Market Overview

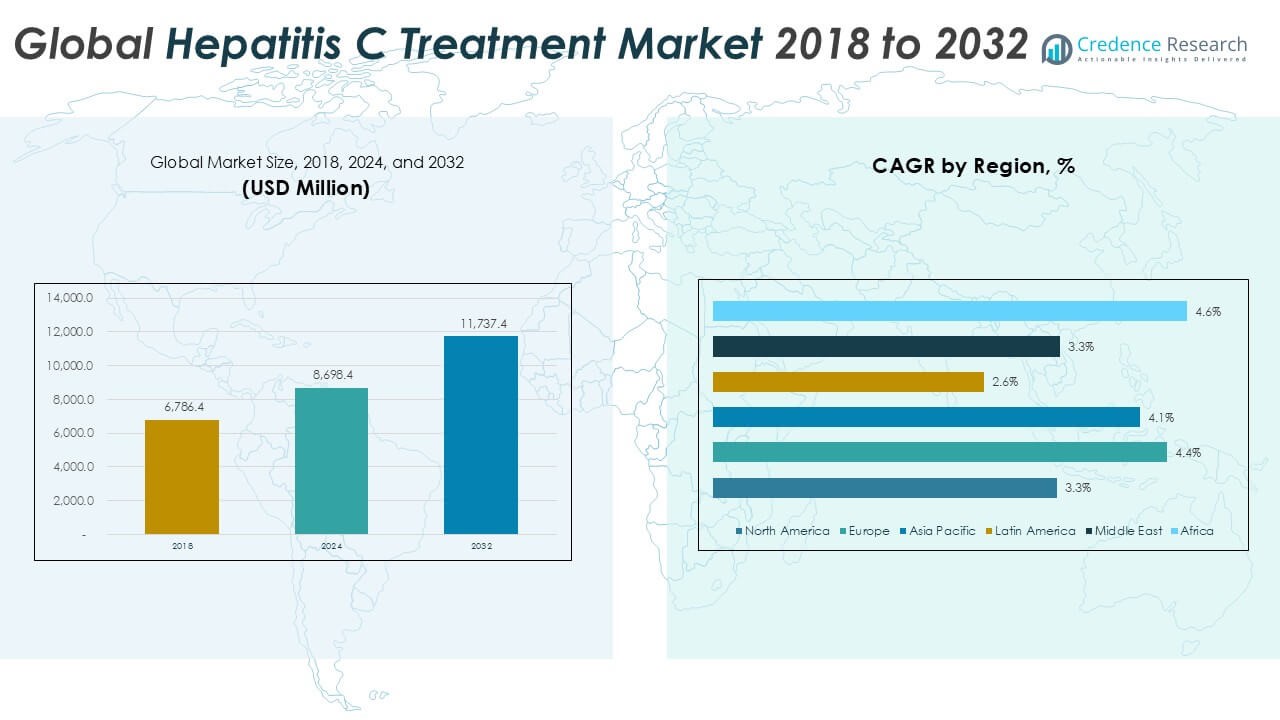

The Global Hepatitis C Treatment Market is projected to grow from USD 8,698.4 million in 2024 to an estimated USD 11,737.4 million by 2032, with a compound annual growth rate (CAGR) of 3.80% from 2025 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Hepatitis C Treatment Market Size 2024 |

USD 8,698.4 Million |

| Hepatitis C Treatment Market, CAGR |

3.80% |

| Hepatitis C Treatment Market Size 2032 |

USD 11,737.4 Million |

Key market drivers include the expanding global burden of hepatitis C, particularly in low- and middle-income countries, and ongoing efforts to eliminate the disease as a public health threat. Governments and NGOs are investing in accessible treatment programs, while pharmaceutical companies are intensifying research to develop next-generation therapies with higher cure rates. The market also benefits from trends such as improved access to generics, integration of digital health tools for patient management, and combination therapies offering simplified treatment regimens.

Geographically, North America holds the largest market share due to the region’s advanced healthcare infrastructure, strong reimbursement policies, and high awareness levels. Europe follows closely, supported by favorable regulatory policies and national hepatitis elimination plans. Meanwhile, the Asia-Pacific region is expected to witness the fastest growth over the forecast period, driven by increasing government initiatives, large patient populations, and expanding healthcare access. Key players in the global hepatitis C treatment market include Gilead Sciences, AbbVie Inc., Merck & Co., Bristol-Myers Squibb, and Roche.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Global Hepatitis C Treatment Market is projected to grow from USD 8,698.4 million in 2024 to USD 11,737.4 million by 2032, at a CAGR of 3.80% between 2025 and 2032.

