Market Overview:

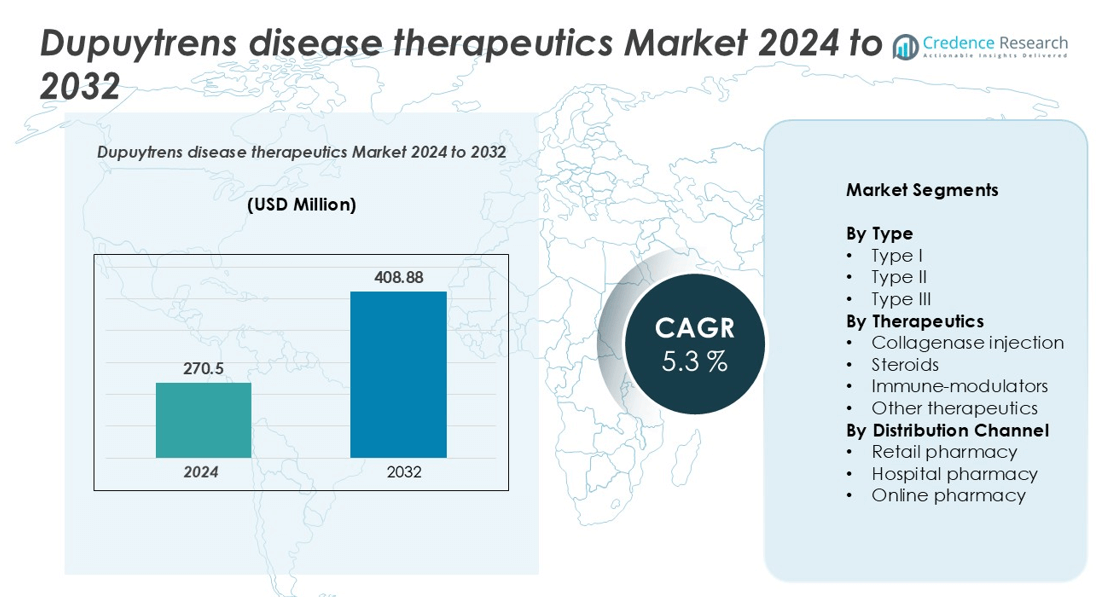

Dupuytren’s Disease Therapeutics Market size was valued at USD 270.5 million in 2024 and is anticipated to reach USD 408.88 million by 2032, at a CAGR of 5.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Dupuytren’s Disease Therapeutics Market Size 2024 |

USD 270.5 million |

| Dupuytren’s Disease Therapeutics Market, CAGR |

5.3% |

| Dupuytren’s Disease Therapeutics Market Size 2032 |

USD 408.88 million |

The Dupuytren’s disease therapeutics market is led by prominent players such as AstraZeneca PLC, GSK plc, Johnson & Johnson, Merck & Co., Inc., Bayer AG, and Bristol-Meyers Squibb Company, alongside emerging participants like Actiza Pharmaceutical Private Limited and Fortress Biotech, Inc. These companies dominate through extensive R&D activities, strong product portfolios, and global distribution networks. North America leads the market with approximately 40% share, driven by advanced healthcare infrastructure and early adoption of minimally invasive therapies. Europe follows with around 30%, supported by favorable reimbursement systems and active clinical development. Asia-Pacific, holding nearly 15%, is rapidly expanding due to improving healthcare access and growing awareness.

Market Insights

- The Dupuytren’s disease therapeutics market was valued at USD 270.5 million in 2024 and is projected to reach USD 408.88 million by 2032, registering a CAGR of 5.3% during the forecast period.

- Market growth is primarily driven by the increasing prevalence of Dupuytren’s disease, early diagnosis rates, and the rising adoption of minimally invasive treatments such as collagenase injections.

- Key trends include advancements in biologic and injectable therapies, expansion of digital pharmacy channels, and increased R&D activities focusing on improved formulations and patient-centric treatment approaches.

- The market is moderately consolidated, with major players like AstraZeneca, GSK, Johnson & Johnson, Merck, and Bayer leading through innovation, strategic collaborations, and strong global distribution networks.

- Regionally, North America holds 40% of the market share, followed by Europe with 30% and Asia-Pacific with 15%, while collagenase injection remains the dominant therapeutic segment, accounting for nearly half of total market revenue.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Type

The Dupuytren’s disease therapeutics market segmented by type includes Type I, Type II, and Type III. Among these, Type I holds the dominant share, accounting for approximately 45% of the market. The high prevalence of early-stage Dupuytren’s disease, coupled with increasing awareness and early diagnosis, drives demand in this sub-segment. Type II and Type III also exhibit steady growth due to rising cases of progressive disease stages. Treatment adoption and improved patient outcomes for early interventions further bolster the Type I segment’s market leadership.

