Market Overview

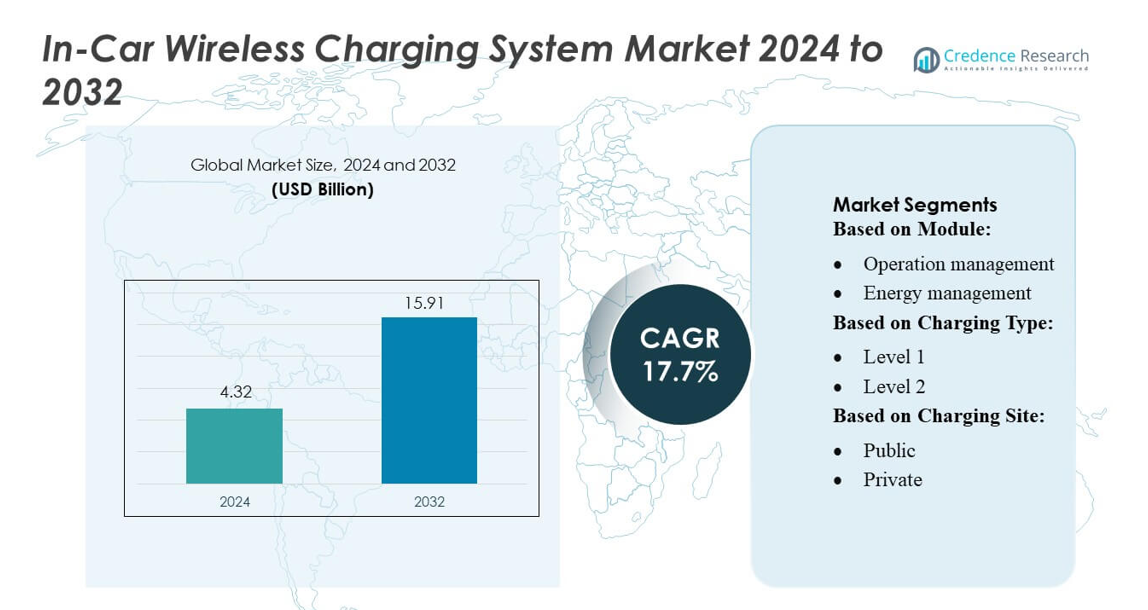

In-Car Wireless Charging System Market size was valued USD 4.32 billion in 2024 and is anticipated to reach USD 15.91 billion by 2032, at a CAGR of 17.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| In-Car Wireless Charging System Market Size 2024 |

USD 4.32 billion |

| In-Car Wireless Charging System Market, CAGR |

17.7% |

| In-Car Wireless Charging System Market Size 2032 |

USD 15.91 billion |

In-Car Wireless Charging System Market include Energous Corporation, Anker Innovations Technology Co., Ltd., Powercast Corporation, InductEV Inc., Apple, Inc., PLUGLESS POWER INC., Belkin International, Inc., Electreon Wireless Ltd., Continental AG, and Ossia Inc. These companies are actively driving market growth through innovations in high-efficiency charging modules, compact designs, and integration with electric and connected vehicles. Strategic partnerships with automotive OEMs and investments in R&D are strengthening their competitive positions. North America leads the market, capturing approximately 32% of the global share, driven by early adoption of advanced automotive technologies, strong EV infrastructure, and consumer demand for convenience and wireless solutions. The combination of technological innovation, regulatory support, and growing electric vehicle penetration reinforces the region’s dominance while the top players continue to expand their footprint through collaborations and product enhancements across multiple vehicle segments.

Market Insights

- The In-Car Wireless Charging System Market size was valued at USD 4.32 billion in 2024 and is projected to reach USD 15.91 billion by 2032, growing at a CAGR of 17.7% during the forecast period.

- Market growth is driven by increasing adoption of electric and connected vehicles, rising consumer demand for convenience, and advancements in high-efficiency, compact charging modules.

- Technological trends include dynamic wireless charging, integration with smart and autonomous vehicle systems, and interoperability across multiple vehicle models, enhancing user experience and safety.

- The competitive landscape is shaped by strategic partnerships, R&D investment, and collaborations between automotive OEMs and technology providers, enabling companies to expand product offerings and maintain a competitive edge.

