| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Turkey Diabetes Drugs Market Size 2023 |

USD 510.09 Million |

| Turkey Diabetes Drugs Market, CAGR |

1.20% |

| Turkey Diabetes Drugs Market Size 2032 |

USD 589.38 Million |

Market Overview

Turkey Diabetes Drugs Market size was valued at USD 510.09 million in 2023 and is anticipated to reach USD 589.38 million by 2032, at a CAGR of 1.20% during the forecast period (2023-2032).

The Turkey diabetes drugs market is driven by the rising prevalence of diabetes, increasing awareness of early diagnosis, and advancements in treatment options. The growing aging population and sedentary lifestyles contribute to higher diabetes incidence, fueling demand for innovative therapies. Government initiatives supporting diabetes management and healthcare infrastructure improvements further accelerate market growth. Additionally, the adoption of novel drug classes, such as GLP-1 receptor agonists and SGLT-2 inhibitors, is reshaping treatment paradigms. The expansion of biosimilars and cost-effective alternatives enhances market accessibility. Pharmaceutical companies are investing in research and development to introduce personalized treatment solutions, improving patient outcomes. Digital health integration, including telemedicine and continuous glucose monitoring systems, is also gaining traction, optimizing diabetes management. However, pricing pressures and regulatory challenges remain key hurdles. Despite these constraints, the market is expected to experience steady growth, driven by technological advancements and evolving treatment approaches.

Geographically, the Turkey diabetes drugs market is concentrated in major urban centers such as Istanbul, Ankara, and Izmir, where the demand for advanced diabetes treatments is higher due to the large population and better healthcare infrastructure. These cities are home to a significant portion of the diabetic population, driving the growth of innovative drug classes and advanced treatment options. In rural areas, the market is expanding as healthcare access improves and awareness about diabetes management rises. Key players in the Turkish diabetes drugs market include multinational pharmaceutical companies like Novo Nordisk A/S, Sanofi, Merck & Co., Inc., Eli Lilly and Company, and AstraZeneca, all of which offer a wide range of insulin, oral antidiabetic medications, and newer drug classes such as GLP-1 receptor agonists and SGLT2 inhibitors. These companies are continuously innovating and expanding their portfolios to meet the growing demand for diabetes care in Turkey.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Turkey diabetes drugs market was valued at USD 510.09 million in 2023 and is expected to reach USD 589.38 million by 2032, growing at a CAGR of 1.20% during the forecast period.

- Increasing diabetes prevalence, driven by sedentary lifestyles and aging populations, is a primary market driver.

- Adoption of innovative drug classes, such as GLP-1 receptor agonists and SGLT2 inhibitors, is reshaping treatment paradigms.

- The rise in biosimilar insulin and cost-effective alternatives is enhancing market accessibility.

- Competitive landscape includes key players like Novo Nordisk, Sanofi, Merck, Eli Lilly, and AstraZeneca, focusing on advanced drug therapies and market expansion.

- Market restraints include regulatory challenges, pricing pressures, and the affordability of new treatments.

- The market is highly concentrated in Istanbul, Ankara, and Izmir, with rural regions showing growing demand due to improved healthcare access.

Report Scope

This report segments the Turkey Diabetes Drugs Market as follows:

Market Drivers

Market Drivers

Rising Prevalence of Diabetes and Aging Population

The increasing incidence of diabetes in Turkey is a major driver of the diabetes drugs market. Changing lifestyles, unhealthy dietary habits, and rising obesity rates contribute significantly to the growing diabetic population. For instance, the International Diabetes Federation (IDF) reported that 15.9% of adults in Turkey were living with diabetes as of 2021, with over 9 million cases documented. Additionally, Turkey’s aging population further escalates the demand for diabetes management solutions. Older adults are at a higher risk of developing diabetes, leading to an increased need for effective treatment options. As a result, pharmaceutical companies are expanding their product portfolios to cater to this growing patient base.

