Market Overview

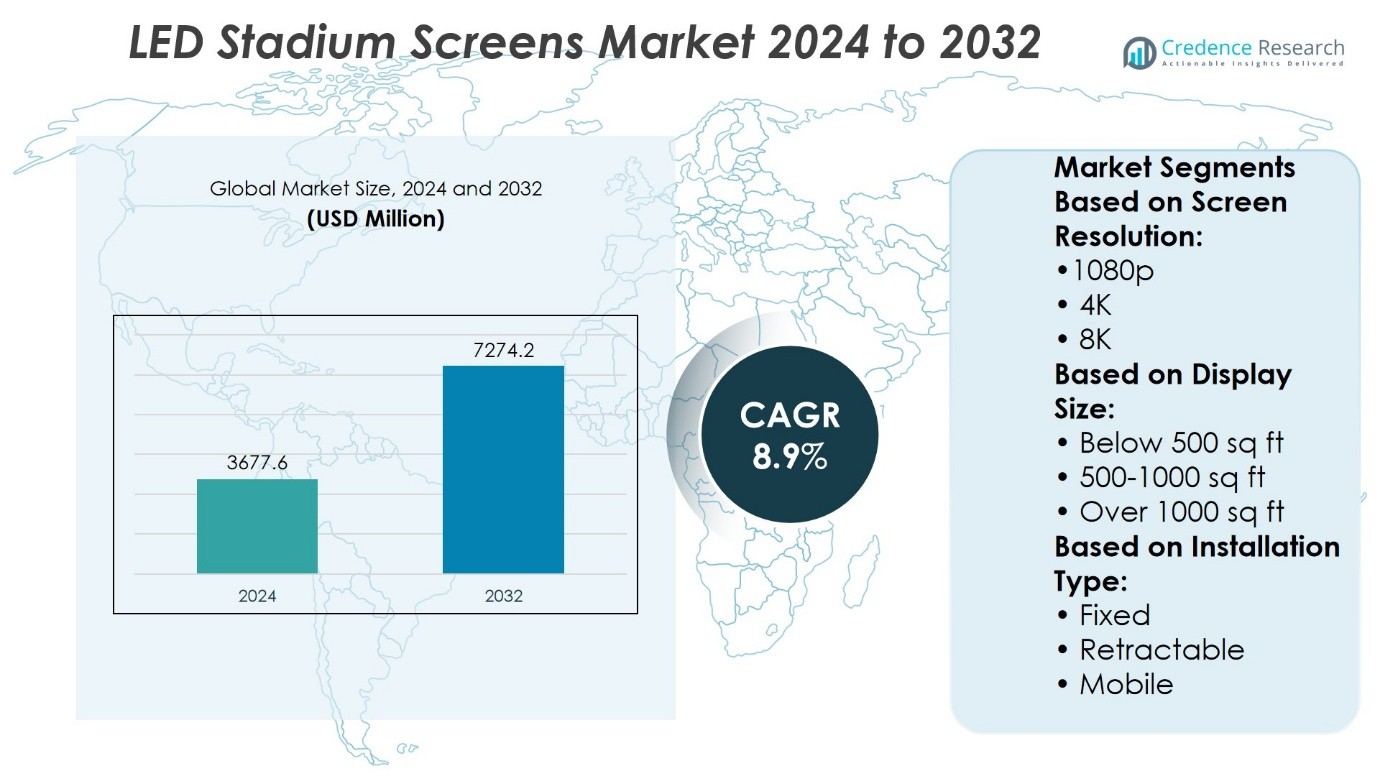

LED Stadium Screens Market size was valued at USD 3677.6 million in 2024 and is anticipated to reach USD 7274.2 million by 2032, at a CAGR of 8.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| LED Stadium Screens Market Size 2024 |

USD 3677.6 Million |

| LED Stadium Screens Market, CAGR |

8.9% |

| LED Stadium Screens Market Size 2032 |

USD 7274.2 Million |

The LED Stadium Screens Market grows through rising demand for immersive viewing experiences, increased investments in sports infrastructure, and the need for advanced advertising platforms within venues. It benefits from technological advancements in pixel pitch, brightness, and energy efficiency, enabling superior image quality and lower operating costs. The adoption of high-resolution formats such as 4K and 8K enhances live event broadcasting and fan engagement. Expanding use in multipurpose venues, integration with real-time content management systems, and the growing focus on sustainability further shape market trends, driving continuous innovation and broadening the scope of applications across global sports and entertainment arenas.

The LED Stadium Screens Market has strong presence across North America, Asia Pacific, Europe, Latin America, and the Middle East & Africa, with North America and Asia Pacific leading due to large-scale stadium projects and advanced technology adoption. Europe maintains significant demand through its extensive sports infrastructure, while other regions grow with new venue developments. Key players include ROE Visual, AOTO Electronics, Hisense Visual Technology, LianTronics, Samsung Electronics, Leyard, Panasonic, Absen, Shenzhen Absen Optoelectronics, and Mitsubishi Electric, each competing through innovation, quality, and project execution capabilities.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The LED Stadium Screens Market was valued at USD 3677.6 million in 2024 and is projected to reach USD 7274.2 million by 2032, at a CAGR of 8.9%.

- Demand rises due to immersive viewing needs, increased sports infrastructure investments, and advanced in-venue advertising capabilities.

- Trends include adoption of 4K and 8K formats, finer pixel pitch, and improved energy efficiency for better performance and lower costs.

- Competition involves innovation, large-scale installation expertise, and turnkey solutions from established global and regional players.

- High initial investment costs and maintenance requirements limit adoption in smaller or budget-constrained venues.

- North America and Asia Pacific lead the market, Europe maintains strong demand, while Latin America and Middle East & Africa expand through new stadium projects.

- Key players focus on integrating real-time content management, enhancing durability, and developing sustainable solutions to strengthen market positioning.

Market Drivers

Growing Investments in Sports Infrastructure and Event Facilities

The LED Stadium Screens Market benefits from significant investments in upgrading sports stadiums and multipurpose event venues. Governments and private stakeholders prioritize large-format digital displays to enhance spectator engagement. It supports real-time score updates, instant replays, and interactive fan experiences. Modern stadium renovation projects increasingly allocate budget for high-definition LED screens. International sports events drive temporary and permanent installations to meet broadcast and audience standards. This infrastructure expansion strengthens long-term demand across regional and global markets.

- For instance, at Truist Park (home to the Atlanta Braves), SNA Displays instalLED a new center-field LED videoboard measuring 65 feet by 121 feet.

Advancements in Display Technology and Visual Performance

The LED Stadium Screens Market gains momentum from continuous improvements in LED display resolution, brightness, and refresh rates. Manufacturers introduce ultra-high-definition panels capable of clear visibility under direct sunlight and in night-time conditions. It delivers seamless image rendering for live sports, concerts, and large-scale events. Innovations in pixel pitch allow more compact yet detaiLED displays, optimizing space utilization. Energy-efficient modules reduce operational costs and meet sustainability goals. These advancements position LED screens as a preferred choice over traditional display solutions.

- For instance, Daktronics did not upgrade the SoFi Stadium’s main video board. It was Samsung that upgraded the video board, which is now known as the “Infinity Screen by Samsung”, and it features approximately 80 million pixels.

Rising Demand for Enhanced Fan Engagement and Sponsorship Opportunities

The LED Stadium Screens Market thrives on the growing emphasis on fan interaction and dynamic advertising. Sports franchises and event organizers leverage these displays to deliver targeted content, live social media feeds, and interactive polls. It creates new revenue streams through high-value sponsorship placements. Real-time data integration enhances the viewing experience both in-stadium and for broadcast audiences. The flexibility of content scheduling maximizes advertising impact for brands. This focus on engagement ensures strong adoption across sports and entertainment sectors.

Expansion of Global Sports and Entertainment Events Calendar

The LED Stadium Screens Market experiences growth through an expanding calendar of international sporting events, concerts, and cultural festivals. Major tournaments, music tours, and esports competitions require reliable, large-scale visual displays. It drives recurring demand from both permanent venues and temporary event setups. Event organizers prioritize quick installation and dismantling capabilities to optimize operational timelines. Rental service providers invest in advanced LED systems to meet diverse client needs. This steady flow of events secures continuous market activity throughout the year.

Market Trends

Advancements in High-Resolution and Energy-Efficient Display Technology

The LED Stadium Screens Market is evolving through the introduction of higher resolution panels and energy-efficient LED modules. Manufacturers develop ultra-high-definition displays with improved pixel density for sharper visuals in large venues. It enhances spectator experience by delivering clearer images and vibrant colors regardless of lighting conditions. Energy-saving driver ICs and advanced thermal management systems reduce operational costs. These technological improvements increase the lifespan of screens and lower maintenance requirements. The trend supports both new stadium projects and the upgrade of existing facilities.

- For instance, SNA Displays’ installation at Truist Park features the BravesVision board with 13.1 million pixels, complemented by ribbon boards totaling 4.1 million pixels.

Growing Demand for Interactive and Multi-Functional Displays

The LED Stadium Screens Market is witnessing a shift toward interactive features and multi-purpose usage. Screens now support live data integration, fan engagement tools, and augmented reality content. It enables stadium operators to create immersive experiences that extend beyond standard broadcasting. Modular systems allow the same screen to be used for sports, concerts, and corporate events. Integration with social media feeds and real-time analytics strengthens audience participation. This multifunctionality maximizes return on investment for venue owners.

- For instance, SNA Displays’ BravesVision center-field videoboard at Truist Park contains 13.1 million pixels, complemented by ribbon boards totaling.

Expansion of Rental and Temporary Installation Services

The LED Stadium Screens Market benefits from the increasing demand for temporary setups at tournaments, concerts, and festivals. Event organizers opt for rental solutions to avoid large capital investments. It encourages screen providers to invest in lightweight, quick-assembly designs for fast deployment. High-brightness portable units ensure visibility in varying weather conditions. Logistics and storage efficiency become key factors in service provider competitiveness. This rental market expansion complements permanent installation growth.

Adoption of Weatherproof and Durable Outdoor Solutions

The LED Stadium Screens Market is trending toward weather-resistant designs that withstand harsh outdoor environments. Manufacturers produce IP65-rated and higher-protection panels to handle rain, dust, and extreme temperatures. It ensures uninterrupted performance during year-round sporting and entertainment events. Rugged construction and reinforced frames extend operational lifespan in high-use stadiums. Advanced coating materials prevent corrosion and maintain visual clarity. This durability focus supports long-term investment value for venue operators.

Market Challenges Analysis

High Installation and Maintenance Costs

The LED Stadium Screens Market faces challenges related to the significant investment required for procurement, installation, and ongoing maintenance. Large-format LED screens demand specialized infrastructure, skilLED technicians, and advanced control systems. It becomes difficult for smaller venues and community stadiums to justify the upfront expenditure. Maintenance costs rise due to the need for periodic calibration, replacement of damaged modules, and software updates. Harsh weather conditions can accelerate wear, leading to higher repair expenses. The financial burden often limits adoption to well-funded stadiums and event organizers.

Rapid Technological Obsolescence and Supply Chain Vulnerabilities

The LED Stadium Screens Market must contend with the fast pace of technological advancements in display resolution, brightness, and energy efficiency. Equipment purchased today can become outdated within a few years, pressuring venue operators to reinvest sooner than planned. It also faces supply chain risks from disruptions in the availability of LED chips, control boards, and other critical components. Global logistics delays and price volatility for electronic parts can affect project timelines and budgets. Dependency on a limited number of specialized suppliers heightens procurement risks. Managing obsolescence while ensuring consistent product availability remains a complex operational challenge.

Market Opportunities

Rising Global Investments in Sports and Entertainment Infrastructure

The LED Stadium Screens Market has strong growth potential supported by increasing investments in new stadium construction and modernization projects worldwide. Governments, sports organizations, and private investors prioritize high-quality visual displays to enhance spectator engagement. It can benefit from large-scale international events such as the FIFA World Cup, Olympics, and major music festivals, which require advanced screen installations. Demand extends to multipurpose arenas that host sports, concerts, and corporate events. Suppliers offering customized screen sizes, modular designs, and high-resolution technology can secure long-term contracts. This infrastructure expansion creates consistent opportunities across developed and emerging markets.

Expansion of Rental and Temporary Event Solutions

The LED Stadium Screens Market can leverage opportunities in the growing rental segment for temporary events, tournaments, and festivals. Event organizers prefer high-quality, quick-installation LED screens to meet short-term needs without heavy capital investment. It can capture this demand by providing portable, weather-resistant, and easily transportable display systems. Rental service providers investing in advanced LED technology can target diverse events beyond sports, including cultural shows and political gatherings. Partnerships with event management companies can strengthen recurring revenue streams. The versatility of temporary solutions expands the market reach beyond permanent stadium installations.

Market Segmentation Analysis:

By Screen Resolution

The LED Stadium Screens Market segments into 1080p, 4K, and 8K resolution categories. 1080p displays continue to find adoption in stadiums that prioritize durability and proven technology over the highest resolution standards, particularly in mid-tier sports venues and community arenas. 4K resolution dominates new installations in large and mid-sized stadiums, delivering enhanced visual clarity and vibrant color reproduction that meet the demands of sponsors, broadcasters, and spectators. It offers an optimal balance between visual performance and cost-efficiency, making it the preferred choice for many upgrading projects. 8K resolution, while still representing a smaller share, is gaining visibility in flagship stadiums hosting global sporting events. It enables ultra-high-definition imagery with exceptional detail, which is especially valuable for close-up action replays and immersive fan experiences in venues exceeding 60,000 seating capacity.

- For instance, the new LED scoreboard at Yankee Stadium is a Mitsubishi Diamond Vision 1080p display measuring 103 × 58 feet, comprised of 8,601,600 individual LEDs—exceeding 8 million LEDs.

By Display Size

Screen size plays a decisive role in audience engagement and content delivery. Below 500 sq ft screens are used in training facilities, community stadiums, and smaller arenas where audience sizes and viewing distances do not require expansive displays. The 500–1000 sq ft range is prevalent in regional stadiums and medium-capacity venues, supporting both live event visuals and sponsorship displays without requiring major structural modifications. Over 1000 sq ft screens dominate high-profile stadiums and multipurpose sports complexes. These large-format installations support split-screen capabilities, live game feeds, multi-angle replays, and synchronized advertising across multiple display zones, providing a more immersive viewing environment for tens of thousands of spectators.

- For instance, Samsung upgraded Minute Maid Park’s display technology, installing a main scoreboard, ribbon boards, and a left-field display. The main scoreboard is 6,875 square feet and features 5.3 million LEDs, while the ribbon boards add 45,000 square feet of display space. The left-field display is 1,000 square feet.

By Installation Type

Installation type varies based on venue design and operational needs. Fixed installations dominate in stadiums with permanent seating and consistent year-round events, offering the best long-term reliability and structural integration. Retractable screens are increasingly adopted in multipurpose venues, allowing operators to adjust visibility and positioning based on event type. Mobile screens provide unmatched flexibility for temporary tournaments, fan zones, and touring entertainment events, with rapid setup and teardown capabilities that minimize logistical downtime.

Segments:

Based on Screen Resolution:

Based on Display Size:

- Below 500 sq ft

- 500-1000 sq ft

- Over 1000 sq ft

Based on Installation Type:

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds around 34% of the LED Stadium Screens Market, making it one of the largest regional contributors. The United States and Canada have a strong tradition of investing in advanced sports infrastructure, which directly drives demand for high-quality stadium screens. Large professional leagues such as the NFL, NBA, MLB, and NHL use advanced LED displays for advertising, instant replays, fan engagement, and live event coverage. Many stadiums in this region have already upgraded to 4K and are exploring 8K technology for a better viewing experience. The presence of major manufacturers and technology providers in North America ensures quick adoption of the latest innovations, making it a leader in this market segment.

Asia Pacific

Asia Pacific leads with the largest share at approximately 35%. This dominance comes from rapid urban development, strong government investment in sports facilities, and the hosting of major global events. China, Japan, India, South Korea, and Australia are key markets where stadium modernization projects are increasing. The demand for LED screens in this region covers both large stadiums and smaller venues, including esports arenas. Local manufacturing capabilities also help reduce costs and improve access to advanced display technologies. Growing interest in cricket, football, and large-scale entertainment events continues to boost demand. The region’s scale and fast adoption make it a central growth driver for the market.

Europe

Europe holds about 20% of the global market. Football stadiums in the UK, Germany, France, Spain, and Italy are major consumers of LED stadium screens. The region has a mature sports infrastructure, with most large venues already equipped with high-resolution displays. Many projects now focus on upgrading existing systems to better support digital advertising, multi-camera broadcasting, and interactive fan experiences. Europe also has strong environmental regulations, leading to demand for energy-efficient LED screens. The combination of long-established sports culture and high expectations for visual quality ensures stable demand.

Latin America

Latin America has a smaller share at around 3%, but it is a growing market. Countries like Brazil, Mexico, and Argentina are upgrading stadiums for football, which is the most popular sport in the region. Investments often increase before major tournaments such as Copa América and FIFA events. While budgets are smaller compared to other regions, the demand for mid-size, high-brightness LED screens is rising as more venues aim to improve fan engagement and sponsorship opportunities.

Middle East & Africa

The Middle East & Africa hold about 2% of the market. Growth is LED by large-scale projects in countries like Qatar, Saudi Arabia, and the UAE, which invest heavily in sports infrastructure to host global events. Africa’s demand is more concentrated in South Africa and parts of North Africa, where major stadiums are undergoing modernization. While the market size is currently smaller, ongoing construction and event hosting are expected to increase adoption in the coming years.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- ROE Visual

- AOTO Electronics

- Hisense Visual Technology

- LianTronics

- Samsung Electronics

- Leyard

- Panasonic

- Absen

- Shenzhen Absen Optoelectronics

- Mitsubishi Electric

Competitive Analysis

The LED Stadium Screens Market features with key players including ROE Visual, AOTO Electronics, Hisense Visual Technology, LianTronics, Samsung Electronics, Leyard, Panasonic, Absen, Shenzhen Absen Optoelectronics, and Mitsubishi Electric. The LED Stadium Screens Market operates in a highly competitive environment where technological innovation, performance reliability, and customization capabilities determine market leadership. Industry participants focus on delivering displays that combine high brightness, fine pixel pitch, and wide viewing angles to ensure excellent visibility in both daylight and low-light conditions. Energy efficiency has become a central competitive factor, with manufacturers developing LED systems that reduce power consumption while maintaining consistent luminance and color accuracy over long operating hours. Durability and weather resistance are equally critical, as stadium installations must withstand rain, dust, and extreme temperatures without compromising performance. Companies differentiate themselves by offering integrated solutions that go beyond the display hardware, including advanced content management systems, remote monitoring capabilities, and compatibility with broadcast production workflows. The ability to deliver large-scale installations within tight deadlines is a significant advantage, particularly for venues preparing for global sporting events. Service offerings such as on-site technical support, extended warranties, and maintenance contracts further enhance brand loyalty.

Recent Developments

- In March 2025, Leyard showcased its new-generation MG-COB Cold Screen Series at the ISLE 2025 exhibition. This series integrates advanced Micro LED technology with energy-efficient constant current driving chips, offering softer light emission and significantly reduced energy consumption with surface.

- In March 2025, Unilumin Group Co., Ltd. (China) launched its next-gen outdoor LED screen series with improved energy efficiency and 8K resolution, targeting smart stadium applications.

- In February 2025, Barco NV (Belgium) introduced a new range of energy-efficient LED perimeter displays optimized for high ambient light conditions.

- In September 2024, Daktronics Inc. (USA) installed one of the largest 4K HDR LED video boards in a U.S. football stadium, enhancing fan engagement and advertising revenue.

Market Concentration & Characteristics

The LED Stadium Screens Market demonstrates a moderately concentrated structure, with a mix of global leaders and regional specialists competing for large-scale projects. It features established manufacturers with strong technological capabilities, extensive distribution networks, and proven experience in delivering high-performance, large-format displays for sports venues. The market is characterized by high entry barriers due to substantial capital requirements, advanced engineering expertise, and the need for long-term relationships with stadium operators and event organizers. It places strong emphasis on image quality, durability, and integration with broadcasting and content management systems. Product differentiation often centers on resolution, pixel pitch, energy efficiency, and weather resistance, with suppliers investing in research and development to enhance these attributes. Competition remains intense, as operators demand turnkey solutions that combine hardware, software, and after-sales support. It benefits from the ongoing modernization of sports infrastructure and the growing importance of fan engagement, which drive demand for dynamic, high-brightness, and large-scale LED installations across global markets.

Report Coverage

The research report offers an in-depth analysis based on Screen Resolution, Display Size, Installation Type and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand will grow for higher resolution screens, including 8K, to enhance live viewing experiences in large venues.

- Energy-efficient LED technologies will gain more adoption to reduce operational costs and meet sustainability goals.

- Integration with advanced content management systems will improve real-time control and display flexibility.

- Mobile and modular LED solutions will see higher demand for temporary events and multi-use stadiums.

- Manufacturers will focus on reducing pixel pitch to deliver sharper visuals at closer viewing distances.

- Weather-resistant and long-life designs will become standard for outdoor stadium applications.

- Partnerships between screen manufacturers and sports leagues will increase to secure long-term installation contracts.

- Interactive features such as live social media feeds and fan engagement tools will be integrated into display systems.

- Regional markets with ongoing stadium construction will drive new installation opportunities.

- Competition will intensify around turnkey solutions that combine hardware, software, and maintenance services.