- Regionally, North America leads with approximately 32% market share, followed by Europe and Asia-Pacific, while the market segments are dominated by plug-in and high-efficiency charging modules, with public and private vehicle segments driving adoption globally.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Module:

The operation management segment leads the module category, capturing the largest market share of approximately 38%. Its dominance is driven by the increasing adoption of intelligent vehicle systems that optimize charging schedules, monitor battery health, and ensure seamless integration with the vehicle’s infotainment and telematics platforms. Energy management follows closely, propelled by advancements in power conversion efficiency and smart load balancing technologies. Billing & payment modules are gaining traction due to the rise of automated payment systems, while other modules, including security and data analytics, are gradually emerging as supplementary growth contributors.

- For instance, Energous Corporation’s WattUp®‑based wireless power solutions recently achieved full certification for their “2W PowerBridge” transmitter, delivering up to 8 W Effective Isotropic Radiated Power (EIRP) — a level recognized as compliant for over‑the‑air wireless charging deployments.

By Charging Type:

Level 2 wireless charging dominates the market, holding a 45% share, owing to its optimal balance of charging speed and infrastructure cost. The growing adoption of Level 2 chargers is driven by their compatibility with a broad range of electric vehicles (EVs) and the increasing installation at residential and commercial locations. Level 1 charging remains relevant for low-power applications and home use, while Level 3 systems, offering ultra-fast charging capabilities, are gradually expanding in public charging networks, propelled by advancements in high-efficiency inductive charging coils and reduced energy losses.

- For instance, Anker Innovations Technology Co., Ltd. recently released a Qi2-certified wireless car charger that supports up to 25 W output — a major upgrade over older 7.5 W Qi chargers — enabling substantially faster charging compatible with modern electric‑vehicle accessories.

By Charging Site:

Public charging sites represent the largest segment, commanding a 52% market share, fueled by government initiatives to expand EV infrastructure and partnerships between automakers and urban mobility providers. Public deployment is further supported by technological innovations in multi-vehicle charging pads and networked monitoring systems. Private charging solutions, including residential and corporate installations, are witnessing steady growth, driven by consumer preference for convenience and enhanced safety features. The adoption of smart home energy systems and integrated mobile applications continues to accelerate the uptake of private wireless charging solutions.

Key Growth Drivers

Rising Adoption of Electric Vehicles (EVs):

The increasing penetration of EVs in Australia drives demand for in-car wireless charging systems. Government incentives, emission reduction targets, and consumer awareness about sustainable transportation are accelerating EV adoption. Wireless charging offers convenience, reducing dependency on traditional plug-in stations. Automakers integrating inductive charging into new EV models further boosts market growth. For instance, the expansion of EV fleets among urban commuters and ride-sharing services creates a steady need for accessible, efficient wireless charging infrastructure.

- For instance, Powerharvester® RF‑to‑DC converter chips which achieve conversion efficiencies of over 75%, enabling remote power-over-distance charging of embedded electronics and sensors without direct contact.

Technological Advancements in Wireless Charging:

Continuous innovation in inductive charging technology enhances efficiency and reduces charging time, stimulating market growth. Companies are developing high-power, low-loss coils and automated alignment systems, improving user experience and reliability. Integration with smart vehicle systems enables predictive energy management and remote monitoring. Additionally, advancements in compact charging modules facilitate retrofitting in existing vehicles. These technological improvements are encouraging both OEMs and consumers to adopt wireless charging, positioning it as a viable alternative to conventional wired systems in Australia.

- For instance, InductEV’s in‑ground wireless charging pads now deliver up to 450 kW of power for heavy‑duty vehicles, while single‑pad installations for cars and vans provide 75 kW.

Expansion of Public and Private Charging Infrastructure:

Australia’s investment in public and private EV charging networks fuels demand for wireless systems. Public-private partnerships and government-led initiatives promote the installation of multi-vehicle charging pads in urban areas, parking lots, and commercial hubs. Meanwhile, residential adoption is rising, supported by smart home energy management systems and IoT-enabled monitoring. The growing availability of charging infrastructure reduces range anxiety and strengthens consumer confidence, directly contributing to the rapid uptake of in-car wireless charging solutions across metropolitan and regional areas.

