| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Scar Treatment Market Size 2024 |

USD 26,250.6 million |

| Scar Treatment Market, CAGR |

9.33% |

| Scar Treatment Market Size 2032 |

USD 53,481.0 million |

Market Overview

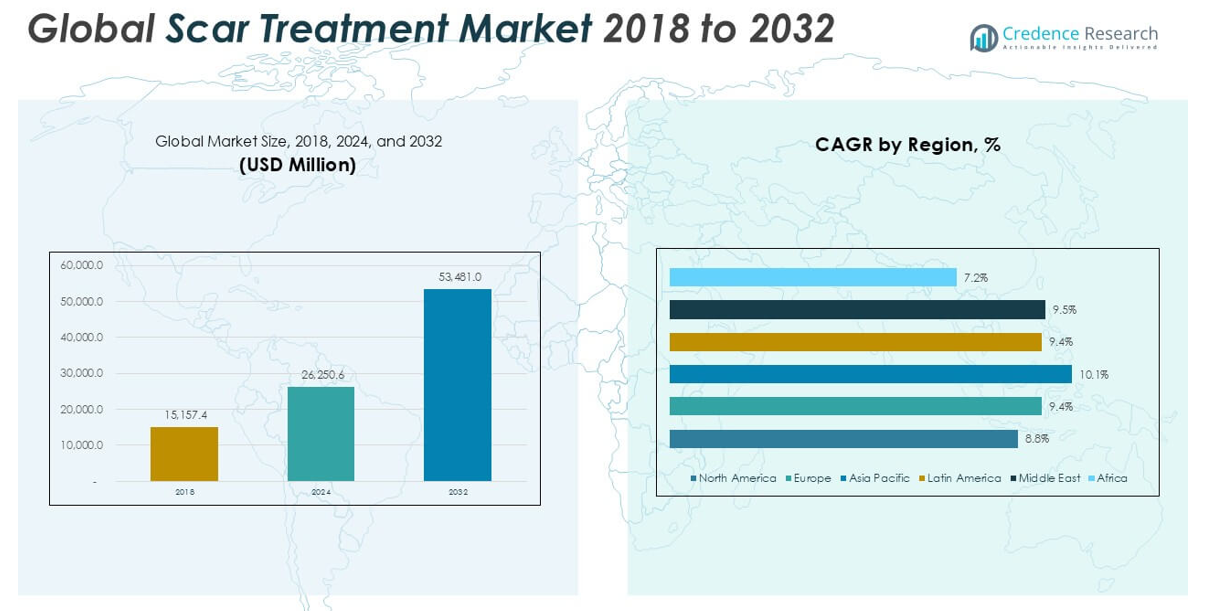

The Scar Treatment market size was valued at USD 15,157.4 million in 2018 and USD 26,250.6 million in 2024, and is anticipated to reach USD 53,481.0 million by 2032, at a CAGR of 9.33% during the forecast period.

The scar treatment market is driven by key players such as Smith & Nephew plc, Lumenis, Sonoma Pharmaceuticals, Inc., Mölnlycke Health Care AB, Scarheal Inc., CCA Industries, Inc., Cynosure, Inc., Merz GMBH & Co KGAA, Valeant Pharmaceuticals International Inc., and Hologic Inc. These companies focus on expanding their product portfolios through technological advancements, mergers, and acquisitions to maintain competitive advantage. North America leads the global scar treatment market, holding the largest market share of 31.2% in 2024, supported by well-established healthcare infrastructure, high patient awareness, and a strong presence of major players. Asia Pacific follows closely, demonstrating the fastest growth driven by rising healthcare investments and increasing demand for aesthetic procedures

Market Insights

- The global scar treatment market was valued at USD 26,250.6 million in 2024 and is expected to reach USD 53,481.0 million by 2032, growing at a CAGR of 9.33% during the forecast period.

- The market is driven by increasing demand for aesthetic procedures, rising incidence of skin-related conditions, and growing awareness of scar management, particularly among the younger population.

- Non-invasive scar treatment options, especially topical products like creams, dominate the market due to their ease of use and affordability, while atrophic scars represent the largest scar type segment.

- The market is highly competitive, with key players focusing on product innovation, partnerships, and expanding their geographic footprint to capture larger market shares.