Government Initiatives and Healthcare Infrastructure Development

The Turkish government is actively supporting diabetes management through various healthcare programs and policies. Investments in public healthcare infrastructure, including diabetes care centers and reimbursement schemes, are improving patient access to essential medications. For instance, the Social Security Institution (SGK) subsidizes essential diabetes medications, ensuring affordability for patients across the country. Additionally, national awareness campaigns emphasize early diagnosis and disease management, encouraging individuals to seek timely medical intervention. These initiatives collectively boost market demand by ensuring better accessibility and affordability of diabetes medications across Turkey.

Advancements in Drug Development and Treatment Innovations

Technological advancements in diabetes drug development are reshaping the market landscape. The introduction of novel drug classes, such as GLP-1 receptor agonists, SGLT-2 inhibitors, and DPP-4 inhibitors, provides more effective treatment options with fewer side effects. These innovations enhance patient compliance and improve overall disease management. Furthermore, the rise of biosimilars and cost-effective alternatives is increasing competition among pharmaceutical companies, leading to more accessible treatment options. Ongoing research and development efforts continue to focus on personalized medicine, targeting specific patient needs and improving long-term health outcomes.

Integration of Digital Health and Telemedicine

The growing adoption of digital health technologies is transforming diabetes management in Turkey. Continuous glucose monitoring (CGM) systems, smart insulin pens, and telemedicine services are becoming integral to diabetes care. These digital solutions allow for real-time monitoring and remote consultations, enhancing treatment efficiency and patient convenience. The COVID-19 pandemic accelerated the shift toward telehealth, encouraging patients and healthcare providers to embrace digital platforms. As technology continues to evolve, its integration with diabetes drug therapies is expected to further drive market growth, improving patient adherence and overall disease control.

Market Trends

Increasing Adoption of Novel Drug Classes

The Turkey diabetes drugs market is witnessing a significant shift toward innovative treatment options, with growing adoption of novel drug classes such as GLP-1 receptor agonists, SGLT-2 inhibitors, and DPP-4 inhibitors. These advanced therapies offer improved glycemic control, cardiovascular benefits, and reduced side effects compared to traditional insulin and oral hypoglycemics. For instance, the Turkish Ministry of Health has endorsed the use of SGLT-2 inhibitors for their proven cardiovascular benefits, particularly in patients with type 2 diabetes and heart disease. As healthcare providers prioritize patient-centric approaches, these drugs are becoming more prevalent in treatment regimens. The rising awareness among physicians and patients about their efficacy and long-term benefits is further fueling market demand.

Expansion of Biosimilars and Cost-Effective Alternatives

The increasing focus on cost-effective treatment options is driving the expansion of biosimilars in the Turkish diabetes drugs market. For instance, the Medicines and Medical Devices Agency of Turkey (TITCK) has streamlined the approval process for biosimilar insulin products, ensuring their timely availability in the market. Biosimilar insulin and oral diabetes drugs provide comparable efficacy at lower prices, improving accessibility for a broader patient population. Pharmaceutical companies are actively investing in biosimilar development, creating a competitive market landscape that encourages affordability without compromising treatment quality. This trend is expected to continue as regulatory frameworks evolve to support biosimilar adoption.

Growing Integration of Digital Health Solutions

The integration of digital health technologies with diabetes drug therapies is becoming a key trend in Turkey. Smart insulin pens, continuous glucose monitoring (CGM) systems, and mobile health applications are enhancing diabetes management by providing real-time monitoring and personalized treatment adjustments. The increasing use of telemedicine and remote consultations is also facilitating better patient engagement and medication adherence. This shift toward digital healthcare solutions aligns with global trends, making diabetes treatment more efficient and accessible. As technology advances, pharmaceutical companies and healthcare providers are expected to collaborate further in developing integrated diabetes care solutions.

Regulatory Reforms and Market Expansion

Regulatory improvements and evolving healthcare policies are playing a crucial role in shaping Turkey’s diabetes drugs market. The government is actively working to streamline drug approval processes and enhance reimbursement policies to ensure wider patient access to innovative therapies. Additionally, multinational pharmaceutical companies are expanding their presence in Turkey, either through partnerships with local firms or direct market entry. These developments are fostering a competitive landscape, encouraging the introduction of new and advanced diabetes medications. As regulatory frameworks continue to adapt to market demands, Turkey is poised to become a key player in the regional diabetes drugs market.