- For instance, Endo’s collagenase clostridium histolyticum (CCH) was approved for Dupuytren’s contracture and offers a less invasive option to surgery. Endo International filed for Chapter 11 bankruptcy in August 2022 due to opioid litigation. A new entity, Endo, Inc., completed the acquisition of substantially all of Endo International’s assets in April 2024, emerging with a strengthened balance sheet.

By Therapeutics

In terms of therapeutics, the market comprises collagenase injections, steroids, immune-modulators, and other therapeutics. Collagenase injection dominates the segment, capturing nearly 50% market share, driven by its minimally invasive nature and proven efficacy in reducing contractures. Steroids and immune-modulators maintain moderate growth, supported by ongoing clinical developments and off-label usage. The increasing preference for non-surgical interventions, coupled with favorable reimbursement policies, further enhances the adoption of collagenase, positioning it as the preferred treatment option for clinicians and patients alike.

- For instance, an article indexed in the National Institutes of Health’s PubMed database described a study that analyzed Dupuytren’s disease treatments in Japan between 2014 and 2020. The study used data from the Japanese government’s National Database of Health Insurance Claims and Specific Health Checkups.

By Distribution Channel

The distribution channel segment includes retail pharmacy, hospital pharmacy, and online pharmacy. Hospital pharmacies lead the market with a share of around 55%, driven by direct physician recommendations, higher treatment adoption rates, and availability of specialized therapeutics. Retail pharmacies show consistent growth, benefiting from prescription refills and accessibility, while online pharmacies are gradually expanding due to convenience and digital healthcare trends. The emphasis on institutional procurement and hospital-based treatment protocols underscores the dominance of hospital pharmacies in this market segment.

Key Growth Drivers

Rising Prevalence and Early Diagnosis

The increasing prevalence of Dupuytren’s disease, particularly among aging populations in Europe and North America, is a primary driver of market growth. Improved awareness and advancements in diagnostic techniques have enabled earlier detection, allowing patients to seek treatment at initial stages of the disease. Early intervention, particularly with minimally invasive therapies like collagenase injections, reduces complications and recurrence, encouraging broader adoption among clinicians. Additionally, screening programs and growing patient education initiatives contribute to higher diagnosis rates. Hospitals and clinics are investing in diagnostic infrastructure to support timely intervention, which directly fuels demand for therapeutics. The combination of rising prevalence, earlier diagnosis, and patient willingness to pursue treatment is accelerating market expansion across all therapeutic sub-segments.

- For instance, a 2010 survey conducted in Flanders, Belgium, found that approximately 32% of individuals over the age of 50 exhibited signs of Dupuytren’s disease, including sub-clinical symptoms.

Increasing Adoption of Minimally Invasive Therapeutics

Minimally invasive treatments, especially collagenase injections, are driving market growth due to their effectiveness, reduced recovery time, and lower risk of complications compared to surgical interventions. Clinicians increasingly prefer these therapies as first-line treatments, supported by clinical evidence demonstrating high success rates in reducing finger contractures. The rising focus on patient convenience, faster rehabilitation, and outpatient procedures has contributed to greater acceptance. Pharmaceutical companies are also expanding their portfolios with improved formulations and delivery methods, enhancing therapeutic outcomes. As patient preference shifts toward non-surgical options, the adoption of collagenase and other injectable therapies continues to propel the market forward, establishing them as dominant treatment options.

- For instance, based on a 2025 study examining the impact of the market withdrawal of collagenase Clostridium histolyticum (CCH) in Japan, CCH injections were a commonly used treatment for Dupuytren’s disease. In 2019, CCH accounted for more than 50% of all treatments in more populated regions of Japan, while accounting for approximately 40% in less populous areas, with the exception of the Tohoku region. Patient preference for this non-surgical option was driven by its minimally invasive nature and faster recovery time.

Favorable Reimbursement and Healthcare Infrastructure

Supportive reimbursement policies and investments in healthcare infrastructure are significantly boosting the market. In developed regions, insurance coverage for Dupuytren’s therapeutics reduces out-of-pocket expenses, making advanced therapies more accessible to patients. Hospitals and specialty clinics are increasingly equipped with treatment facilities for minimally invasive procedures, enhancing patient reach. Government initiatives and private insurance schemes that prioritize chronic and age-related conditions encourage early treatment adoption. Moreover, collaborations between pharmaceutical companies and healthcare providers to expand therapeutic availability in hospitals and clinics are strengthening distribution networks. This combination of financial support and robust healthcare infrastructure sustains market growth and ensures broad patient access.