- Rising awareness, early diagnosis initiatives, and effective direct-acting antivirals are key contributors to market expansion.

- Growing investments from governments and NGOs in accessible treatment programs are accelerating therapy adoption worldwide.

- High treatment costs and limited access to modern therapies in low-income regions continue to restrict market penetration.

- North America dominates the market due to advanced healthcare systems and high public health awareness.

- Asia Pacific is expected to witness the fastest growth, supported by large patient populations and expanding healthcare infrastructure.

- Market growth is hindered by low diagnosis rates, social stigma, and inconsistent healthcare regulations in developing regions.

Market Drivers

Rising Global Prevalence and Improved Screening Initiatives Accelerate Treatment Demand

The Global Hepatitis C Treatment Market is significantly driven by the growing number of individuals infected with the hepatitis C virus (HCV), particularly in developing nations. Increasing government-led awareness campaigns and routine screening programs have helped identify more cases at earlier stages. With early detection, the need for timely and effective treatment becomes more urgent. Public health bodies such as the WHO have pushed for global elimination targets, prompting countries to expand screening access. High prevalence in regions such as Asia-Pacific and the Middle East fuels the demand for scalable treatment programs. It strengthens the need for both branded and generic medications across different patient demographics.

- For instance, the World Health Organization reported in 2024 that over 58,000,000 people worldwide were living with chronic hepatitis C infection, and more than 9,000,000 individuals received HCV screening in national programs that year.

Advancements in Direct-Acting Antivirals Enhance Treatment Outcomes

Innovations in pharmaceutical research have led to the development of direct-acting antivirals (DAAs) that offer higher cure rates with shorter treatment durations. These medications have revolutionized the standard of care by minimizing side effects and reducing treatment failure. The introduction of pan-genotypic regimens simplifies prescribing, making treatment accessible in both specialized and general healthcare settings. It supports broader clinical adoption and increases treatment coverage across multiple geographies. Pharmaceutical companies continue to invest in refining DAA therapies to improve tolerability and effectiveness. Patent expirations also open doors for affordable generic options that support market expansion.

- For instance, Gilead Sciences reported distributing over 2,500,000 courses of its sofosbuvir-based DAAs globally in 2024, including significant shipments to public health programs in India, Egypt, and Brazil.

Government and NGO Funding Strengthens Access to Affordable Therapies

Public and private health agencies play a crucial role in expanding access to hepatitis C therapies in low- and middle-income countries. Governments collaborate with pharmaceutical firms to secure cost-effective drugs through licensing agreements and subsidy programs. Global health organizations fund mass treatment initiatives, especially in high-burden regions. It creates a favorable environment for large-scale treatment rollouts and drives higher patient compliance. Policy frameworks also aim to integrate hepatitis C treatment into national health insurance schemes. These factors collectively reinforce steady market growth and treatment outreach.

Strategic Partnerships and Regional Manufacturing Boost Market Penetration

Leading pharmaceutical companies engage in partnerships with regional players to expand their reach and reduce supply chain barriers. Local manufacturing capabilities improve affordability and ensure consistent drug availability in underserved regions. It helps mitigate the impact of logistical challenges and fluctuating import costs. Strategic licensing agreements allow for rapid market entry of generic versions in cost-sensitive economies. These efforts increase access while maintaining treatment quality standards. Companies also focus on collaborative distribution models to streamline operations and enhance regional market penetration.

Market Trends

Advancements in Direct-Acting Antivirals Are Transforming Treatment Protocols

The Global Hepatitis C Treatment Market has experienced a paradigm shift with the development of direct-acting antivirals (DAAs). These drugs target specific proteins in the hepatitis C virus and disrupt its replication cycle. DAAs have significantly improved cure rates, shortened treatment durations, and reduced side effects compared to older therapies like interferon-based regimens. Pharmaceutical companies continue to invest in enhancing DAA formulations to cover more genotypes and improve tolerability. Simplified, once-daily oral regimens have improved patient compliance and broadened adoption. It strengthens treatment accessibility across both developed and developing regions.

