Market Overview:

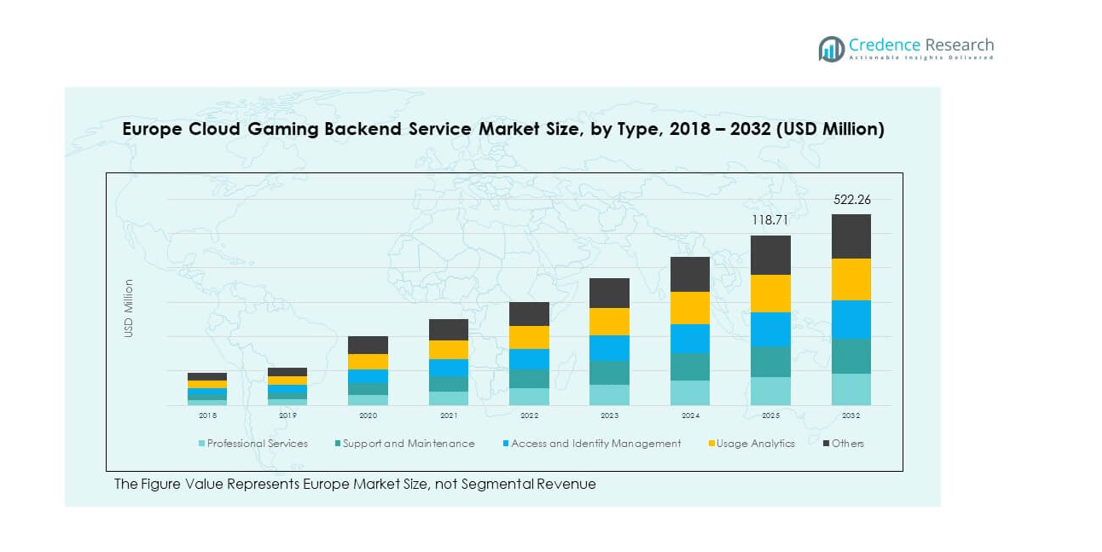

The Europe Cloud Gaming Backend Service Market size was valued at USD 18.05 million in 2018 to USD 96.02 million in 2024 and is anticipated to reach USD 522.26 million by 2032, at a CAGR of 23.60% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Europe Cloud Gaming Backend Service Market Size 2024 |

USD 96.02 million |

| Europe Cloud Gaming Backend Service Market, CAGR |

23.60% |

| Europe Cloud Gaming Backend Service Market Size 2032 |

USD 522.26 million |

The market is driven by rising demand for high-quality gaming experiences without hardware limitations. Cloud gaming backend services enable seamless streaming, reduced latency, and flexible access across multiple devices. Strong broadband penetration, adoption of 5G networks, and growing interest in subscription-based models are further accelerating adoption. Gaming companies are investing in backend infrastructure to meet surging demand for real-time rendering and multiplayer support. Additionally, partnerships between telecom operators and cloud providers are fueling market expansion in Europe.

Geographically, Western Europe leads the Europe Cloud Gaming Backend Service Market, with countries like Germany, the UK, and France at the forefront due to strong digital infrastructure and early adoption of cloud services. Southern and Eastern Europe are emerging markets, showing growth as internet connectivity improves and cloud-based ecosystems expand. Nordic countries also stand out for advanced broadband penetration and high gaming engagement. This geographic diversity highlights both mature and high-potential regions contributing to the overall market’s growth.

Market Insights:

- The Europe Cloud Gaming Backend Service Market was valued at USD 18.05 million in 2018, reached USD 96.02 million in 2024, and is projected to hit USD 522.26 million by 2032, registering a CAGR of 23.60%.

- Western Europe held the largest share of 42% due to robust infrastructure and advanced 5G adoption, followed by Northern Europe at 23% with strong ICT ecosystems, while Southern and Eastern Europe together accounted for 35% with growing connectivity and rising smartphone penetration.

- Southern and Eastern Europe are the fastest-growing subregions with 35% share, fueled by expanding broadband networks, telecom investments, and increasing demand for affordable gaming access.

- By type, professional services dominated with 34% of market share in 2024, driven by deployment and optimization needs.