Market Challenges Analysis

Pricing Pressures and Reimbursement Constraints

One of the key challenges in the Turkey diabetes drugs market is the pressure on drug pricing and reimbursement policies. The government, through the Social Security Institution (SGK), regulates drug prices to ensure affordability, but this often limits the profitability of pharmaceutical companies. Strict pricing controls and frequent revisions to reimbursement policies create financial constraints for manufacturers, affecting their ability to invest in research and development. Additionally, the increasing demand for cost-effective treatment options has led to greater competition among generic and biosimilar drug manufacturers, further squeezing profit margins. These financial challenges may slow the introduction of innovative therapies, limiting patient access to advanced diabetes treatments.

Regulatory and Market Access Barriers

The regulatory landscape in Turkey presents significant challenges for diabetes drug manufacturers. Lengthy approval processes and complex market entry requirements can delay the launch of new medications. For instance, the Turkish Medicines and Medical Devices Agency (TITCK) requires extensive clinical trial data and economic evaluations before granting market approval, which can extend timelines for new drug introductions. Moreover, economic fluctuations and currency depreciation impact the cost of imported drugs, making it difficult for international manufacturers to maintain stable pricing. Market access barriers, coupled with bureaucratic hurdles, create uncertainties for pharmaceutical firms looking to expand in Turkey. Overcoming these regulatory constraints will be crucial for ensuring continuous innovation and the availability of high-quality diabetes drugs in the market.

Market Opportunities

The Turkey diabetes drugs market presents significant opportunities driven by the increasing prevalence of diabetes and advancements in treatment options. As the diabetic population grows due to changing lifestyles, aging demographics, and rising obesity rates, the demand for innovative and effective therapies continues to expand. Pharmaceutical companies have the opportunity to introduce advanced drug classes, such as GLP-1 receptor agonists and SGLT-2 inhibitors, which offer improved efficacy and additional cardiovascular benefits. Additionally, the growing acceptance of biosimilars provides a cost-effective alternative to expensive branded drugs, improving accessibility for a larger patient base. With the Turkish government actively supporting healthcare infrastructure development and reimbursement programs, companies can leverage these initiatives to enhance patient access and market penetration.

The integration of digital health solutions and telemedicine further strengthens market opportunities. Smart insulin pens, continuous glucose monitoring (CGM) systems, and mobile health applications are revolutionizing diabetes management, enabling real-time monitoring and personalized treatment adjustments. Pharmaceutical companies can collaborate with technology firms to develop integrated healthcare solutions that enhance patient adherence and overall disease control. Moreover, Turkey’s strategic location as a bridge between Europe and Asia presents an opportunity for multinational companies to establish regional operations and expand their footprint in the broader Middle East and North Africa (MENA) market. With ongoing regulatory reforms and an evolving healthcare landscape, the Turkey diabetes drugs market offers a promising environment for growth, innovation, and investment.

Market Segmentation Analysis:

