Market Overview

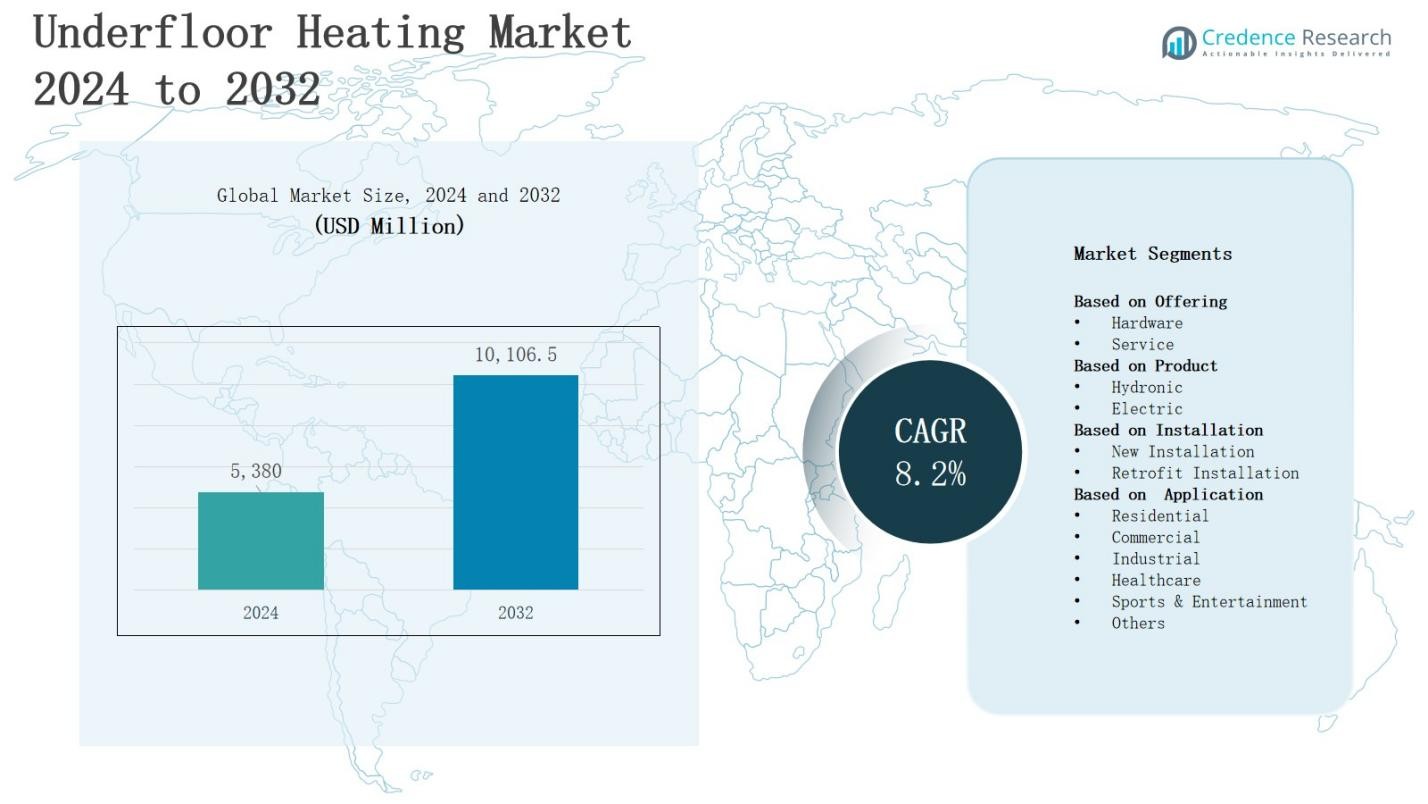

The underfloor heating market was valued at USD 5,380 million in 2024 and is projected to reach USD 10,106.5 million by 2032, expanding at a CAGR of 8.2% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Underfloor Heating Market Size 2024 |

USD 5,380 Million |

| Underfloor Heating Market, CAGR |

8.2% |

| Underfloor Heating Market Size 2032 |

USD 10,106.5 Million |

The underfloor heating market is driven by rising demand for energy-efficient heating solutions, growing adoption of sustainable construction practices, and increasing consumer preference for enhanced indoor comfort. Supportive government initiatives promoting green building standards further accelerate market growth. Advancements in smart thermostats and integration with home automation systems enhance convenience and efficiency, boosting adoption in both residential and commercial spaces. Trends shaping the market include the shift toward renewable energy-powered heating, rising retrofitting activities in existing buildings, and technological innovations in hydronic and electric systems, which collectively expand application potential and strengthen long-term market penetration.