- For instance, in 2024, over 2,300,000 hepatitis C patients worldwide were treated with direct-acting antiviral therapies, according to pharmaceutical company treatment registries and international health agency reports.

Increasing Screening and Diagnosis Rates Are Driving Treatment Uptake

Governments and health agencies worldwide have prioritized early screening and diagnosis of hepatitis C to reduce disease burden. Expanded access to diagnostic tools and integration of hepatitis testing into routine health check-ups support this objective. The market benefits from targeted testing among high-risk populations, including intravenous drug users and patients with co-infections. It boosts early treatment initiation and improves outcomes. National awareness campaigns and global elimination goals are pushing healthcare systems to increase diagnosis rates. The Global Hepatitis C Treatment Market reflects growing demand tied directly to proactive screening strategies.

- For instance, in 2024, government health programs in the United States and Europe conducted more than 18,000,000 hepatitis C screening tests, leading to a substantial increase in new diagnoses and early treatment initiations, as documented in public health surveillance data and official reports.

Widening Access to Generic Medications Strengthens Market Expansion

The availability of generic hepatitis C drugs has made treatment more affordable, especially in low- and middle-income countries. Governments and global organizations have facilitated voluntary licensing agreements with pharmaceutical manufacturers to produce low-cost alternatives. These efforts help improve drug accessibility while maintaining quality standards. It supports large-scale public health interventions and treatment coverage in high-prevalence regions. The Global Hepatitis C Treatment Market is expanding into underserved markets through the wider adoption of generics. Cost-effective therapies are now integral to national hepatitis elimination programs.

Collaborations and Funding Initiatives Support Market Growth in Emerging Regions

Public-private partnerships and multilateral funding initiatives are playing a key role in scaling up treatment infrastructure. Organizations like the WHO and UNITAID are working with local governments to implement widespread treatment campaigns. Collaborative efforts help reduce the financial burden on national health systems and ensure steady drug supplies. It enhances healthcare provider training and streamlines patient care delivery. The Global Hepatitis C Treatment Market benefits from these joint programs, particularly in countries with limited resources. Partnerships also encourage technology transfer and local manufacturing to support long-term treatment goals.

Market Challenges

High Treatment Costs and Limited Access in Low-Income Regions Restrict Market Penetration

The Global Hepatitis C Treatment Market faces significant challenges due to the high cost of direct-acting antivirals and limited access in low- and middle-income countries. Despite the availability of generics, pricing disparities across regions prevent uniform adoption. Many healthcare systems lack the financial resources or reimbursement frameworks to cover the full course of treatment. Weak infrastructure and insufficient diagnostic capabilities delay timely interventions. The market struggles to reach rural and underserved populations where awareness and healthcare delivery remain poor. Without equitable access, global efforts to control and eliminate hepatitis C remain fragmented.

- For instance, the initial price of a 12-week course of sofosbuvir, a widely used direct-acting antiviral, exceeded 80,000 units in the United States, while some low- and middle-income countries have managed to negotiate prices as low as 60 units per patient for generic versions. However, over 70 million people worldwide remain untreated, with the lowest access rates reported in regions such as Africa and Central America, highlighting the persistent disparities in treatment availability and affordability

Stigma, Low Diagnosis Rates, and Regulatory Barriers Undermine Treatment Efforts

It continues to face obstacles from social stigma, inadequate awareness, and insufficient screening efforts, leading to low diagnosis rates in many regions. Patients often delay seeking treatment due to fear, misinformation, or lack of knowledge about available therapies. Regulatory challenges, such as delayed drug approvals and inconsistent healthcare policies, slow down market expansion. Variability in national treatment guidelines creates confusion and hinders standardization. Some regions experience gaps in physician training or resistance to adopting newer therapies. The Global Hepatitis C Treatment Market must address these systemic issues to ensure effective and sustainable growth.

Market Opportunities

Expansion of Screening Programs and Rising Awareness Present Significant Growth Opportunities

The Global Hepatitis C Treatment Market benefits from expanding screening initiatives and growing public awareness worldwide. Governments and health organizations increasingly prioritize early detection, which drives demand for effective therapies. Improved diagnostic technologies support large-scale screening campaigns, enabling earlier intervention and better patient outcomes. Increased awareness campaigns help reduce stigma and encourage more individuals to seek testing and treatment. It creates an environment conducive to higher treatment adoption rates. The integration of hepatitis C screening into routine healthcare protocols opens new avenues for market growth, especially in emerging economies.