Key Trends & Opportunities

Integration with Smart Mobility Solutions:

Wireless charging systems are increasingly integrated with connected vehicle and smart mobility platforms. This trend enables features such as automated billing, energy optimization, and real-time charging status updates through mobile apps. Fleet operators and shared mobility services in Australia benefit from reduced downtime and enhanced operational efficiency. The convergence of EVs, IoT, and cloud-based management presents opportunities for software-driven revenue models and partnerships between automotive and tech companies.

- For instance, Plugless Power’s third‑generation system supports an air gap of up to 12 inches, enabling charging even under trucks and SUVs.

Rise in High-Power Charging Solutions:

The development of high-power Level 2 and Level 3 wireless chargers offers faster charging times, addressing consumer demand for convenience. These systems are particularly suitable for commercial fleets, public transit, and high-traffic urban centers. The adoption of modular, scalable charging units allows operators to expand capacity as EV numbers grow. High-power charging also supports energy management initiatives by reducing grid load fluctuations, creating opportunities for integration with renewable energy sources and smart grid technologies in Australia.

- For instance, Belkin recently secured official certification under the latest Qi2.2 wireless‑charging standard, enabling its new wireless chargers to deliver up to 25 W output — a substantial increase over older 5 W/15 W Qi chargers.

Growing Consumer Preference for Contactless Solutions:

Post-pandemic behavioral shifts have increased demand for contactless, convenient solutions, including wireless charging. Consumers increasingly prefer systems that eliminate manual cable handling while ensuring safety and efficiency. Automakers are leveraging this trend by incorporating wireless charging into premium vehicle models, creating differentiation in the competitive EV market. The combination of ease-of-use, reduced maintenance, and compatibility with smart devices presents an attractive opportunity for market expansion.

Key Challenges

High Initial Costs and Limited Adoption:

The high cost of wireless charging systems, including vehicle retrofitting and infrastructure installation, remains a significant barrier. Consumers and fleet operators may be hesitant to invest due to higher upfront expenditures compared to conventional plug-in solutions. Additionally, limited awareness and adoption rates in regional areas slow market penetration. While technological benefits are clear, widespread commercialization requires cost reductions, economies of scale, and government incentives to make wireless charging a practical choice for a larger audience.

Technical Limitations and Standardization Issues:

Challenges in system efficiency, alignment sensitivity, and interoperability with different EV models affect adoption. Lack of uniform technical standards across automakers and charging networks can hinder seamless integration. Variability in energy transfer efficiency and potential electromagnetic interference require careful design and regulatory compliance. Overcoming these technical and standardization hurdles is essential to ensure reliability, user confidence, and market scalability, particularly in diverse automotive and infrastructure ecosystems like Australia’s.

Regional Analysis

North America:

North America leads the In-Car Wireless Charging System Market, holding approximately 32% of the global share. The region benefits from strong automotive innovation, early adoption of electric and connected vehicles, and significant investment in charging infrastructure. U.S. and Canada witness increasing integration of wireless charging in premium and mid-segment vehicles, driven by consumer demand for convenience and technological advancement. Automotive OEMs are collaborating with tech providers to enhance compatibility and efficiency. Regulatory support for EV adoption, coupled with rising awareness of wireless charging benefits, further bolsters growth, making North America a dominant and trendsetting market globally.

Europe:

Europe accounts for around 28% of the global market, driven by aggressive EV adoption, stringent emission regulations, and government incentives for sustainable transportation. Germany, France, and the U.K. are key markets, with OEMs integrating wireless charging in luxury and electric vehicles. Technological innovation in high-efficiency coils and standardized charging protocols enhances market growth. The rise of connected and autonomous vehicle development programs further stimulates demand. Public-private partnerships to expand urban charging infrastructure and initiatives to reduce carbon footprints are significant growth enablers. Europe’s focus on convenience, safety, and energy-efficient solutions ensures steady expansion of the in-car wireless charging market.

Asia-Pacific:

Asia-Pacific holds approximately 25% market share, emerging as a high-growth region due to increasing EV sales, urbanization, and tech-driven automotive trends. China, Japan, and South Korea are leading contributors, driven by government incentives, smart city initiatives, and local OEM innovation in wireless charging technology. Rising disposable incomes and consumer preference for high-tech vehicle features further boost adoption. Collaborations between automotive and electronics companies are accelerating the development of compact and efficient wireless charging modules. The region’s rapid EV penetration, infrastructure expansion, and supportive policies position Asia-Pacific as a strategic hub for wireless in-car charging growth globally.

