reflecting stronger near-term comfort with supervised autonomy and easier integration into current farm workflows.

- GPS/GNSS modules led the component mix with 35.4% share in 2025, as positioning accuracy remains foundational for repeatable navigation and implement performance.

- Tillage represented 37.2% share in 2025, as straight-line draft work is among the most automation-ready operations for early deployments.

- The market is projected to reach USD 16531.08 million by 2032 from USD 3709 million in 2025, reflecting rapid scaling of autonomy use cases across field operations.

Segment Analysis

Adoption is progressing through a practical path that prioritizes measurable returns and operational reliability. Farms are typically starting with autonomy capabilities that reduce operator workload and extend operating hours during critical windows, then expanding functionality once performance is proven in daily use. Retrofit-led deployment strategies are also widening the addressable base by enabling existing tractor fleets to gain autonomy features without full platform replacement. These dynamics are reinforcing demand for positioning, sensing, and software stacks that deliver repeatable outcomes across variable field conditions.

Technology development is also shifting procurement criteria toward integrated systems rather than standalone features. Buyers increasingly evaluate autonomy packages based on end-to-end performance, including navigation stability, obstacle handling, remote supervision, service coverage, and data workflow integration with existing precision-ag platforms. As more operations adopt multi-machine coordination and standardized digital workflows, interoperability with guidance systems, telematics, and agronomic analytics is becoming a stronger differentiator. This supports growth in software and services alongside hardware attach rates.

By Component Insights

GPS/GNSS modules accounted for the largest share of 35.4% in 2025. Positioning accuracy is a core requirement for repeatable guidance paths, consistent implement overlap control, and reliable execution in tillage, planting, and spraying workflows. GNSS systems also integrate smoothly into established precision-ag ecosystems, supporting faster deployment and operator acceptance. As fleets scale, standardizing positioning hardware simplifies calibration, reduces variability across machines, and improves service efficiency.

By Level of Automation / Technology Insights

Semi-autonomous accounted for the largest share of 66.8% in 2025. Farms are adopting supervised autonomy as a lower-friction pathway that delivers labor productivity benefits while keeping human oversight for edge cases and safety considerations. Semi-autonomous feature sets can be deployed sooner within existing operating practices and dealer support models. The category also benefits from retrofit options that reduce capital barriers and accelerate time-to-value on installed fleets.

By Application (Farm Operation) Insights

Tillage accounted for the largest share of 37.2% in 2025. Tillage is often the first operation to scale because routes are relatively predictable and performance can be validated through measurable outcomes such as coverage consistency and implement depth control. Long operating-hour potential increases the value of autonomy in field-preparation windows where delays cascade into later operations. Confidence built in tillage deployments supports follow-on adoption in higher-complexity tasks such as spraying and planting.

By Power Output Insights

30–100 HP (mid power) accounted for the largest share of 39.6% in 2025. Mid-power tractors align with common mixed-use needs across mid-sized farms and contractors, making the installed base large and commercially attractive for autonomy feature rollouts. This power band balances affordability and capability across multiple farm operations, supporting broader adoption. OEM platforms in this range also tend to have strong dealer coverage and mature attachment ecosystems, easing deployment and serviceability.

By Crop Type Insights

Cereals & grains, oilseeds & pulses, and fruits & vegetables are seeing differing adoption pathways based on field structure, task complexity, and labor intensity. Row-crop systems often provide larger, more uniform fields that simplify navigation and enable repeatable autonomy routes across seasons. Specialty crops can justify autonomy through high labor costs and frequent operations, but require more robust perception and maneuvering capabilities. Crop-specific implement integration and validation pace influence how quickly autonomy moves from supervised workflows to higher automation levels.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising labor constraints and operating-window pressure

Farm labor availability is tightening across many regions, raising the operational cost of completing repetitive field tasks at the required speed and quality. Autonomous and semi-autonomous tractors help farms maintain schedules by reducing dependence on scarce skilled operators. Longer operating hours and consistent execution can be particularly valuable in narrow planting, spraying, and harvest windows. These benefits are driving adoption of supervised autonomy as a near-term solution with a clearer operational fit.

- For instance, John Deere’s autonomous-ready 8R tractor platform has been demonstrated to run up to 30 hours continuously with only brief refueling pauses, enabling around-the-clock tillage and planting while reducing the need for multiple skilled operators in a single shift.

Expansion of precision agriculture ecosystems and data-driven farming

Precision-ag adoption has increased the readiness of farms to integrate autonomy into existing digital workflows. Guidance systems, telematics, and farm management platforms create the data backbone needed for route planning, task recording, and performance verification. Autonomy packages that connect seamlessly with these systems reduce deployment friction and strengthen perceived ROI. As buyers prioritize interoperability, integrated stacks that combine positioning, sensing, and analytics gain preference.