The underfloor heating market spans North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, each contributing uniquely to growth. Europe leads with strict energy regulations and widespread adoption, while Asia Pacific grows rapidly through urbanization and smart city projects. North America benefits from modernization and smart home integration, whereas Latin America advances through urban housing projects. The Middle East & Africa expand with luxury construction and infrastructure investment. Key players include Nvent Electric PLC, Danfoss, Siemens AG, Emerson Electric Co., Mitsubishi Electric, Rehau, Nexans, Robert Bosch GmbH, Resideo Technologies Inc., Myson, Incognito Heat Co., and Amuheat.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The underfloor heating market was valued at USD 5,380 million in 2024 and is projected to reach USD 10,106.5 million by 2032, expanding at a CAGR of 8.2% during the forecast period.

- Rising demand for energy-efficient heating solutions and sustainable construction practices strengthens adoption across residential and commercial sectors.

- Growing consumer preference for enhanced indoor comfort, modern interiors, and space optimization drives market expansion.

- Government policies promoting green building standards and certifications such as LEED and BREEAM encourage system integration.

- High installation costs and complex retrofitting requirements remain key barriers, while slow response time and floor compatibility challenges limit adoption.

- Europe leads with 36% share, followed by Asia Pacific at 28%, North America at 21%, Latin America at 7%, and Middle East & Africa at 8%.

- Key players include Nvent Electric PLC, Danfoss, Siemens AG, Emerson Electric Co., Mitsubishi Electric, Rehau, Nexans, Robert Bosch GmbH, Resideo Technologies Inc., Myson, Incognito Heat Co., and Amuheat.

Market Drivers

Growing Demand for Energy-Efficient Heating Solutions

The underfloor heating market benefits from rising emphasis on energy efficiency in modern infrastructure. It delivers uniform heat distribution and reduces overall energy consumption compared to traditional systems. Governments and organizations promote low-energy building designs, which strengthens adoption. Rising electricity and fuel costs push households and businesses toward efficient heating alternatives. It supports sustainable development goals while lowering carbon footprints. Demand for efficient heating technologies keeps expanding across both residential and commercial projects.

- For instance, Danfoss reports that users can reduce floor heating energy consumption by 6–12 percent by lowering room temperature by 1–2 °C and using hydronic systems with proper insulation and wireless temperature control.

Rising Preference for Enhanced Indoor Comfort and Aesthetics

The underfloor heating market gains traction from increasing consumer preference for comfortable indoor environments. It offers even heat coverage, eliminating cold spots common in radiator systems. Architects and developers favor it because it maximizes space utilization without visible heating equipment. Growing demand for modern interiors aligns with this feature. Homeowners value its quiet operation and consistent performance. Rising disposable incomes support investments in premium housing with integrated comfort-oriented technologies.

- For instance, Uponor introduced its Minitec underfloor heating system with a pipe dimension of just 9.9 mm, enabling ultra-low-profile installation with floor build-up heights as low as 15 mm, which allows seamless integration into modern interior designs without compromising aesthetics.

Government Regulations and Supportive Green Building Initiatives

The underfloor heating market is influenced strongly by supportive policies encouraging sustainable construction. Regulations aimed at reducing greenhouse gas emissions promote energy-efficient heating solutions. Certification systems such as LEED and BREEAM highlight the importance of eco-friendly heating technologies. Governments offer incentives for adopting sustainable designs, encouraging builders to include underfloor systems. It aligns with national carbon reduction strategies. Increasing awareness of environmental responsibility drives further adoption across residential, industrial, and commercial projects.