Key Trends & Opportunities

Expansion of Digital and Online Pharmacy Channels

The rise of digital health solutions and online pharmacies presents a significant opportunity for market growth. Patients increasingly prefer purchasing therapeutics through online platforms due to convenience, home delivery, and access to detailed product information. Telemedicine consultations complement this trend, allowing physicians to prescribe treatments remotely and guide patients on proper administration. Pharmaceutical companies are also exploring direct-to-patient models, enhancing distribution efficiency and patient engagement. This shift not only increases market reach but also supports adherence to therapy, particularly for chronic and long-term conditions like Dupuytren’s disease. The growing integration of digital platforms and telehealth is reshaping distribution strategies, creating a key growth avenue for market players.

- For instance, Endo Pharmaceuticals partnered with Tanner Pharma Group to initiate a multi-year Named Patient Program (NPP) for XIAFLEX®. The program was launched to provide access to XIAFLEX® for patients with Dupuytren’s contracture and Peyronie’s disease in countries. The collaboration began in March 2020, following the withdrawal of the related product XIAPEX® from European markets.

Research and Development of Novel Therapeutics

Ongoing R&D efforts in collagenase formulations, immune-modulators, and steroid-based therapies offer promising growth opportunities. Companies are focusing on enhancing efficacy, minimizing side effects, and developing combination therapies to improve patient outcomes. Clinical trials and innovative delivery mechanisms are expanding the range of treatment options, enabling personalized care. Strategic collaborations between biotech firms and research institutions are accelerating product development and regulatory approvals. The introduction of new therapeutics addressing unmet needs in severe or recurrent cases can attract a larger patient base, driving revenue growth. Continuous innovation in this space represents a critical opportunity to strengthen competitive positioning in the market.

Increasing Awareness and Patient Education

Patient education initiatives highlighting early detection and available treatment options are driving demand for Dupuytren’s therapeutics. Awareness campaigns by healthcare providers and patient advocacy groups emphasize the benefits of minimally invasive treatments, influencing treatment-seeking behavior. Educational programs also reduce stigma associated with the disease, encouraging timely intervention. As patients become more informed, the adoption of advanced therapeutics, including collagenase injections and immune-modulators, rises. Increased awareness not only improves patient outcomes but also fosters loyalty to specific treatment protocols, presenting opportunities for market players to expand their offerings and strengthen brand presence.

Key Challenges

High Cost of Advanced Therapeutics

The high cost associated with minimally invasive treatments, particularly collagenase injections, remains a significant barrier to market growth. Many patients, especially in emerging regions, face affordability issues due to limited insurance coverage or out-of-pocket expenses. This financial constraint can delay treatment initiation or force patients to opt for less effective alternatives. Additionally, the cost of maintaining specialized healthcare infrastructure for administration further adds to the economic burden. Companies need to balance pricing strategies while ensuring access, particularly in cost-sensitive markets, to overcome this challenge and sustain adoption rates.

Limited Awareness in Emerging Regions

In developing countries, low disease awareness and limited access to trained specialists hinder market growth. Patients often present at advanced stages of Dupuytren’s disease, reducing the efficacy of minimally invasive therapeutics. Lack of infrastructure, inadequate physician training, and insufficient patient education further constrain adoption. Overcoming these barriers requires targeted awareness campaigns, physician training programs, and expansion of healthcare facilities. Without addressing these challenges, the potential for market penetration in emerging regions remains limited, restricting overall global growth opportunities for Dupuytren’s disease therapeutics.

Regional Analysis

North America

North America dominates the Dupuytren’s disease therapeutics market, accounting for approximately 40% market share. High prevalence of the disease among the aging population, coupled with advanced healthcare infrastructure, drives adoption of minimally invasive therapies such as collagenase injections. Well-established reimbursement policies, extensive physician awareness, and patient education initiatives further bolster market growth. The presence of leading pharmaceutical companies and ongoing clinical research enhances treatment availability. Additionally, early diagnosis programs and strong hospital networks ensure wide patient reach, making North America the most lucrative region for therapeutic adoption and fostering continuous innovation in treatment options.

Europe

Europe holds around 30% of the global Dupuytren’s disease therapeutics market, driven by increasing incidence among elderly populations and well-developed healthcare systems. Countries like Germany, the UK, and France exhibit high adoption of collagenase injections and other minimally invasive therapies due to favorable reimbursement policies. Awareness campaigns and specialized clinics enhance early diagnosis and treatment. The region benefits from robust research and development activities, expanding therapeutic options and improving patient outcomes. Additionally, Europe’s focus on outpatient care and non-surgical interventions supports consistent demand, positioning it as a key growth region alongside North America.