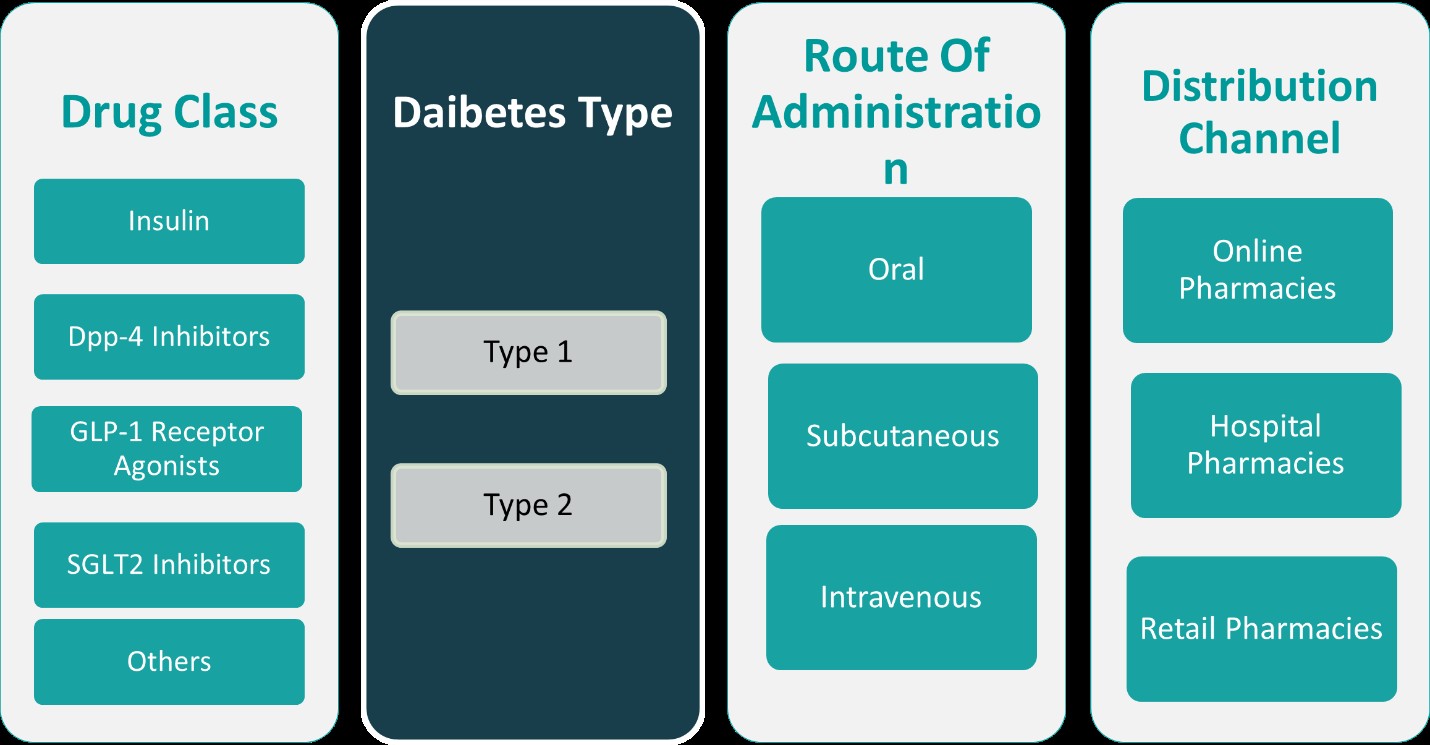

By Drug Class:

The Turkey diabetes drugs market is segmented based on drug class, including insulin, DPP-4 inhibitors, GLP-1 receptor agonists, SGLT2 inhibitors, and other diabetes medications. Insulin remains a dominant segment due to its essential role in managing Type 1 and advanced Type 2 diabetes. With the growing diabetic population, the demand for rapid-acting, long-acting, and biosimilar insulin formulations continues to rise. DPP-4 inhibitors, known for their ability to improve glycemic control with minimal side effects, are widely prescribed for Type 2 diabetes patients. The market for GLP-1 receptor agonists is expanding, driven by their efficacy in lowering blood sugar levels while providing cardiovascular benefits. SGLT2 inhibitors are gaining traction due to their dual advantage of glucose control and heart failure risk reduction, making them a preferred choice among healthcare providers. Other diabetes drugs, including traditional oral antidiabetic agents and combination therapies, contribute to market growth by offering alternative treatment options tailored to patient needs.

