CHAPTER NO. 1 : INTRODUCTION 19

1.1.1. Report Description 19

Purpose of the Report 19

USP & Key Component 19

1.1.2. Key Benefits for Stakeholders 19

1.1.3. Target Audience 20

1.1.4. Report Scope 20

CHAPTER NO. 2 : EXECUTIVE SUMMARY 21

2.1. Geospatial Analytics Market Snapshot 21

2.1.1. Canada Geospatial Analytics Market, 2018 – 2032 (USD Million) 22

CHAPTER NO. 3 : GEOPOLITICAL CRISIS IMPACT ANALYSIS 23

3.1. Russia-Ukraine and Israel-Palestine War Impacts 23

CHAPTER NO. 4 : GEOSPATIAL ANALYTICS MARKET – INDUSTRY ANALYSIS 24

4.1. Introduction 24

4.2. Market Drivers 25

4.2.1. Driving Factor 1 Analysis 25

4.2.2. Driving Factor 2 Analysis 26

4.3. Market Restraints 27

4.3.1. Restraining Factor Analysis 27

4.4. Market Opportunities 28

4.4.1. Market Opportunities Analysis 28

4.5. Porter’s Five Force analysis 29

4.6. Value Chain Analysis 30

4.7. Buying Criteria 31

CHAPTER NO. 5 : ANALYSIS COMPETITIVE LANDSCAPE 32

5.1. Company Market Share Analysis – 2023 32

5.1.1. Canada Geospatial Analytics Market: Company Market Share, by Revenue, 2023 32

5.1.2. Canada Geospatial Analytics Market: Top 6 Company Market Share, by Revenue, 2023 32

5.1.3. Canada Geospatial Analytics Market: Top 3 Company Market Share, by Revenue, 2023 33

5.2. Canada Geospatial Analytics Market Company Revenue Market Share, 2023 34

5.3. Company Assessment Metrics, 2023 35

5.3.1. Stars 35

5.3.2. Emerging Leaders 35

5.3.3. Pervasive Players 35

5.3.4. Participants 35

5.4. Start-ups /Code Assessment Metrics, 2023 35

5.4.1. Progressive Companies 35

5.4.2. Responsive Companies 35

5.4.3. Dynamic Companies 35

5.4.4. Starting Blocks 35

5.5. Strategic Developments 36

5.5.1. Acquisition & Mergers 36

New Product Launch 36

Regional Expansion 36

5.6. Key Players Product Matrix 37

CHAPTER NO. 6 : PESTEL & ADJACENT MARKET ANALYSIS 38

6.1. PESTEL 38

6.1.1. Political Factors 38

6.1.2. Economic Factors 38

6.1.3. Social Factors 38

6.1.4. Technological Factors 38

6.1.5. Environmental Factors 38

6.1.6. Legal Factors 38

6.2. Adjacent Market Analysis 38

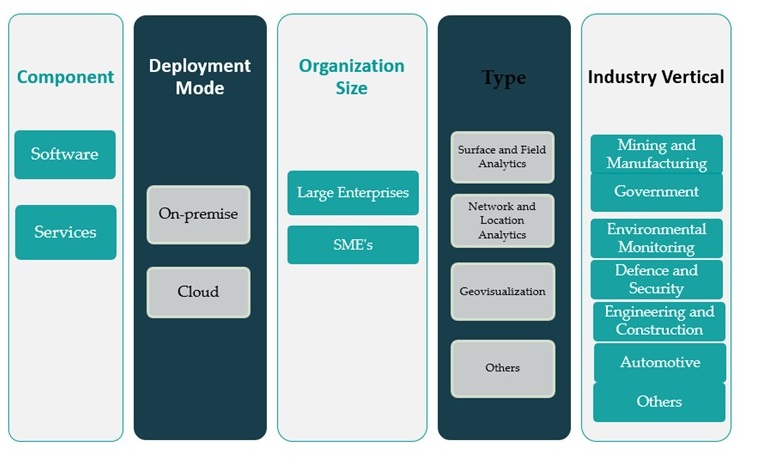

CHAPTER NO. 7 : GEOSPATIAL ANALYTICS MARKET – BY COMPONENT SEGMENT ANALYSIS 39

7.1. Geospatial Analytics Market Overview, by Component Segment 39

7.1.1. Geospatial Analytics Market Revenue Share, By Component, 2023 & 2032 40

7.1.2. Geospatial Analytics Market Attractiveness Analysis, By Component 41

7.1.3. Incremental Revenue Growth Opportunities, by Component, 2024 – 2032 41

7.1.4. Geospatial Analytics Market Revenue, By Component, 2018, 2023, 2027 & 2032 42

7.2. Software 43

7.3. Services 44

CHAPTER NO. 8 : GEOSPATIAL ANALYTICS MARKET – BY DEPLOYMENT MODE SEGMENT ANALYSIS 45