Technological Advancements and Integration with Smart Systems

The underfloor heating market expands with innovations in electric and hydronic systems. Advancements improve installation efficiency, reduce maintenance requirements, and optimize energy usage. Integration with smart thermostats and home automation enhances convenience for users. It enables remote monitoring and customized heat settings, attracting tech-savvy consumers. Manufacturers invest in product development to meet growing expectations for intelligent, efficient heating. Rising popularity of connected homes ensures continued demand for innovative underfloor heating solutions globally.

Market Trends

Increasing Adoption of Renewable Energy-Powered Heating Systems

The underfloor heating market is experiencing strong growth with the integration of renewable energy sources. Solar panels and geothermal heat pumps are increasingly paired with underfloor systems to reduce dependence on conventional fuels. It enhances sustainability while aligning with global carbon reduction goals. Developers prefer renewable-compatible heating to meet stricter environmental standards. Growing government focus on clean energy further drives adoption. This trend positions underfloor heating as a cornerstone of future green building designs.

- For instance, Uponor collaborated on projects in Sweden where solar-assisted underfloor heating systems reduced building CO₂ emissions.

Rising Popularity of Retrofitting Projects in Residential and Commercial Spaces

The underfloor heating market is witnessing significant demand from retrofitting applications in older buildings. Homeowners and businesses are upgrading existing structures to improve comfort and energy efficiency. It supports renovation trends in urban centers where modern heating solutions replace outdated radiators. Advancements in installation techniques make retrofitting cost-effective and less disruptive. Growing urbanization and property upgrades fuel this momentum. Increased investments in building modernization ensure long-term opportunities for underfloor heating providers.

- For instance, Warmup PLC introduced its DCM-PRO Peel & Stick system in 2023, which allows installers to cover up to 10 m² per hour, minimizing downtime in commercial refurbishments.

Integration of Smart Home Technologies and Connected Devices

The underfloor heating market is being shaped by the rise of smart home ecosystems. Integration with intelligent thermostats, IoT-enabled sensors, and mobile applications enhances user control. It allows real-time adjustments, energy monitoring, and personalized comfort settings. Consumers value systems that combine efficiency with convenience. Manufacturers respond by offering advanced digital interfaces and wireless connectivity. Rising demand for connected living spaces ensures ongoing innovation in heating technologies tailored for modern households and businesses.

Focus on Sustainability and Eco-Friendly Construction Materials

The underfloor heating market benefits from the rising trend of sustainable construction practices. Developers increasingly specify eco-friendly insulation, low-emission materials, and recyclable components in heating systems. It strengthens compliance with international green building standards. Growing awareness of environmental health influences buyer preferences toward sustainable heating. Manufacturers invest in research to introduce greener alternatives. This trend reflects the alignment of consumer choices, regulatory expectations, and corporate responsibility with global sustainability initiatives in construction.

Market Challenges Analysis

High Installation Costs and Complex Retrofitting Requirements

The underfloor heating market faces challenges due to high upfront installation costs compared to conventional systems. It requires specialized materials, skilled labor, and in many cases, structural modifications, which raise expenses. Retrofitting older buildings presents added complexity, often involving removal of existing flooring and adjustments to insulation. Many homeowners hesitate to invest despite long-term savings. Commercial projects also weigh budget constraints against potential efficiency benefits. These cost-related barriers limit widespread adoption in price-sensitive markets.

Slow Heating Response and Compatibility Limitations

The underfloor heating market also encounters performance-related challenges that affect consumer decisions. It has a slower response time compared to radiators, which delays immediate temperature adjustments. Compatibility issues arise in poorly insulated buildings or spaces requiring rapid heating cycles. Certain floor types, such as thick carpets or hardwood, restrict efficiency and uniformity of heat distribution. Consumers often perceive these limitations as trade-offs against comfort. Overcoming such drawbacks is essential for expanding its acceptance globally.

Market Opportunities

Expansion Across Emerging Economies and Urban Infrastructure Projects

The underfloor heating market holds significant opportunities in rapidly urbanizing regions where infrastructure development is accelerating. Rising investments in modern housing and commercial complexes create strong demand for advanced heating systems. It aligns with government initiatives promoting energy-efficient buildings in Asia-Pacific, Latin America, and the Middle East. Expanding middle-class populations with higher disposable incomes further drive adoption. Developers view it as a value-added feature that enhances property appeal. These factors establish fertile ground for market penetration.