By Diabetes Types:

The diabetes drugs market in Turkey is also categorized by diabetes type, including Type 1, Type 2, and rarer forms such as Type 3, Type 4, and Type 5 diabetes. Type 2 diabetes dominates the market, accounting for the largest share due to its high prevalence among the adult population. The increasing incidence of obesity, sedentary lifestyles, and genetic predisposition continues to drive demand for a broad range of oral and injectable antidiabetic medications. Type 1 diabetes, though less common, requires lifelong insulin therapy, sustaining the demand for both traditional and biosimilar insulin products. Type 3 diabetes, associated with Alzheimer’s disease and insulin resistance in the brain, is an emerging area of research, presenting new opportunities for pharmaceutical innovation. Type 4 diabetes, often linked to aging-related insulin resistance, is gaining recognition, emphasizing the need for tailored treatment strategies. Type 5 diabetes, characterized by rare genetic disorders affecting insulin regulation, represents a niche segment with potential for specialized drug development.

Segments:

Based on Drug Class:

- Insulin

- DPP-4 Inhibitors

- GLP-1 Receptor Agonists

- SGLT2 Inhibitors

- Others

Based on Diabetes Types:

- Type 1

- Type 2

- Diabetes Type 3

- Diabetes Type 4

- Diabetes Type 5

Based on Route of Administration:

- Oral

- Subcutaneous

- Intravenous

- Route of Administration 4

- Route of Administration 5

Based on Technology:

- Technology 1

- Technology 2

- Technology 3

Based on Distribution Channel:

- Online Pharmacies

- Hospital Pharmacies

- Retail Pharmacies

- Distribution Channel 4

- Distribution Channel 5

Based on the Geography:

- Istanbul

- Ankara

- Izmir

- Other

Regional Analysis

Istanbul

Istanbul holds the largest market share, accounting for approximately 40% of the total market. As the largest city in Turkey and an economic hub, Istanbul’s demand for diabetes drugs is fueled by its extensive healthcare infrastructure, high population density, and concentration of healthcare providers. The city’s large diabetic population, coupled with a rising prevalence of lifestyle diseases such as obesity and cardiovascular disorders, increases the need for advanced drug therapies. The availability of specialized medical centers and cutting-edge healthcare services further accelerates market growth in this region.

Ankara

Ankara, the capital of Turkey, represents the second-largest regional market for diabetes drugs, contributing about 25% to the overall market. The city’s well-established healthcare system, with both public and private healthcare institutions, plays a pivotal role in driving the demand for diabetes medications. In addition to a large population of diabetic patients, Ankara’s government institutions, including the Ministry of Health, actively promote awareness and disease management initiatives. As a result, the demand for both oral and injectable diabetes drugs is steadily increasing, particularly among the aging population and those at higher risk of Type 2 diabetes.

Izmir

Izmir, Turkey’s third-largest city, accounts for approximately 15% of the diabetes drugs market share. As a major port city and a key economic region, Izmir is home to a growing population of middle-aged and elderly individuals who are more susceptible to diabetes and related comorbidities. The region benefits from an expanding healthcare network, including clinics and hospitals dedicated to diabetes care. The demand for innovative therapies, such as GLP-1 receptor agonists and SGLT2 inhibitors, is on the rise due to an increasing focus on improving patient outcomes and reducing the burden of diabetes-related complications.

Other regions of Turkey contribute about 20% of the overall market share, with rural and less urbanized areas showing a growing demand for diabetes drugs. Although these regions have lower market shares compared to Istanbul, Ankara, and Izmir, the adoption of diabetes treatments is increasing due to enhanced access to healthcare services, government initiatives, and growing awareness about diabetes management. With ongoing improvements in healthcare infrastructure and distribution networks, the potential for market growth in these regions remains significant, particularly as the prevalence of diabetes continues to rise in rural and suburban areas.

Key Player Analysis

- Novo Nordisk A/S

- Sanofi

- Merck & Co., Inc.

- Eli Lilly and Company

- AstraZeneca

- Takeda Pharmaceutical Company Limited

- Boehringer Ingelheim International GmbH

- Novartis AG

- Johnson & Johnson Services, Inc.