- North America leads with a 31.2% share in 2024, followed by Asia Pacific at 25.9%, with the latter showing the fastest growth; however, high treatment costs and limited efficacy for complex scars may restrain market expansion.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Product:

The topical products segment dominated the scar treatment market and accounted for the largest market share in 2024. Among topical products, creams held a significant share due to their ease of application, affordability, and wide availability across both prescription and over-the-counter channels. The demand for topical creams is driven by their non-invasive nature, minimal side effects, and growing consumer preference for self-care solutions. Additionally, increasing awareness about scar management and advancements in formulation, such as the inclusion of natural ingredients and improved absorption technologies, have further boosted the demand for topical scar treatment products.

- For instance, Sonoma Pharmaceuticals reported that its Microcyn® Technology, integrated into over 55 commercial products, has demonstrated enhanced scar healing with significant reductions in inflammation within 7 days of application.

By Scar Type

The atrophic scars segment emerged as the leading category, holding the largest market share in 2024. This dominance is primarily due to the high prevalence of acne-related atrophic scars, particularly among the adolescent and young adult population. Increasing consumer demand for aesthetic improvement and the psychological impact of visible facial scars significantly drive the adoption of scar treatments targeting atrophic scars. Growing awareness of available treatment options, rising disposable incomes, and increasing access to dermatological care, especially in emerging economies, further contribute to the expansion of this segment.

- For instance, Cynosure’s PicoSure® picosecond laser achieved more than 50% physician-rated improvement in acne scar appearance in 77 out of 100 patients after three sessions, and physician satisfaction reached 97% at one-month follow-up.

By End User

Hospitals accounted for the largest market share among end users in the scar treatment market in 2024. The dominance of this segment is driven by the availability of advanced treatment options, such as laser therapies and injectable procedures, which are typically performed in hospital settings. Additionally, hospitals provide comprehensive care with skilled dermatologists and access to multi-disciplinary treatment approaches, increasing patient preference for these facilities. The rising number of trauma and burn cases requiring scar management and the expansion of hospital infrastructure globally have further supported the growth of this segment.

Market Overview

Increasing Demand for Aesthetic Procedures

The growing demand for aesthetic improvement is a major driver propelling the scar treatment market. Rising consumer awareness about appearance enhancement, coupled with the psychological impact of visible scars, is encouraging individuals to seek effective treatment options. Both surgical and non-invasive procedures are gaining popularity, particularly among younger populations. Additionally, the rise of social media and growing beauty consciousness are further amplifying this demand. The increasing affordability and accessibility of scar treatment products and services also contribute to the expanding market size.

- For instance, Smith & Nephew’s ReCell Spray‑On Skin System showed complete epithelialization within 13±2 days in 42 burn patients in a comparative study, significantly reducing donor site morbidity and procedure complexity.

Technological Advancements in Scar Treatment

Continuous technological advancements in scar treatment, including innovations in laser therapy, topical formulations, and injectable products, are significantly boosting market growth. The development of more effective and minimally invasive laser systems, silicone-based therapies, and advanced topical agents with faster healing properties has improved treatment outcomes. These innovations are enhancing patient satisfaction, reducing treatment time, and increasing procedural safety. Furthermore, the integration of combination therapies and personalized treatment plans is providing new avenues for scar management, driving the adoption of these solutions across healthcare settings.

- For instance, Lumenis’ UltraPulse® CO₂ laser using SCAAR FX™ mode delivers ablation depths up to 4 mm in a single pulse, enabling effective restructuring of dense scar tissues and improved mobility after only a few sessions.

Rising Incidence of Skin-related Conditions and Trauma

The increasing prevalence of skin conditions such as acne, burns, and surgical interventions is contributing to a higher demand for scar treatment solutions. Growing rates of road accidents, burn injuries, and post-surgical scarring across both developed and emerging markets are fueling market growth. Additionally, the rising burden of chronic wounds and the surge in cosmetic surgeries, particularly in urban areas, further escalate the need for scar management products and services. This growing patient pool is expected to sustain long-term demand in the scar treatment market.