8.1. Geospatial Analytics Market Overview, by Deployment Mode Segment 45

8.1.1. Geospatial Analytics Market Revenue Share, By Deployment Mode, 2023 & 2032 46

8.1.2. Geospatial Analytics Market Attractiveness Analysis, By Deployment Mode 47

8.1.3. Incremental Revenue Growth Opportunities, by Deployment Mode, 2024 – 2032 47

8.1.4. Geospatial Analytics Market Revenue, By Deployment Mode, 2018, 2023, 2027 & 2032 48

8.2. On-premise 49

8.3. Cloud 50

CHAPTER NO. 9 : GEOSPATIAL ANALYTICS MARKET – BY TYPE SEGMENT ANALYSIS 51

9.1. Geospatial Analytics Market Overview, by Type Segment 51

9.1.1. Geospatial Analytics Market Revenue Share, By Type, 2023 & 2032 52

9.1.2. Geospatial Analytics Market Attractiveness Analysis, By Type 53

9.1.3. Incremental Revenue Growth Opportunities, by Type, 2024 – 2032 53

9.1.4. Geospatial Analytics Market Revenue, By Type, 2018, 2023, 2027 & 2032 54

9.2. Surface and Field Analytics 55

9.3. Network and Location Analytics 56

9.4. Geovisualization 57

9.5. Others 58

CHAPTER NO. 10 : GEOSPATIAL ANALYTICS MARKET – BY INDUSTRY VERTICAL SEGMENT ANALYSIS 59

10.1. Geospatial Analytics Market Overview, by Industry Vertical Segment 59

10.1.1. Geospatial Analytics Market Revenue Share, By Industry Vertical, 2023 & 2032 60

10.1.2. Geospatial Analytics Market Attractiveness Analysis, By Industry Vertical 61

10.1.3. Incremental Revenue Growth Opportunities, by Industry Vertical, 2024 – 2032 61

10.1.4. Geospatial Analytics Market Revenue, By Industry Vertical, 2018, 2023, 2027 & 2032 62

10.2. Mining and Manufacturing 63

10.3. Government 64

10.4. Environmental Monitoring 65

10.5. Defence and Security 66

10.6. Engineering and Construction 67

10.7. Automotive 68

10.8. Others 69

CHAPTER NO. 11 : GEOSPATIAL ANALYTICS MARKET – CANADA 70

11.1. Canada 70

11.1.1. Key Highlights 70

11.2. Component 71

11.3. Canada Geospatial Analytics Market Revenue, By Component, 2018 – 2023 (USD Million) 71

11.4. Canada Geospatial Analytics Market Revenue, By Component, 2024 – 2032 (USD Million) 71

11.5. Deployment Mode 72

11.6. Canada Geospatial Analytics Market Revenue, By Deployment Mode, 2018 – 2023 (USD Million) 72

11.6.1. Canada Geospatial Analytics Market Revenue, By Deployment Mode, 2024 – 2032 (USD Million) 72

11.7. Enterprise Size 73

11.8. Canada Geospatial Analytics Market Revenue, By Enterprise Size, 2018 – 2023 (USD Million) 73

11.8.1. Canada Geospatial Analytics Market Revenue, By Enterprise Size, 2024 – 2032 (USD Million) 73

11.9. Type 74

11.10. Canada Geospatial Analytics Market Revenue, By Type, 2018 – 2023 (USD Million) 74

11.10.1. Canada Geospatial Analytics Market Revenue, By Type, 2024 – 2032 (USD Million) 74