Development of Next-Generation Therapies and Strategic Collaborations Enhance Market Potential

Innovations in antiviral therapies, including pan-genotypic regimens and shorter treatment durations, offer significant market opportunities. Pharmaceutical companies focus on enhancing drug efficacy and patient compliance to capture a larger share. Strategic collaborations between governments, NGOs, and industry players improve access to affordable medications, particularly in resource-limited settings. Technology transfer and local manufacturing agreements help reduce costs and ensure steady supply chains. It enables rapid market penetration and supports global elimination goals. The Global Hepatitis C Treatment Market stands to gain from these advancements and partnerships in the coming years.

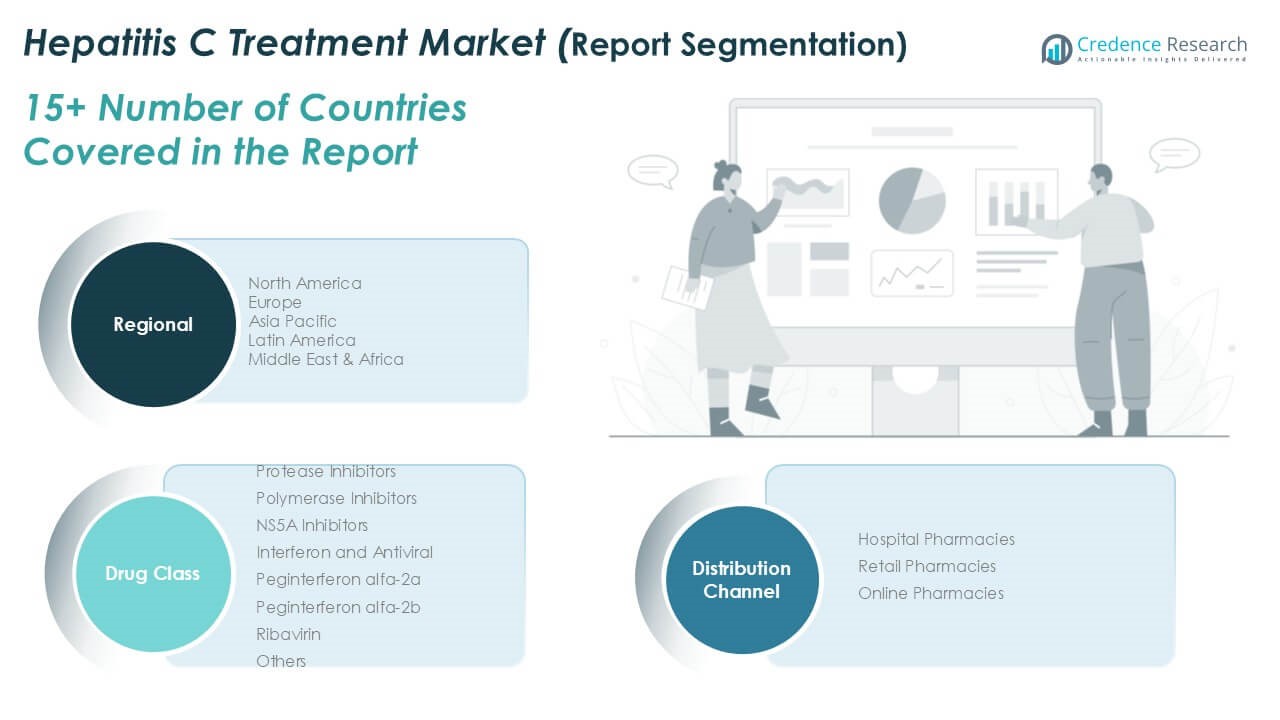

Market Segmentation Analysis

By Drug Class

The Global Hepatitis C Treatment Market is segmented into protease inhibitors, polymerase inhibitors, NS5A inhibitors, interferon and antiviral therapies, and others. Among these, NS5A inhibitors hold a significant market share due to their broad-spectrum antiviral activity and ability to suppress viral replication across genotypes. Protease and polymerase inhibitors also contribute notably, often forming part of combination therapies that improve treatment efficacy and reduce resistance. Interferon-based treatments, including Peginterferon alfa-2a, Peginterferon alfa-2b, and Ribavirin, have witnessed declining usage due to their side effects and the rise of direct-acting antivirals. However, they still serve as options in certain cases or regions where newer therapies are less accessible. It continues to evolve as pharmaceutical companies introduce more effective regimens tailored for shorter treatment durations and fewer side effects.