- Bayer AG

- Company 11

- Company 12

- Company 13

- Company 14

Competitive Analysis

The competitive landscape of the Turkey diabetes drugs market is characterized by the presence of several leading multinational pharmaceutical companies, including Novo Nordisk A/S, Sanofi, Merck & Co., Inc., Eli Lilly and Company, AstraZeneca, Takeda Pharmaceutical Company Limited, Boehringer Ingelheim International GmbH, Novartis AG, Johnson & Johnson Services, Inc., and Bayer AG. These companies dominate the market with a wide range of diabetes treatment options, from traditional insulin products to advanced oral and injectable therapies. These companies are focused on delivering innovative solutions to improve patient outcomes, with an increasing emphasis on personalized medicine and precision therapies. The competition is driven by constant research and development to introduce new drug classes that offer better efficacy, fewer side effects, and improved convenience for patients. Additionally, the increasing adoption of biosimilars and cost-effective alternatives is creating a more price-competitive market. The companies also focus on expanding their presence through partnerships with healthcare providers and leveraging digital health technologies, such as continuous glucose monitoring and telemedicine, to optimize diabetes management. With regulatory challenges and price pressures, market players must navigate these complexities while ensuring broad patient access and treatment effectiveness. As the market evolves, companies are actively looking for opportunities to enhance their portfolios and strengthen their position in Turkey.

Recent Developments

- In March 2025, Novo Nordisk signed a deal worth up to $2 billion for the rights to UBT251, a new obesity and diabetes drug developed by United BioTechnology. The drug combines GLP-1, GIP, and glucagon to manage blood sugar and reduce hunger.

- In February 2025, Sanofi received FDA approval for MERILOG, the first rapid-acting insulin aspart biosimilar, to improve glycemic control in adults and pediatric patients with diabetes.

- In December 2024, JD Health began offering Merck’s GLUCOPHAGE XR (Reduce Mass) online in China, enhancing access to metformin hydrochloride extended-release tablets for type 2 diabetes patients.

- In December 2024, Torrent Pharma acquired three diabetes brands from Boehringer Ingelheim, including those with Empagliflozin, to strengthen its anti-diabetes portfolio

- In November 2024, AstraZeneca presented promising early data for its obesity pipeline, including AZD5004, an oral GLP-1 receptor blocker, at ObesityWeek 2024.

Market Concentration & Characteristics

The Turkey diabetes drugs market exhibits moderate concentration, with a mix of global pharmaceutical giants and local players driving competition. While multinational companies dominate, particularly in urban centers like Istanbul, Ankara, and Izmir, the market remains accessible to local and regional firms offering specialized products. This balance between global and local players creates a dynamic market environment, fostering innovation in drug therapies and diabetes care solutions. The market is characterized by a broad portfolio of treatment options, ranging from traditional insulin products to newer classes such as GLP-1 receptor agonists, SGLT2 inhibitors, and biosimilar therapies. The competition is primarily driven by factors such as the efficacy of treatments, patient adherence, cost-effectiveness, and technological integration. As demand for diabetes management solutions grows, companies are focusing on expanding their product offerings, improving patient access, and incorporating digital health technologies to enhance treatment outcomes and maintain market share.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Drug Class, Diabetes Types, Route of Administration, Technology, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Turkey diabetes drugs market is expected to experience steady growth driven by the increasing prevalence of diabetes.

- Advancements in drug development, particularly in GLP-1 receptor agonists and SGLT2 inhibitors, will continue to shape the treatment landscape.

- The demand for biosimilar insulin products will rise as healthcare costs remain a significant concern.

- A shift towards personalized medicine will lead to more tailored treatment options for patients.

- Digital health solutions, including continuous glucose monitoring and telemedicine, will become more integrated with diabetes drug therapies.

- The aging population in Turkey will contribute to higher demand for diabetes treatments.

- Growing awareness of diabetes management and early diagnosis will increase drug adoption.

- Increased government support for healthcare infrastructure and diabetes care will enhance access to treatments.

- Competition among global and local pharmaceutical companies will intensify, encouraging innovation and cost-effective options.

- Regulatory reforms are expected to further improve market access and streamline drug approvals.