OEM-led commercialization through dealer networks and service models

Large OEMs and established dealer networks reduce adoption risk by providing installation support, training, spare parts coverage, and predictable maintenance pathways. This infrastructure matters because autonomy performance depends on sustained calibration, software updates, and reliable connectivity. Dealer-led commercialization also enables bundled offerings that combine hardware, software, and services into simpler purchase decisions. These dynamics accelerate scaling beyond early adopters into broader farm segments.

Growth of retrofit autonomy pathways and lower-capex adoption

Retrofit solutions enable farms to add autonomy features to existing tractors, reducing the need for complete fleet replacement. This pathway shortens time-to-deployment and improves affordability, especially for cost-sensitive customers. Retrofitting also allows farms to standardize autonomy capability across mixed fleets and extend asset lifecycles. As retrofit performance improves, adoption expands from pilot deployments to scaled rollouts across multiple machines.

- For instance, Sabanto’s Steward retrofit kit has autonomously executed operations such as mowing, spraying, and tillage across multiple U.S. states on platforms including John Deere 5075E and 5100E, Fendt 700 Vario, and Kubota M5 tractors, allowing mixed-brand fleets to standardize autonomy without buying new machines.

Market Challenges

Autonomy deployment faces operational and safety constraints that vary by geography, farm environment, and task complexity. Unpredictable field conditions, variable terrain, weather-driven visibility changes, and obstacles can reduce performance consistency and increase the need for supervision. Liability considerations and cautious operating practices can slow adoption of fully autonomous modes, especially where regulatory guidance is evolving. These factors push buyers to prioritize reliability, support, and clear operating boundaries rather than maximum automation claims.

- For instance, John Deere’s fully autonomous 8R tractor uses six pairs of stereo cameras and a deep neural network that classifies every pixel in approximately 100 milliseconds to enable 360‑degree obstacle detection and keeps the machine within less than an inch of its geofenced boundary, underscoring how high‑precision perception and tight operating envelopes are required to safely manage variable field conditions.

Total cost of ownership remains a key barrier for many farms, particularly where utilization is seasonal or acreage is limited. Autonomy packages often require ongoing spending for connectivity, software subscriptions, updates, and service, which can complicate ROI justification. Integration challenges can also emerge when fleets use mixed brands or legacy precision-ag systems with different data standards. Buyers therefore favor solutions that reduce integration work and provide predictable lifecycle support.

Market Trends and Opportunities

Autonomy is increasingly being packaged as a service-led offering, combining hardware kits with remote monitoring, diagnostics, and performance optimization. This trend supports recurring revenue models for suppliers and reduces operational risk for farms through proactive support. Integrated workflows that link autonomy to agronomic analytics are also gaining momentum, enabling farms to measure coverage quality, reduce overlap, and standardize outcomes across operators and sites. These capabilities strengthen the business case beyond labor savings alone.

Opportunities are expanding in specialized and high-frequency use cases where repeatability and uptime are especially valuable. Farms and contractors are exploring multi-machine coordination, remote supervision, and standardized digital task templates to improve productivity across multiple operations. As sensing costs decline and compute improves, higher-complexity tasks become more feasible, supporting broader application coverage. Suppliers that combine implement integration, robust safety features, and strong service ecosystems are positioned to capture this next wave of deployments.

- For instance, autonomous orchard and vineyard robots for repetitive tasks such as weeding and targeted spraying now operate on tightly scheduled daily cycles, with continuous sensor feedback used to maintain mission uptime and reduce missed rows in perennial crops.

Regional Insights

North America

North America represented 28.3% of the market in 2025, supported by high precision-ag penetration and strong OEM-dealer ecosystems that speed commercialization. Large-acreage farming structures increase the value of labor substitution and extended operating hours during critical field windows. Buyers typically prioritize reliability, service coverage, and integration with existing guidance and telematics stacks. Retrofit pathways also resonate due to the scale of the installed tractor base and the desire to avoid full fleet replacement.

Europe

Europe accounted for 19.6% share in 2025, with adoption supported by high mechanization levels and modernization priorities across commercial farms. Farm fragmentation in parts of the region can influence deployment pace, but strong equipment standards and technology readiness support steady uptake. Demand is linked to productivity improvements, operator availability, and the drive for more consistent operations. Supplier differentiation often depends on safety systems, implement compatibility, and aftersales coverage.

Asia Pacific

Asia Pacific held the largest share at 44.6% in 2025, reflecting broad mechanization momentum and scaling adoption of digital farming tools across diverse agricultural systems. Large and rapidly modernizing farming segments support investment in autonomy to address labor constraints and productivity goals. Adoption pathways often emphasize supervised autonomy first, then expansion as confidence builds in performance and service support. The region’s scale also supports faster diffusion once OEM and local partner ecosystems stabilize.

Latin America

Latin America captured 5.7% share in 2025, driven by large-scale commercial farming where autonomy ROI can be attractive in repetitive field operations. Adoption is supported by the need to maximize operating windows and improve consistency over wide acreages. However, capex cycles, connectivity variability, and service availability can shape adoption speed across countries. Solutions that prove durability and minimize integration complexity are more likely to scale.