Integration with Smart Technologies and Sustainable Energy Solutions

The underfloor heating market also benefits from opportunities created by integration with smart technologies and renewable energy sources. It can be paired with solar heating, geothermal pumps, and intelligent thermostats to maximize efficiency and sustainability. Growing consumer preference for connected homes drives manufacturers to innovate with IoT-enabled features. Demand for eco-friendly construction materials supports greener product development. These advancements position underfloor systems as a future-ready solution. Expanding smart city projects will strengthen long-term adoption potential.

Market Segmentation Analysis:

By Offering

The underfloor heating market is segmented into hardware and services. Hardware dominates due to the large-scale demand for heating mats, pipes, and control units in both residential and commercial projects. It drives initial system adoption and remains the largest revenue contributor. Services gain importance through installation, maintenance, and system optimization. Growing demand for specialized expertise in retrofitting projects supports service expansion. Together, these segments create a balanced ecosystem that strengthens adoption across diverse applications.

- For instance, Danfoss introduced its Ally smart heating system in 2024, which is voice-controlled and includes the Icon2 hydronic floor heating control, enhancing ease of use through smart home integration and energy efficiency optimization.

By Product

The underfloor heating market is divided into hydronic and electric systems. Hydronic solutions lead in large-scale applications such as commercial buildings and industrial facilities, valued for their long-term efficiency and cost-effectiveness. Electric systems gain traction in residential projects due to easier installation and flexibility across floor types. It aligns with consumer preference for smart and compact heating options. Rising innovation in energy-saving technologies continues to boost demand across both categories.

- For instance, Pipelife installed hydronic underfloor heating in the Jaguar car showroom in Ireland, highlighting its ability to provide consistent heat while allowing the use of heavy machinery on the floor.

By Installation

The underfloor heating market is segmented into new installations and retrofit installations. New installations dominate in ongoing residential and commercial construction projects where heating systems can be seamlessly integrated into designs. Retrofit installations are expanding quickly due to urban renovation trends and rising consumer interest in upgrading comfort and energy efficiency. It faces higher costs but benefits from advancements that simplify retrofitting. Both installation types highlight diverse growth avenues for manufacturers and service providers.

Segments:

Based on Offering

Based on Product

Based on Installation

- New Installation

- Retrofit Installation

Based on Application

- Residential

- Commercial

- Industrial

- Healthcare

- Sports & Entertainment

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds 21% share of the underfloor heating market, supported by strong adoption in residential and commercial construction. Consumers prioritize comfort, energy efficiency, and modern design integration, making it a preferred solution across housing projects. Government initiatives promoting green building standards also encourage adoption. It benefits from technological advancements and integration with smart home ecosystems. The United States leads growth with high investments in infrastructure modernization. Canada contributes with demand from luxury housing and eco-friendly construction.

Europe

Europe accounts for 36% share of the underfloor heating market, making it the largest regional segment. Strict energy regulations, strong sustainability goals, and a preference for advanced heating solutions drive growth. It is widely installed in residential buildings, offices, and public infrastructure. Countries like Germany, the UK, and Nordic nations lead adoption with advanced construction practices. Rising retrofitting activities in older buildings further support expansion. The region remains the hub for technological innovation and eco-friendly product development.

Asia Pacific

Asia Pacific captures 28% share of the underfloor heating market, fueled by rapid urbanization and extensive residential construction. Rising disposable incomes and consumer demand for premium housing strengthen adoption. It benefits from government investments in smart city projects and energy-efficient building regulations. China and India are key contributors with strong housing development trends. Japan and South Korea support growth with advanced heating technologies. Rising awareness of indoor comfort and sustainability continues to expand market penetration.

Latin America

Latin America holds 7% share of the underfloor heating market, supported by demand from urban housing and commercial renovations. Rising interest in modern construction techniques drives adoption in countries such as Brazil and Mexico. It faces barriers from higher upfront costs but benefits from gradual modernization of infrastructure. Growing real estate development in metropolitan areas creates opportunities. Luxury housing projects increasingly incorporate advanced heating systems. Rising awareness of energy savings strengthens long-term demand potential.