- Usage analytics accounted for 21% in 2024, reflecting rising demand for player behavior tracking and performance optimization across backend systems.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Broadband Penetration and 5G Expansion Supporting Cloud Gaming Backend Growth

The growing broadband penetration across Europe, combined with the rollout of 5G networks, has strengthened the foundation for cloud gaming services. The availability of high-speed internet reduces latency, enabling smooth gameplay and advanced graphics rendering on multiple devices. Telecom providers are collaborating with gaming companies to deliver stable connections, which is essential for large-scale multiplayer environments. Consumer expectations for low-latency streaming experiences have encouraged operators to prioritize backend service reliability. Strong digital infrastructure in developed markets has made early adoption possible, while emerging regions are now catching up. Cloud service providers are optimizing data centers to manage high gaming workloads and ensure quality performance. This improvement in infrastructure creates favorable conditions for the Europe Cloud Gaming Backend Service Market.

- For example, Vodafone Germany enabled 5G standalone (SA) across over 16,000 mobile stations, extending 5G coverage to around 92% of the population with standalone coverage above 90%, targeting 95% by mid-2025. The network supports speeds exceeding 1,000 Mbps via frequency aggregation, enabling high-bandwidth applications such as mobile gaming and AR/VR.

Shift Toward Subscription-Based Gaming Models Accelerating Backend Service Demand

Gaming behavior in Europe has shifted from physical game ownership to subscription-driven models that offer affordable access. Consumers prefer streaming platforms that provide an extensive game library, eliminating the need for expensive hardware. This transformation has created high demand for backend services that support content delivery and user management. Service providers are investing in scalable backend infrastructure to meet rising subscriber volumes. The growth of platforms offering monthly access to popular titles has strengthened reliance on backend architecture. It ensures data synchronization, content storage, and real-time gameplay. The Europe Cloud Gaming Backend Service Market benefits from this trend as more users adopt cloud-based subscription packages. It reinforces backend service development by ensuring continuous engagement with a large user base.

- For example, Ubisoft+ likely served around 1.8 to 2 million subscribers as of early 2025, according to industry estimates. Ubisoft’s global player base reached 134 million unique active players during the fiscal year ending March 2025.

Increased Consumer Interest in Cross-Device Compatibility Fueling Adoption of Backend Services

Consumers increasingly demand seamless gaming experiences across smartphones, tablets, PCs, and consoles, raising backend requirements. The market is responding with systems that synchronize user progress across platforms without interruptions. This capability enhances player retention and loyalty, making backend services critical for ecosystem stability. Developers focus on backend frameworks that integrate authentication, real-time data handling, and performance optimization. It creates opportunities for service providers to differentiate with flexible solutions. Multi-device adoption also drives the demand for security measures embedded within backend platforms. The Europe Cloud Gaming Backend Service Market is supported by this multi-device gaming culture. It highlights the importance of versatile backend systems to maintain consistency across platforms.

Strategic Partnerships Between Telecom Operators and Cloud Service Providers Expanding Ecosystem

Strategic collaborations between telecom operators and cloud service providers have accelerated backend service availability in Europe. Telecom firms leverage existing customer bases and high-capacity networks to deliver cloud gaming bundles. Backend providers integrate with these ecosystems to support game hosting, analytics, and customer management. This cooperation ensures scalable solutions for growing user demand. It also improves accessibility for gamers in regions previously limited by infrastructure challenges. Telecom-backed platforms rely on backend expertise for stable delivery and continuous optimization. The Europe Cloud Gaming Backend Service Market benefits directly from these partnerships, strengthening competitive positioning. It establishes a foundation for sustained growth and wider adoption of cloud gaming services.

Market Trends:

Expansion of Edge Computing Enhancing Backend Efficiency and Reducing Latency

Edge computing deployment is reshaping backend performance for cloud gaming in Europe. Service providers are placing data servers closer to users, which lowers latency and improves real-time responsiveness. Gamers benefit from smoother experiences with reduced delays, especially in multiplayer scenarios. Providers enhance backend efficiency by balancing loads across distributed networks. It ensures stable access in both urban and rural regions. Edge computing also helps optimize bandwidth consumption by processing data locally. The Europe Cloud Gaming Backend Service Market is witnessing strong adoption of this approach, reflecting the industry’s focus on reliability. It positions edge computing as a key enabler for future gaming infrastructure.