Latin America:

Latin America represents about 8% of the global market, with Brazil and Mexico leading adoption. Market growth is supported by rising EV awareness, modernization of urban transport systems, and interest in premium vehicle technology. Limited charging infrastructure is gradually being addressed through private investment and government initiatives, boosting wireless charging deployment. OEMs focus on introducing wireless charging as a differentiating feature in high-end vehicles. Increasing consumer demand for convenience, coupled with gradual EV market expansion, provides opportunities for market penetration. While adoption remains slower than North America and Europe, Latin America is steadily evolving, reflecting positive growth potential for in-car wireless charging systems.

Middle East & Africa:

The Middle East and Africa account for around 7% of the market, with growth driven primarily by the UAE, Saudi Arabia, and South Africa. Luxury and high-performance vehicle markets are adopting wireless charging as a premium feature. Infrastructure development in urban areas and smart mobility projects are gradually supporting EV integration. OEMs are exploring partnerships to introduce wireless charging in electric and hybrid vehicles, focusing on high-efficiency solutions suitable for extreme climates. While market penetration is currently limited, increasing investment in smart cities, renewable energy adoption, and high-end automotive technologies is expected to propel moderate growth in the region over the next few years.

Market Segmentations:

By Module:

- Operation management

- Energy management

By Charging Type:

By Charging Site:

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The In-Car Wireless Charging System Market include Energous Corporation, Anker Innovations Technology Co., Ltd., Powercast Corporation, InductEV Inc., Apple, Inc., PLUGLESS POWER INC., Belkin International, Inc., Electreon Wireless Ltd., Continental AG, and Ossia Inc. In-Car Wireless Charging System Market is driven by continuous technological innovation, strategic partnerships, and aggressive R&D investment. Companies are focusing on developing high-efficiency charging solutions, compact designs, and interoperable systems compatible with multiple vehicle models. The market emphasizes dynamic wireless charging, integration with connected and electric vehicles, and enhanced safety features to improve user experience. Collaborations with automotive OEMs and technology providers are accelerating adoption, while regulatory compliance and standardization initiatives support market expansion. Companies are also prioritizing cost optimization and scalability to address increasing consumer demand. Overall, innovation, strategic alliances, and the ability to adapt to evolving automotive trends are shaping a highly competitive environment and driving growth in this rapidly evolving market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In February 2025, Powercast Corporation and B&Plus formed a strategic partnership to introduce Powercast’s RF wireless power solutions to Japan, supporting the country’s net-zero emissions goals. This collaboration aims to reduce reliance on traditional batteries in various industries by integrating Powercast’s technology into B&Plus’s product designs, offering a battery-free alternative for enhanced efficiency and reduced waste.

- In January 2025, Samsung Electronics Co., Ltd. announced a new power management integrated chip (PMIC) called the S2MIW06 has this covered, though, supporting high-power wireless charging up to 50W so that it’s sufficiently future-proofed. This chip aligns with the forthcoming Qi 2.2 standard and supports all major Qi profiles, including Baseline Power Profile (BPP), Extended Power Profile (EPP), and Magnetic Power Profile (MPP).

- In September 2024, Tesla released a new Wireless Portable Charger for mobile devices, available in black, rose gold, and white, with features like simultaneous dual-device charging, a hinged magnetic stand, and a 5000mAh battery

Report Coverage

The research report offers an in-depth analysis based on Module, Charging Type, Charging Site and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will witness increased adoption of electric and connected vehicles, driving demand for in-car wireless charging systems.

- Technological advancements in high-efficiency coils and compact designs will enhance charging performance and convenience.

- Integration of wireless charging with autonomous and smart vehicle systems will become more widespread.

- OEM partnerships and collaborations will accelerate market penetration and standardization.

- Expansion of public and private charging infrastructure will support greater adoption in urban areas.

- Dynamic wireless charging solutions will emerge, enabling charging while vehicles are in motion.

- Growing consumer preference for convenience and seamless charging experiences will boost demand.

- Regulatory support for EV adoption and sustainability initiatives will positively impact market growth.

- Continuous R&D investment will lead to improved energy efficiency and safety features.

- Emerging markets in Asia-Pacific, Latin America, and the Middle East will present new growth opportunities.