11.11. Industry Vertical 75

11.11.1. Canada Geospatial Analytics Market Revenue, By Industry Vertical, 2018 – 2023 (USD Million) 75

11.11.2. Canada Geospatial Analytics Market Revenue, By Industry Vertical, 2024 – 2032 (USD Million) 75

CHAPTER NO. 12 : COMPANY PROFILES 76

12.1. General Electric 76

12.1.1. Company Overview 76

12.1.2. Product Portfolio 76

12.1.3. Swot Analysis 76

12.1.4. Business Strategy 77

12.1.5. Financial Overview 77

12.2. SAP SE 78

12.3. Google, Inc. 78

12.4. Bentley Systems, Incorporated 78

12.5. Alteryx, Inc. 78

12.6. Oracle Corporation 78

12.7. TOMTOM International, Inc 78

12.8. Hexagon AB 78

12.9. MDA Corporation 78

12.10. Trimble, Inc. 78

12.11. Esri 78

12.12. Furgo NV 78

12.13. PlanetLabs 78

12.14. Ouster 78

12.15. Microsoft Corporation 78

12.16. Others 78

]

List of Figures

FIG NO. 1. Canada Geospatial Analytics Market Revenue, 2018 – 2032 (USD Million) 22

FIG NO. 2. Porter’s Five Forces Analysis for Canada Geospatial Analytics Market 29

FIG NO. 3. Value Chain Analysis for Canada Geospatial Analytics Market 30

FIG NO. 4. Company Share Analysis, 2023 32

FIG NO. 5. Company Share Analysis, 2023 32

FIG NO. 6. Company Share Analysis, 2023 33

FIG NO. 7. Geospatial Analytics Market – Company Revenue Market Share, 2023 34

FIG NO. 8. Geospatial Analytics Market Revenue Share, By Component, 2023 & 2032 40

FIG NO. 9. Market Attractiveness Analysis, By Component 41

FIG NO. 10. Incremental Revenue Growth Opportunities by Component, 2024 – 2032 41

FIG NO. 11. Geospatial Analytics Market Revenue, By Component, 2018, 2023, 2027 & 2032 42

FIG NO. 12. Canada Geospatial Analytics Market for Software, Revenue (USD Million) 2018 – 2032 43

FIG NO. 13. Canada Geospatial Analytics Market for Services, Revenue (USD Million) 2018 – 2032 44

FIG NO. 14. Geospatial Analytics Market Revenue Share, By Deployment Mode, 2023 & 2032 46

FIG NO. 15. Market Attractiveness Analysis, By Deployment Mode 47

FIG NO. 16. Incremental Revenue Growth Opportunities by Deployment Mode, 2024 – 2032 47

FIG NO. 17. Geospatial Analytics Market Revenue, By Deployment Mode, 2018, 2023, 2027 & 2032 48

FIG NO. 18. Canada Geospatial Analytics Market for On-premise, Revenue (USD Million) 2018 – 2032 49

FIG NO. 19. Canada Geospatial Analytics Market for Cloud, Revenue (USD Million) 2018 – 2032 50

FIG NO. 20. Geospatial Analytics Market Revenue Share, By Type, 2023 & 2032 52

FIG NO. 21. Market Attractiveness Analysis, By Type 53

FIG NO. 22. Incremental Revenue Growth Opportunities by Type, 2024 – 2032 53

FIG NO. 23. Geospatial Analytics Market Revenue, By Type, 2018, 2023, 2027 & 2032 54