Asia-Pacific

Asia-Pacific accounts for nearly 15% of the market, exhibiting steady growth due to increasing healthcare investments and improving access to specialized therapeutics. Rising prevalence among aging populations, coupled with growing awareness of Dupuytren’s disease, is driving demand for early intervention. Countries such as Japan, China, and Australia are witnessing increased adoption of minimally invasive treatments supported by hospital expansion and physician training programs. However, affordability and limited insurance coverage in some developing countries pose challenges. Strategic collaborations between international pharmaceutical companies and local healthcare providers are helping expand access, creating significant growth potential for the region.

Latin America

Latin America represents approximately 8% of the Dupuytren’s disease therapeutics market. Market growth is primarily driven by improving healthcare infrastructure, increasing awareness of early-stage interventions, and gradual adoption of minimally invasive treatments. Countries like Brazil and Mexico are witnessing expansion in hospital networks and access to advanced therapeutics. However, limited reimbursement policies and lower patient affordability continue to restrict widespread adoption. Strategic initiatives by pharmaceutical companies, including partnerships with healthcare institutions and educational programs for physicians, are improving treatment accessibility. Increasing urbanization and awareness are expected to gradually enhance the region’s market share over the forecast period.

Middle East & Africa

The Middle East & Africa accounts for around 7% of the global market, with growth fueled by gradual improvements in healthcare infrastructure and increasing adoption of advanced therapeutics. Countries such as Saudi Arabia, UAE, and South Africa are investing in specialty clinics and hospital networks, enabling access to collagenase injections and other therapies. However, market expansion is constrained by limited awareness, insufficient reimbursement coverage, and high treatment costs. Initiatives to enhance physician training and patient education are emerging to address these challenges. The region presents untapped potential, especially in urban centers, offering opportunities for market players to expand their presence.

Market Segmentations:

By Type

By Therapeutics

- Collagenase injection

- Steroids

- Immune-modulators

- Other therapeutics

By Distribution Channel

- Retail pharmacy

- Hospital pharmacy

- Online pharmacy

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Dupuytren’s disease therapeutics market features a moderately consolidated competitive landscape, with key players focusing on product innovation, clinical research, and strategic collaborations to strengthen their market presence. Major companies such as AstraZeneca PLC, GSK plc, Johnson & Johnson, Merck & Co., Inc., and Bayer AG actively invest in research and development to enhance the efficacy and safety of minimally invasive therapies like collagenase injections and immune-modulators. Emerging players including Actiza Pharmaceutical Private Limited and Fortress Biotech, Inc. are expanding their portfolios through partnerships and regional market penetration. Leading manufacturers are emphasizing regulatory approvals, patient-centric formulations, and global distribution expansion to gain competitive advantage. Additionally, mergers and acquisitions are shaping market dynamics, enabling companies to broaden therapeutic applications and improve access in developing markets. The increasing focus on innovation, affordability, and accessibility continues to drive competition and sustain market growth in Dupuytren’s disease therapeutics.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In March 2024, Bristol Myers Squibb completed its acquisition of Karuna Therapeutics, Inc. This strategic move highlights Bristol Myers Squibb’s dedication to expanding its capabilities and advancing innovation in the therapeutic sector.

- In August 3, 2023, 180 Life Sciences Corp., a clinical-stage biotechnology company focused on the development of novel drugs that fulfill unmet needs in inflammatory diseases, fibrosis and pain, announced that it has submitted a request to the U.K.’s Medicines and Healthcare products Regulatory Agency (MHRA) for a follow up scientific advice meeting where the company will seek guidance on a plan to obtain Conditional Marketing Authorization (CMA) for the use of adalimumab in the treatment of early stage Dupuytren’s disease.

- In May 2023, Teva Pharmaceutical Industries Ltd. announced a new strategic framework with four main pillars to position the Company for a new era of growth. This strategy aims to bolster the Company’s strong commercial portfolio with AUSTEDO, AJOVY, UZEDYTM and biosimilars, amplify its innovative pipeline, sustain its generics powerhouse and focus the business.

Report Coverage

The research report offers an in-depth analysis based on Type, Therapeutics, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market is expected to witness steady growth driven by increasing awareness and early diagnosis of Dupuytren’s disease.

- Advancements in minimally invasive therapies will continue to enhance patient outcomes and treatment adoption.

- Pharmaceutical companies will invest more in R&D to develop safer and more effective collagenase formulations.

- Expansion of digital and online pharmacy channels will improve therapeutic accessibility across regions.

- Strategic collaborations between global and regional players will strengthen distribution networks.

- Rising healthcare expenditure in emerging economies will create new growth opportunities.

- Favorable reimbursement policies will support wider adoption of advanced treatment options.

- Ongoing clinical trials will lead to the introduction of novel drug classes and combination therapies.

- The Asia-Pacific region will emerge as a high-potential market due to growing healthcare infrastructure.

- Focus on patient-centric care and personalized treatment approaches will shape future market strategies.