Key Trends & Opportunities

Growing Popularity of Non-Invasive Treatments

The rising preference for non-invasive and minimally invasive scar treatment options presents a significant market opportunity. Consumers increasingly opt for topical products, silicone sheets, and laser therapies that offer faster recovery with minimal discomfort. The availability of over-the-counter scar treatment solutions further enhances accessibility, supporting market expansion. This trend is also encouraging manufacturers to invest in developing innovative, user-friendly products that deliver effective results without the need for complex medical procedures, making scar treatment more mainstream.

- For instance, Smith & Nephew’s ALLEVYN LIFE silicone gel sheets demonstrated significant scar size reduction within 12 weeks of continuous use in over 500 patient applications worldwide.

Expansion in Emerging Markets

Emerging economies present lucrative growth opportunities for the scar treatment market due to improving healthcare infrastructure, rising disposable incomes, and increasing awareness of aesthetic treatments. Countries in Asia-Pacific, Latin America, and the Middle East are witnessing a growing demand for both surgical and non-surgical scar treatments. The expanding medical tourism sector, coupled with the presence of cost-effective treatment options, is further attracting patients to these regions. Additionally, government initiatives to enhance healthcare accessibility are expected to support the future growth of the scar treatment market in these areas.

- For instance, Lumenis Ltd. has successfully installed over 1,500 laser therapy systems across India, Thailand, and Brazil, offering minimally invasive scar treatments in both urban and semi-urban healthcare centers.

Key Challenges

High Treatment Costs

One of the major challenges limiting the growth of the scar treatment market is the high cost associated with advanced procedures such as laser therapy and injectable treatments. These high costs often restrict access for middle- and low-income populations, particularly in developing regions. Although topical products offer a more affordable alternative, advanced treatments that deliver faster and more noticeable results remain financially inaccessible for many. This pricing barrier continues to pose a constraint on the widespread adoption of premium scar treatment solutions.

Limited Efficacy for Certain Scar Types

Scar treatment solutions often exhibit limited efficacy when dealing with severe or complex scar types, such as keloids and contracture scars. These scars typically require prolonged treatment cycles and may not respond well to conventional therapies. Patients with resistant scars frequently experience dissatisfaction due to incomplete results or recurrence, which can undermine confidence in available treatment options. This challenge highlights the need for continued research and development to improve treatment effectiveness and address the unmet needs in managing difficult scar types.

Risk of Side Effects and Post-Treatment Complications

Despite advancements in scar treatment technologies, potential side effects and post-treatment complications remain key concerns. Laser therapies and injectables can sometimes cause skin irritation, pigmentation changes, or additional scarring if not performed correctly. These risks deter some patients from pursuing treatment, particularly in regions where skilled dermatological expertise may be limited. The fear of adverse outcomes may also lead to treatment delays or preference for less effective but safer options, thus impacting the overall growth potential of the market.

Regional Analysis

North America

In 2024, North America dominated the scar treatment market, accounting for the largest market share of approximately 31.2%, with a market size of USD 8,191.67 million, up from USD 4,867.03 million in 2018. The region is expected to further grow to USD 16,044.31 million by 2032, registering a CAGR of 8.8% during the forecast period. The growth is driven by the increasing demand for advanced scar treatment procedures, high consumer awareness, and widespread availability of innovative products. The strong presence of key market players and well-established healthcare infrastructure also supports market expansion in North America.

Europe

Europe held a significant share of 21.8% in the global scar treatment market in 2024, with a market size of USD 5,737.62 million, rising from USD 3,301.27 million in 2018. The market is projected to reach USD 11,744.43 million by 2032, expanding at a CAGR of 9.4%. The region’s growth is attributed to the increasing adoption of non-invasive treatments, rising prevalence of skin-related conditions, and favorable reimbursement policies. Additionally, the growing emphasis on aesthetic appearance and the rapid adoption of advanced laser technologies are fueling the demand for scar treatment across Europe.

Asia Pacific

The Asia Pacific region captured a substantial market share of 25.9% in 2024, with the market valued at USD 6,817.64 million, up from USD 3,756.00 million in 2018. The region is expected to grow to USD 14,739.37 million by 2032, exhibiting the highest CAGR of 10.1% among all regions. Rapid urbanization, increasing disposable incomes, and growing awareness regarding scar treatment options are the primary drivers. The rising incidence of road accidents, burns, and skin disorders, combined with a flourishing medical tourism industry, particularly in countries like India, China, and Thailand, is supporting market growth.