FIG NO. 24. Canada Geospatial Analytics Market for Surface and Field Analytics, Revenue (USD Million) 2018 – 2032 55

FIG NO. 25. Canada Geospatial Analytics Market for Network and Location Analytics, Revenue (USD Million) 2018 – 2032 56

FIG NO. 26. Canada Geospatial Analytics Market for Geovisualization, Revenue (USD Million) 2018 – 2032 57

FIG NO. 27. Canada Geospatial Analytics Market for Others, Revenue (USD Million) 2018 – 2032 58

FIG NO. 28. Geospatial Analytics Market Revenue Share, By Industry Vertical, 2023 & 2032 60

FIG NO. 29. Market Attractiveness Analysis, By Industry Vertical 61

FIG NO. 30. Incremental Revenue Growth Opportunities by Industry Vertical, 2024 – 2032 61

FIG NO. 31. Geospatial Analytics Market Revenue, By Industry Vertical, 2018, 2023, 2027 & 2032 62

FIG NO. 32. Canada Geospatial Analytics Market for Mining and Manufacturing, Revenue (USD Million) 2018 – 2032 63

FIG NO. 33. Canada Geospatial Analytics Market for Government, Revenue (USD Million) 2018 – 2032 64

FIG NO. 34. Canada Geospatial Analytics Market for Environmental Monitoring, Revenue (USD Million) 2018 – 2032 65

FIG NO. 35. Canada Geospatial Analytics Market for Defence and Security, Revenue (USD Million) 2018 – 2032 66

FIG NO. 36. Canada Geospatial Analytics Market for Engineering and Construction, Revenue (USD Million) 2018 – 2032 67

FIG NO. 37. Canada Geospatial Analytics Market for Automotive, Revenue (USD Million) 2018 – 2032 68

FIG NO. 38. Canada Geospatial Analytics Market for Others, Revenue (USD Million) 2018 – 2032 69

FIG NO. 39. Canada Geospatial Analytics Market Revenue, 2018 – 2032 (USD Million) 70

List of Tables

TABLE NO. 1. : Canada Geospatial Analytics Market: Snapshot 21

TABLE NO. 2. : Drivers for the Geospatial Analytics Market: Impact Analysis 25

TABLE NO. 3. : Restraints for the Geospatial Analytics Market: Impact Analysis 27

TABLE NO. 4. : Canada Geospatial Analytics Market Revenue, By Component, 2018 – 2023 (USD Million) 71

TABLE NO. 5. : Canada Geospatial Analytics Market Revenue, By Component, 2024 – 2032 (USD Million) 71

TABLE NO. 6. : Canada Geospatial Analytics Market Revenue, By Deployment Mode, 2018 – 2023 (USD Million) 72

TABLE NO. 7. : Canada Geospatial Analytics Market Revenue, By Deployment Mode, 2024 – 2032 (USD Million) 72

TABLE NO. 8. : Canada Geospatial Analytics Market Revenue, By Enterprise Size, 2018 – 2023 (USD Million) 73

TABLE NO. 9. : Canada Geospatial Analytics Market Revenue, By Enterprise Size, 2024 – 2032 (USD Million) 73

TABLE NO. 10. : Canada Geospatial Analytics Market Revenue, By Type, 2018 – 2023 (USD Million) 74

TABLE NO. 11. : Canada Geospatial Analytics Market Revenue, By Type, 2024 – 2032 (USD Million) 74

TABLE NO. 12. : Canada Geospatial Analytics Market Revenue, By Industry Vertical, 2018 – 2023 (USD Million) 75

TABLE NO. 13. : Canada Geospatial Analytics Market Revenue, By Industry Vertical, 2024 – 2032 (USD Million) 75