- For instance, in 2023, more than 2.5 million treatment courses containing NS5A inhibitors were dispensed globally, while interferon-based therapies accounted for fewer than 200,000 treatment courses in the same year according to pharmaceutical industry data and government health reports.

By Distribution Channel

The market is categorized into hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacies dominate the distribution landscape, supported by their ability to manage chronic disease treatments and ensure physician oversight. Retail pharmacies also hold a strong position, driven by convenience and wide accessibility in urban and semi-urban areas. Online pharmacies are gaining traction due to rising internet penetration, growing e-commerce adoption, and discreet access to treatment options. It benefits from the diversification of distribution channels that expand reach and support patient adherence. Each channel plays a critical role in facilitating timely and effective therapy for hepatitis C patients across different demographics.

- For instance, a 2023 survey of major pharmaceutical distributors reported that hospital pharmacies dispensed over 1.8 million hepatitis C treatment courses worldwide, compared to 1.2 million through retail pharmacies and approximately 400,000 via online pharmacies.

Segments

Based on Drug Class

- Protease Inhibitors

- Polymerase Inhibitors

- NS5A Inhibitors

- Interferon and Antiviral

- Peginterferon alfa-2a

- Peginterferon alfa-2b

- Ribavirin

- Others

Based on Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Based on Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America Hepatitis C Treatment Market

North America accounted for approximately **23.9%** of the global Hepatitis C Treatment Market in 2024, with a market size of USD 2,078.17 million. It is projected to reach USD 2,699.61 million by 2032, growing at a CAGR of 3.3%. The region benefits from advanced healthcare systems, early adoption of innovative therapies, and well-established screening programs. The United States holds the majority share within the region due to favorable reimbursement policies and aggressive public health campaigns. Canada contributes moderately but shows consistent treatment coverage through universal healthcare access. It remains a mature market with strong focus on preventive initiatives and sustained patient education.

Europe Hepatitis C Treatment Market

Europe held nearly **22.5%** of the global market in 2024, valued at USD 1,960.12 million and expected to reach USD 2,762.99 million by 2032, expanding at the highest regional CAGR of 4.4%. Countries like Germany, France, and the UK drive growth through national hepatitis elimination strategies and expanded treatment access. The European Medicines Agency ensures streamlined regulatory pathways, supporting the approval of new drug combinations. It benefits from harmonized pricing models and robust public-private partnerships. Eastern European countries show potential due to growing investments in infectious disease control programs. The region emphasizes early detection and standardized treatment protocols.

Asia Pacific Hepatitis C Treatment Market

Asia Pacific dominated the global market in 2024 with the largest **regional market share of 34.3%**, reaching USD 2,984.29 million and projected to hit USD 4,122.19 million by 2032 at a CAGR of 4.1%. High disease prevalence in countries like China and India drives significant demand for affordable and accessible therapies. Governments are expanding screening coverage and negotiating generic drug licensing to reduce treatment costs. Japan contributes substantially through research, innovation, and public insurance programs. It offers a large untapped rural population with increasing awareness and healthcare reach. Cross-border collaborations and investment in healthcare infrastructure support regional growth.

Latin America Hepatitis C Treatment Market

Latin America represented approximately **9.9%** of the global market in 2024, valued at USD 858.40 million and estimated to reach USD 1,056.37 million by 2032, growing at a CAGR of 2.6%. Brazil and Mexico are the leading contributors due to national hepatitis programs and expanding access to low-cost medications. Public health systems focus on decentralized testing and mass treatment campaigns to improve disease control. However, inconsistent healthcare access in remote regions remains a key limitation. It sees gradual improvements through policy reforms and partnerships with global health organizations. Government-led awareness campaigns continue to expand diagnosis and treatment coverage.

Middle East Hepatitis C Treatment Market

The Middle East accounted for around **6.5%** of the global market in 2024, with a size of USD 567.88 million, expected to reach USD 739.46 million by 2032, growing at a CAGR of 3.3%. Countries such as Saudi Arabia and the UAE invest in modernizing healthcare infrastructure and improving infectious disease control. Awareness programs and early detection initiatives are gradually being implemented through public-private efforts. It shows increasing interest in digital health integration for better patient tracking and adherence. Access to branded therapies is growing, although cost containment remains a challenge in some economies. Ongoing clinical collaborations enhance regional market visibility.