AI and Analytics Integration Strengthening Backend Performance and Personalization

The integration of artificial intelligence and analytics tools has transformed backend services across the gaming industry. Providers use AI to monitor server loads, predict demand spikes, and optimize resource allocation. This proactive approach prevents downtime and enhances service reliability. Analytics platforms assess user behavior to deliver personalized gaming experiences. It also allows developers to fine-tune game features and monetization models. AI-driven backend systems create adaptive infrastructures that respond to shifting player demands. The Europe Cloud Gaming Backend Service Market incorporates these tools to maintain performance standards. It illustrates the growing influence of AI in shaping backend strategies.

Rising Adoption of Cloud-Native Development Models Boosting Flexibility in Backend Systems

Cloud-native development practices are gaining ground in Europe’s gaming industry, offering agility in backend design. Microservices-based architectures allow developers to scale individual components without affecting the entire system. This flexibility ensures faster updates, bug fixes, and feature releases. It reduces dependency on monolithic structures, enabling quick adaptation to market changes. The Europe Cloud Gaming Backend Service Market reflects this trend, with providers investing in cloud-native ecosystems. Developers benefit from containerization, which supports efficient workload distribution. It ensures backend resilience and improves overall gaming service delivery. Cloud-native adoption has become a defining trend for scalable and reliable backend solutions.

- For example, Microsoft Azure PlayFab showcases AI and analytics integration in gaming backend services. It provides dynamic scaling for multiplayer servers while maintaining high reliability across global deployments. With real-time analytics and AI-driven resource management, PlayFab enhances matchmaking, optimizes performance, and delivers personalized gaming experiences.

Growth of Social Gaming Features Driving Backend Service Enhancements

Social engagement has become a defining aspect of modern gaming in Europe, increasing backend demands. Gamers expect interactive features such as chat, live streaming, and in-game communities. These features require robust backend platforms capable of real-time data synchronization. It highlights the growing role of backend services in supporting immersive social experiences. Developers prioritize backend systems that handle increased traffic during peak engagement. The Europe Cloud Gaming Backend Service Market is responding to this trend by integrating social functionality at scale. It strengthens user loyalty by combining entertainment with social connectivity. This shift enhances both player satisfaction and platform competitiveness.

- For example, Discord demonstrates backend scalability in supporting large-scale social gaming engagement. The platform has more than 350 million registered users and around 150 million monthly active users. Its infrastructure reliably manages peak concurrent loads exceeding 10 million, enabling real-time voice, chat, and streaming features that strengthen global community interaction and player loyalty.

Market Challenges Analysis:

Infrastructure Variability and Latency Concerns Across Regions

Infrastructure variability across European regions creates challenges for consistent service delivery. Developed countries enjoy strong digital frameworks, while less connected regions face limitations in broadband speed and coverage. It restricts smooth gaming access and creates disparities in adoption rates. Latency remains a critical barrier, especially for real-time multiplayer environments requiring rapid responsiveness. Service providers must address these gaps to maintain user satisfaction. Backend optimization strategies often require heavy investment, limiting smaller firms from competing effectively. The Europe Cloud Gaming Backend Service Market continues to face these challenges, reflecting the need for balanced infrastructure development. It highlights the difficulty of achieving uniform adoption across diverse markets.

Rising Operational Costs and Data Privacy Concerns Limiting Market Expansion

The operational cost of maintaining scalable backend services has increased significantly. Providers must invest in data centers, energy-efficient infrastructure, and security frameworks to meet demand. It creates financial pressure, especially for mid-tier firms competing against established players. Compliance with European data protection laws adds another layer of complexity. Strict regulations require providers to ensure secure handling of personal information. The Europe Cloud Gaming Backend Service Market experiences constraints from these cost and compliance factors. It raises concerns about market expansion speed and profitability. Addressing cost efficiency and trust remains central to overcoming these market challenges.

Market Opportunities:

Increasing Demand for Emerging Gaming Ecosystems Creating New Revenue Streams

The growing appeal of cloud-based gaming ecosystems across Europe creates new revenue opportunities. Rising consumer interest in cross-platform access enables backend providers to expand their service portfolios. It positions them to cater to publishers, telecom operators, and technology firms seeking scalable infrastructure. Emerging markets within Europe offer fresh growth potential as digital access expands. Backend services that support immersive technologies such as AR and VR hold strong promise. The Europe Cloud Gaming Backend Service Market is well placed to benefit from this consumer demand. It reinforces opportunities for innovation and diversification in service offerings.

Integration of Advanced Technologies Enabling Differentiated Cloud Gaming Experiences

The integration of advanced technologies into backend frameworks presents a strong opportunity for providers. AI, blockchain, and advanced analytics are shaping unique models of user engagement. It strengthens operational efficiency while supporting personalized experiences and secure transactions. Cloud platforms that leverage these tools can enhance loyalty and improve service reliability. Developers gain from differentiated service offerings that set them apart in competitive landscapes. The Europe Cloud Gaming Backend Service Market gains momentum from such technology-driven opportunities. It demonstrates how backend innovation can support sustainable growth and strengthen industry competitiveness.

Market Segmentation Analysis:

By type, professional services hold a significant role in ensuring the smooth deployment of backend solutions. Enterprises rely on consulting, integration, and managed services to optimize performance and align operations with strategic goals. Support and maintenance contribute by offering continuous system reliability and timely updates. Access and identity management is essential for secure user authentication, safeguarding data, and managing privacy compliance. Usage analytics enhances decision-making by tracking player behavior and system efficiency, creating value for both providers and developers. Others, including custom backend tools, extend flexibility for niche requirements and tailored solutions. The Europe Cloud Gaming Backend Service Market benefits from this diverse range of service offerings that address distinct operational and security needs. It strengthens the foundation for scalable growth across different environments.

- For instance, Accenture in 2025 expanded its AI Refinery platform in Europe integrating sovereign AI architectures and data-residency compliant cloud solutions, enabling AI deployments for critical industries with detailed observability and control facilitating secure backend services for large enterprise clients and public institutions

By end-user, small and medium enterprises are adopting backend services to reduce infrastructure costs and expand market reach. Cloud platforms provide SMEs with affordable access to advanced tools, enabling competitive positioning in the gaming ecosystem. Large enterprises dominate due to extensive resources, broader user bases, and established infrastructure. They demand advanced backend frameworks capable of handling high traffic volumes, advanced security, and cross-device integration. It enables them to deliver consistent and premium gaming experiences across regions. The Europe Cloud Gaming Backend Service Market reflects this dual adoption pattern, where SMEs drive new opportunities while large enterprises consolidate leadership. It creates a balanced structure that fuels both innovation and market stability.

- For instance, Quasr, a European CIAM platform, specializes in passwordless and privacy-friendly identity solutions widely adopted by SMEs for secure, user-centric access management, with flexible integrations that enhance login efficiency and data protection compliance.

Segmentation:

By Type

- Professional Services

- Support and Maintenance

- Access and Identity Management

- Usage Analytics

- Others

By End-User

- Small and Medium Enterprises

- Large Enterprises

Regional Analysis:

Western Europe dominates the Europe Cloud Gaming Backend Service Market with a market share of 42%. Strong digital infrastructure, widespread 5G coverage, and advanced broadband networks support seamless gaming experiences across the region. Countries such as Germany, the UK, and France lead adoption due to high demand for premium gaming services and strong investment in cloud technologies. Large enterprises and telecom operators in these markets continue to expand backend frameworks to handle increasing user traffic. It reinforces Western Europe’s leadership position by combining consumer readiness with technological maturity. The subregion remains the central hub for innovation and large-scale deployment of cloud gaming platforms.

Northern Europe accounts for 23% of the market, driven by high internet penetration and strong interest in gaming across the Nordic countries. Denmark, Sweden, and Finland demonstrate rapid adoption, supported by advanced ICT ecosystems and digitally engaged populations. Cloud-native models are being integrated into backend services to improve agility and efficiency in delivery. The growing popularity of subscription-based gaming services in this subregion further strengthens demand for backend solutions. It highlights Northern Europe as a key contributor to market innovation, with companies leveraging technology to meet evolving consumer expectations. The region demonstrates how smaller but highly advanced economies can shape broader industry trends.

Southern and Eastern Europe together represent 35% of the market, showing strong growth potential as digital infrastructure improves. Italy, Spain, and Poland are emerging hotspots where better connectivity and rising smartphone adoption support market expansion. Investment from telecom providers and partnerships with cloud platforms are unlocking new opportunities for backend development. It reflects the growing appetite for affordable gaming access and scalable backend frameworks among both SMEs and large enterprises. Russia and other parts of Eastern Europe are contributing with a gradual but steady uptake in cloud gaming ecosystems. The Europe Cloud Gaming Backend Service Market benefits from these developments, underscoring the importance of emerging economies in creating balanced regional growth.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- NVIDIA GeForce Now

- Blacknut

- Shadow (Blade SAS)

- Ubitus

- Google Cloud Platform

- Amazon Web Services (AWS)

- Microsoft Azure

- IBM Cloud

- Scaleway

- GameSparks

Competitive Analysis:

The Europe Cloud Gaming Backend Service Market is highly competitive, with global technology leaders and regional specialists shaping its structure. Major players such as NVIDIA GeForce Now, Google Cloud Platform, Amazon Web Services, and Microsoft Azure dominate through strong infrastructure, advanced backend frameworks, and established client bases. Their focus remains on delivering low-latency services, secure identity management, and scalable usage analytics. It gives them a distinct advantage in addressing the complex requirements of large enterprises and telecom operators. Regional providers like Blacknut, Shadow, Ubitus, and Scaleway contribute by offering tailored solutions for niche markets and specific customer segments. Competition is driven by innovation in backend optimization, edge computing integration, and AI-based service personalization. Strategic partnerships with telecom operators and gaming publishers are central to expanding market reach and improving consumer engagement. Companies invest in data center expansions and cross-device compatibility to attract both small and medium enterprises and large enterprises. The Europe Cloud Gaming Backend Service Market reflects a mix of global dominance and regional specialization, ensuring both standardization and adaptability.

Recent Developments:

- In August 2025, Samsung Electronics announced the expansion of its mobile cloud gaming platform into the European market, starting with a beta launch in the United Kingdom and Germany. This move allows Galaxy device users in these countries to instantly stream mobile games without downloads or installations, lowering the barriers to accessing quality titles and demonstrating Samsung’s commitment to making gaming more accessible and social for consumers across Europe.

- In August 2025, NVIDIA introduced its largest upgrade yet by bringing the Blackwell RTX architecture to GeForce NOW in Europe. This rollout delivers RTX 5080-class cloud gaming performance, enabling 5K resolution at 120 fps and integrating new features such as Install-to-Play, which significantly expands the GeForce NOW cloud game library.

- In June 2025, NVIDIA entered additional publisher partnerships that added over 25 new titles to GeForce NOW in North America, reflecting the company’s continued collaboration-oriented growth in the backend gaming service space.

- In March 2025, Xsolla and AWS entered into a key partnership designed to empower game developers with the latest advancements in cloud gaming and LiveOps solutions. The collaboration leverages AWS’s cloud infrastructure and Xsolla’s developer platform to create scalable, flexible backend solutions, further strengthening their positions in the expanding global cloud gaming backend service sector.

Report Coverage:

The research report offers an in-depth analysis based on type and end-user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Growing demand for high-quality gaming experiences will drive the need for advanced backend frameworks.

- Expansion of 5G and broadband networks will enhance service delivery and user accessibility.

- Integration of AI and analytics will strengthen personalization and improve backend efficiency.

- Partnerships between telecom providers and cloud platforms will accelerate adoption across regions.

- Cross-device compatibility will remain a critical factor shaping backend development strategies.

- Subscription-based gaming services will create steady demand for scalable backend systems.

- Edge computing deployment will reduce latency and support seamless real-time experiences.

- SMEs will increase adoption, creating opportunities for cost-effective backend solutions.

- Large enterprises will continue to dominate, leveraging advanced infrastructure for wide-scale operations.

- Regional growth in Southern and Eastern Europe will expand the overall market footprint.