Latin America

Latin America accounted for 11.3% of the scar treatment market share in 2024, reaching USD 2,963.31 million, a considerable rise from USD 1,705.20 million in 2018. The market is anticipated to grow to USD 6,064.75 million by 2032, progressing at a CAGR of 9.4%. The regional growth is driven by increasing consumer awareness, improving healthcare access, and rising demand for aesthetic and cosmetic procedures. Countries such as Brazil and Mexico are key contributors, with a growing number of dermatological clinics and rising interest in both surgical and non-surgical scar treatment solutions.

Middle East

The Middle East scar treatment market was valued at USD 1,429.91 million in 2024, up from USD 818.50 million in 2018, holding a 5.4% market share. The market is projected to reach USD 2,946.80 million by 2032, growing at a CAGR of 9.5%. Rising disposable incomes, expanding healthcare infrastructure, and an increasing focus on personal appearance are key factors driving market growth. The growing popularity of cosmetic and laser procedures and a gradual rise in skin-related conditions such as burns and acne scars further contribute to the increasing demand for scar treatment in this region.

Africa

Africa represented the smallest share of 4.2% in the global scar treatment market in 2024, with a market value of USD 1,110.40 million, increasing from USD 709.36 million in 2018. The market is projected to reach USD 1,941.36 million by 2032, expanding at a CAGR of 7.2%. Market growth in Africa is primarily supported by improving healthcare access, rising awareness of scar treatment options, and a growing population seeking cosmetic improvements. However, limited availability of advanced technologies and high treatment costs continue to pose challenges, restricting faster market penetration in the region.

Market Segmentations:

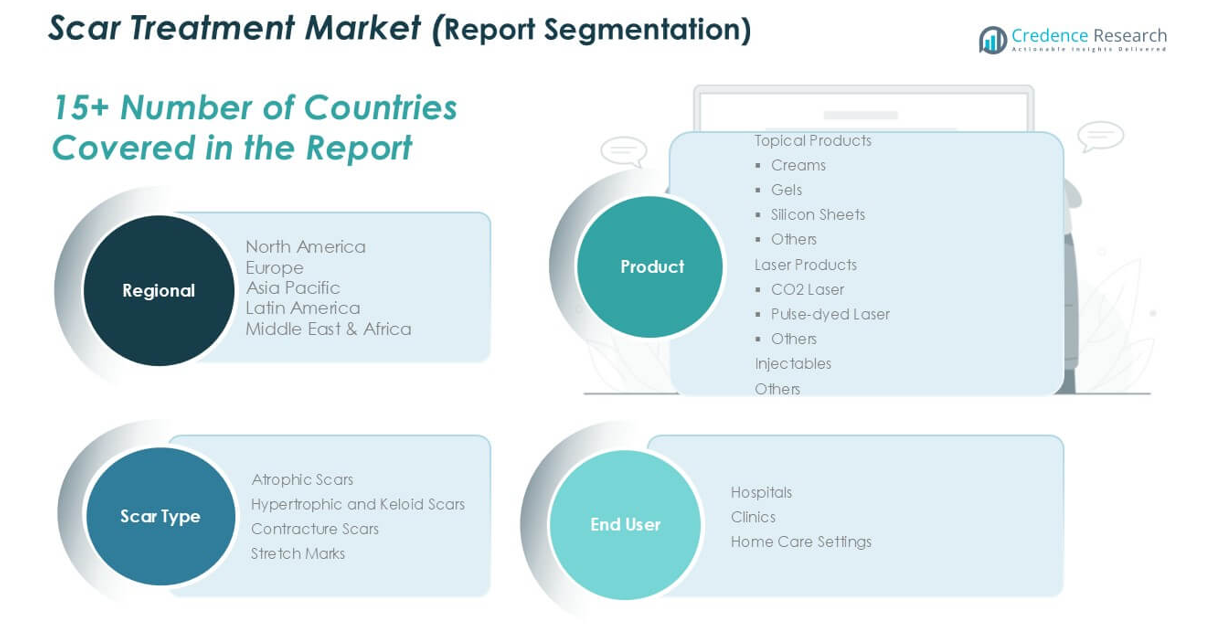

By Product

- Topical Products

- Creams

- Gels

- Silicon Sheets

- Others

- Laser Products

- CO2 Laser

- Pulse-dyed Laser

- Others

- Injectables

- Others

By Scar Type

- Atrophic Scars

- Hypertrophic and Keloid Scars

- Contracture Scars

- Stretch Marks

- Others

By End User

- Hospitals

- Clinics

- Home Care Settings

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The scar treatment market is highly competitive, with key players focusing on product innovation, strategic partnerships, and geographic expansion to strengthen their market position. Companies such as Smith & Nephew plc, Lumenis, Sonoma Pharmaceuticals, Inc., and Mölnlycke Health Care AB lead the market with a diverse portfolio of advanced scar management solutions, including topical products, laser treatments, and silicone-based therapies. Competitive strategies commonly include the development of technologically advanced and minimally invasive products to meet the growing demand for effective and user-friendly treatments. Mergers, acquisitions, and collaborations are also prominent as companies aim to broaden their product offerings and expand their global reach. Additionally, players are investing in research and development to introduce products with improved efficacy and faster healing times. Increasing consumer preference for aesthetic improvements continues to drive competition, prompting manufacturers to focus on both product quality and affordability to capture a larger share in this rapidly evolving market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Smith & Nephew plc.

- Lumenis

- Sonoma Pharmaceuticals, Inc.

- Scarheal Inc.

- CCA Industries, Inc.

- Cynosure, Inc.

- Mölnlycke Health Care AB

- Merz GMBH & Co KGAA

- Valeant Pharmaceuticals International Inc.

- Hologic Inc.

Recent Developments

- In March 2024, the U.S. FDA approved Rezdiffra (resmetirom), which is used for treating adults with NASH (noncirrhotic non-alcoholic steatohepatitis) with moderate or advanced liver scarring.

- In January 2023, Sonoma Pharmaceuticals, Inc. introduced a range of go-to office products specifically designed for skin care professionals.

- In August 2023, Sofwave Medical Ltd. announced FDA clearance of its Precise SUPERB Applicator for the treatment of acne scars. This newest approval adds yet another treatment indication to Sofwave’s SUPERB device, which can now be used to improve acne scars, facial lines and wrinkles.

- In May 2024, Nuance Medical has strategically acquired Biocorneum, a silicone gel scar treatment brand previously owned by Sientra. This acquisition enhances Nuance’s portfolio, integrating Biocorneum’s strong healthcare sector presence with Biodermis’ comprehensive silicone scar management solutions. The move solidifies Nuance’s position in the growing scar treatment market, expanding its product offerings.

- In April 2025, Bausch Health unveiled Solta Medical’s Fraxel FTX™ dual-wavelength fractional laser, promising lower downtime and improved scar resolution.

- In April 2025, Galderma introduced ALASTIN Restorative Skin Complex with Next Generation TriHex Technology, enhancing collagen and elastin production in post-procedure care regimens.

Market Concentration & Characteristics

The Scar Treatment Market shows a moderately fragmented structure with a mix of established global players and emerging regional participants. It features high competition, driven by continuous product innovation, technological advancements, and expanding consumer demand for aesthetic solutions. Companies compete by offering diverse treatment options, including topical products, laser therapies, and injectable solutions. Product differentiation and pricing strategies significantly influence market positioning. The market benefits from increasing patient awareness and the growing importance of personal appearance. It responds quickly to advancements in dermatology and consumer preferences for non-invasive treatments. Strong distribution networks and strategic partnerships support wider market penetration.

Report Coverage

The research report offers an in-depth analysis based on Product, Scar Type, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The scar treatment market is expected to grow steadily, driven by increasing demand for aesthetic and non-invasive solutions.

- Topical products, especially creams, will continue to dominate due to their accessibility and consumer preference for home-based care.

- Laser therapies are projected to gain higher adoption with advancements in precision and safety.

- Rising awareness about scar management in emerging economies will create significant growth opportunities.

- Hospitals will remain the leading end-user segment, supported by the availability of advanced treatment options.

- The market will benefit from continuous product innovation focused on faster healing and improved effectiveness.

- Increasing cosmetic consciousness among younger populations will support consistent market demand.

- Companies will invest more in developing combination therapies for complex scar types.

- Partnerships and mergers will strengthen global distribution channels and product reach.

- The Asia Pacific region is expected to lead future growth due to expanding healthcare access and rising medical tourism.