Africa Hepatitis C Treatment Market

Africa held the smallest share at **2.9%** of the global Hepatitis C Treatment Market in 2024, valued at USD 249.52 million and projected to grow to USD 356.82 million by 2032, with the fastest CAGR of 4.6%. High disease burden and late-stage diagnosis continue to hamper control efforts across many nations. However, the region is witnessing support from global health agencies and donor-funded initiatives. Countries like Egypt have made substantial progress through mass treatment programs and generic drug access. It has begun leveraging mobile health platforms to reach underserved communities. Increasing healthcare investments and targeted intervention plans offer long-term market potential.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key players

- Gilead Sciences, Inc.

- AbbVie Inc.

- Kadmon Holdings, Inc.

- Hoffmann-La Roche Ltd

- GSK plc

- Bristol-Myers Squibb Company

- Merck & Co., Inc.

- Johnson & Johnson Services Inc.

- Vertex Pharmaceuticals

- AbbieVie Inc.

Competitive Analysis

The Global Hepatitis C Treatment Market features a highly competitive landscape led by companies with robust drug portfolios and established global distribution networks. Gilead Sciences, Inc. and AbbVie Inc. dominate the market through their successful antiviral therapies, particularly in the direct-acting antiviral segment. Companies such as Merck & Co., Bristol-Myers Squibb, and Johnson & Johnson invest heavily in clinical trials to improve cure rates and drug safety. New entrants focus on affordable generic versions to penetrate cost-sensitive regions. It continues to see intense competition in innovation, pricing strategies, and regional partnerships. Market leaders aim to expand through product launches, strategic collaborations, and targeted acquisition strategies.

Recent Developments

- On April 29, 2025, Gilead Sciences presented new data at the EASL Congress showing that investigational bulevirtide maintained virologic response in hepatitis delta patients post-treatment

- On June 11, 2025, AbbVie received FDA approval to expand the label of MAVYRET® (glecaprevir/pibrentasvir) to include treatment for acute Hepatitis C virus (HCV) infection. This approval makes MAVYRET the first and only oral, eight-week, pangenotypic treatment with a reported 96% cure rate for acute HCV.

Market Concentration and Characteristics

The Global Hepatitis C Treatment Market is moderately concentrated, with a few major pharmaceutical players holding significant market shares due to strong brand recognition, extensive drug portfolios, and established distribution networks. It is characterized by high barriers to entry, driven by complex regulatory approvals, high R&D costs, and patent protections. The market emphasizes innovation in direct-acting antiviral therapies, with a focus on pan-genotypic regimens and simplified dosing. Generic competition is rising, particularly in low- and middle-income countries where affordability is critical. It shows a mix of mature demand in developed regions and untapped potential in emerging markets. Strategic collaborations, licensing agreements, and public health partnerships shape competitive dynamics and support long-term market sustainability.

Report Coverage

The research report offers an in-depth analysis based on Drug Class, Distribution Channel and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Governments and health organizations will expand screening programs, leading to earlier diagnosis and higher treatment uptake across all regions.

- The market will witness an increasing shift toward pan-genotypic antiviral regimens, streamlining treatment for diverse patient populations with simplified protocols.

- Generic versions of key antiviral drugs will gain greater acceptance, particularly in low- and middle-income countries, driving affordability and access.

- The integration of telemedicine and mobile health platforms will enhance patient tracking, adherence, and outreach in remote and underserved areas.

- Collaborations between governments, NGOs, and pharmaceutical companies will strengthen funding and delivery infrastructure for mass treatment programs.

- Pharmaceutical companies will intensify research into therapies targeting drug-resistant hepatitis C strains to improve cure rates and address clinical gaps.

- Payers and public health systems are expected to update reimbursement frameworks, covering newer therapies and supporting broader access to treatment.

- These regions will attract significant investment due to high prevalence rates, growing awareness, and improving healthcare infrastructure.

- Regulatory bodies are likely to fast-track approvals for next-generation antiviral drugs, encouraging quicker market entry and treatment innovation.

- With WHO’s hepatitis C elimination targets by 2030, nations will prioritize testing and treatment, resulting in consistent long-term market growth.