Middle East & Africa

Middle East & Africa represented 1.8% share in 2025, reflecting uneven mechanization levels and fewer autonomy-ready large-acreage deployments across much of the region. Adoption is more concentrated in pockets where commercial farming, availability of service infrastructure, and connectivity conditions support advanced equipment use. Buyers emphasize reliability, ease of maintenance, and strong partner support due to operating environment variability. Scalable opportunities improve as mechanization and precision-ag readiness expand.

Competitive Landscape

Competition in the Autonomous Tractors Market is shaped by established OEMs leveraging platform integration, dealer networks, and bundled solutions that combine hardware, software, and services. Large players focus on scaling supervised autonomy and retrofit pathways to broaden adoption across installed fleets, while also advancing fully autonomous capabilities through improved perception, compute, and remote supervision workflows. Specialist firms and technology-focused suppliers compete by offering autonomy stacks, guidance technologies, and integration layers that can accelerate deployment for specific operations. Differentiation increasingly depends on reliability in real farm conditions, interoperability with precision-ag ecosystems, and the strength of aftersales support.

Deere & Company (John Deere) is positioned around an integrated autonomy roadmap that pairs machine platforms with perception, guidance, and software capabilities designed for scalable field deployment. The company’s approach emphasizes practical autonomy use cases that can be validated in core operations and expanded through upgradeable kits and platform-ready designs. Strong dealer coverage supports installation, maintenance, and operator enablement, reducing adoption risk for commercial farms. This combination supports wider rollout across segments that value predictable outcomes, service continuity, and workflow integration.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Deere & Company (John Deere)

- CNH Industrial (Case IH, New Holland)

- AGCO Corporation (Fendt, Massey Ferguson, Valtra)

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- CLAAS KGaA mbH

- Yanmar Holdings Co., Ltd.

- SDF Group (SAME Deutz-Fahr)

- TYM Corporation

- Iseki & Co., Ltd.

- Monarch Tractor

- Trimble Inc.

- Raven Industries, Inc.

- Autonomous Solutions, Inc. (ASI)

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In January 2026, John Deere began field deployment of its next-generation autonomy kit enabling fully driverless operation on 8R and 9RX tractors, building on the CES 2025 launch with upgraded 360-degree stereo camera coverage, longer detection range, and enhanced AI-based obstacle avoidance.

- In January 2026, AGCO Corporation (Fendt) highlighted continued progress and development direction for autonomy and field-robotics concepts supporting farm automation roadmaps. The update reflects sustained OEM focus on expanding autonomy beyond a single machine category into broader automated field operations.

- In June 2025, Kubota North America entered into a strategic collaboration with Agtonomy to commercialize autonomous operations on Kubota diesel tractors, initially focusing on integrating Agtonomy’s autonomy platform with the Kubota M5N tractor for spraying and mowing tasks.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 3,709 million |

| Revenue forecast in 2032 |

USD 16,531.08 million |

| Growth rate (CAGR) |

23.8% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Component Outlook: Sensors (proximity, vision, radar, ultrasonic), GPS/GNSS modules, LiDAR & radar systems, Camera / vision systems, Onboard controllers, Software, Services; By Level of Automation / Technology Outlook: Fully autonomous tractors, Semi-autonomous; By Application (Farm Operation) Outlook: Tillage, Planting & seeding / seed sowing, Spraying & fertilizing / fertilization, Harvesting, Irrigation & other field preparation tasks; By Power Output Outlook: Up to 30 HP (low power), 30–100 HP (mid power), Above 100 HP (high power); By Crop Type Outlook: Cereals & grains, Oilseeds & pulses, Fruits & vegetables |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Deere & Company (John Deere); CNH Industrial (Case IH, New Holland); AGCO Corporation (Fendt, Massey Ferguson, Valtra); Kubota Corporation; Mahindra & Mahindra Ltd.; CLAAS KGaA mbH; Yanmar Holdings Co., Ltd.; SDF Group; TYM Corporation; Iseki & Co., Ltd.; Monarch Tractor; Trimble Inc.; Raven Industries, Inc.; Autonomous Solutions, Inc. (ASI) |

| No. of Pages |

342 |

Segmentation

By Component

- Sensors (proximity, vision, radar, ultrasonic)

- GPS/GNSS modules

- LiDAR & radar systems

- Camera / vision systems

- Onboard controllers

- Software

- Services

By Level of Automation / Technology

- Fully autonomous tractors

- Semi-autonomous

By Application (Farm Operation)

- Tillage

- Planting & seeding / seed sowing

- Spraying & fertilizing / fertilization

- Harvesting

- Irrigation & other field preparation tasks

By Power Output

- Up to 30 HP (low power)

- 30–100 HP (mid power)

- Above 100 HP (high power)

By Crop Type

- Cereals & grains

- Oilseeds & pulses

- Fruits & vegetables

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa