Market Overview:

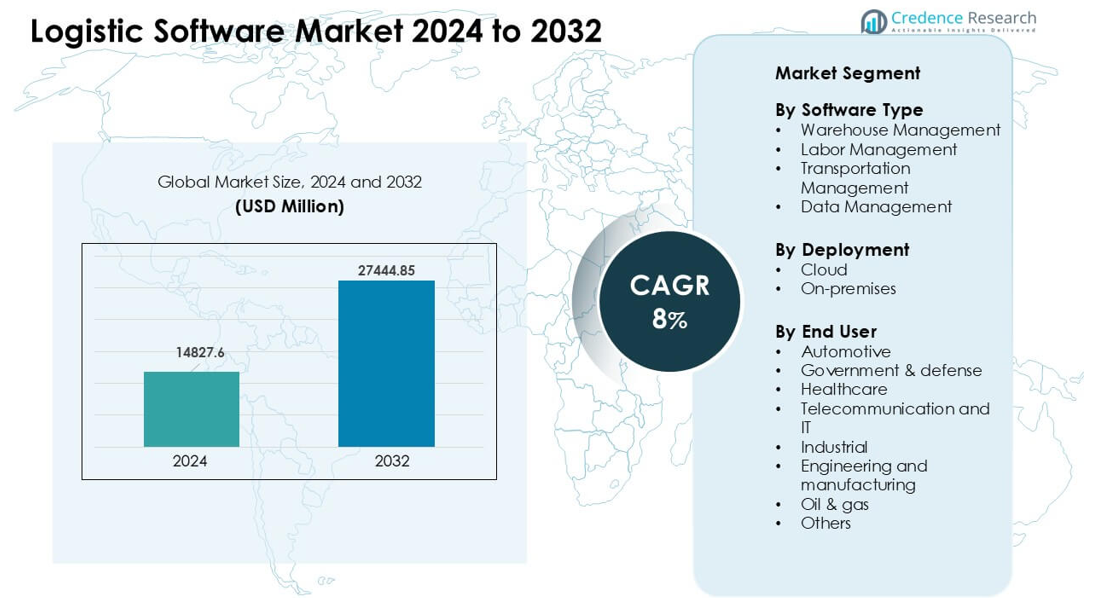

Logistic Software Market was valued at USD 14827.6 million in 2024 and is anticipated to reach USD 27444.85 million by 2032, growing at a CAGR of 8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Logistic Software Market Size 2024 |

USD 14827.6 million |

| Logistic Software Market, CAGR |

8% |

| Logistic Software Market Size 2032 |

USD 27444.85 million |

The logistic software market is shaped by major players such as SAP SE, Manhattan Associates, Körber AG & Infor, IBM Corporation, Oracle, The Descartes Systems Group, FarEye, LogiNext Solutions, WiseTech Global, and Alvys Inc. These vendors compete by offering advanced warehouse, transport, and visibility solutions that support real-time tracking and faster decision-making across global supply chains. Cloud deployment, automation, and AI-driven optimization remain key focus areas for product growth. North America emerged as the leading region with about 36% share, supported by strong digital adoption, high e-commerce activity, and significant investment in next-generation logistics platforms.

Market Insights:

- The logistic software market reached a significant value at USD 14827.6 million in 2024 and is projected to grow steadily by 2032 at a strong CAGR of 8%, supported by rising automation and cloud adoption across supply chains.

- Growth is driven by real-time visibility needs, fast e-commerce expansion, and increased demand for advanced warehouse and transport management tools.

- Key trends include wider use of AI forecasting, predictive analytics, and sustainability-focused routing that helps lower emissions and improve delivery efficiency.

- Competition remains strong as SAP SE, Manhattan Associates, Oracle, IBM, and others enhance cloud platforms, integration features, and automation capabilities for higher performance.

- North America led with about 36% share, followed by Europe at 29% and Asia-Pacific at 27%, while warehouse management held the largest segment share due to high adoption in retail, 3PL, and manufacturing operations.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Software Type

Warehouse management held the dominant share at about 38%. Many firms adopted these tools to gain better control over inventory, picking, and real-time tracking. Strong interest came from e-commerce players who needed quicker order cycles. Transportation management grew as companies aimed to cut freight costs and improve routing. Labor management advanced in large warehouses due to rising pressure to boost workforce output. Data management expanded as logistics teams used analytics to support planning, demand forecasting, and network visibility.

- For instance, a recent industry survey found that 89% of organizations surveyed planned to use modernized Warehouse Management System (WMS) functionality for labor planning and management by the end of 2024, indicating a strong trend toward technology adoption to track labor efficiency across fulfillment centers.

By Deployment

Cloud deployment led this segment with nearly 64% share. Businesses selected cloud systems for faster updates, lower setup needs, and easy scaling during peak demand. Many operators used cloud modules to connect warehouses, fleet systems, and partner networks in real time. On-premises solutions stayed relevant where strict security rules or legacy systems limited migration. Growth in global trade, rising shipment volumes, and remote access needs helped cloud platforms maintain the leading position.

- For instance, in 2023, while the majority of new adoptions globally were for cloud-based WMS, a significant number of organizations in sectors like pharmaceuticals, manufacturing, or regulated inventory continued to opt for on-premise or hybrid solutions, preferring greater local control over data and infrastructure to meet strict regulatory compliance and security standards.

By End User

Automotive emerged as the leading end-user segment with around 22% share. Carmakers relied on advanced logistics tools to manage complex supply chains, track components, and support just-in-time production. Healthcare usage grew as providers required stronger cold-chain control and shipment traceability. Government and defense agencies deployed secure systems for mission-critical logistics. Telecom, IT, industrial, and manufacturing groups adopted software to cut delays and improve delivery accuracy. Oil and gas companies used logistics platforms to support field operations and asset movement across remote sites.

Key Growth Drivers:

Rising Need for Real-Time Supply Chain Visibility

Real-time visibility acts as a major growth driver as companies face tighter delivery windows and higher customer expectations. Many logistics teams now depend on platforms that track inventory, fleet status, and shipment conditions across large networks. Faster decision-making reduces delays and lowers error rates, while predictive alerts help avoid disruptions caused by traffic, weather, or supply shortages. E-commerce growth also pushes firms to monitor parcels at every stage. These factors increase demand for integrated software that connects warehouses, carriers, and distribution partners on a single platform. Strong interest in accuracy and speed keeps visibility tools at the center of industry expansion.

- For instance, according to a 2024 survey by Tive, the share of respondents using IoT‑enabled devices for real-time shipment tracking increased from 25% to 53% in just one year demonstrating a sharp acceleration in visibility adoption across shippers and carriers globally.

Expansion of E-Commerce and Omnichannel Distribution

The rapid rise of online retail drives strong adoption of advanced logistics software. Retailers face heavy order volumes and need systems that support quick fulfillment, automated sorting, and smooth returns. Omnichannel operations add more pressure as companies combine store pickup, same-day delivery, and direct-to-customer shipping. Logistic software helps maintain stock accuracy, reduce last-mile delays, and ensure consistent delivery quality. Many brands also invest in tools that improve peak-season planning and warehouse throughput. As digital buying grows in both urban and rural areas, software becomes essential to handle complex routing and demand swings, pushing steady market growth.

- For instance, many newer logistics and visibility platforms launched by 2025 incorporate AI‑driven predictive analytics alongside IoT-based tracking enabling companies to better anticipate demand surges, route changes, or inventory shortages, which is critical for omnichannel operations that mix store‑pickup, home delivery and returns.

Increasing Automation Across Warehousing and Transportation

Automation fuels strong demand for logistics software as companies replace manual workflows to cut cost and raise output. Modern tools support coordinated use of robotics, automated guided vehicles, and smart conveyors inside warehouses. Transportation modules help optimize routes, reduce fuel use, and manage driver schedules. Growing pressure to meet tight service-level targets encourages firms to automate repetitive tasks such as order allocation, label generation, and load planning. Rising labor shortages in many countries also drive adoption of automated systems. As more operators integrate sensors and connected equipment, logistics software becomes the backbone that links hardware with planning and execution processes.

Key Trends & Opportunities:

Growth of AI and Predictive Analytics

AI adoption expands as firms use predictive tools to improve planning accuracy and reduce operational waste. Many logistics teams rely on machine learning to forecast demand, detect bottlenecks, and optimize distribution networks. Predictive models help prevent stockouts, lower buffer inventory, and improve fleet uptime. Real-time analytics support decisions during disruptions and allow faster re-routing. These capabilities create new opportunities for vendors offering integrated intelligence layers across warehouse, transport, and labor systems. Rising data availability from sensors, GPS, and order flows strengthens the shift toward AI-enabled optimization.

- For instance, the PwC 2025 Digital Trends in Operations Survey found that around 57% of operations and supply chain leaders have integrated AI into selected functions or throughout their organization. Alternatively, a Gartner study conducted in August 2024 (for 2025 insights) noted that 71% of companies reported using generative AI, moving beyond the pilot stage in many supply chain functions.

Rising Demand for Sustainable Logistics Operations

Sustainability trends create fresh opportunities as companies aim to cut emissions and meet environmental rules. Software providers now offer carbon-tracking dashboards, load-optimization tools, and route-efficiency modules that help reduce fuel use. Many brands adopt green distribution practices, including consolidated shipping and optimized warehouse layouts. Governments also introduce stricter emission norms that push logistics players to upgrade digital systems. Firms see sustainability not only as compliance but also as a way to lower cost and improve brand value. These shifts create strong long-term momentum for eco-focused logistics software.

- For instance, a 2025 study documented that AI‑driven route optimization in logistics using real‑time traffic, weather, and vehicle data can reduce fuel consumption and associated emissions markedly compared to baseline routing.

Key Challenges:

Cybersecurity and Data Privacy Risks

Rising digital adoption increases exposure to cyberattacks, making security a major challenge. Logistics networks store sensitive data on inventory, customers, routing, and transactions, which can attract threats. Breaches disrupt operations, delay shipments, and raise recovery costs. Many small and mid-size firms lack strong security budgets, which widens risk. Complex supplier networks also create more access points for attackers. Vendors must invest in encryption, access controls, and continuous monitoring to protect users. Without strong cybersecurity, digital adoption in logistics faces slowdowns.

High Integration and Implementation Costs

Integration challenges impact market growth as many companies run mixed legacy systems that require complex upgrades. Implementing warehouse, transport, and analytics platforms often needs skilled teams and careful data mapping. High setup costs deter smaller operators, especially in regions with limited digital budgets. Downtime during transition also affects adoption. Some firms avoid full-scale transformation due to fear of workflow disruption. Vendors must offer flexible pricing, modular deployments, and strong support to improve adoption rates and reduce the burden of integration.

Regional Analysis:

North America

North America held the largest share at about 36% due to strong digital adoption across transport, retail, and manufacturing sectors. Many firms in the United States and Canada deployed advanced warehouse and transport management systems to improve service levels and control operating costs. High e-commerce penetration increased the need for real-time tracking, automated routing, and demand forecasting. Logistics providers also invested in cloud platforms to support multi-site operations and cross-border shipping. A strong ecosystem of software vendors, 3PL companies, and technology partners helped the region sustain its leadership position in 2024.

Europe

Europe captured nearly 29% share, driven by strict regulatory frameworks, rising sustainability goals, and strong logistics networks across major economies. Companies in Germany, the U.K., France, and the Netherlands adopted advanced planning and visibility tools to meet compliance needs and improve delivery accuracy. Green logistics programs encouraged firms to use software that reduces emissions, optimizes loads, and supports multimodal transport. Expanding cross-border trade and e-commerce also increased reliance on integrated management platforms. Widespread digital transformation across manufacturing and retail sectors helped strengthen regional growth.

Asia-Pacific

Asia-Pacific accounted for roughly 27% share and showed the fastest growth due to rapid industrial expansion and rising online retail volumes. China, India, Japan, and Southeast Asia invested heavily in cloud-based logistics tools to support large-scale distribution, warehouse automation, and last-mile delivery. Growing demand for real-time tracking, reverse logistics, and route optimization drove strong software uptake. Many firms upgraded systems to handle fluctuating demand and large inventory flows. Government programs supporting digital infrastructure and smart logistics hubs further boosted adoption across the region.

Latin America

Latin America held close to 5% share, supported by expanding retail activity and broader logistics modernization efforts in Brazil, Mexico, and Colombia. Companies increased investment in transport management and warehouse automation to reduce delivery delays and improve cost control. E-commerce growth encouraged firms to adopt tracking tools and route-optimization systems. However, uneven digital infrastructure and high deployment costs limited faster uptake in smaller markets. Despite these challenges, rising interest in cloud software and last-mile improvement programs supported steady regional momentum.

Middle East & Africa

The Middle East & Africa region captured about 3% share, driven by logistics upgrades linked to growing trade activity and infrastructure development in the UAE, Saudi Arabia, and South Africa. Firms adopted software to enhance fleet coordination, warehouse efficiency, and cross-border movement. Investments in free-trade zones, smart ports, and e-commerce hubs helped increase demand for visibility and planning tools. Adoption remained slower in developing markets due to limited budgets and lower digital maturity. Still, expanding logistics corridors and rising demand for automated systems supported gradual growth.

Market Segmentations:

By Software Type

- Warehouse Management

- Labor Management

- Transportation Management

- Data Management

By Deployment

By End User

- Automotive

- Government & defense

- Healthcare

- Telecommunication and IT

- Industrial

- Engineering and manufacturing

- Oil & gas

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape:

The competitive landscape of the logistic software market features leading players such as SAP SE, Manhattan Associates, Körber AG & Infor, IBM Corporation, Oracle, The Descartes Systems Group, FarEye, LogiNext Solutions, WiseTech Global, and Alvys Inc. These companies compete by offering integrated warehouse, transport, labor, and visibility platforms that support end-to-end supply chain control. Many vendors expand their reach through cloud-based deployments that enable faster updates, easier scaling, and smooth connectivity across global networks. Firms also invest in AI, automation, and predictive analytics to raise forecasting accuracy and cut operational waste. Strategic partnerships with 3PLs, retailers, manufacturers, and e-commerce providers help strengthen adoption. Continuous upgrades in route optimization, real-time tracking, and multimodal planning allow these players to maintain strong customer retention in a highly competitive environment.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- SAP SE (Germany)

- Manhattan Associates (U.S.)

- Körber AG & Infor (Germany)

- IBM Corporation (U.S.)

- The Descartes Systems Group, Inc. (Canada)

- Oracle (U.S.)

- FarEye (U.S.)

- LogiNext Solutions (U.S.)

- WiseTech Global (Australia)

- Alvys Inc. (U.S.)

Recent Developments:

- In November 2025, SAP publicly surfaced major supply-chain / logistics moves at its 2025 events and product updates, pushing agentic AI & AI-native automation into supply-chain workflows (SAP announced new Joule/agent capabilities and showcased Supply Chain Connect updates), while also facing a high-profile trade-secrets lawsuit filed against it in the U.S. in late Nov 2025.

- In October 2025, Infor continued rolling out supply-chain and logistics enhancements (Infor Nexus/Distribution Management and Industry AI Agents were highlighted in 2024–2025 product communications and at Infor Nexus Connect in Oct 2025), emphasising network orchestration, embedded AI agents for SCM, and tighter ERP→WMS integration.

- In March 2025, Körber rebranded its supply-chain software business (including the combined strengths of Körber Supply Chain Software and MercuryGate) under a new brand Infios (public announcement in early March 2025) a strategic move to consolidate TMS/WMS/transport capabilities and position the unit for broader global go-to-market in logistics software. Körber also promoted new smart-logistics showcases at events such as LogiMAT 2025.

Report Coverage:

The research report offers an in-depth analysis based on Software Type, Deployment, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market

Future Outlook:

- Demand for real-time visibility tools will rise as supply chains grow more complex.

- Cloud-based platforms will expand as firms seek faster scaling and lower setup needs.

- AI-driven forecasting will improve planning accuracy and reduce operational delays.

- Automation inside warehouses and transport will increase to counter labor shortages.

- Sustainability features will gain adoption as companies aim to cut emissions.

- Last-mile optimization tools will grow due to higher e-commerce delivery pressure.

- Integrated dashboards will strengthen decision-making across multi-site operations.

- Cybersecurity upgrades will become essential as digital logistics networks expand.

- Partnerships between software vendors and 3PL providers will increase to support wider use.

- Emerging markets will adopt modern systems faster due to rising trade and industrial growth.