Middle East & Africa

The Middle East & Africa represent 8% share of the underfloor heating market, driven by rising infrastructure investments and premium housing projects. The Middle East leads adoption with demand from high-end residential and hospitality sectors. It aligns with regional construction booms in the UAE, Saudi Arabia, and Qatar. Africa’s growth remains modest but strengthens through urbanization in South Africa and Nigeria. Integration with renewable energy supports adoption in climate-sensitive areas. Market opportunities expand through luxury-oriented projects and sustainability initiatives.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Myson

- Mitsubishi Electric

- Robert Bosch GmbH

- Resideo Technologies Inc

- Incognito Heat Co.

- Amuheat

- Siemens AG

- Rehau

- Emerson Electric Co.

- Nexans

- Danfoss

- Nvent Electric PLC

Competitive Analysis

The underfloor heating market is highly competitive, shaped by established multinational corporations and specialized regional players focusing on innovation and efficiency. Companies such as Nvent Electric PLC, Danfoss, Emerson Electric Co., Mitsubishi Electric, and Siemens AG leverage advanced technologies to strengthen their product portfolios and expand global reach. It emphasizes energy efficiency, integration with smart home systems, and compatibility with renewable energy sources, driving continuous product enhancements. Robert Bosch GmbH, Resideo Technologies Inc., Rehau, and Nexans maintain strong positions through broad distribution networks and sustainable product development. Myson, Incognito Heat Co., and Amuheat target niche segments with tailored solutions that meet regional demand for premium and cost-effective heating systems. Intense competition encourages strategic collaborations, acquisitions, and geographic expansion, with leading players investing heavily in research and development to address rising consumer demand for eco-friendly and connected heating solutions. The market reflects a dynamic balance where global leaders pursue scale while emerging firms focus on specialized offerings, collectively advancing adoption and long-term growth.

Recent Developments

- In February 2025, HeatUp joined the Elydan Group, strengthening its European presence and expanding synergies with Elydan’s geothermal heating portfolio.

- In March 2024, JVIS launched its MicroHeat Series 6 hydronic system, enabling faster retrofitting and offering digital power adjustment for precise underfloor heating control.

- In April 2023, Resideo Technologies introduced the Honeywell Home T10+ Smart Thermostat Kits with RedLINK® 3.0 technology, enhancing integration with indoor air quality systems for improved energy efficiency.

- In April 2025, the Purmo Group acquired UFHN, a UK‑based specialist in hydronic and electric underfloor‑heating systems, heat pumps, and controls, bolstering its presence in complete indoor‑climate solutions across the UK

Market Concentration & Characteristics

The underfloor heating market demonstrates a moderately consolidated structure, with global leaders and regional specialists competing to expand presence across diverse applications. Large multinational firms such as Nvent Electric PLC, Danfoss, Siemens AG, Emerson Electric Co., Mitsubishi Electric, and Robert Bosch GmbH maintain strong market positions through extensive product portfolios, advanced technologies, and established distribution networks. It reflects high entry barriers due to significant installation expertise, compliance requirements, and upfront investment costs. Smaller players like Myson, Incognito Heat Co., and Amuheat compete by offering tailored solutions for specific regional demands, creating a balance between global scale and localized specialization. The market is characterized by strong emphasis on energy efficiency, integration with smart home ecosystems, and compatibility with renewable energy sources. Rapid technological advancements and increasing sustainability requirements continue to shape its competitive dynamics, reinforcing innovation and strategic collaborations as key features of market concentration and characteristics.

Report Coverage

The research report offers an in-depth analysis based on Offering, Product, Installation, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with rising adoption of energy-efficient heating systems in residential and commercial projects.

- Demand will grow through integration of underfloor systems with smart home technologies and connected devices.

- Retrofitting opportunities will increase as older buildings undergo modernization and energy upgrades.

- Renewable energy integration, including solar and geothermal, will enhance long-term adoption.

- Consumer preference for enhanced indoor comfort and modern aesthetics will strengthen product demand.

- Green building regulations and sustainability initiatives will encourage wider system installations.

- Technological advancements in electric and hydronic systems will improve efficiency and ease of installation.

- Luxury housing and premium infrastructure projects will create consistent growth opportunities.

- Regional expansion will accelerate in Asia Pacific, Latin America, and the Middle East with rising urbanization.

- Strategic collaborations among manufacturers, developers, and technology providers will shape future competitive dynamics.